North America Non-lethal Weapons Market Outlook to 2030

Region:North America

Author(s):Mukul

Product Code:KROD6319

October 2024

99

About the Report

North America Non-lethal Weapons Market Overview

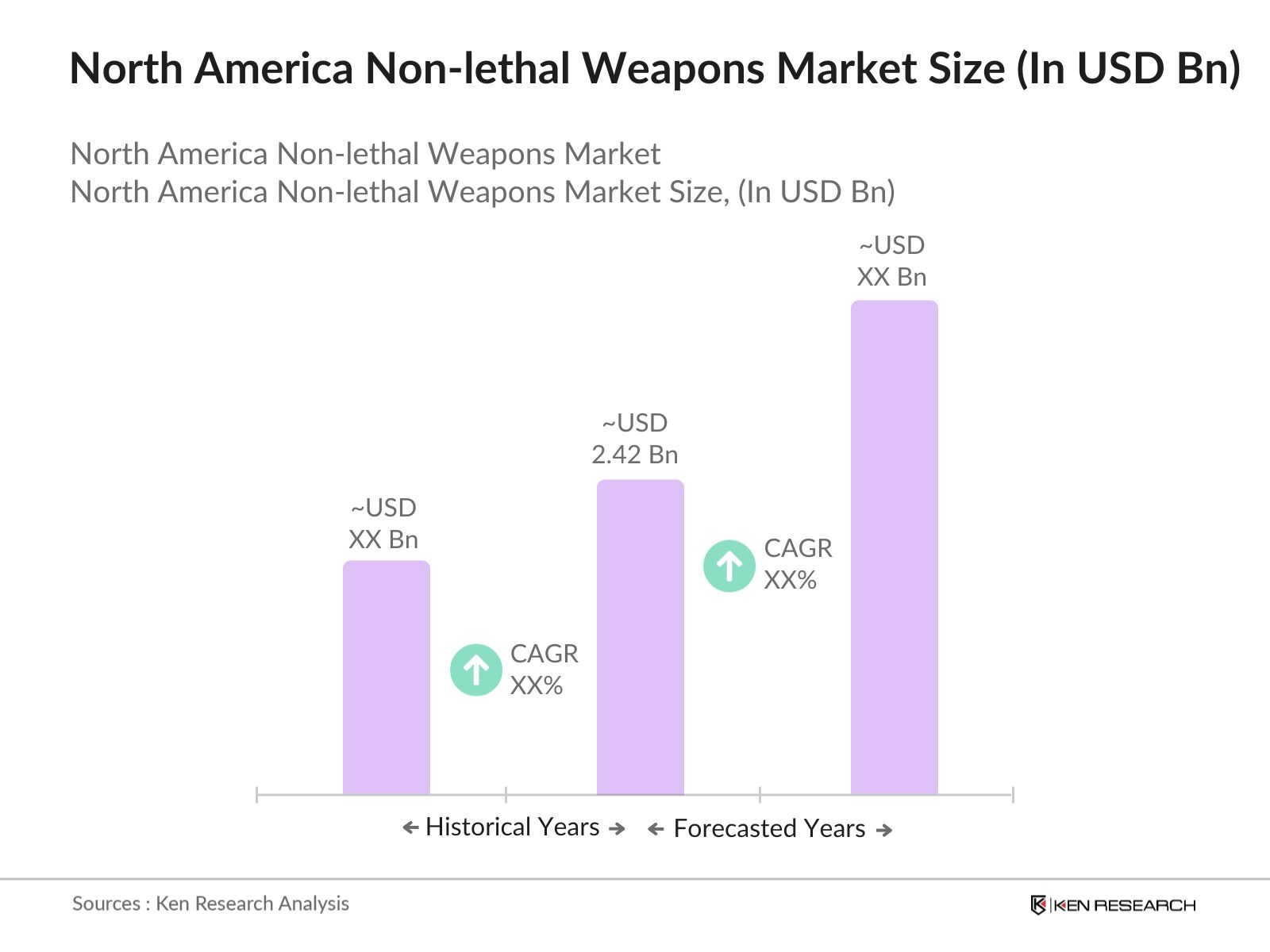

- The North America non-lethal weapons market is valued at USD 2.42 billion, with demand driven by increasing adoption across law enforcement, military, and civilian security. The market growth is fueled by the rising need for crowd control during civil unrest and the growing trend of militarization among police forces. Non-lethal weapons offer a less damaging alternative compared to lethal options, making them ideal for situations where the use of deadly force would be inappropriate. Significant advancements in technology, including directed energy and electric shock devices, further support market growth, particularly in the United States.

- The market is dominated by the United States, driven by its large defense budget, heavy investment in law enforcement, and extensive research in weapon innovation. Major cities such as New York, Los Angeles, and Chicago witness higher adoption due to increased civil disturbances and the need for effective crowd control measures. Canada follows, with its focus on modernizing its defense and law enforcement systems, which increases demand for non-lethal weapons in both urban and rural settings.

- Federal and state-level regulations governing the use of non-lethal weapons have become more stringent. In 2023, the U.S. Department of Justice issued updated guidelines requiring law enforcement agencies to report incidents where non-lethal weapons are deployed. States like California and New York have introduced additional compliance tracking measures to ensure that these weapons are used appropriately and within legal frameworks. This regulatory tightening reflects concerns over potential misuse and the need for more transparency in non-lethal weapon deployments.

