North America Maltodextrin Market Outlook to 2030

Region:North America

Author(s):Yogita Sahu

Product Code:KROD6813

Region:North America

Author(s):Yogita Sahu

Product Code:KROD6813

December 2024

91

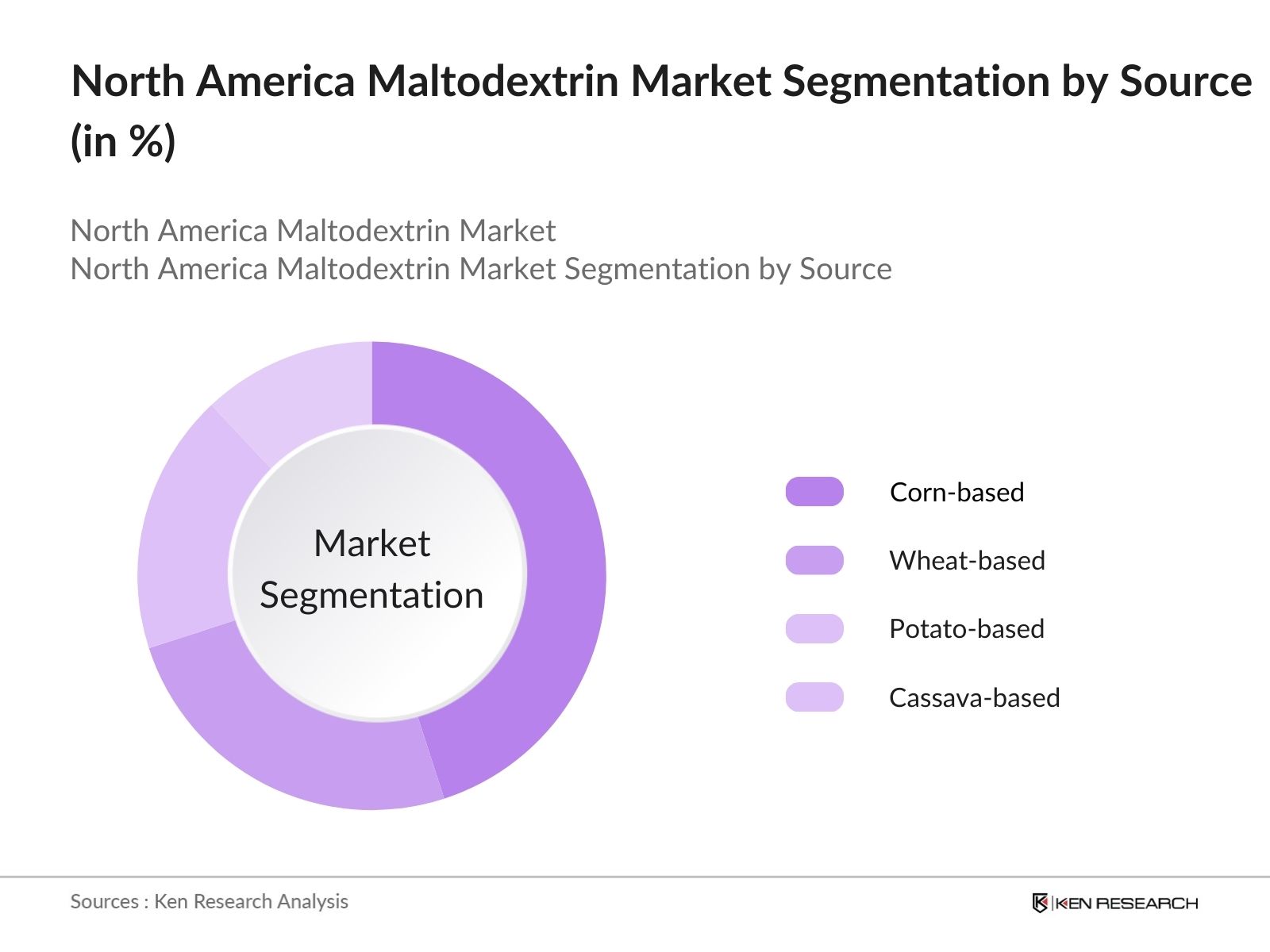

By Source: The market in North America is segmented by source into corn-based, wheat-based, potato-based, and cassava-based. Corn-based maltodextrin currently dominates the market due to its widespread availability and cost-effectiveness. This source is highly favored by manufacturers because of the robust corn production in the United States, making it a reliable and affordable option. Corn-based maltodextrin holds a significant share in various applications like food, beverages, and pharmaceuticals.

