North America Medical Grade Silicone Market Outlook to 2030

Region:Global

Author(s):Sanjna

Product Code:KROD9018

November 2024

100

About the Report

North America Medical Grade Silicone Market Overview

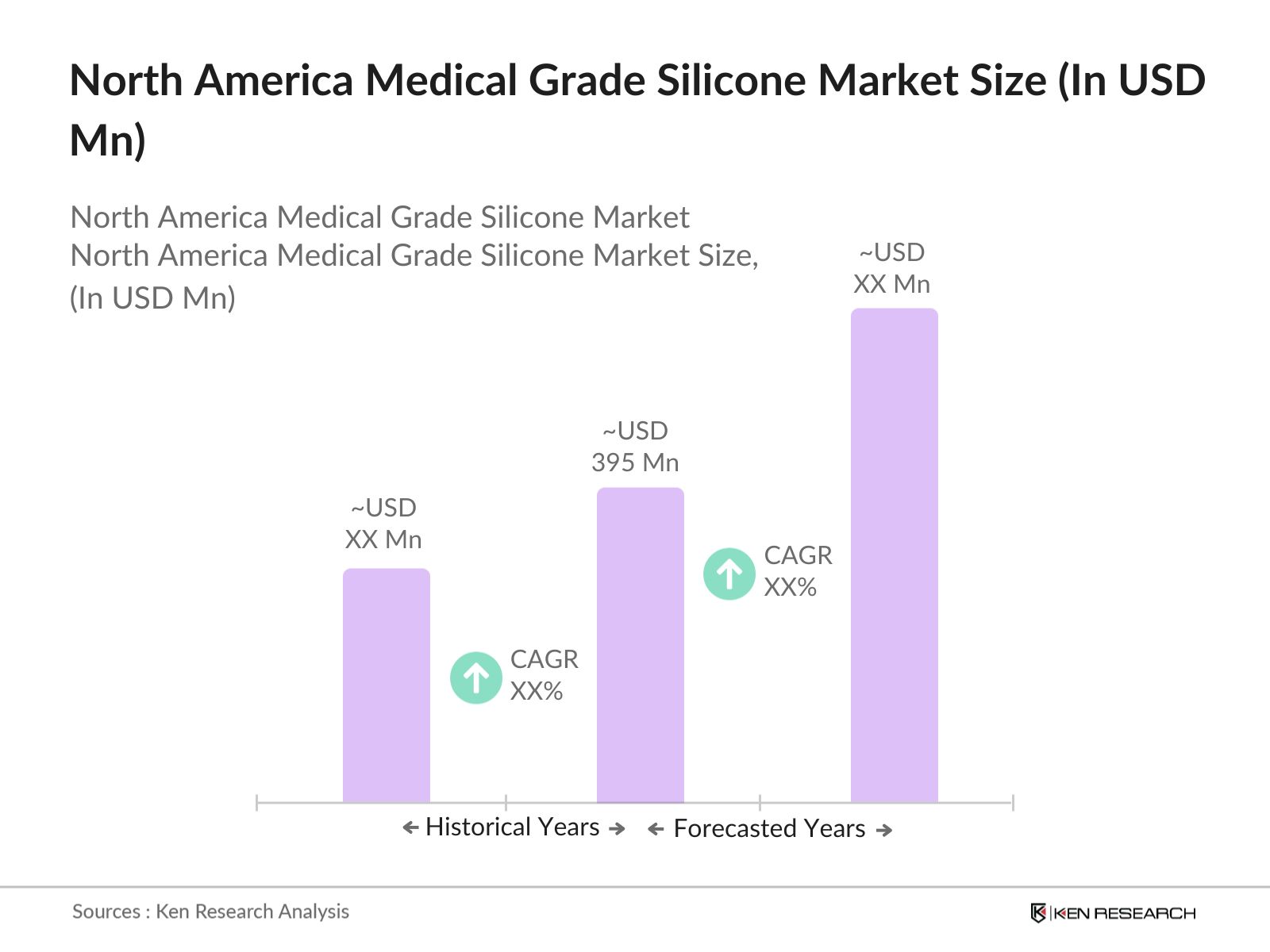

- The North America medical grade silicone market is valued at USD 305 million, driven primaryly by the increasing demand for advanced medical devices and implants. The rising prevalence of chronic diseases, which necessitates the use of silicone-based products like implants, catheters, and prosthetics, is a significant factor driving market growth. Additionally, the biocompatibility of medical grade silicone makes it the preferred material for medical devices used in surgeries and other therapeutic procedures, thus bolstering its demand.

