North America Population Health Management Market Outlook to 2030

Region:North America

Author(s):Naman Rohilla

Product Code:KROD8411

December 2024

91

About the Report

North America Population Health Management Market Overview

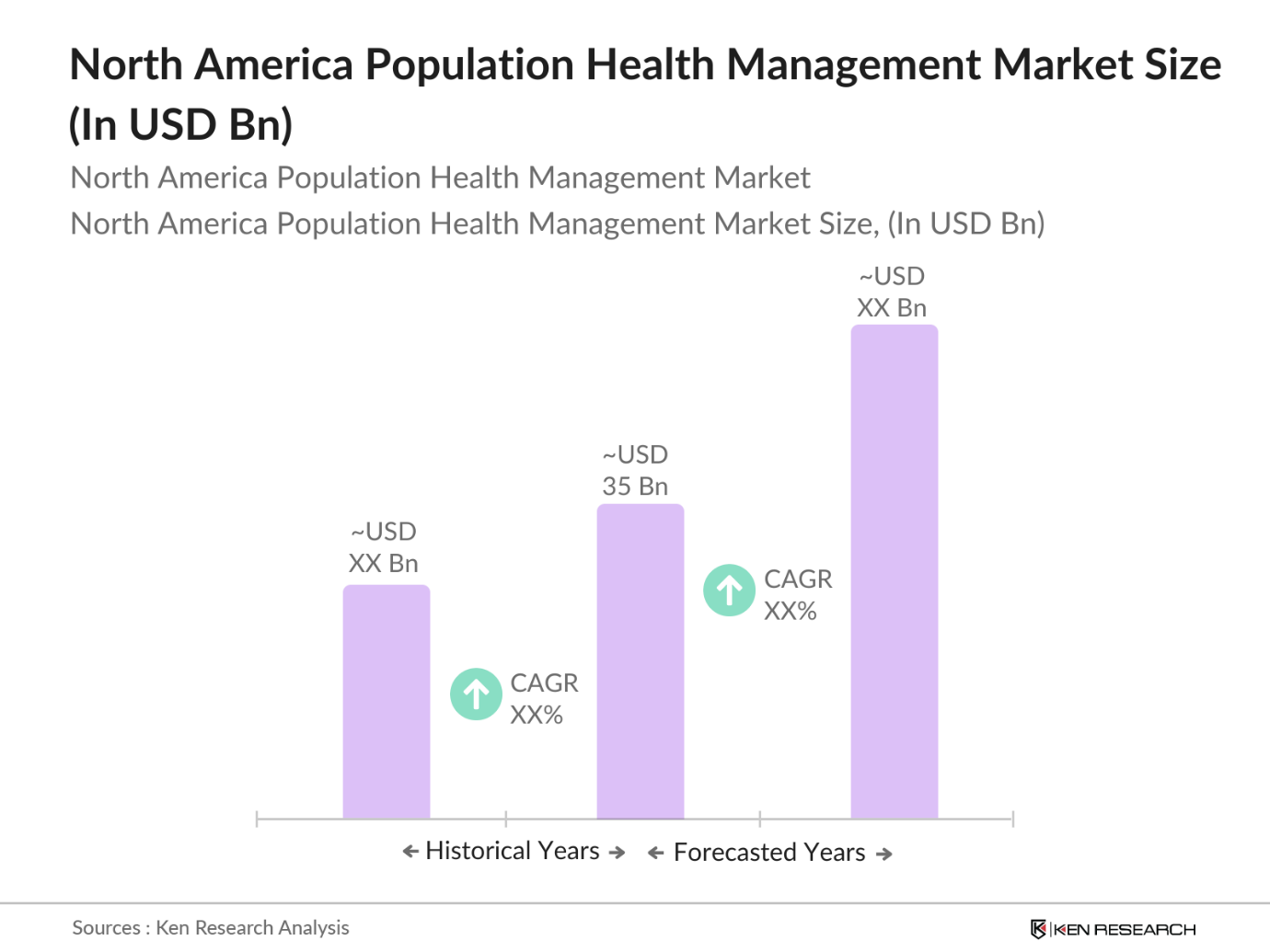

- The North America Population Health Management (PHM) market, currently valued at USD 35 billion, has experienced steady growth driven by the increasing adoption of integrated healthcare technologies and the need to manage the high incidence of chronic diseases. The sector is primarily influenced by advanced data integration technologies, cloud-based platforms, and analytics that streamline healthcare provider workflows and reduce medical costs. The shift towards value-based care models has propelled demand for PHM solutions as they enable healthcare providers to better manage population health metrics while simultaneously lowering costs through efficient disease management practices.