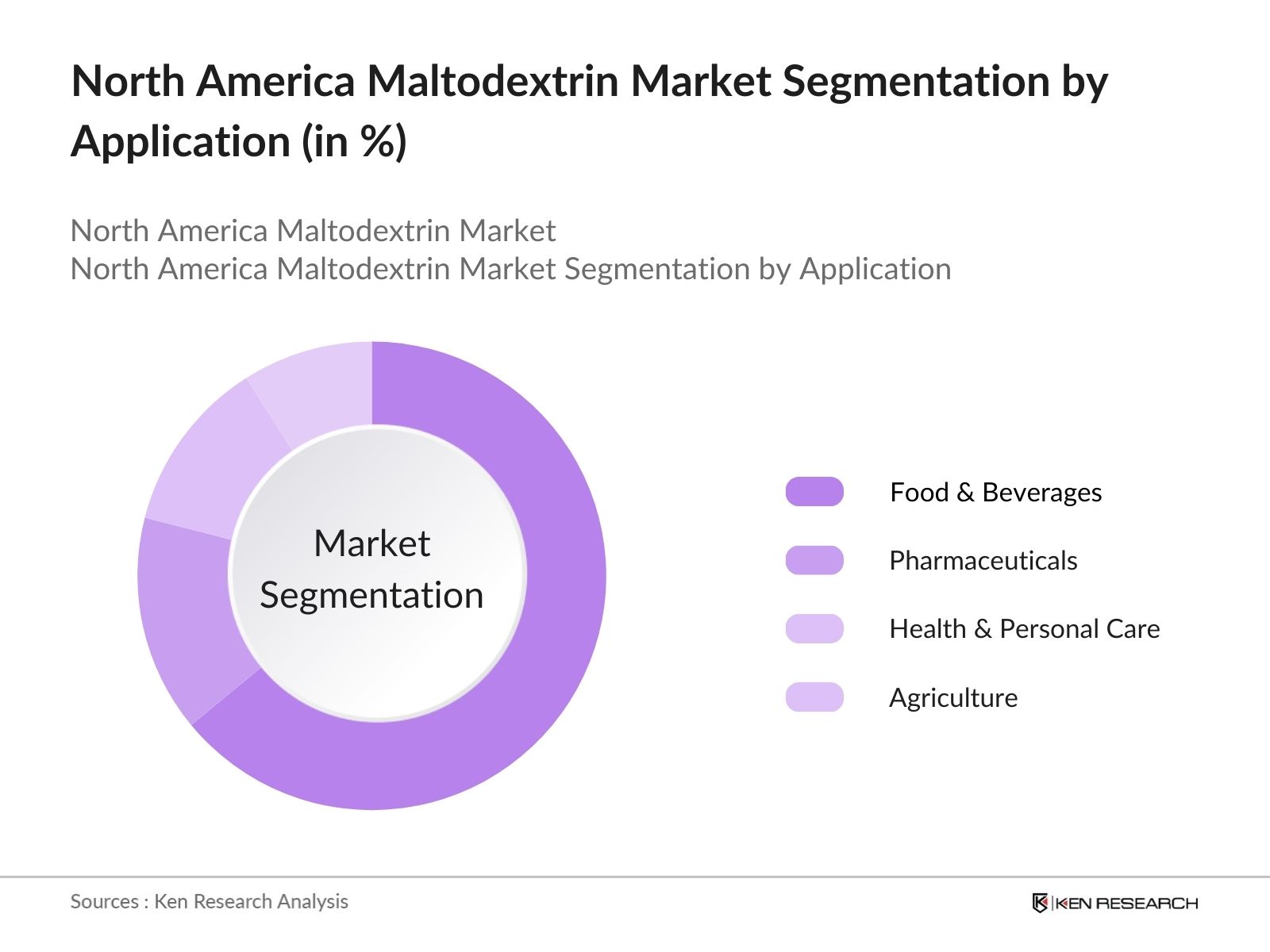

By Application: The market is also segmented by application into food & beverages, pharmaceuticals, health & personal care, and agriculture. The food & beverage segment is the largest in this market, driven by the growing consumption of processed foods, infant nutrition, and sports supplements. Maltodextrins role as a bulking agent and stabilizer makes it indispensable in these sectors. Within this segment, sports nutrition and energy drinks are seeing increased usage due to the rising health consciousness and demand for performance-enhancing products.

