North America Luxury Goods Market Outlook to 2030

Region:North America

Author(s):Shreya Garg

Product Code:KROD8220

December 2024

88

About the Report

North America Luxury Goods Market Overview

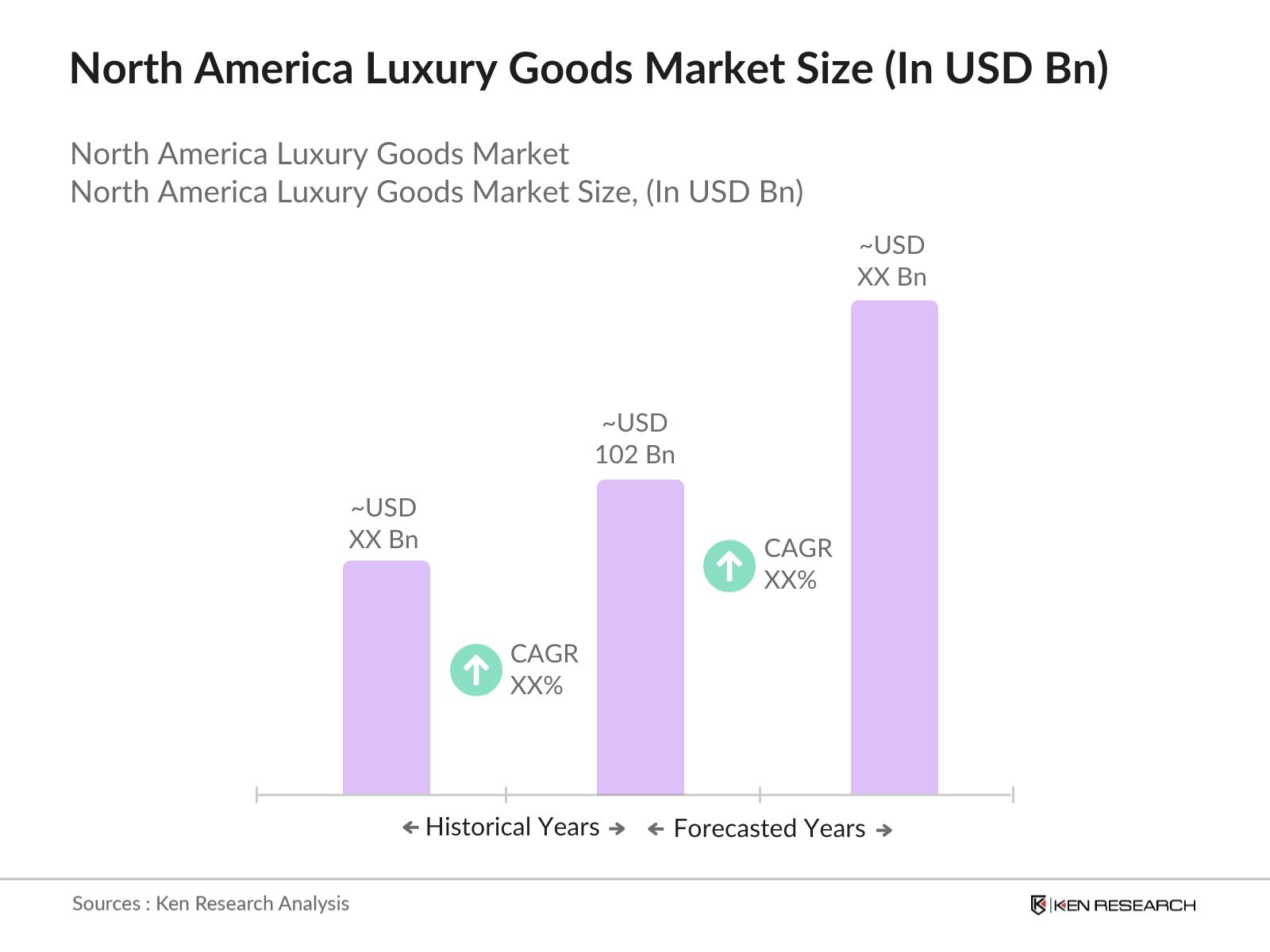

- The North America luxury goods market is valued at USD 102 billion, based on a detailed five-year historical analysis. This market is driven by a rise in disposable incomes, a growing class of high-net-worth individuals, and increased spending on premium goods. The appeal of luxury brands is further amplified by the cultural integration of luxury into aspirational living, amplified by social medias influence on consumer behavior and the expansion of digital sales channels for luxury products. This has set a foundation for consistent growth in the luxury sector.