- The market in North America is largely dominated by the United States, where investment in healthcare technology and government policies, such as the Affordable Care Act, support the expansion of PHM systems. This dominance stems from the U.S. being a major hub for healthcare technology innovation, with many companies based there continuously enhancing PHM solutions with features like electronic health record (EHR) integration and big data analytics. Canada also contributes to this growth due to its expanding healthcare IT infrastructure and focus on chronic disease prevention.

- The Affordable Care Act (ACA) remains a pillar of PHM by incentivizing preventive care and mandating adherence to value-based care standards across healthcare providers. These mandates align with PHMs objective of reducing hospital readmissions and improving care coordination. In 2024, these ACA-driven initiatives directly support the uptake of PHM systems, as organizations seek compliance with the ACAs outcome-based frameworks to qualify for government reimbursements.

North America Population Health Management Market Segmentation

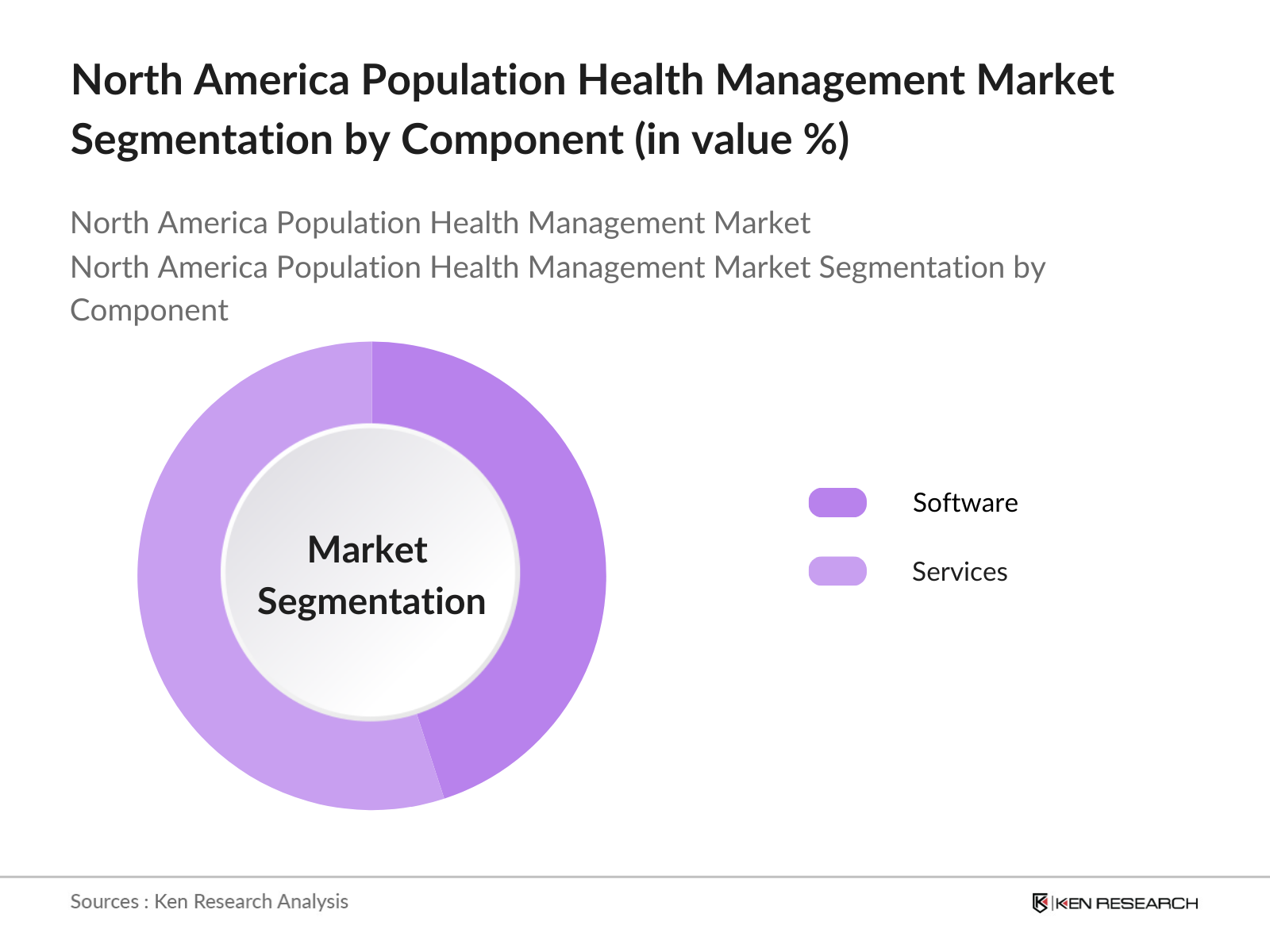

- By Component: The PHM market is segmented by component into Software and Services. Services, including post-sale maintenance, consulting, and implementation, have a substantial market share due to the increasing demand among healthcare providers for support in integrating and maintaining PHM systems. Services are integral to the market as they enable healthcare providers to optimize their workflow with customized solutions that enhance data accuracy and patient outcomes. The complexity and scale of these implementations often require extensive support, making services a critical segment within the PHM market.

