North America Military Antenna Market Outlook to 2030

Region:North America

Author(s):Shreya Garg

Product Code:KROD10520

November 2024

98

About the Report

North America Military Antenna Market Overview

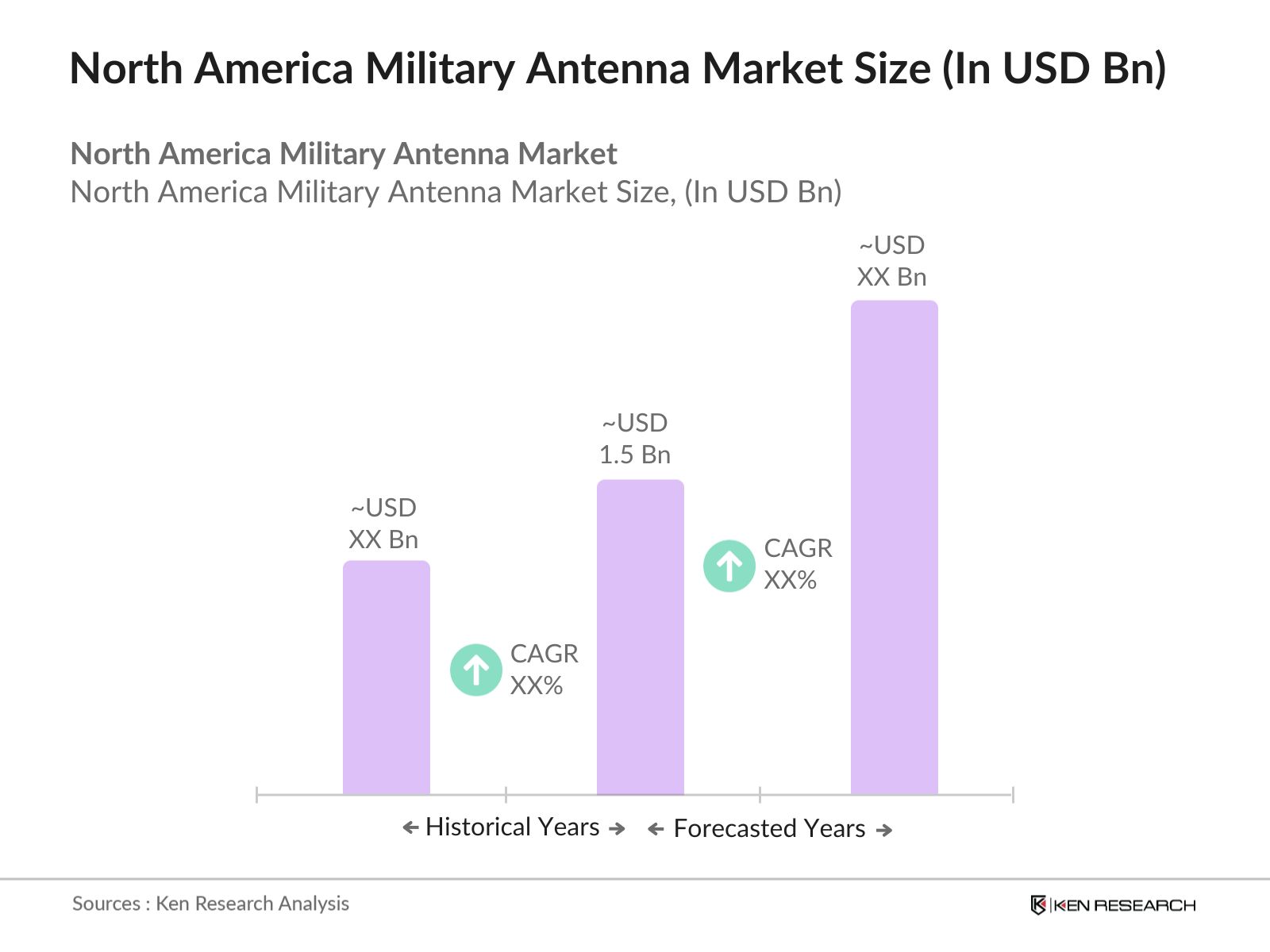

- The North America Military Antenna market is valued at USD 1.5 billion, based on a five-year historical analysis. This market size is driven by increasing defense budgets across the United States and Canada, which are prioritizing investments in advanced communication technologies to enhance military capabilities. The growing adoption of SATCOM (Satellite Communication) antennas, especially for airborne and naval applications, significantly contributes to the market's expansion. Additionally, the increasing demand for secure, high-frequency communication systems by the armed forces drives the deployment of modern military antennas.

