North America Nasal Splint Market Outlook to 2030

Region:North America

Author(s):Paribhasha Tiwari

Product Code:KROD5784

December 2024

93

About the Report

North America Nasal Splint Market Overview

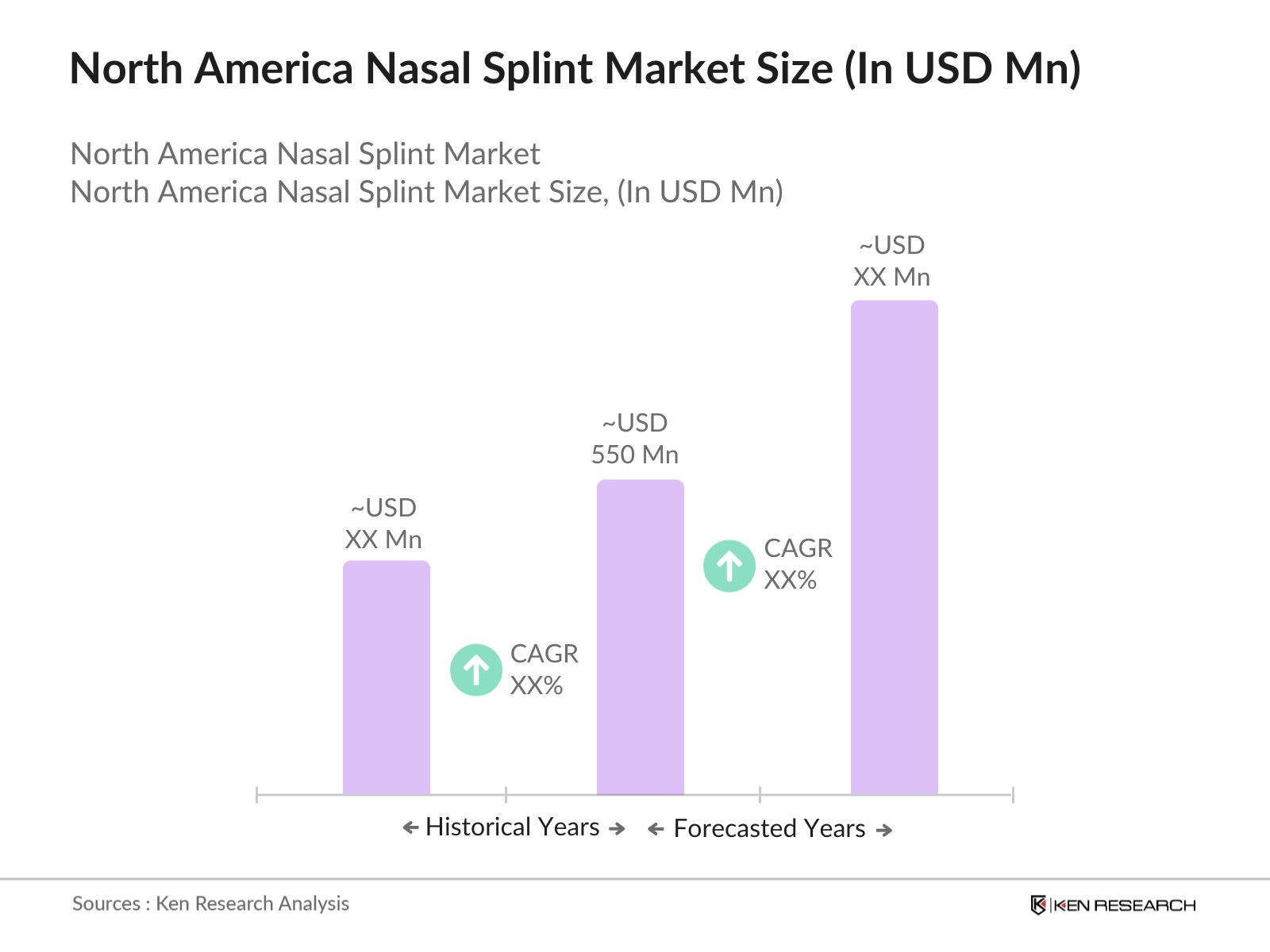

- The North America nasal splint market is valued at USD 550 million, based on a five-year historical analysis. The market growth is driven primarily by the increasing number of rhinoplasty surgeries and trauma-related nasal injuries, alongside advancements in splint technology. Nasal surgeries have become more common due to both cosmetic and medical reasons, boosting the demand for nasal splints, particularly in the United States and Canada, where healthcare infrastructure and patient awareness are robust.