- Countries like the United States and Canada dominate the North America medical grade silicone market due to their advanced healthcare infrastructure and high healthcare expenditure. The presence of major healthcare technology companies and the growing demand for medical-grade materials for devices and prosthetics in these regions further drive their market leadership. Both nations also benefit from strong regulatory frameworks that encourage innovation in medical devices, increasing the application of silicone-based products across various segments of the healthcare industry.

- The environmental impact of silicone production has come under scrutiny, leading to new regulations in 2023 focused on reducing carbon emissions during manufacturing. The U.S. Environmental Protection Agency (EPA) introduced guidelines requiring medical silicone manufacturers to cut emissions by 20%. Additionally, Canadian authorities introduced sustainability goals for silicone manufacturing plants, further increasing regulatory compliance burdens. These measures aim to mitigate the environmental footprint of silicone production in North America.

North America Medical Grade Silicone Market Segmentation

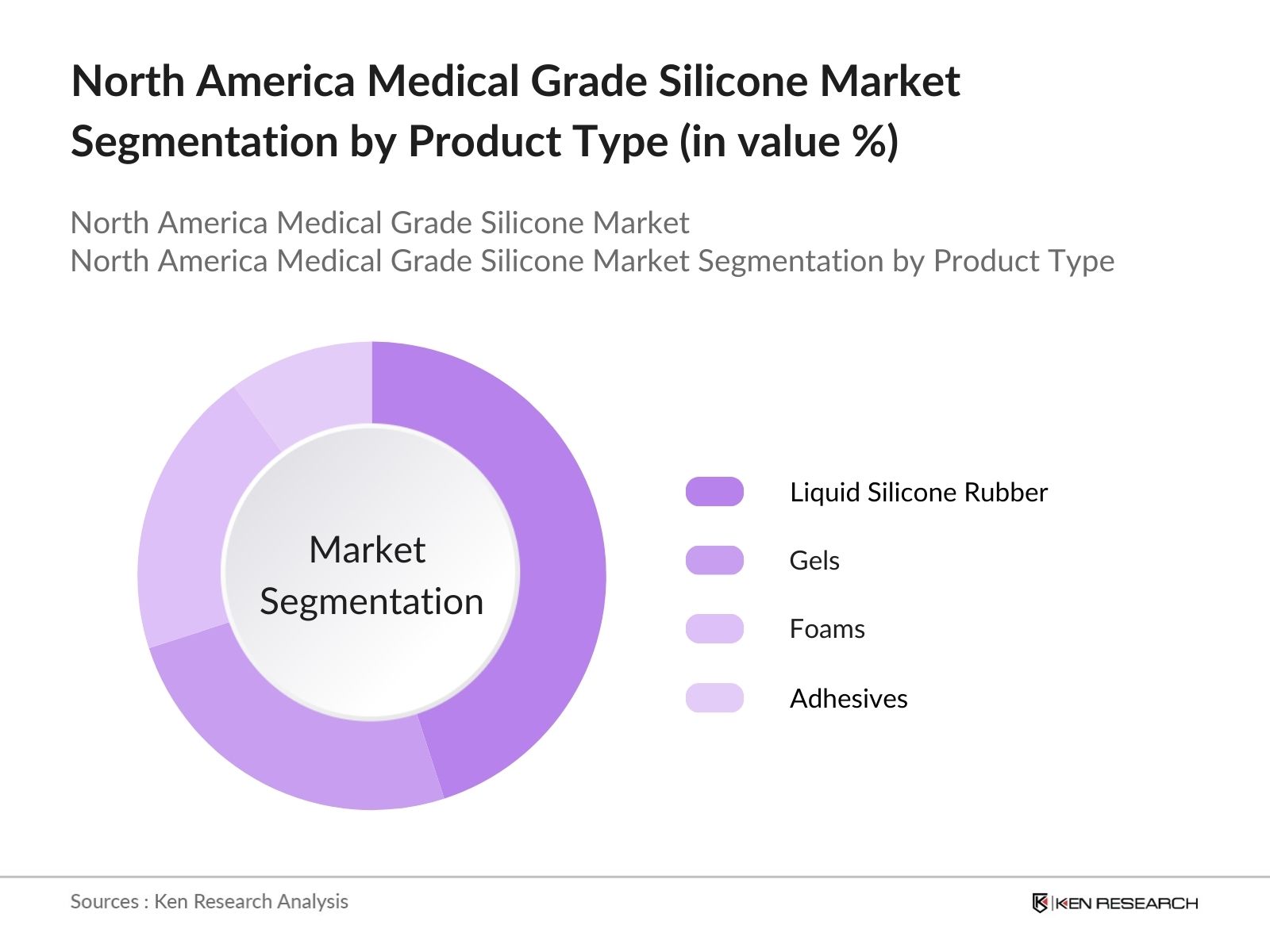

By Product Type: The North America medical grade silicone market is segmented by product type into liquid silicone rubber, gels, foams, and adhesives. Liquid silicone rubber holds a dominant market share under this segmentation due to its versatile applications in medical devices, particularly in implants and catheters. Liquid silicone rubber's biocompatibility and excellent performance in sterilization and temperature control make it the material of choice for critical medical devices. Its flexibility and durability also ensure long-term reliability, contributing to its large market share.