- The United States is a dominant player in the North America Military Antenna market due to its substantial defense spending and continuous investments in military modernization. The countrys emphasis on developing advanced warfare technologies and securing communication networks for diverse military applications makes it a key market driver. Canada also plays a significant role, leveraging its collaboration with NATO and investment in upgrading its communication systems for defense purposes. Both countries have robust R&D capabilities and are committed to advancing the integration of high-performance antennas in military operations.

- ITAR continues to regulate the export of military communication equipment, including antennas, impacting North American manufacturers. In 2024, the U.S. government imposed stringent controls on exporting sensitive communication technologies, with violations leading to penalties of up to USD 1 million per infraction. Compliance with ITAR is essential for companies aiming to engage in international trade, as it affects the ability to supply military-grade antennas to allied nations. This regulation ensures secure handling of defense-related technologies but also limits the market scope for manufacturers.

North America Military Antenna Market Segmentation

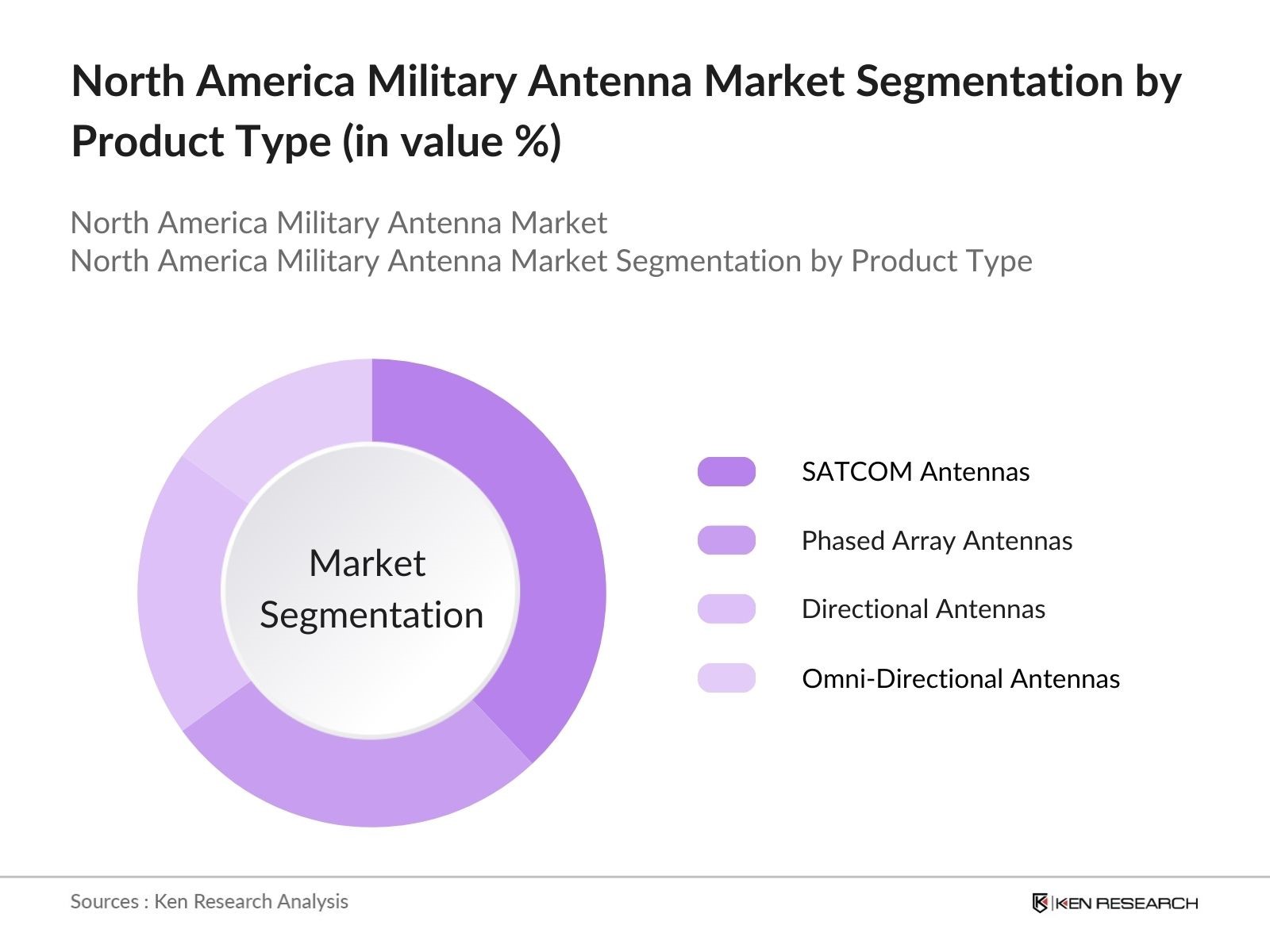

By Product Type: The market is segmented by product type into directional antennas, omni-directional antennas, phased array antennas, and SATCOM antennas. Recently, SATCOM antennas have a dominant market share under this segmentation. This is attributed to the increasing use of satellite communications for long-range operations, especially in remote regions. SATCOM antennas provide secure and reliable communication, crucial for coordinating modern military operations. Their enhanced data transmission capabilities and resilience to jamming further solidify their preference among military forces.