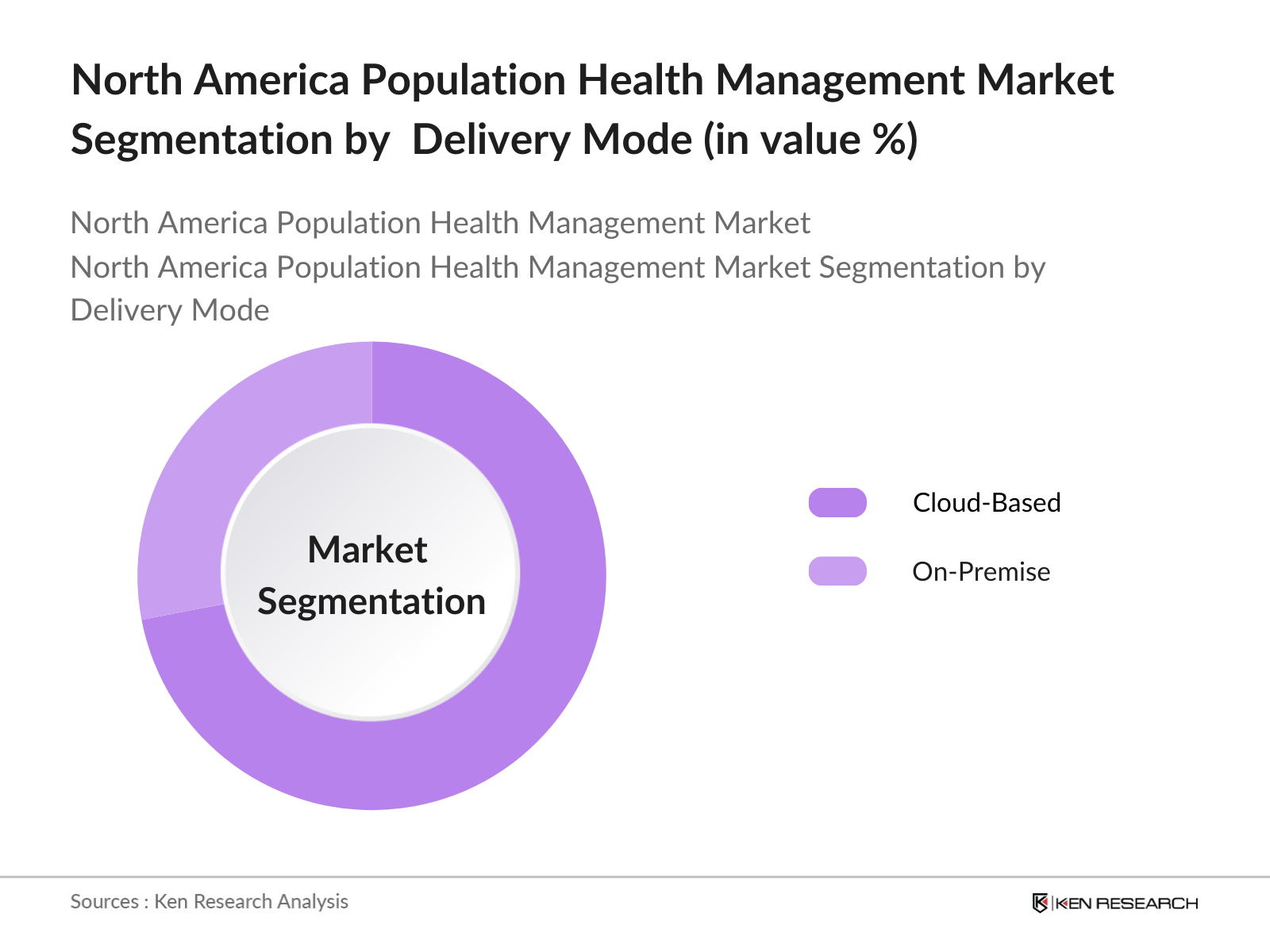

- By Delivery Mode: The market is further segmented by delivery mode into Cloud-Based and On-Premise solutions. Cloud-based solutions hold a dominant market position because they enable healthcare providers to access and analyze patient data from various locations seamlessly. Cloud systems are particularly favored for their flexibility, scalability, and cost-efficiency, which are essential as healthcare organizations seek to expand data storage capacities while maintaining secure and compliant systems. This accessibility supports continuous data integration, essential for achieving population health goals efficiently.

North America Population Health Management Market Competitive Landscape

The North America PHM market is highly competitive, with several key players contributing to innovation and the widespread adoption of PHM solutions. Leading companies have leveraged strategic partnerships, mergers, and product advancements to maintain a stronghold in the market. This competitive environment underscores the dominance of global brands and large healthcare technology firms, which drive industry standards through their extensive R&D investments and comprehensive solution offerings.

North America Population Health Management Market Analysis

North America Population Health Management Market Growth Drivers

- Rising Prevalence of Chronic Diseases: Chronic diseases like diabetes and heart disease continue to impact North America's population health substantially, with chronic conditions now accounting for over 80 million cases across the U.S. alone, as recorded by the CDC in 2024. This increasing chronic disease burden is a critical driver for population health management (PHM), as healthcare systems prioritize preventive and long-term management solutions to mitigate hospitalization rates and enhance patient outcomes. With non-communicable diseases contributing to a notable portion of healthcare expenditure, the focus on PHM has intensified across the region.