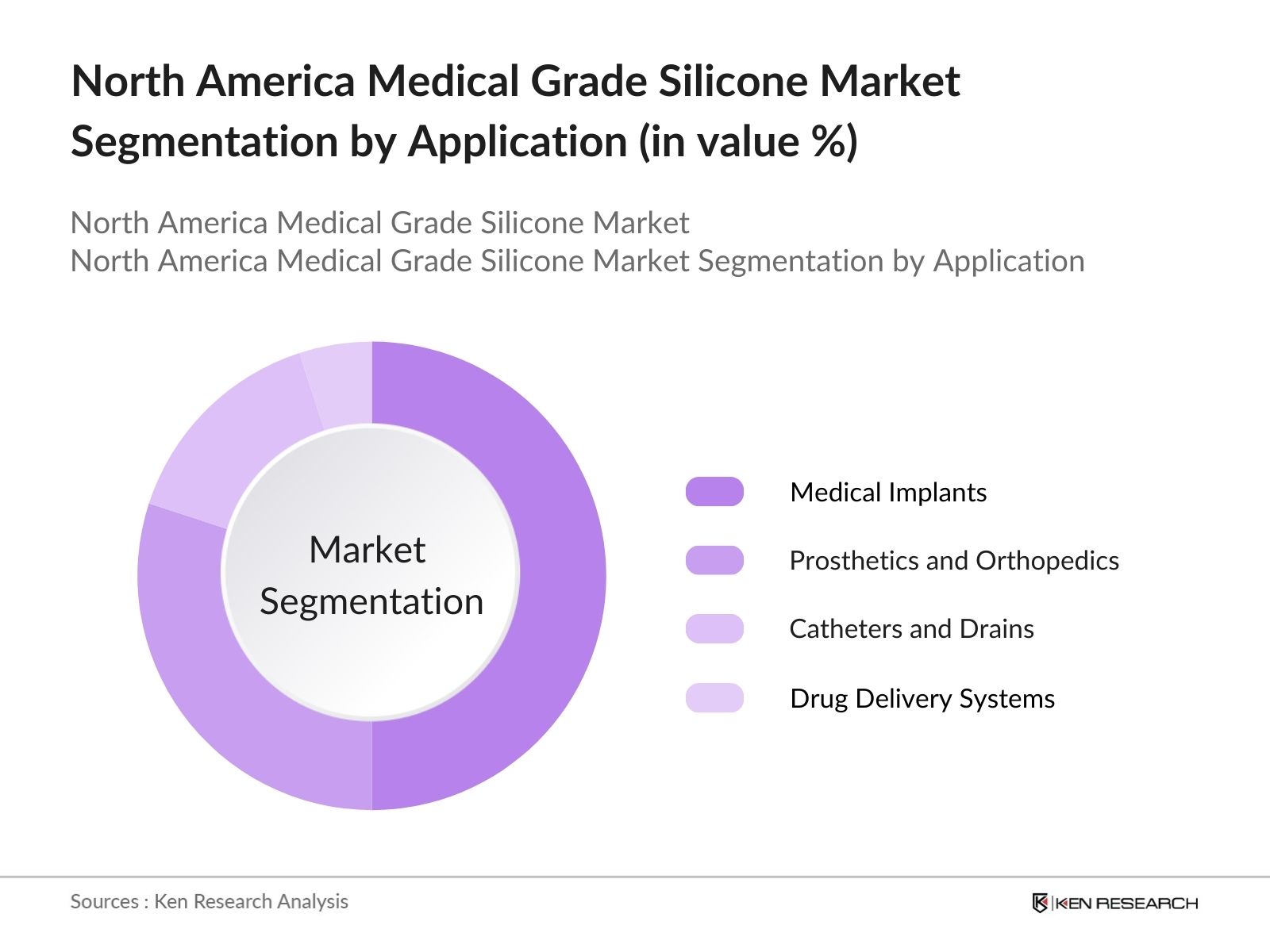

By Application: The market is also segmented by application into medical implants, prosthetics and orthopedics, catheters and drains, and drug delivery systems. Medical implants dominate this category due to the growing demand for cosmetic and reconstructive surgeries. Medical-grade silicone is extensively used in breast implants, facial implants, and other reconstructive devices. The safety and durability of silicone materials make them ideal for implants, which require biocompatibility and long-lasting performance.

North America Medical Grade Silicone Market Competitive Landscape

The North America medical grade silicone market is dominated by a few key players who possess strong market presence due to their product innovation, regulatory approvals, and technological integration. Companies like Dow Inc., Wacker Chemie AG, and Avantor, Inc. maintain significant influence, contributing to market consolidation. These firms lead the market by investing in research and development to create innovative silicone-based medical products that meet stringent regulatory requirements in North America.

|

Company |

Establishment Year |

Headquarters |

Market Presence |

Technology Integration |

Regional Focus |

Revenue (USD) |

Employees |

Sustainability Initiatives |

|---|---|---|---|---|---|---|---|---|

|

Dow Inc. |

1897 |

Midland, USA |

- |

- |

- |

- |

- |

- |

|

Wacker Chemie AG |

1914 |

Munich, Germany |

- |

- |

- |

- |

- |

- |

|

Avantor, Inc. |

1904 |

Radnor, USA |

- |

- |

- |

- |

- |

|

|

Shin-Etsu Chemical Co. Ltd |

1926 |

Tokyo, Japan |

- |

- |

- |

- |

- |

|

|

Elkem Silicones |

1906 |

Oslo, Norway |

- |

- |

- |