North America Non-lethal Weapons Market Segmentation

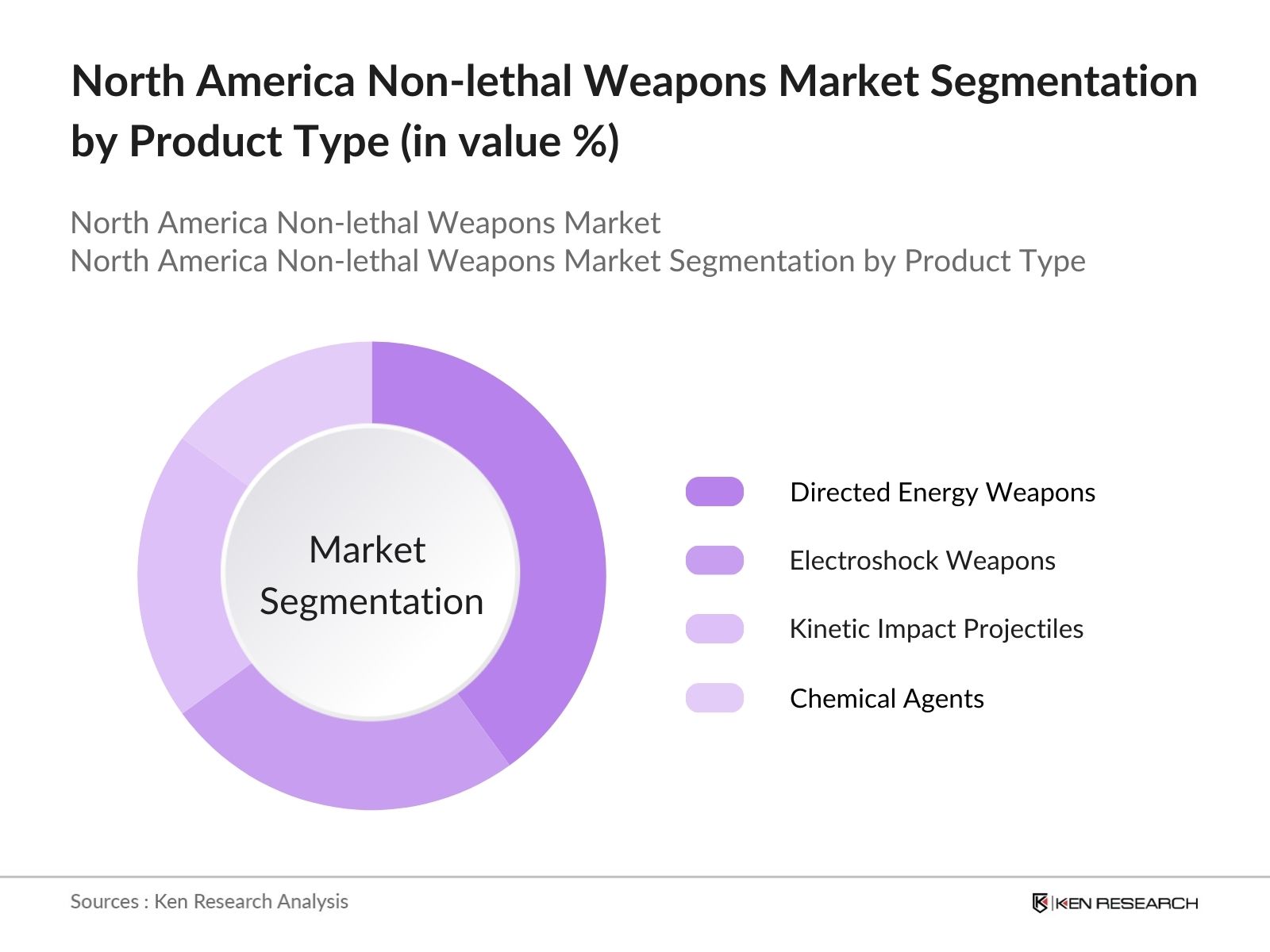

- By Product Type: The North America non-lethal weapons market is segmented by product type into directed energy weapons, electroshock weapons, kinetic impact projectiles, chemical agents, and acoustic devices. Directed energy weapons currently dominate this segmentation due to their cutting-edge technology and the ability to incapacitate targets without physical contact. Their non-kinetic nature, coupled with precision targeting, makes them highly suitable for law enforcement and military operations, where minimizing harm is crucial. Electroshock weapons, including tasers, follow closely due to their widespread use in policing.