- The United States is the dominant region in North America's luxury goods market, primarily due to its large consumer base with high disposable income levels and a prominent culture of luxury consumption. Cities like New York and Los Angeles are major hubs, hosting flagship stores for globally recognized luxury brands and being prime locations for affluent consumers and tourists. Canada also holds a significant share, particularly in metropolitan areas like Toronto, where there is a rising demand for luxury products among high-net-worth individuals and a growing interest in sustainable luxury goods.

- Luxury goods in North America are subject to stringent import and export regulations, impacting pricing and supply chains. The U.S. Customs and Border Protection agency enforces compliance, with penalties for non-compliance reaching over $300 million in 2023 alone. This regulatory landscape requires luxury brands to manage complex logistics, ensuring that all products meet North American compliance standards, impacting operational costs and pricing strategies

North America Luxury Goods Market Segmentation

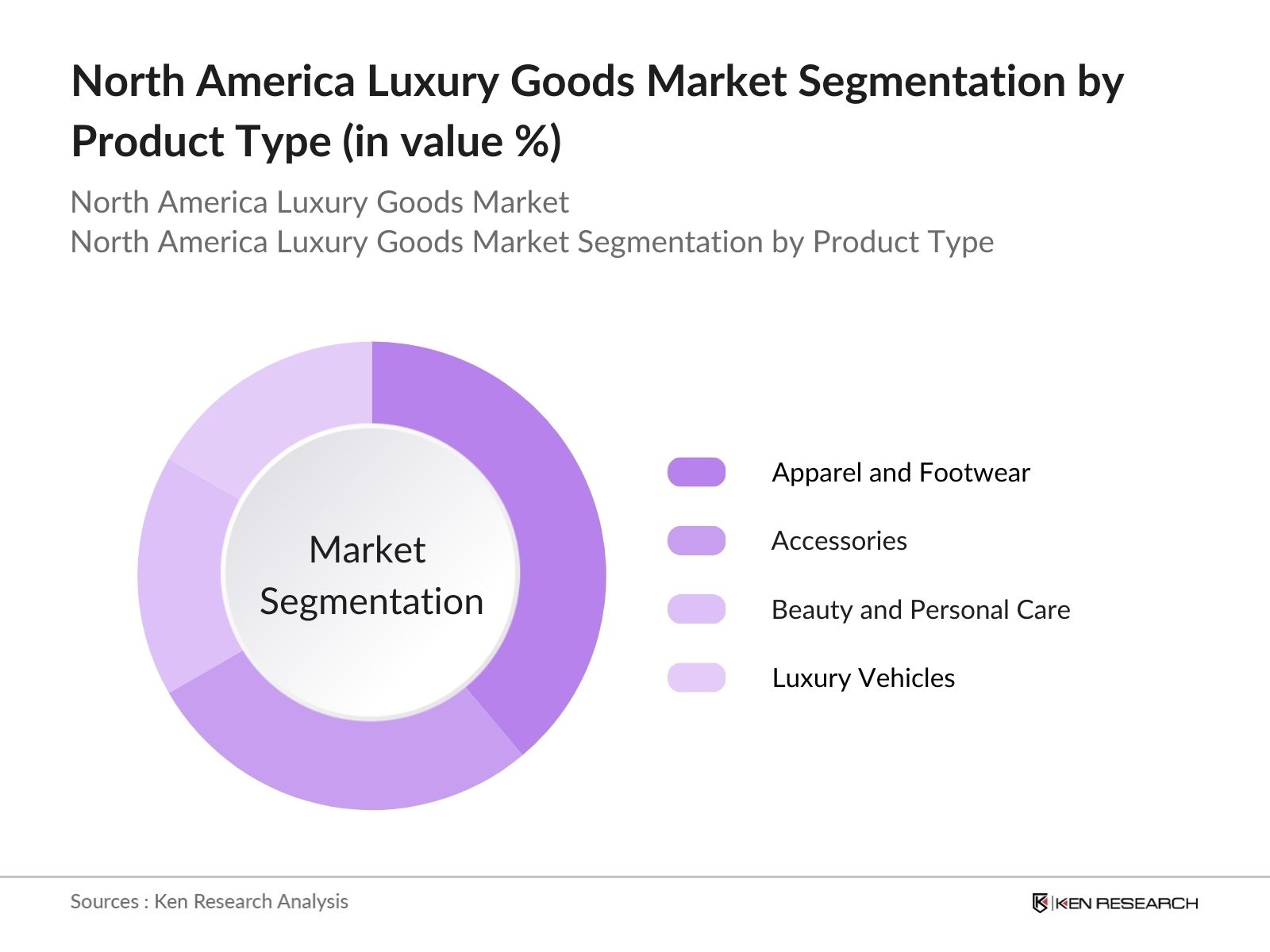

By Product Type: The market is segmented by product type into apparel and footwear, accessories, beauty and personal care, luxury vehicles, and home and lifestyle goods. Recently, luxury apparel and footwear hold a dominant market share in North America, supported by established brands like Gucci and Louis Vuitton, which have fostered high brand loyalty. These products enjoy substantial demand among younger, affluent consumers, driven by exclusive designs and limited-edition releases that heighten their appeal in the market.