The North America Maltodextrin market is highly consolidated, with key players dominating the space. Major companies such as Cargill, Inc., The Archer Daniels Midland Company, and Ingredion Incorporated play a pivotal role in the industry.

Over the next five years, the North America maltodextrin industry is expected to witness steady growth, driven by continuous demand from the food and beverage sector, advancements in product innovation, and a growing preference for non-GMO and organic variants.

|

By Source |

Corn-Based Wheat-Based Potato-Based Cassava-Based |

|

By Application |

Food & Beverages Pharmaceuticals Health & Personal Care Agriculture |

|

By Region |

United States Canada Mexico |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rise in Processed Food Consumption

3.1.2. Expanding Use in Pharmaceuticals and Cosmetics

3.1.3. Growing Demand in Sports Nutrition and Energy Drinks

3.1.4. Increasing Adoption of Clean-Label Ingredients

3.2. Market Challenges

3.2.1. Health Concerns Regarding Sugar Substitutes

3.2.2. Fluctuating Raw Material Prices

3.2.3. Regulatory Constraints in Food Additives

3.3. Opportunities

3.3.1. Expansion into Organic and Non-GMO Variants

3.3.2. Increasing Applications in Animal Feed

3.3.3. Innovation in Maltodextrin Derivatives

3.4. Trends

3.4.1. Shift Towards Natural and Sustainable Ingredients

3.4.2. Technological Advancements in Production Processes

3.5. Government Regulations

3.5.1. FDA Standards for Food Additives

3.5.2. Nutritional Labeling Requirements

3.6. SWOT Analysis

3.7. Porters Five Forces

3.8. Competitive Ecosystem Analysis

4.1. By Source (In Value %)

4.1.1. Corn-Based

4.1.2. Wheat-Based

4.1.3. Potato-Based

4.1.4. Cassava-Based

4.2. By Application (In Value %)

4.2.1. Food and Beverages

4.2.2. Pharmaceuticals

4.2.3. Health and Personal Care

4.2.4. Agriculture

4.3. By Region (In Value %)

4.3.1. United States

4.3.2. Canada

4.3.3. Mexico

5.1. Detailed Profiles of Major Companies

5.1.1. Cargill, Incorporated

5.1.2. The Archer Daniels Midland Company

5.1.3. Ingredion Incorporated

5.1.4. Roquette Frres

5.1.5. Tate & Lyle PLC

5.1.6. TEREOS Group

5.1.7. Grain Processing Corporation

5.1.8. The Agrana Group

5.1.9. AVEBE

5.1.10. Matsutani Chemical Industry Co., Ltd.

5.1.11. Cargill Foods India

5.1.12. Samyang Genex

5.1.13. Sudzucker Group

5.1.14. Corn Products International

5.1.15. Global Sweeteners Holdings Ltd.

5.2. Cross Comparison Parameters (Market Share, Revenue, R&D Investment, Geographic Reach, Product Portfolio, Innovation Capability, Strategic Initiatives, Sustainability Practices)

5.3. Market Share Analysis

5.4. Strategic Initiatives and Partnerships

5.5. Mergers and Acquisitions

5.6. Investment Analysis

6.1. Environmental Standards

6.2. Certification and Compliance

6.3. Nutritional Guidelines

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Source (In Value %)

8.2. By Application (In Value %)

8.3. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing and Brand Positioning

9.4. White Space Opportunity Analysis

Disclaimer Contact UsThis phase involves creating a comprehensive map of the North America Maltodextrin Market by identifying key stakeholders, market drivers, and trends. Extensive desk research is conducted using both secondary and proprietary databases to gather insights on production capacities, consumption trends, and regulatory requirements.

During this phase, historical data on production, sales, and market penetration is compiled. The market size and growth rates are calculated by assessing the demand across food, beverage, and pharmaceutical sectors, supported by data from industry reports and government publications.

Expert interviews are conducted with industry professionals and market leaders to validate the market hypotheses. These interviews provide critical insights into pricing trends, competitive dynamics, and the impact of regulatory frameworks on production and sales.

The final phase involves synthesizing the collected data and insights into a detailed report. The report is validated by engaging directly with maltodextrin manufacturers, ensuring that all market estimates and projections are accurate and reliable.