- |

- |

North America Medical Grade Silicone Market Analysis

Growth Drivers

- Increasing Demand for Medical Implants: The demand for medical-grade silicone in the North American medical implants sector has surged due to its biocompatibility and durability. According to the U.S. National Library of Medicine, there were over 2 million prosthetic surgeries in the U.S. in 2022, with silicone playing a crucial role in implants like breast, heart valves, and joint replacements. Silicones flexibility and ability to integrate with body tissues have made it indispensable for manufacturers.

- Expanding Healthcare Infrastructure: The North American healthcare infrastructure continues to expand, fueled by increasing government spending. This growth supports the rising demand for medical-grade silicone in surgical equipment, catheters, and diagnostic tools. The Canadian healthcare sector also saw significant investment, with $72 billion in healthcare expenditure in 2023. These investments create opportunities for the silicone market as hospitals and clinics enhance their offerings.

- Technological Advancements in Silicone Products: Technological advancements in medical-grade silicone products have enhanced their application scope. In 2024, the introduction of nanotechnology-enabled silicone devices allowed for more precise drug delivery systems and improved patient outcomes. North American manufacturers have also developed high-performance liquid silicone rubber (LSR) for wearable medical devices, expanding the usability of silicone in wearable health monitors and therapeutic equipment. The integration of silicone into next-generation healthcare technologies highlights its versatility and growing demand.