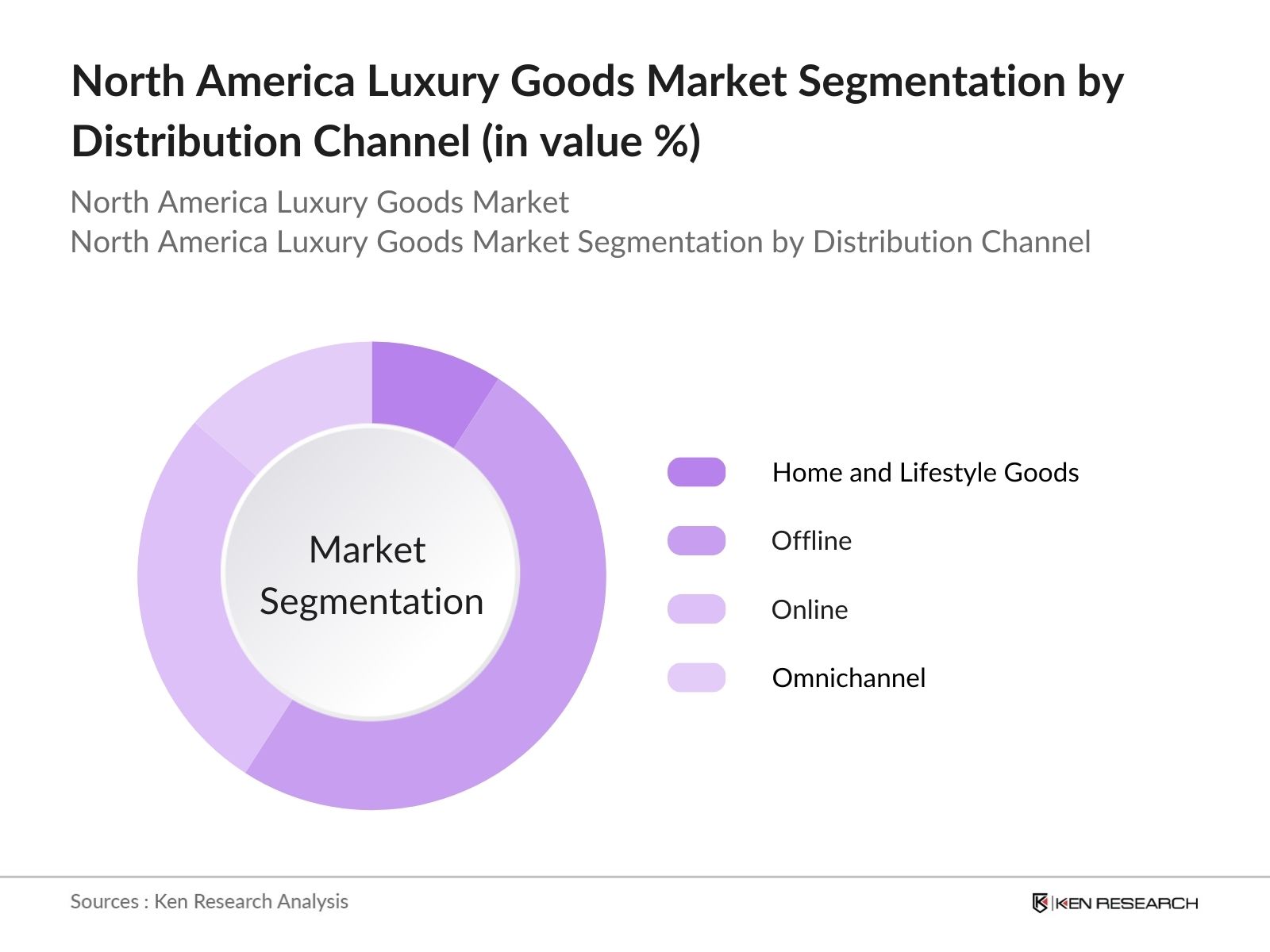

By Distribution Channel: The distribution channels are categorized into offline, online, and omnichannel. Offline channels, particularly luxury brand-owned flagship stores, continue to lead in market share. The immersive shopping experiences and personalized customer service offered at these physical locations strengthen brand identity and loyalty among consumers, which remains a crucial factor in the appeal of luxury goods despite the rise of e-commerce options.

North America Luxury Goods Market Competitive Landscape

The North American luxury goods market is characterized by strong competition, with key players dominating through brand equity, extensive retail presence, and digital strategies. Luxury brands like LVMH and Chanel capitalize on brand heritage, exclusivity, and a robust omnichannel approach to maintain market positioning. High consumer loyalty and brand exclusivity have driven these brands to the forefront of the market.

|

Company |

Establishment Year |

Headquarters |

Market Focus |

Product Range |

Revenue (USD Mn) |

E-commerce Adoption |

Sustainability Initiatives |

Regional Presence |

|

LVMH |

1987 |

Paris, France |

||||||

|

Chanel |

1910 |

Paris, France |

||||||

|

Richemont |

1988 |

Geneva, Switzerland |

||||||

|

Gucci (Kering Group) |

1921 |

Florence, Italy |

||||||

|

Rolex |

1905 |

Geneva, Switzerland |

North America Luxury Goods Industry Analysis

Growth Drivers

- Increase in Disposable Income: The increase in disposable income across North America has significantly impacted the luxury goods market, with notable spending trends among high-income households. In the U.S., data from the Bureau of Economic Analysis indicates a 2.6% increase in real disposable personal income from 2022 to 2023, adding substantial purchasing power for luxury goods. This surge is driven by economic stability in regions like Canada and the U.S., where individual incomes have shown upward mobility, especially in the top 20% income bracket, which controls approximately 50% of total spending.