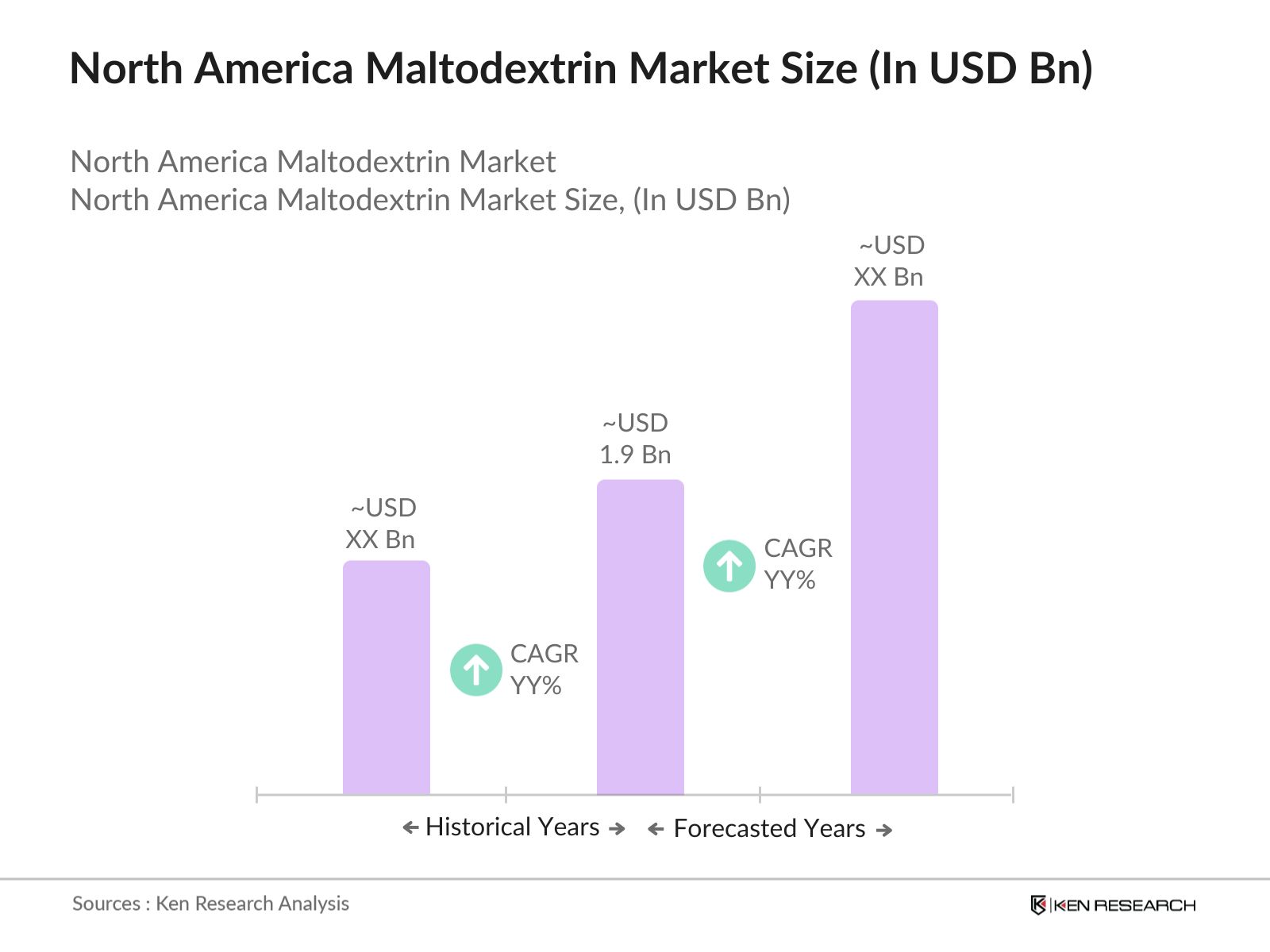

The North America Maltodextrin market was valued at USD 1.9 billion, driven by its growing applications in food and beverages, pharmaceuticals, and health products.

Key challenges in the North America Maltodextrin market include fluctuating raw material prices, particularly corn, and health concerns over maltodextrin consumption, such as potential blood sugar spikes.

Leading players in the North America Maltodextrin market include Cargill, Inc., Archer Daniels Midland Company, Ingredion Incorporated, Roquette Frres, and Tate & Lyle PLC, which dominate due to their global reach and innovation in product development.

Growth in the North America Maltodextrin market is driven by the increasing use of maltodextrin in packaged foods, infant nutrition, and sports supplements, along with the rising demand for clean-label and non-GMO products.

The United States and Canada dominate the North America Maltodextrin market due to their strong food processing industries and extensive corn production.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.