- Increasing Adoption of IT Solutions in Healthcare: IT integration within North American healthcare is rapidly advancing, with health information technology infrastructure investments reaching nearly $25 billion in the U.S. by 2024, as per the National Health IT report. This adoption supports the deployment of electronic health records, digital monitoring systems, and telehealth, which are foundational to PHM's effectiveness. By enabling real-time patient tracking and predictive analytics, IT solutions facilitate proactive patient engagement and personalized care delivery, essential for managing population health efficiently.

- Favorable Government Regulations: The Affordable Care Act (ACA) and value-based care programs continue to push the PHM market forward. In 2024, over 40% of Medicare spending is tied to value-based contracts that emphasize quality care over volume, prompting providers to adopt PHM strategies to meet performance standards and lower readmission penalties. These policies encourage the integration of preventive care, chronic disease management, and coordinated care approaches. Additionally, the U.S. Department of Health and Human Services (HHS) mandates reporting for various population health metrics, further embedding PHM practices in healthcare operations.

North America Population Health Management Market Challenges

- High Costs of PHM Solutions and Training: The high financial requirements for deploying and maintaining PHM solutions remain a major barrier. In 2024, an average mid-sized hospital in North America faces installation costs of up to $1.5 million for PHM systems, compounded by ongoing costs for software updates and staff training. This expense can strain healthcare providers, especially in small and rural facilities with limited budgets, hampering their ability to invest in full-scale PHM initiatives.