- Cities like Los Angeles, New York, and Houston dominate the nasal splint market in North America. This dominance is attributed to the concentration of high-income individuals seeking cosmetic surgeries, well-established healthcare facilities, and top-tier plastic surgeons. Additionally, the rising number of outpatient surgeries in these urban centers supports a high demand for nasal splints, especially post-surgical products that aid in recovery.

- The U.S. Major funding flows include the American Rescue Plan Act, which allocated $1 trillion for healthcare facility upgrades, and the Build Back Better Act, which added $10 billion. Key projects include mental health hospitals in Texas and a major medical campus in Utah. These investments are part of broader federal and state efforts to expand healthcare access and upgrade outdated facilities, driving significant improvements in healthcare infrastructure across North America.

North America Nasal Splint Market Segmentation

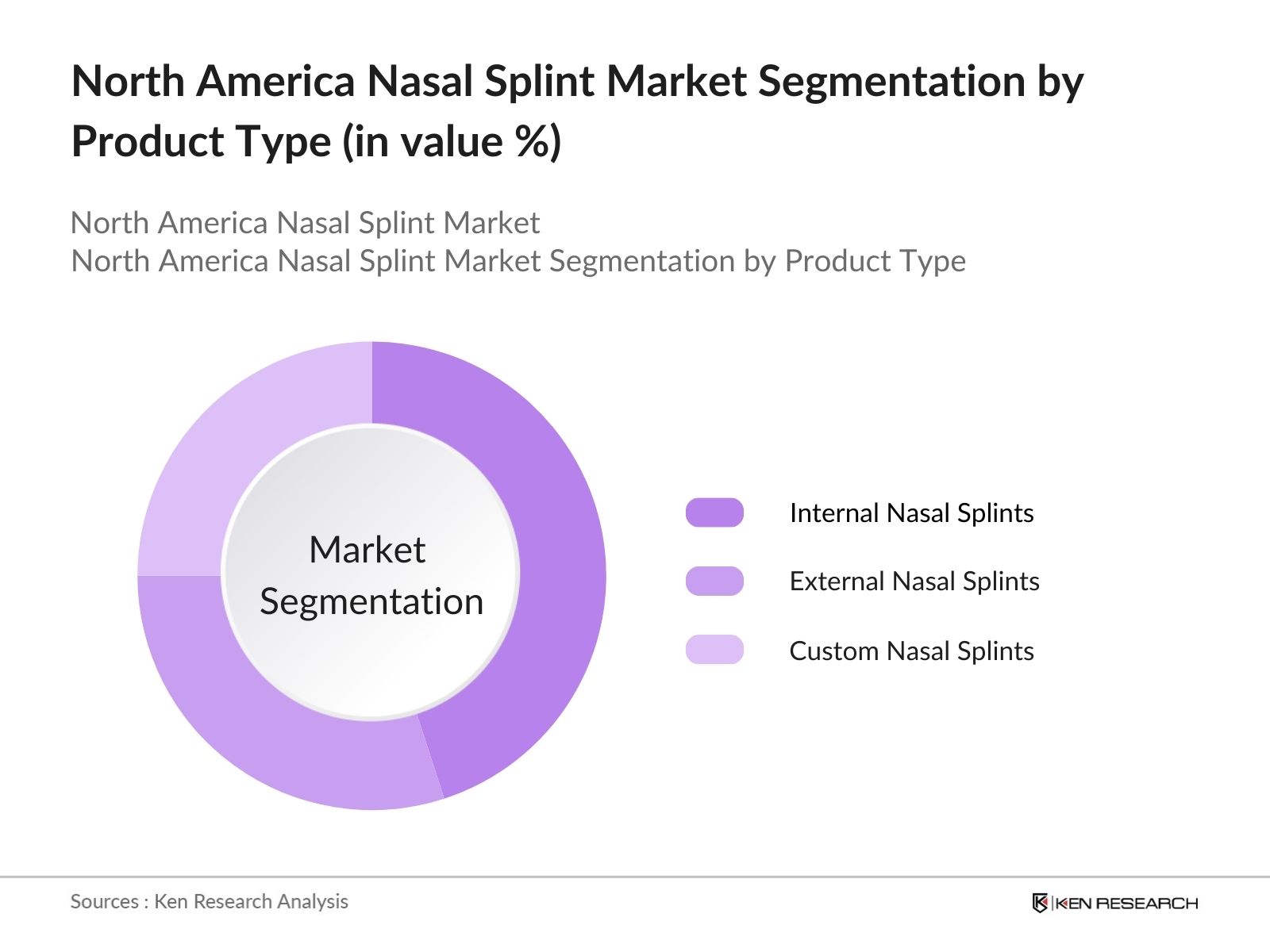

By Product Type: The North America nasal splint market is segmented by product type into internal nasal splints, external nasal splints, and custom nasal splints. Among these, internal nasal splints hold a dominant market share due to their extensive use in post-surgical recovery after rhinoplasty or septoplasty. These splints are often preferred because of their ability to prevent septal hematomas and maintain nasal structure post-surgery. Their popularity is also driven by the increasing number of nasal surgeries across the region and growing awareness of post-surgical care.