- Rise in High-Net-Worth Individuals: North America continues to host a growing base of high-net-worth individuals (HNWIs), intensifying demand for luxury goods. The U.S. Department of Treasury reports over 23 million HNWIs in 2023, driven by gains in the financial and technology sectors, which contributed over $3 trillion to individual wealth last year alone. The impact is apparent in luxury spending behaviors, with these individuals favoring high-end brands for exclusivity and social status. Canada has also seen HNWI growth, further solidifying North America as a core luxury market region.

- Digital Penetration: Luxury retail is embracing e-commerce, accelerated by the digital readiness in North America. The International Telecommunication Union (ITU) notes that in 2023, 92% of Americans and 90% of Canadians had internet access, allowing luxury brands to leverage e-commerce for reaching high-income consumers efficiently. The U.S. Census Bureau reports e-commerce sales of $1.03 trillion for 2023, marking a clear shift toward online luxury retail, especially in urban centers where digital transactions for high-end goods surged by 8.9% from 2022 to 2023.

Market Challenges

- Counterfeit Product Proliferation: Counterfeit luxury products pose a challenge, with U.S. Customs and Border Protection seizing over $1.1 billion worth of counterfeit goods in 2023 alone, a significant portion of which were luxury items. The influx of fake products, primarily from China and Southeast Asia, has pressured luxury brands to intensify anti-counterfeit measures. This issue not only affects brand reputation but also translates to substantial economic losses for legitimate luxury brands.