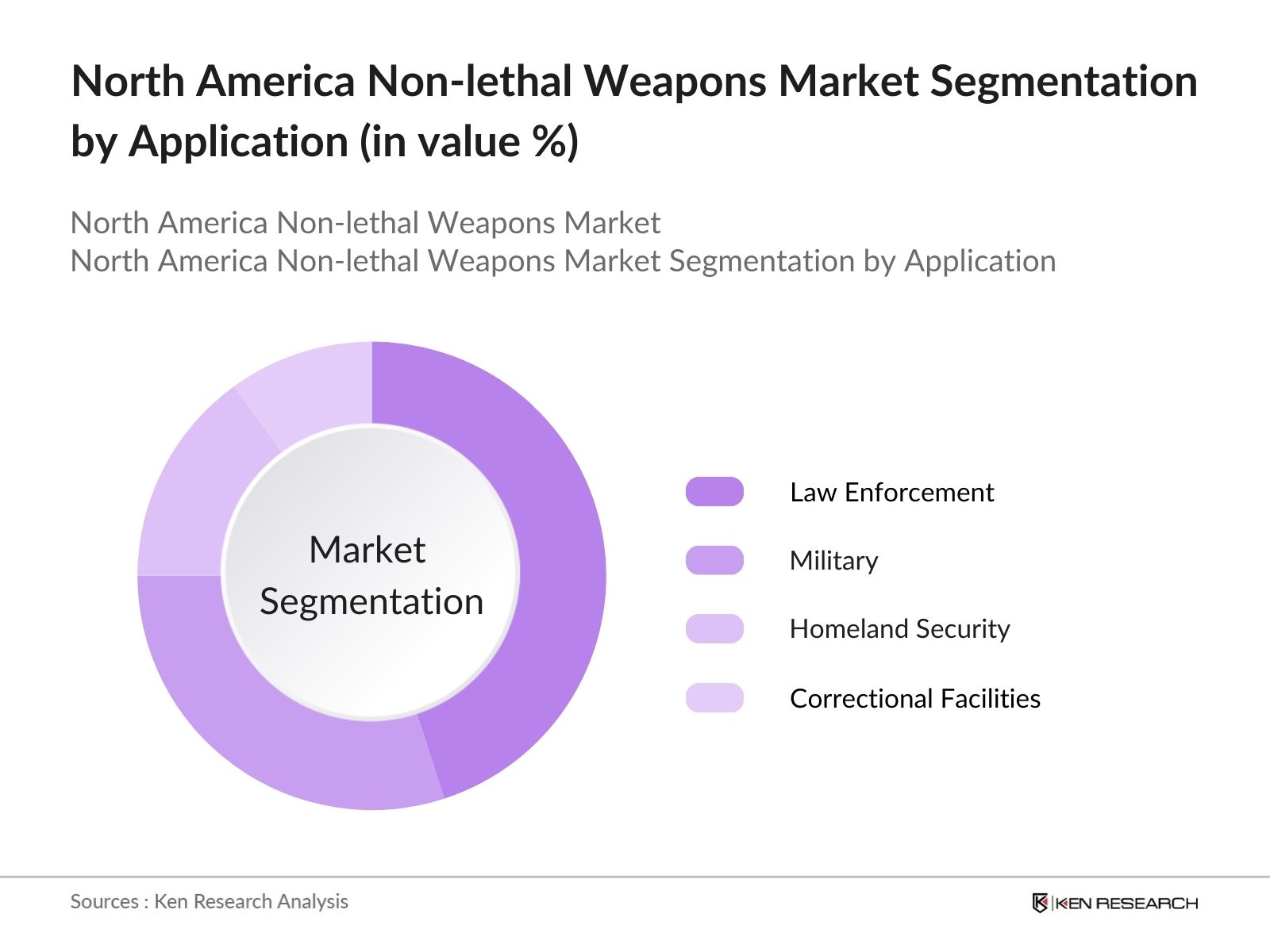

- By Application: The North America non-lethal weapons market is further segmented by application into law enforcement, military, homeland security, correctional facilities, and civilian use. Law enforcement holds a dominant share, with a large portion of non-lethal weapons being procured for riot control, arrests, and incapacitating violent suspects. The U.S. police forces extensively use non-lethal tools like tasers and pepper spray, particularly in urban centers facing higher crime rates. The military segment follows due to the growing deployment of non-lethal options in peacekeeping missions and crowd control during conflict scenarios.

North America Non-lethal Weapons Market Competitive Landscape

The North American non-lethal weapons market is highly competitive, with a few dominant players driving most of the innovation and sales. Companies such as Axon Enterprise, BAE Systems, and Raytheon Technologies lead the market, primarily due to their strong research and development capabilities and established relationships with defense agencies. The market's competitive landscape is characterized by collaborations between major defense contractors and government bodies, aiming to meet the rising demand for non-lethal solutions in both domestic and international markets.

|

Company Name |

Establishment Year |

Headquarters |

Product Range |

Revenue (USD) |

R&D Expenditure |

Government Contracts |

Key Partnerships |

Technological Innovations |

|

Axon Enterprise, Inc. |

1993 |

Scottsdale, Arizona |

||||||

|

BAE Systems Plc |

1999 |

Farnborough, UK |

||||||

|

Raytheon Technologies Corp |

2020 |

Waltham, Massachusetts |

||||||

|

General Dynamics Corp |

1952 |

Reston, Virginia |

||||||

|

Leonardo S.p.A |

1948 |

Rome, Italy |

North America Non-lethal Weapons Industry Analysis

Market Growth Drivers

- Increased Law Enforcement and Military Use: Law enforcement agencies and military units across North America have increasingly adopted non-lethal weapons to handle a range of situations. In 2024, over 85% of police departments in the United States, according to the U.S. Bureau of Justice Statistics, reported the use of non-lethal weapons such as tasers and rubber bullets. The U.S. Department of Defense has also scaled its usage of non-lethal options, reflecting their importance in minimizing casualties during operations. Military training in non-lethal technologies has expanded to include crowd control and de-escalation tactics, reinforcing this trend in both military and civilian applications.