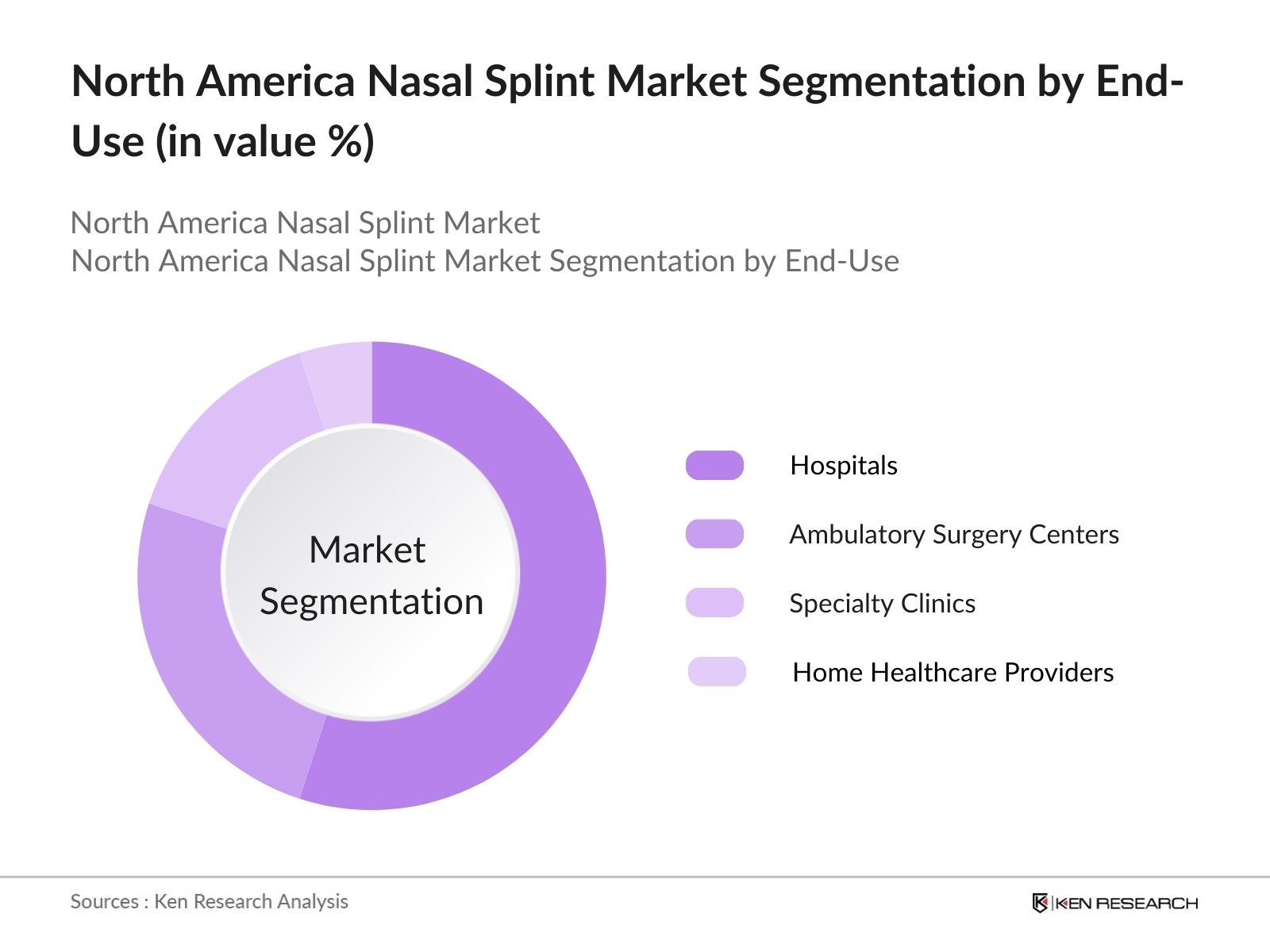

By End-User: The market is also segmented by end-user into hospitals, ambulatory surgery centers (ASCs), specialty clinics, and home healthcare providers. Hospitals dominate the market due to the high volume of nasal surgeries performed in these settings, supported by advanced surgical equipment and postoperative care. Hospitals are the primary care centers for both trauma-related and elective nasal surgeries, driving the higher demand for nasal splints. The large-scale infrastructure, better access to skilled surgeons, and availability of healthcare reimbursement further cement hospitals' leading position in the market.

North America Nasal Splint Market Competitive Landscape

The North America nasal splint market is dominated by both global and regional players who invest heavily in product innovation, R&D, and distribution networks. The market is characterized by a high level of consolidation, with leading companies holding significant market shares. The North America nasal splint market features a mix of established global players and specialized medical device manufacturers. Key players such as Stryker Corporation, Medtronic Plc, and Boston Scientific Corporation lead the market due to their expansive product portfolios and strong distribution channels. Other players, like Integra LifeSciences and Merocel Corporation, maintain a competitive edge by focusing on niche segments, such as custom splints or advanced materials. These companies are actively involved in strategic mergers, acquisitions, and collaborations to enhance their market presence and develop innovative nasal splint products.

|

Company Name |

Establishment Year |

Headquarters |

Product Range |

R&D Investments |

FDA Approvals |

Revenue (USD Bn) |

Distribution Network |

Market Presence |

|---|---|---|---|---|---|---|---|---|

|

Stryker Corporation |

1941 |

Michigan, USA |

- | - | - | - | - | - |

|

Medtronic Plc |

1949 |

Dublin, Ireland |

- | - | - | - | - | - |

|

Boston Scientific Corporation |

1979 |

Massachusetts, USA |

- | - | - | - | - | - |

|

Integra LifeSciences |

1989 |

New Jersey, USA |

- | - | - | - | - | - |

|