Challenges

- Regulatory Approvals: Securing regulatory approvals remains a key challenge in the North American medical-grade silicone market. In 2023, the U.S. FDA updated its medical device regulations, which caused delays in the approval of new silicone-based products. Over 1,500 new device applications were held up, leading to longer product development cycles. Similarly, Health Canadas stringent testing and certification procedures require manufacturers to adhere to rigorous standards, which increases the time and cost for market entry, hindering smaller silicone suppliers.

- Limited Biocompatibility Standards: Although medical-grade silicone is widely used, the lack of uniform biocompatibility standards across North America poses a challenge for manufacturers. The FDA and Health Canada each have their own testing criteria, which can complicate the production process. In 2023, over 500 medical devices were recalled in the U.S. due to failure in meeting biocompatibility standards, emphasizing the need for more consistent regulations. This inconsistency hampers product innovation and market entry.

North America Medical Grade Silicone Market Future Outlook

North America medical grade silicone market is expected to experience robust growth, driven by increasing demand for minimally invasive surgical procedures and advancements in medical technology. The growing application of silicone in drug delivery systems and 3D-printed medical devices further enhances the market's outlook. Additionally, government support for research in medical technologies and the expansion of healthcare infrastructure are key factors likely to propel market growth in the future.

Market Opportunities

- Rise in Cosmetic Surgeries: The rising number of cosmetic surgeries in North America has created significant growth opportunities for medical-grade silicone, particularly in breast implants and reconstructive surgeries. In 2022, the American Society of Plastic Surgeons reported over 2.5 million cosmetic surgeries in the U.S., with silicone being the preferred material for soft tissue implants. As demand for cosmetic enhancements continues to grow, so does the need for high-quality silicone products, offering lucrative opportunities for silicone manufacturers.

- Increasing Geriatric Population and Associated Medical Needs: North America's rapidly aging population is creating opportunities for medical-grade silicone in products aimed at elder care. The U.S. Census Bureau reported that, by 2024, more than 56 million people will be over the age of 65, significantly increasing demand for medical devices such as catheters, hearing aids, and prostheticsall of which utilize silicone. This demographic shift is expected to sustain long-term growth in the silicone market as healthcare providers focus on age-related medical solutions.

Scope of the Report

|

Segments |

Sub-Segments |

|

By Product Type |

Liquid Silicone Rubber Gels Foams Adhesives |

|

By Application |

Medical Implants Prosthetics and Orthopedics Catheters and Drains Drug Delivery Systems |

|

By End-Use Industry |

Hospitals and Clinics Ambulatory Surgical Centers Diagnostic Centers |

|

By Region |

United States Canada Mexico |

|

By Manufacturing Process |

Injection Molding Extrusion Compression Molding |

Products

Key Target Audience

Medical Device Manufacturers

Prosthetic and Orthopedic Device Companies

Hospitals and Clinics

Drug Delivery System Developers

Silicone Material Suppliers

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (FDA, Health Canada)

Healthcare Product Distributors

Companies

Players Mentioned in the Report

Dow Inc.

Wacker Chemie AG

Avantor, Inc.

Shin-Etsu Chemical Co. Ltd

Elkem Silicones

NuSil Technology LLC

Momentive Performance Materials Inc.

Rogers Corporation

Henkel AG & Co. KGaA

Specialty Silicone Fabricators, Inc.

Table of Contents

1. North America Medical Grade Silicone Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. North America Medical Grade Silicone Market Size (In USD Mn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. North America Medical Grade Silicone Market Analysis