- Growing Civil Unrest and Public Protests: Civil unrest and public protests have surged in North America, driving the demand for non-lethal crowd control measures. The U.S. saw over 10,000 protests in 2023 alone, according to data from the Armed Conflict Location & Event Data Project (ACLED). Canadian cities experienced a 35% rise in public demonstrations between 2022 and 2023. These events have heightened the need for non-lethal solutions that ensure crowd management without causing long-term harm. The deployment of tear gas, water cannons, and stun guns has become a common response in handling large-scale protests across the region.

- Technological Advancements: The non-lethal weapons sector in North America has witnessed significant technological advancements. Directed energy weapons, like Active Denial Systems, have gained prominence due to their ability to disperse crowds from a distance. In 2024, the U.S. Army Research Laboratory reported investments in non-lethal lasers and other cutting-edge technologies. The development of smart weapons that can adjust intensity based on a subjects behavior has also seen widespread interest, as agencies look for more effective solutions to control crowds and handle threats without causing permanent damage.

Market Restraints

- Public Concerns About Safety: Public sentiment regarding the safety of non-lethal weapons remains a significant challenge. According to the U.S. Department of Justice's Community Oriented Policing Services (COPS) report, public confidence in non-lethal weapons was only 65% in 2023, as concerns about improper use and potential for injury persist. High-profile incidents involving misapplication have sparked public debate, fueling skepticism around the deployment of these weapons in crowd control situations. Striking a balance between effective law enforcement and ensuring minimal harm to civilians remains a delicate task for authorities.

- High Cost of Advanced Non-lethal Weapons: The high costs associated with advanced non-lethal weapons are a deterrent for widespread adoption. For example, an Active Denial System can cost over $1 million per unit, as reported by the U.S. Government Accountability Office (GAO) in 2024. This puts a strain on municipal budgets, particularly in smaller cities with fewer financial resources. Even less advanced options like electroshock weapons can cost hundreds of dollars per unit, limiting procurement. The high costs relative to traditional firearms mean that adoption is often delayed despite the potential safety benefits of non-lethal systems.

North America Non-lethal Weapons Market Future Outlook

The North American non-lethal weapons market is expected to continue its upward trajectory over the coming years, propelled by increased government investment in public safety and defense modernization. Law enforcement agencies are likely to prioritize non-lethal solutions in response to rising public scrutiny and calls for less violent alternatives. Additionally, technological advancements in directed energy and electroshock weapons will play a crucial role in driving further market adoption across both military and civilian applications. The development of drone-based non-lethal systems is also anticipated to gain significant traction in the market, catering to crowd control needs in urban environments.

Market Opportunities

- Growing Use in Correctional Facilities: The use of non-lethal weapons in correctional facilities has expanded in North America. In 2024, the U.S. Federal Bureau of Prisons reported that 60% of correctional institutions had implemented non-lethal solutions such as tasers and pepper spray to manage inmate behavior. The adoption rate is expected to rise as prisons increasingly prioritize de-escalation tactics over physical confrontations. This shift towards non-lethal solutions is seen as a way to reduce injuries among inmates and staff, while also addressing concerns about excessive force in correctional settings.

- New Government Initiatives for Public Safety: Government initiatives aimed at enhancing public safety have opened new avenues for the adoption of non-lethal weapons. In 2024, the U.S. Congress allocated $500 million through the National Defense Authorization Act (NDAA) for non-lethal weapon procurement by law enforcement agencies, emphasizing crowd control and de-escalation measures. Similar initiatives were introduced in Canada, where provincial governments allocated grants to local police forces for non-lethal weapon acquisition. These initiatives underscore a growing legislative support for equipping law enforcement with alternatives to lethal force.