Merocel Corporation |

1982 |

Minnesota, USA |

- | - | - | - | - | - |

North America Nasal Splint Market Analysis

Growth Drivers

- Increasing Rhinoplasty and Nasal Trauma Surgeries: The North American region has seen a significant rise in rhinoplasty and nasal trauma surgeries. According to the American Society of Plastic Surgeons, over 352,000 rhinoplasty procedures were performed in 2023, driven by increased patient demand for both cosmetic and reconstructive purposes. Additionally, nasal injuries due to sports-related incidents are rising, with the CDC reporting over 200,000 sports-related facial injuries annually, prompting a surge in the demand for nasal splints post-surgery.

- Aging Population and Rising Healthcare Expenditure: The elderly population in North America is growing rapidly, with over 54 million people aged 65 and older in 2023, as reported by the U.S. Census Bureau. This demographic is more prone to nasal surgeries due to structural weaknesses, sleep apnea, or trauma. Combined with a projected $4.9 trillion expenditure on healthcare by 2025, the need for advanced medical devices like nasal splints is expected to grow as healthcare access improves.

- Technological Advancements in Medical Devices: Advancements in the materials used for nasal splints, including the development of biocompatible, flexible materials, have improved patient outcomes. In 2023, several medical device companies launched splints made from advanced silicone and memory foam, which can enhance healing and minimize discomfort. With over 6,000 ambulatory surgery centers operational in the U.S. alone, the demand for these next-gen devices is expected to increase substantially.

Market Challenges

- High Costs Associated with Advanced Splint Materials: Advanced nasal splints made from biocompatible materials or those incorporating drug-delivery mechanisms come at a higher cost. In 2023, the average price of a nasal splint using cutting-edge materials ranged between $150 and $500, making it unaffordable for some patients, especially those without comprehensive health insurance coverage. This cost barrier limits the markets penetration, particularly in low-income groups.