- Data Integration and Interoperability Challenges: Interoperability remains a pressing issue, as less than 50% of healthcare systems in North America report seamless data sharing across platforms, per HHS data. This lack of standardization hinders PHM efficacy, as inconsistent patient data flows compromise coordinated care. Efforts are ongoing to standardize data protocols, but disparate systems, vendor-specific limitations, and privacy concerns create substantial challenges. Effective interoperability is crucial for cohesive data analytics, which underpins population health strategies.

North America Population Health Management Market Future Outlook

The North America Population Health Management market is poised for robust growth over the next five years, driven by advancements in healthcare data analytics, increased adoption of telehealth solutions, and continuous government support for value-based care. Healthcare providers are likely to further integrate predictive analytics and patient engagement tools, supported by the expansion of cloud technologies that simplify data access and management. This trend reflects a market that increasingly values preventive healthcare and personalized medicine, which PHM solutions make possible on a large scale.

North America Population Health Management Market Opportunities

- Telemedicine and Telehealth Expansion: Telehealth utilization in North America has increased by nearly 30% since 2022, with 2024 seeing consistent demand as patients seek accessible healthcare solutions, particularly for chronic condition management. This shift has prompted healthcare providers to integrate PHM frameworks that support telemedicine for remote patient monitoring, continuous care, and engagement. By reducing geographical and logistical barriers, telehealth offers PHM a powerful tool for enhancing patient outcomes across diverse populations.

- Advances in Data Analytics and AI Integration: North Americas healthcare sector is adopting AI-powered data analytics, with over 60% of major health organizations leveraging AI in 2024 for predictive analytics and risk stratification. PHM systems use these technologies to identify high-risk patients and anticipate future health needs, enabling proactive, data-driven care approaches. AIs role in PHM, especially in real-time health status monitoring and early disease detection, is expected to streamline clinical decision-making and bolster personalized care.

Scope of the Report

Component | Software Services (Consulting, Maintenance, Training) |

Delivery Mode | Cloud-based On-premise |

End-User | Healthcare Providers Payers Employer Groups Government Bodies |

Application | Chronic Disease Management Preventive Health Care Coordination |

Region | United States Canada |

Products

Key Target Audience

Healthcare Providers (Hospitals, Clinics)

Government and Regulatory Bodies (Centers for Medicare & Medicaid Services, U.S. Department of Health and Human Services)

Private and Public Payers

Healthcare Technology Providers

Banks and Financial Intitutions

Medical Equipment Manufacturers

Investor and Venture Capitalist Firms

Healthcare IT Consultants

Employer Groups Seeking Population Health Insights

Companies

Players Mentioned in the Report

Allscripts Healthcare Solutions

Cerner Corporation

Optum Inc.

McKesson Corporation

Philips Healthcare

Veradigm LLC

Athenahealth Inc.

IBM (Watson Health)

eClinicalWorks

Epic Systems Corporation

Table of Contents

1. North America Population Health Management Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Key Market Drivers and Restraints