Scope of the Report

|

By Product Type |

Directed Energy Weapons, Electroshock Weapons, Kinetic Impact Projectiles, Chemical Agents, Acoustic Devices |

|

By Application |

Law Enforcement, Military, Homeland Security, Correctional Facilities, Civilian Use |

|

By Technology |

Mechanical and Kinetic Non-lethal Weapons, Electrical and Shock Weapons, Chemical Non-lethal Weapons, Acoustics and Ultrasound Weapons |

|

By Deployment Type |

Handheld Devices, Vehicle-mounted Devices, Drone-mounted Devices |

|

By Region |

United States, Canada, Mexico |

Products

Key Target Audience

Law Enforcement Agencies (U.S. Police Departments)

Military and Defense Organizations (U.S. Department of Defense)

Homeland Security and Border Control Agencies (DHS)

Correctional Facilities

Civilian Security Companies

Private Security Firms

Investment and Venture Capitalist Firms

Government and Regulatory Bodies (NATO, Federal Bureau of Investigation)

Companies

Players Mentioned in the Report:

Axon Enterprise, Inc.

BAE Systems Plc

Raytheon Technologies Corporation

General Dynamics Corporation

Leonardo S.p.A

Rheinmetall AG

The Boeing Company

KRATOS Defense & Security Solutions

Safariland, LLC

Heckler & Koch GmbH

Combined Systems, Inc.

Lamperd Less Lethal Inc.

FN Herstal

ISPRA Ltd.

TASER International

Table of Contents

1. North America Non-lethal Weapons Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Non-lethal Weapons Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Non-lethal Weapons Market Analysis

3.1. Growth Drivers

3.1.1. Increased Law Enforcement and Military Use (Adoption rate)

3.1.2. Growing Civil Unrest and Public Protests (Incidents count)

3.1.3. Technological Advancements (Product innovations)

3.1.4. Rising Demand for Crowd Control Weapons (Demand spikes in urban centers)

3.2. Market Challenges

3.2.1. Public Concerns About Safety (Public sentiment index)

3.2.2. High Cost of Advanced Non-lethal Weapons (Cost comparison index)

3.2.3. Complex Legal and Regulatory Landscape (Compliance requirements)

3.3. Opportunities

3.3.1. Growing Use in Correctional Facilities (Penetration rate in corrections)

3.3.2. New Government Initiatives for Public Safety (Legislative support for deployment)

3.3.3. Partnerships with Defense Organizations (Strategic collaborations)

3.4. Trends

3.4.1. Increasing Use of Directed Energy Weapons (Technological development index)

3.4.2. Demand for De-escalation Tools (Equipment purchase orders by government agencies)

3.4.3. Use of Drone-Based Non-lethal Weapons (Integration with UAV systems)

3.5. Government Regulation

3.5.1. National Defense Authorization Act Provisions (Non-lethal weapons procurement clauses)

3.5.2. Federal and State-Level Regulations (Compliance tracking)

3.5.3. Public Safety Programs (Grants and funding allocations)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.7.1. Suppliers (List of major suppliers)

3.7.2. Manufacturers (Non-lethal weapon producers)

3.7.3. End Users (Law enforcement, military, private security)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. North America Non-lethal Weapons Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Directed Energy Weapons

4.1.2. Electroshock Weapons

4.1.3. Kinetic Impact Projectiles

4.1.4. Chemical Agents

4.1.5. Acoustic Devices

4.2. By Application (In Value %)

4.2.1. Law Enforcement

4.2.2. Military

4.2.3. Homeland Security

4.2.4. Correctional Facilities

4.2.5. Civilian Use

4.3. By Technology (In Value %)

4.3.1. Mechanical and Kinetic Non-lethal Weapons

4.3.2. Electrical and Shock Weapons

4.3.3. Chemical Non-lethal Weapons

4.3.4. Acoustics and Ultrasound Weapons

4.4. By Deployment Type (In Value %)

4.4.1. Handheld Devices

4.4.2. Vehicle-mounted Devices

4.4.3. Drone-mounted Devices

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5. North America Non-lethal Weapons Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Axon Enterprise, Inc.