- Stringent Regulatory Approvals for New Products: Regulatory requirements by bodies such as the FDA in the U.S. make the introduction of new nasal splint products challenging. In 2023, it was reported that over 30% of medical devices, including nasal splints, faced delays in approvals due to stringent clinical testing requirements. This often delays the launch of new, innovative splints, slowing market growth.

North America Nasal Splint Market Future Outlook

Over the next five years, the North America nasal splint market is expected to show significant growth driven by an increase in outpatient surgeries, technological advancements in nasal splints, and rising awareness of post-surgical care. In addition, the development of biodegradable and 3D-printed splints presents opportunities for growth, especially as patient preferences shift towards more comfortable and sustainable options. The demand for minimally invasive surgeries and enhanced patient care will further fuel market expansion, particularly in urban centers with advanced healthcare infrastructure.

Market Opportunities

- Customization of Nasal Splints Using 3D Printing: The customization of nasal splints through 3D printing technology is opening new avenues for personalized treatment. In 2023, the global market for 3D-printed medical devices surpassed 500,000 units. North American hospitals are increasingly using this technology to create patient-specific nasal splints, improving fit and recovery outcomes. The shift towards personalized medical devices could drive further growth in the nasal splint market.

- Increasing Healthcare Coverage for Nasal Surgeries: Efforts to expand healthcare coverage for reconstructive nasal surgeries are improving market prospects. In 2023, more states in the U.S. began mandating insurance coverage for procedures involving nasal trauma. This shift towards greater coverage could benefit patients requiring post-surgical nasal splints, with over 2 million nasal surgeries expected to be covered annually by 2025.

Scope of the Report

|

By Product Type |

Internal Nasal Splints External Nasal Splints Custom Nasal Splints |

|

By Material Type |

Silicone Thermoplastic Biodegradable Material |

|

By End-User |

Hospitals Ambulatory Surgery Centers Specialty Clinics Home Healthcare Providers |

|

By Distribution Channel |

Direct Sales Distributors E-commerce |

|

By Region |

United States Canada Mexico |

Products

Key Target Audience

Nasal Surgery Clinics

ENT Specialists

Hospital Procurement Departments

Ambulatory Surgery Centers

Home Healthcare Providers

Government and Regulatory Bodies (FDA, Health Canada)

Investors and Venture Capitalist Firms

Medical Device Distributors

Companies

Players Mentioned in the Report:

Stryker Corporation

Medtronic Plc

Boston Scientific Corporation

Integra LifeSciences

Merocel Corporation

Olympus Corporation

Cook Medical Inc.

Karl Storz GmbH

Arthrex Inc.

Innovia Medical

Table of Contents

1. North America Nasal Splint Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Nasal Splint Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Nasal Splint Market Analysis

3.1. Growth Drivers (Patient demand for minimally invasive procedures, increasing awareness of nasal injuries, advancements in splinting materials, growth in outpatient surgeries)

3.1.1. Increasing Rhinoplasty and Nasal Trauma Surgeries

3.1.2. Aging Population and Rising Healthcare Expenditure

3.1.3. Technological Advancements in Medical Devices

3.1.4. Expansion of Ambulatory Surgery Centers

3.2. Market Challenges (Lack of awareness, potential side effects, stringent regulatory requirements, reimbursement challenges)

3.2.1. High Costs Associated with Advanced Splint Materials

3.2.2. Stringent Regulatory Approvals for New Products

3.2.3. Limited Reimbursement Policies for Nasal Surgeries

3.2.4. Limited Penetration in Low-Income Groups

3.3. Opportunities (Customization of splints, increasing insurance coverage, market expansion into pediatric care, technological integration for patient comfort)

3.3.1. Customization of Nasal Splints Using 3D Printing

3.3.2. Increasing Healthcare Coverage for Nasal Surgeries

3.3.3. Expansion in Pediatric Care and ENT Services

3.3.4. Technological Integration for Enhanced Patient Comfort

3.4. Trends (Patient-centric approaches, biodegradable splints, product innovation, telemedicine integration)

3.4.1. Adoption of Patient-Centric Nasal Splinting Solutions

3.4.2. Development of Biodegradable and Absorbable Splints

3.4.3. Increasing Use of Post-Surgical Splints for Nasal Reconstruction

3.4.4. Integration of Telemedicine in Post-Operative Care

3.5. Regulatory Framework

3.5.1. FDA Approval Process for Medical Devices

3.5.2. CE Marking Requirements for Export

3.5.3. HIPAA Compliance in Digital Solutions

3.5.4. Occupational Safety and Health Administration (OSHA) Regulations

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Hospitals, Clinics, Ambulatory Surgery Centers, Home Healthcare Providers)