- Economic Downturn Impact: Economic fluctuations in North America can hinder luxury spending, with recent inflationary pressures impacting discretionary income levels. According to the Bureau of Economic Analysis, U.S. inflation reached 5.5% in 2023, reducing disposable income by 0.9% across middle-income households. This reduction influences luxury brands, as more consumers limit spending on non-essential high-end items during economic uncertainty.

North America Luxury Goods Market Future Outlook

The North America luxury goods market is poised for steady growth, driven by expanding disposable incomes, sustained demand from high-net-worth individuals, and the rise of eco-conscious luxury preferences. In addition, technological integration into luxury shopping, such as virtual stores and augmented reality for enhanced consumer experiences, is expected to redefine the market dynamics. The growing trend towards personalization and sustainable luxury practices is likely to shape consumer preferences in the years ahead.

Future Market Opportunities

- Expanding Online Luxury Shopping Platforms: Online luxury shopping is booming in North America, with the U.S. Census Bureau reporting a 9% growth in high-end e-commerce sales in 2023. Enhanced digital infrastructure, especially in urban hubs, facilitates this trend, allowing luxury brands to expand their reach beyond brick-and-mortar. Digital luxury sales are further propelled by the ease of cross-border transactions within North America, setting a foundation for continued growth in online luxury shopping.

- Sustainable and Ethical Luxury Demand: With a clear shift toward ethical and sustainable products, luxury brands now have a substantial opportunity to cater to eco-conscious consumers. A recent U.S. Environmental Protection Agency report shows that 74% of North American luxury consumers prefer brands with transparent sustainability practices, creating a growing niche for ethically produced luxury items. This aligns with the current demand for eco-friendly materials in luxury fashion and accessories, supporting market expansion among conscious consumers.

Scope of the Report

|

Product Category |

Apparel and Footwear Accessories (Watches, Jewelry) Beauty and Personal Care Products Luxury Vehicles Home and Lifestyle Goods |

|

Consumer Demographics |

High-Net-Worth Individuals Millennials Generation Z Digital Natives |

|

Distribution Channel |

Offline (Flagship Stores, Department Stores) Online (Brand Websites, E-commerce Platforms) Omnichannel Sales |

|

Region |

United States Canada Mexico Regional Hubs (Key Cities) |

|

Price Range |

Entry-Level Luxury Mid-Tier Luxury High-End Luxury Ultra-Luxury Segment |

Products

Key Target Audience

High-Net-Worth Individuals

Investor and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., Department of Commerce, Federal Trade Commission)

Luxury Retailers and Boutiques

Online Luxury Platforms and E-commerce Providers

Hospitality Chains and Luxury Hotels

Digital and Social Media Marketing Firms

Environmental Advocacy Groups (focused on sustainable luxury)

Companies

Major Players

LVMH

Chanel

Richemont

Gucci (Kering Group)

Rolex

Tiffany & Co.

Prada Group

Burberry

Tesla, Inc.

Cartier

Herms

Ralph Lauren

Estee Lauder

Bvlgari

Ferrari

Table of Contents

North America Luxury Goods Market Overview

Definition and Scope

Market Taxonomy

Growth Rate and Forecasts

Overview of Market Segmentation

North America Luxury Goods Market Size (in USD Mn)

Historical Market Size Analysis

Year-on-Year Growth Analysis

Key Developments and Milestones in Market

North America Luxury Goods Market Analysis

Growth Drivers

Increase in Disposable Income

Rise in High-Net-Worth Individuals

Digital Penetration (E-commerce Dynamics)

Influence of Social Media on Brand Perception

Market Challenges

Counterfeit Product Proliferation

Economic Downturn Impact

High Import Duties

Evolving Consumer Preferences

Opportunities

Expanding Online Luxury Shopping Platforms

Sustainable and Ethical Luxury Demand

Cross-Border E-commerce Expansion

Trends

Demand for Limited-Edition and Customized Products

Growth in Pre-Owned Luxury Market

Shift towards Experiential Luxury (Travel, Wellness)