5.1.2. BAE Systems Plc

5.1.3. Raytheon Technologies Corporation

5.1.4. General Dynamics Corporation

5.1.5. Leonardo S.p.A

5.1.6. Rheinmetall AG

5.1.7. The Boeing Company

5.1.8. KRATOS Defense & Security Solutions

5.1.9. Safariland, LLC

5.1.10. Heckler & Koch GmbH

5.1.11. Combined Systems, Inc.

5.1.12. Lamperd Less Lethal Inc.

5.1.13. FN Herstal

5.1.14. ISPRA Ltd.

5.1.15. TASER International

5.2 Cross Comparison Parameters

5.2.1. Product Portfolio

5.2.2. Technology Innovations

5.2.3. Geographical Reach

5.2.4. Manufacturing Capacity

5.2.5. Revenue

5.2.6. R&D Investments

5.2.7. Partnerships and Collaborations

5.2.8. Government Contracts

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. North America Non-lethal Weapons Market Regulatory Framework

6.1. Federal Non-lethal Weapon Policies

6.2. Compliance Requirements for Manufacturers

6.3. Import and Export Regulations

7. North America Non-lethal Weapons Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Non-lethal Weapons Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By Deployment Type (In Value %)

8.5. By Region (In Value %)

9. North America Non-lethal Weapons Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial stage involves identifying the key variables that influence the North America non-lethal weapons market. This includes product types, technology adoption rates, and procurement patterns. Extensive secondary research from verified government databases is used to gather initial insights into market dynamics.

Step 2: Market Analysis and Construction

This phase involves a detailed examination of market size and segmentation, focusing on historical data related to non-lethal weapons adoption. Data is cross-referenced with industry reports, government procurement records, and company disclosures to ensure accuracy in market assessments.

Step 3: Hypothesis Validation and Expert Consultation

In this step, consultations with key stakeholders in the industry are conducted to validate market hypotheses. This includes interviews with representatives from law enforcement agencies, military officials, and defense contractors. These discussions provide deeper insights into the market's competitive landscape and future growth prospects.

Step 4: Research Synthesis and Final Output

The final phase compiles all research findings, expert insights, and data points to provide a comprehensive view of the non-lethal weapons market. This synthesis allows for the creation of validated market projections and the identification of key growth areas, ensuring a robust and reliable report.

Frequently Asked Questions

01. How big is the North America non-lethal weapons market?

The North America non-lethal weapons market is valued at USD 2.42 billion, driven by increasing demand from law enforcement, military, and civilian security forces. The growth in the market is further fueled by rising civil unrest and the need for less lethal options.

02. What are the challenges in the North America non-lethal weapons market?

Challenges in the market include public concerns over the safety and misuse of non-lethal weapons, high production costs, and strict regulatory compliance across different states and countries. Furthermore, ensuring the right balance between effective incapacitation and reduced harm remains a challenge for manufacturers.

03. Who are the major players in the North America non-lethal weapons market?

Key players in the market include Axon Enterprise, Inc., BAE Systems Plc, Raytheon Technologies Corporation, General Dynamics Corporation, and Leonardo S.p.A. These companies dominate the market due to their strong technological innovation and extensive defense contracts.

04. What are the growth drivers of the North America non-lethal weapons market?

Growth is driven by increased government spending on public safety, rising civil unrest, and the militarization of police forces. Additionally, the introduction of technologically advanced weapons such as directed energy systems has significantly increased adoption rates.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.