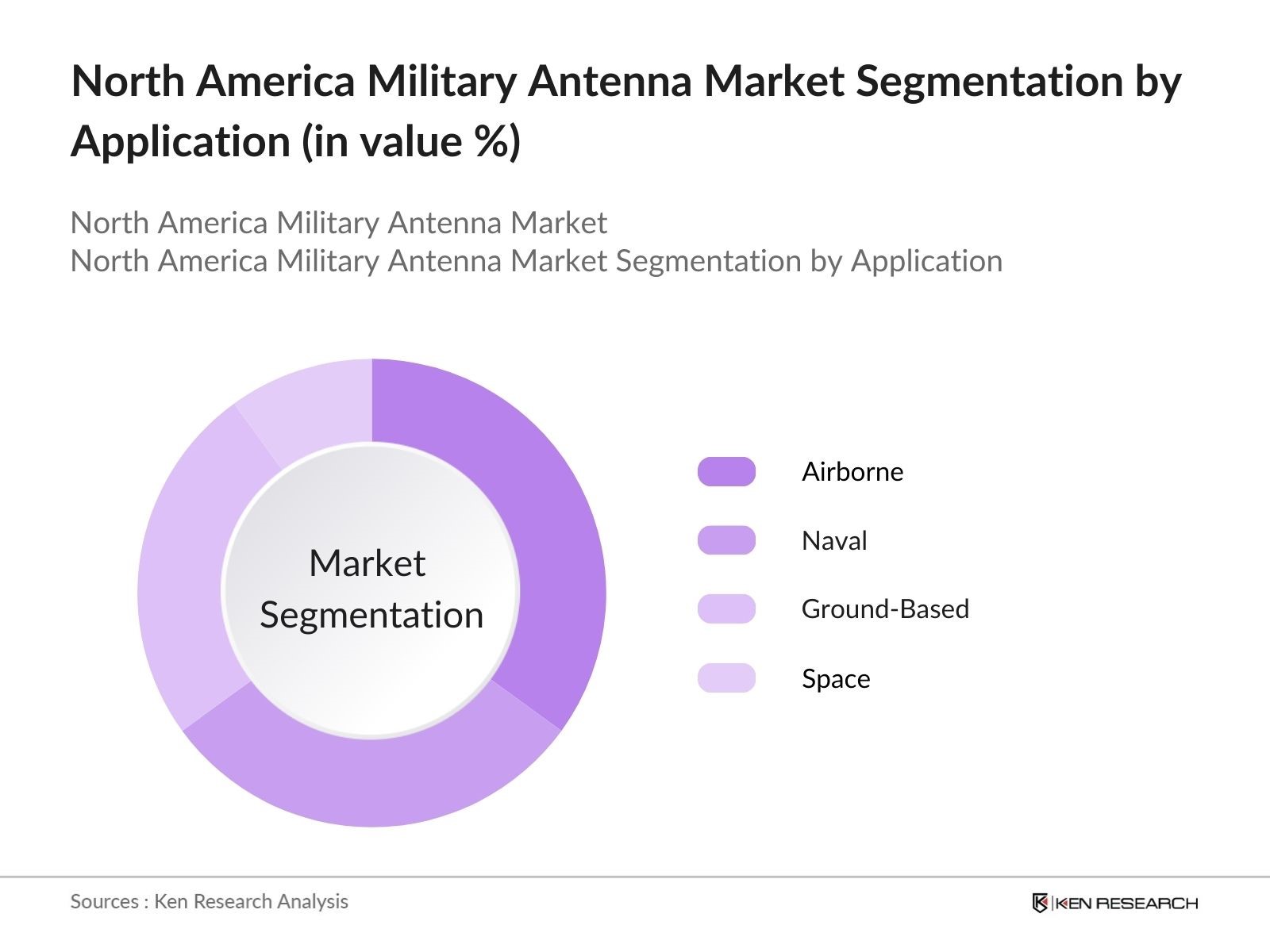

By Application: The market is segmented by application into airborne, naval, ground-based, and space applications. Airborne applications dominate the market due to the increased use of UAVs (Unmanned Aerial Vehicles) and aircraft for surveillance, reconnaissance, and communication relay. The demand for advanced communication solutions for these platforms drives the adoption of specialized antennas that support high-frequency and multi-band operations, ensuring seamless communication across various military missions.

North America Military Antenna Market Competitive Landscape

The North America Military Antenna market is dominated by key players, including industry giants and specialized manufacturers. This competitive landscape underscores the influence of well-established companies that continually invest in R&D and innovation to meet the evolving needs of the military sector.

|

Company |

Establishment Year |

Headquarters |

R&D Investment |

Revenue (USD Million) |

Product Portfolio Size |

Regional Presence |

Customer Base |

Technology Patents |

Strategic Partnerships |

|

Raytheon Technologies Corporation |

1922 |

||||||||

|

Lockheed Martin Corporation |

1995 |

||||||||

|

L3Harris Technologies Inc. |

2019 |

||||||||

|

Northrop Grumman Corporation |

1939 |

||||||||

|

BAE Systems |

1999 |

North America Military Antenna Industry Analysis

Growth Drivers

- Rising Defense Budgets: The North American military antenna market is bolstered by increasing defense budgets, notably in the United States and Canada. In 2024, the U.S. Department of Defense's budget stands at approximately USD 842 billion, reflecting heightened investments in advanced communication and surveillance systems. Canada allocated around CAD 32 billion to its National Defence in the same year, reflecting a continued focus on enhancing communication infrastructure for military operations . These allocations are aimed at upgrading communication channels, directly impacting demand for advanced military antennas to enhance strategic capabilities across North America.