Government Regulations

Import and Export Compliance

Counterfeit Product Prevention Measures

Sustainable Practice Regulations

North America Luxury Goods Market Segmentation

By Product Category (in Value %)

Apparel and Footwear

Accessories (Watches, Jewelry)

Beauty and Personal Care Products

Luxury Vehicles

Home and Lifestyle Goods

By Consumer Demographics (in Value %)

High-Net-Worth Individuals

Millennials

Generation Z

Digital Natives

By Distribution Channel (in Value %)

Offline (Flagship Stores, Department Stores)

Online (Brand Websites, E-commerce Platforms)

Omnichannel Sales

By Region (in Value %)

United States

Canada

Mexico

Regional Hubs (Key Cities)

By Price Range (in Value %)

Entry-Level Luxury

Mid-Tier Luxury

High-End Luxury

Ultra-Luxury Segment

North America Luxury Goods Market Competitive Analysis

Detailed Profiles of Major Companies

LVMH

Kering

Richemont

Estee Lauder

Ralph Lauren

Chanel

Gucci

Burberry

Prada Group

Tesla, Inc.

Rolex

Tiffany & Co.

Herms

Bvlgari

Cartier

Cross Comparison Parameters (Revenue, Headquarters Location, Market Segment Focus, Product Innovation Score, Digital Transformation Score, Regional Presence, Corporate Social Responsibility Initiatives, Employee Size)

Market Share Analysis

Strategic Initiatives and Investments

Mergers and Acquisitions

Capital Expenditure Trends

Partnerships and Collaborations

North America Luxury Goods Market Regulatory Framework

Import and Export Duties on Luxury Goods

Advertising Standards and Consumer Protection

Counterfeit Prevention Policies

Regulations on Sustainable Luxury Practices

Future Market Size of North America Luxury Goods Market (in USD Mn)

Forecasted Market Size

Drivers of Future Growth

Future Segmentation of North America Luxury Goods Market

By Product Category

By Consumer Demographics

By Distribution Channel

By Region

By Price Range

North America Luxury Goods Market Analysts Recommendations

TAM/SAM/SOM Analysis

Brand Loyalty Programs and Retention Strategies

Marketing and Digital Campaign Insights

Opportunity for White Space and Untapped Markets

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The research process starts with constructing an ecosystem map of all stakeholders in the North America luxury goods market. This initial step employs comprehensive desk research using secondary databases to identify critical variables such as demand drivers, consumer demographics, and distribution channels.

Step 2: Market Analysis and Construction

The second phase involves compiling and analyzing historical data related to market penetration and sales distribution. This includes examining sales channels, brand positioning, and revenue streams, focusing on how these elements shape overall market dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed based on initial data and validated through consultations with industry experts. These interviews provide insights on consumer behavior, market challenges, and emerging trends, enhancing the reliability of the gathered data.

Step 4: Research Synthesis and Final Output

The final phase synthesizes data and findings from primary and secondary sources, providing a comprehensive and validated report. This phase involves close collaboration with luxury brands to gather insights on consumer engagement, sales strategies, and product preferences.

Frequently Asked Questions

01 How big is the North America luxury goods market?

The North America luxury goods market is valued at USD 102 billion, with demand driven by a combination of disposable income growth, high-net-worth individuals, and luxury lifestyle integration.

02 What are the challenges in the North America luxury goods market?

Challenges in the North America luxury goods market include counterfeit product issues, high tariffs on imports, and a need for constant innovation to appeal to changing consumer preferences in luxury.

03 Who are the major players in the North America luxury goods market?

Key players in the North America luxury goods market include LVMH, Chanel, Gucci (Kering Group), Rolex, and Cartier. These brands dominate due to their brand heritage, extensive product portfolios, and strong distribution networks.

04 What factors drive growth in the North America luxury goods market?

Growth in the North America luxury goods market is fueled by rising disposable incomes, increased digital penetration in luxury sales, and consumer interest in sustainability and high-quality experiences.

05 Which distribution channel holds the largest share in the North America luxury goods market?

Offline channels, particularly flagship stores, hold the largest market share in the North America luxury goods market due to their personalized shopping experience, which is essential in luxury retail.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.