3.8. Porters Five Forces

3.9. Competitive Landscape (Competitive Intensity, Market Share Distribution, Barriers to Entry, and Exit Strategies)

4. North America Nasal Splint Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Internal Nasal Splints

4.1.2. External Nasal Splints

4.1.3. Custom Nasal Splints

4.2. By Material Type (In Value %)

4.2.1. Silicone

4.2.2. Thermoplastic

4.2.3. Biodegradable Material

4.3. By End-User (In Value %)

4.3.1. Hospitals

4.3.2. Ambulatory Surgery Centers

4.3.3. Specialty Clinics

4.3.4. Home Healthcare Providers

4.4. By Distribution Channel (In Value %)

4.4.1. Direct Sales

4.4.2. Distributors

4.4.3. E-commerce

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5. North America Nasal Splint Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Stryker Corporation

5.1.2. Medtronic Plc

5.1.3. Boston Scientific Corporation

5.1.4. Smith & Nephew Plc

5.1.5. Olympus Corporation

5.1.6. Integra LifeSciences

5.1.7. Merocel Corporation

5.1.8. Innovia Medical

5.1.9. Eon Meditech Pvt Ltd

5.1.10. Mentor Worldwide LLC

5.1.11. Arthrex Inc.

5.1.12. Cook Medical Inc.

5.1.13. Karl Storz GmbH

5.1.14. Summit Medical Inc.

5.1.15. Medasil Surgical Ltd.

5.2. Cross Comparison Parameters (Product Range, Material Innovation, FDA Approvals, Distribution Networks, Manufacturing Capacity, Revenue, R&D Investment, Market Penetration)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Product Launches, Partnerships, Geographical Expansion)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Private Equity Investments

6. North America Nasal Splint Market Regulatory Framework

6.1. FDA Approval Process

6.2. CE Marking Requirements

6.3. Reimbursement Policies

6.4. Medical Device Certification

7. North America Nasal Splint Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Nasal Splint Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Material Type (In Value %)

8.3. By End-User (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9. North America Nasal Splint Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involved the identification of key stakeholders within the North America nasal splint market. Extensive desk research was conducted to gather industry data from secondary and proprietary databases. The primary focus was on identifying variables like product adoption, distribution channels, and regulatory frameworks.

Step 2: Market Analysis and Construction

We collected and analyzed historical data, focusing on market penetration, product performance, and revenue generation. This analysis covered the growth trajectory of the nasal splint market and its adoption across different regions, with a special emphasis on hospitals and outpatient centers.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses about market growth drivers and challenges were formulated and validated through direct consultations with industry experts via CATIs. Feedback from key stakeholders, such as ENT surgeons and medical device manufacturers, provided insights into market trends and operational challenges.

Step 4: Research Synthesis and Final Output

The final stage involved synthesizing data from both top-down and bottom-up approaches, ensuring a robust analysis. Input from major manufacturers, combined with sales data, allowed for a comprehensive assessment of the market's current size and future potential.

Frequently Asked Questions

01. How big is the North America Nasal Splint Market?

The North America nasal splint market is valued at USD 550 million, driven by an increase in rhinoplasty procedures and trauma-related surgeries.

02. What are the challenges in the North America Nasal Splint Market?

Challenges in the North America nasal splint market include stringent regulatory approvals, limited reimbursement policies, and the high cost of advanced nasal splints, which may hinder the market's growth potential.

03. Who are the major players in the North America Nasal Splint Market?

Major players in the North America nasal splint market include Stryker Corporation, Medtronic Plc, Boston Scientific Corporation, Integra LifeSciences, and Merocel Corporation. These companies dominate due to their strong product portfolios and extensive distribution networks.

04. What are the growth drivers of the North America Nasal Splint Market?

Key drivers in the North America nasal splint market include the rise in cosmetic and reconstructive nasal surgeries, advancements in post-surgical care technology, and the growing preference for minimally invasive procedures.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.