2. North America Population Health Management Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Growth Rate Analysis

2.3 Key Market Developments and Milestones

3. North America Population Health Management Market Analysis

3.1 Growth Drivers (Chronic Disease Management, Healthcare Digitalization, Regulatory Mandates)

3.1.1 Rising prevalence of chronic diseases

3.1.2 Increasing adoption of IT solutions in healthcare

3.1.3 Favorable government regulations (ACA, Value-based Care Initiatives)

3.1.4 Integration of Electronic Health Records (EHRs)

3.2 Market Challenges (Cost, Interoperability, Data Management)

3.2.1 High costs of PHM solutions and training

3.2.2 Data integration and interoperability challenges

3.2.3 Lack of skilled professionals and technical support

3.3 Opportunities (Telehealth, Big Data, Remote Monitoring)

3.3.1 Telemedicine and telehealth expansion

3.3.2 Advances in data analytics and AI integration

3.3.3 Growing demand for personalized healthcare

3.4 Trends (Cloud-based Solutions, Wearable Technology)

3.4.1 Transition to cloud-based PHM solutions

3.4.2 Adoption of wearable health devices

3.4.3 Rise in mobile health applications

3.5 Government Regulation (Compliance Standards, Healthcare Reforms)

3.5.1 ACA mandates and compliance with healthcare reforms

3.5.2 Data privacy and security regulations (HIPAA)

3.5.3 Initiatives to reduce healthcare costs and improve patient outcomes

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

4. North America Population Health Management Market Segmentation

4.1 By Component (In Value %)

4.1.1 Software

4.1.2 Services (Consulting, Maintenance, Training)

4.2 By Delivery Mode (In Value %)

4.2.1 Cloud-based

4.2.2 On-premise

4.3 By End-User (In Value %)

4.3.1 Healthcare Providers

4.3.2 Payers (Public and Private)

4.3.3 Employer Groups

4.3.4 Government Bodies

4.4 By Application (In Value %)

4.4.1 Chronic Disease Management

4.4.2 Preventive Health and Wellness

4.4.3 Care Coordination and Patient Engagement

4.5 By Region (In Value %)

4.5.1 United States

4.5.2 Canada

5. North America Population Health Management Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Allscripts Healthcare Solutions Inc.

5.1.2 Cerner Corporation

5.1.3 eClinicalWorks

5.1.4 McKesson Corporation

5.1.5 IBM (Watson Health)

5.1.6 Health Catalyst

5.1.7 Philips Healthcare

5.1.8 Optum (UnitedHealth Group)

5.1.9 Athenahealth

5.1.10 NextGen Healthcare

5.1.11 Medecision

5.1.12 Epic Systems Corporation

5.1.13 Welltok (Virgin Pulse)

5.1.14 Conifer Health Solutions

5.1.15 Veradigm LLC

5.2 Cross Comparison Parameters (Revenue, Employees, Services, Technology Solutions, Market Presence, Strategic Initiatives, Partnerships, Mergers & Acquisitions)

6. North America Population Health Management Market Regulatory Framework

6.1 Healthcare Legislation (ACA, Medicare, Medicaid)

6.2 Data Security and Privacy (HIPAA Compliance)

6.3 Value-Based Care Initiatives

7. North America Population Health Management Future Market Projections

7.1 Projected Market Size

7.2 Growth Opportunities

8. North America Population Health Management Market Segmentation

8.1 By Component (In Value %)

8.2 By Delivery Mode (In Value %)

8.3 By End-User (In Value %)

8.4 By Application (In Value %)

8.5 By Region (In Value %)

9. Market Analyst Recommendations

9.1 Customer Cohort Analysis

9.2 Marketing Strategies and Initiatives

9.3 White Space Opportunities

9.4 Value Chain Enhancement

DisclaimerContact UsResearch Methodology

Step 1: Identification of Key Variables

This initial step involves mapping out critical stakeholders within the North America PHM ecosystem, including providers, technology firms, and regulatory agencies. Primary and secondary data sources are utilized to assess variables influencing market demand and technology adoption trends.

Step 2: Market Analysis and Construction

In this stage, historical market data is compiled to understand revenue flows within the PHM sector. Analysis includes the evaluation of core service segments, such as software and services, and their respective adoption rates across healthcare institutions.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses around market trends and growth drivers are developed and validated through consultations with industry experts. Interviews are conducted with senior professionals from PHM providers to assess market sentiment and gain insights on regulatory impacts and technology adoption.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing findings from direct stakeholder consultations and data analysis to provide a validated market assessment. This ensures a comprehensive, data-backed outlook on current trends and projected growth pathways in the North America PHM market.

Frequently Asked Questions

01. How big is the North America Population Health Management Market?

The North America Population Health Management Market, valued at USD 35 billion, is driven by healthcare digitalization, regulatory support, and the rising demand for efficient patient care solutions.

02. What are the challenges in the North America Population Health Management Market?

Challenges include high costs associated with implementation, interoperability issues across systems, and the need for skilled healthcare IT professionals.

03. Who are the major players in the North America Population Health Management Market?

Key players include Allscripts Healthcare Solutions, Cerner Corporation, Optum Inc., McKesson Corporation, and Philips Healthcare, leading through technological advancements and market expansion strategies.

04. What are the growth drivers in the North America Population Health Management Market?

The market is propelled by government initiatives promoting value-based care, the adoption of advanced data analytics, and increasing demand for remote monitoring technologies.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.