- Technological Advancements in Communication Systems: Technological progress in military communication systems has driven demand for advanced antenna solutions across North America. By 2024, the integration of AI and machine learning in signal processing has become standard in military applications, improving communication clarity and reducing interference. For instance, the U.S. DoD has been actively deploying AI-enabled communication tools, dedicating over USD 2 billion for AI integration in various communication systems. These advancements are critical for the adoption of military antennas that support real-time data transmission and secure communications, meeting the evolving needs of modern warfare.

- Expanding Surveillance Operations: The expansion of surveillance operations, particularly along North America's borders, drives the demand for military antennas. The U.S. allocated USD 15 billion in 2024 for border surveillance technology, emphasizing the deployment of advanced radars and communication equipment. This includes the use of high-frequency antennas for surveillance drones and remote monitoring. Canada has similarly enhanced its Arctic surveillance capabilities with CAD 500 million allocated in 2024 for aerial surveillance systems. Such investments in surveillance underscore the critical role of military antennas in maintaining border security and situational awareness.

Market Challenges

- High R&D Costs: The development of advanced military antennas involves substantial R&D investments, posing challenges for manufacturers. In 2024, the U.S. DoD allocated over USD 100 billion for R&D, a portion of which is directed toward developing next-generation communication and radar systems. However, smaller firms struggle with similar investments, limiting their ability to compete with established players. These high costs create barriers for new entrants and restrict innovation to a few key players, impacting the overall growth potential of the market.