3.1 Growth Drivers

3.1.1 Increasing Demand for Medical Implants

3.1.2 Expanding Healthcare Infrastructure

3.1.3 Growing Applications in Prosthetics and Orthopedics

3.1.4 Technological Advancements in Silicone Products

3.2 Market Challenges

3.2.1 Regulatory Approvals (FDA, Health Canada)

3.2.2 Raw Material Price Volatility

3.2.3 Limited Biocompatibility Standards

3.3 Opportunities

3.3.1 Rise in Cosmetic Surgeries

3.3.2 Expanding Application in Drug Delivery Systems

3.3.3 Increasing Geriatric Population and Associated Medical Needs

3.4 Trends

3.4.1 Surge in Minimally Invasive Surgeries

3.4.2 Bio-Resorbable Silicone Product Development

3.4.3 Growing Demand for 3D-Printed Silicone Medical Devices

3.5 Government Regulations (FDA, Health Canada Compliance)

3.5.1 Medical Device Regulation Updates

3.5.2 Environmental Impact Regulations on Manufacturing

3.5.3 Trade Tariffs and Export/Import Restrictions

4. North America Medical Grade Silicone Market Segmentation

4.1 By Product Type (In Value %)

4.1.1 Liquid Silicone Rubber

4.1.2 Gels

4.1.3 Foams

4.1.4 Adhesives

4.2 By Application (In Value %)

4.2.1 Medical Implants

4.2.2 Prosthetics and Orthopedics

4.2.3 Catheters and Drains

4.2.4 Drug Delivery Systems

4.3 By End-Use Industry (In Value %)

4.3.1 Hospitals and Clinics

4.3.2 Ambulatory Surgical Centers

4.3.3 Diagnostic Centers

4.4 By Region (In Value %)

4.4.1 United States

4.4.2 Canada

4.4.3 Mexico

4.5 By Manufacturing Process (In Value %)

4.5.1 Injection Molding

4.5.2 Extrusion

4.5.3 Compression Molding

5. North America Medical Grade Silicone Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Dow Inc.

5.1.2 Wacker Chemie AG

5.1.3 Avantor, Inc.

5.1.4 Shin-Etsu Chemical Co., Ltd.

5.1.5 Elkem Silicones

5.1.6 NuSil Technology LLC

5.1.7 Momentive Performance Materials Inc.

5.1.8 Rogers Corporation

5.1.9 Henkel AG & Co. KGaA

5.1.10 Specialty Silicone Fabricators, Inc.

5.2 Cross Comparison Parameters (Revenue, Product Portfolio, Innovation, Manufacturing Capabilities, Geographic Presence, Partnerships, Regulatory Approvals, Research and Development Expenditure)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. North America Medical Grade Silicone Market Regulatory Framework

6.1 FDA Approval Processes

6.2 Health Canada Guidelines

6.3 Environmental Standards

6.4 Certification Processes

6.5 Import/Export Compliance

7. North America Medical Grade Silicone Future Market Size (In USD Mn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. North America Medical Grade Silicone Future Market Segmentation

8.1 By Product Type (In Value %)

8.2 By Application (In Value %)

8.3 By End-Use Industry (In Value %)

8.4 By Region (In Value %)

8.5 By Manufacturing Process (In Value %)

9. North America Medical Grade Silicone Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

In the initial phase, an ecosystem map is constructed, encompassing all major stakeholders within the North America Medical Grade Silicone Market. This step involves comprehensive desk research, utilizing a mix of secondary and proprietary databases to identify critical variables influencing market dynamics, including product types and applications.

Step 2: Market Analysis and Construction

During this phase, historical data related to the medical grade silicone market in North America is compiled. Key areas of focus include market penetration, application-specific analysis, and revenue generation based on product types. Quality assurance is conducted through cross-verification of data sources.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through expert consultations with industry professionals. These consultations, conducted via interviews and surveys, provide valuable insights into the operational, financial, and technological aspects of medical grade silicone products.

Step 4: Research Synthesis and Final Output

In the final phase, direct engagement with key manufacturers and medical institutions is undertaken to gather insights into product performance, consumer preferences, and market growth opportunities. This data is synthesized with the initial research to create a detailed, validated report.

Frequently Asked Questions

01. How big is the North America Medical Grade Silicone Market?

The North America medical grade silicone market is valued at USD 305 million, driven by increasing demand for silicone-based products in medical implants, prosthetics, and drug delivery systems.

02. What are the challenges in the North America Medical Grade Silicone Market?

Challenges in North America medical grade silicone market include regulatory hurdles such as FDA and Health Canada approvals, volatile raw material prices, and the need for biocompatibility standards in silicone products.

03. Who are the major players in the North America Medical Grade Silicone Market?

Key players in North America medical grade silicone market include Dow Inc., Wacker Chemie AG, Avantor, Inc., Shin-Etsu Chemical Co. Ltd, and Elkem Silicones, all of whom lead the market through innovation and advanced product offerings.

04. What are the growth drivers of the North America Medical Grade Silicone Market?

North America medical grade silicone market is driven by increasing demand for medical implants, advancements in minimally invasive surgical procedures, and the expansion of healthcare infrastructure in the U.S. and Canada.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.