- Export Regulations and Compliance: Export regulations, particularly those enforced under ITAR (International Traffic in Arms Regulations), present significant hurdles for the military antenna market in North America. In 2024, exports of military communication systems from the U.S. are subject to stringent controls, impacting market dynamics. Violations can result in penalties of up to USD 1 million per infraction, deterring potential exporters. Such regulations affect the ability of manufacturers to access international markets, limiting their revenue streams and making compliance a critical aspect of market operations.

North America Military Antenna Market Future Outlook

Over the next five years, the North America Military Antenna market is expected to experience significant advancements driven by the rising integration of 5G technology in military communication, increased defense budgets, and a growing focus on developing advanced SATCOM solutions. The modernization of existing communication infrastructure and the ongoing adoption of UAVs for reconnaissance and combat operations are anticipated to fuel demand for high-performance military antennas. Furthermore, collaboration between defense contractors and government bodies will play a critical role in driving innovation within this market.

Future Market Opportunities

- Expansion of 5G for Military Applications: The expansion of 5G networks has opened opportunities for military applications, including communication between drones, vehicles, and command centers. As of 2024, the U.S. military invested USD 600 million in deploying 5G testbeds across various bases. This rollout supports the use of military antennas that can operate at higher frequencies, enabling faster and more secure communication. Canada also explores the use of 5G for defense applications, with CAD 200 million allocated for pilot projects in 2024. The increased adoption of 5G supports the development of new, high-frequency military antennas.

- Demand for UAV (Unmanned Aerial Vehicle) Antennas: UAVs have become integral to military surveillance and combat missions, increasing the demand for specialized antennas. In 2024, the U.S. military's UAV fleet exceeded 15,000 units, each requiring advanced antenna systems for communication and navigation. Canadas Department of National Defence also invested CAD 100 million in UAV development, including communication systems, in 2024. This demand highlights the need for compact, high-performance antennas that can be integrated into small, unmanned aircraft, providing an avenue for growth in the military antenna market.

Scope of the Report

|

Product Type |

Directional Antennas Omni-Directional Antennas Phased Array Antennas Satellite Communication (SATCOM) Antennas |

|

Frequency Band |

VHF/UHF Band L-Band Ku-Band Ka-Band |

|

Application |

Airborne Naval Ground-Based, Space |

|

Component Type |

Reflectors Feed Horns Low Noise Amplifiers (LNA) Transmit/Receive Modules |

|

Region |

United States Canada Mexico Rest of North America |

Products

Key Target Audience

Defense Contractors and System Integrators

Government and Regulatory Bodies (e.g., Federal Communications Commission, Department of Defense)

Satellite Communication Providers

Military R&D Institutions

Antenna Manufacturers

Electronics and Telecommunication Suppliers

Investor and Venture Capitalist Firms

UAV and Drone Manufacturers

Banks and Financial Institutions

Companies

Major Players

Raytheon Technologies Corporation

Lockheed Martin Corporation

L3Harris Technologies Inc.

Northrop Grumman Corporation

BAE Systems

Cobham Limited

General Dynamics Corporation

Rohde & Schwarz GmbH & Co KG

Thales Group

Airbus S.A.S

Honeywell International Inc.

QinetiQ Group plc

Comrod Communication AS

Southwest Antennas, Inc.

Antenna Research Associates, Inc.

Table of Contents

1. North America Military Antenna Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview (Frequency Range, Antenna Type, Platform, End-User, Geography)

2. North America Military Antenna Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (Technological Advancements, Military Modernization Programs, Strategic Alliances)

3. North America Military Antenna Market Analysis

3.1. Growth Drivers

3.1.1. Increased Defense Spending

3.1.2. Growing Need for Advanced Communication Systems

3.1.3. Expanding Military Operations

3.1.4. Rising Use of UAVs and Drones

3.2. Market Challenges

3.2.1. High Cost of Development

3.2.2. Supply Chain Disruptions

3.2.3. Cybersecurity Concerns in Communication Systems

3.3. Opportunities

3.3.1. Integration with 5G and Satellite Technologies

3.3.2. Growing Demand for Multi-Band Antennas

3.3.3. Increasing Focus on C4ISR Capabilities

3.4. Trends

3.4.1. Development of Stealth Antennas

3.4.2. Advancements in Phased Array Antennas

3.4.3. Miniaturization of Military Antennas

3.5. Government Regulations

3.5.1. ITAR (International Traffic in Arms Regulations)

3.5.2. Spectrum Allocation Policies

3.5.3. National Security Regulations

3.6. SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

3.7. Stake Ecosystem (OEMs, Component Suppliers, Integrators)

3.8. Porters Five Forces

3.8.1. Bargaining Power of Suppliers

3.8.2. Bargaining Power of Buyers

3.8.3. Threat of New Entrants

3.8.4. Threat of Substitutes

3.8.5. Industry Rivalry

3.9. Competition Ecosystem

4. North America Military Antenna Market Segmentation

4.1. By Frequency Range (In Value %)

4.1.1. High Frequency (HF)

4.1.2. Very High Frequency (VHF)

4.1.3. Ultra High Frequency (UHF)

4.1.4. Super High Frequency (SHF)

4.2. By Antenna Type (In Value %)

4.2.1. Dipole Antennas

4.2.2. Monopole Antennas

4.2.3. Array Antennas

4.2.4. Parabolic Reflector Antennas

4.3. By Platform (In Value %)

4.3.1. Ground

4.3.2. Airborne

4.3.3. Naval

4.3.4. Space

4.4. By End-User (In Value %)

4.4.1. Defense Forces

4.4.2. Homeland Security

4.4.3. Intelligence Agencies

4.4.4. Defense Contractors

4.5. By Geography (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5. North America Military Antenna Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Raytheon Technologies Corporation

5.1.2. Lockheed Martin Corporation

5.1.3. Northrop Grumman Corporation

5.1.4. L3Harris Technologies, Inc.

5.1.5. Cobham Limited

5.1.6. General Dynamics Corporation

5.1.7. BAE Systems

5.1.8. Boeing Defense, Space & Security

5.1.9. Rohde & Schwarz GmbH & Co KG

5.1.10. Commscope Inc.

5.1.11. Harris Corporation

5.1.12. ViaSat Inc.

5.1.13. Thales Group

5.1.14. HENSOLDT

5.1.15. Airbus Defense and Space

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Product Portfolio, Defense Contracts, Revenue, Military Contracts, Technological Capabilities, International Presence)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7 Venture Capital Funding

5.8. Government Contracts

5.9. Private Equity Investments

6. North America Military Antenna Market Regulatory Framework

6.1. ITAR Compliance

6.2. Defense Production Act

6.3. Export Control Regulations

6.4. Cybersecurity Maturity Model Certification (CMMC)

7. North America Military Antenna Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Defense Budgets, Technological Advancements, New Military Programs)

8. North America Military Antenna Future Market Segmentation

8.1. By Frequency Range (In Value %)

8.2. By Antenna Type (In Value %)

8.3. By Platform (In Value %)

8.4. By End-User (In Value %)

8.5. By Geography (In Value %)

9. North America Military Antenna Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the North America Military Antenna Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we will compile and analyze historical data pertaining to the North America Military Antenna Market. This includes assessing market penetration, the ratio of antenna manufacturers to defense contractors, and the resultant revenue generation. Furthermore, an evaluation of product quality statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple military antenna manufacturers to acquire detailed insights into product segments, sales performance, customer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the North America Military Antenna market.

Frequently Asked Questions

01 How big is the North America Military Antenna Market?

The North America Military Antenna market is valued at USD 1.5 billion, based on a five-year historical analysis. It is driven by rising defense budgets and the growing need for advanced communication systems.

02 What are the challenges in the North America Military Antenna Market?

Challenges in the North America Military Antenna market include high R&D costs, compliance with strict export regulations, and integration challenges with existing military communication systems. These factors can impede market growth and product development cycles.

03 Who are the major players in the North America Military Antenna Market?

Key players in the North America Military Antenna market include Raytheon Technologies Corporation, Lockheed Martin Corporation, L3Harris Technologies Inc., Northrop Grumman Corporation, and BAE Systems, each contributing through their advanced technology offerings and extensive product portfolios.

04 What are the growth drivers of the North America Military Antenna Market?

The North America Military Antenna market is driven by increased defense investments, advancements in satellite communication technologies, and the rising adoption of UAVs. The need for secure, high-bandwidth communication systems further fuels demand.

05 Why is the United States the leading market in North America?

The United States leads the North America Military Antenna market due to its substantial defense spending and focus on upgrading communication infrastructure. Its commitment to military modernization and R&D investments in advanced antenna systems supports this dominance.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.