North America Retail Vending Machine Market Outlook to 2030

Region:North America

Author(s):Sanjeev

Product Code:KROD4628

October 2024

89

About the Report

North America Retail Vending Machine Market Overview

-

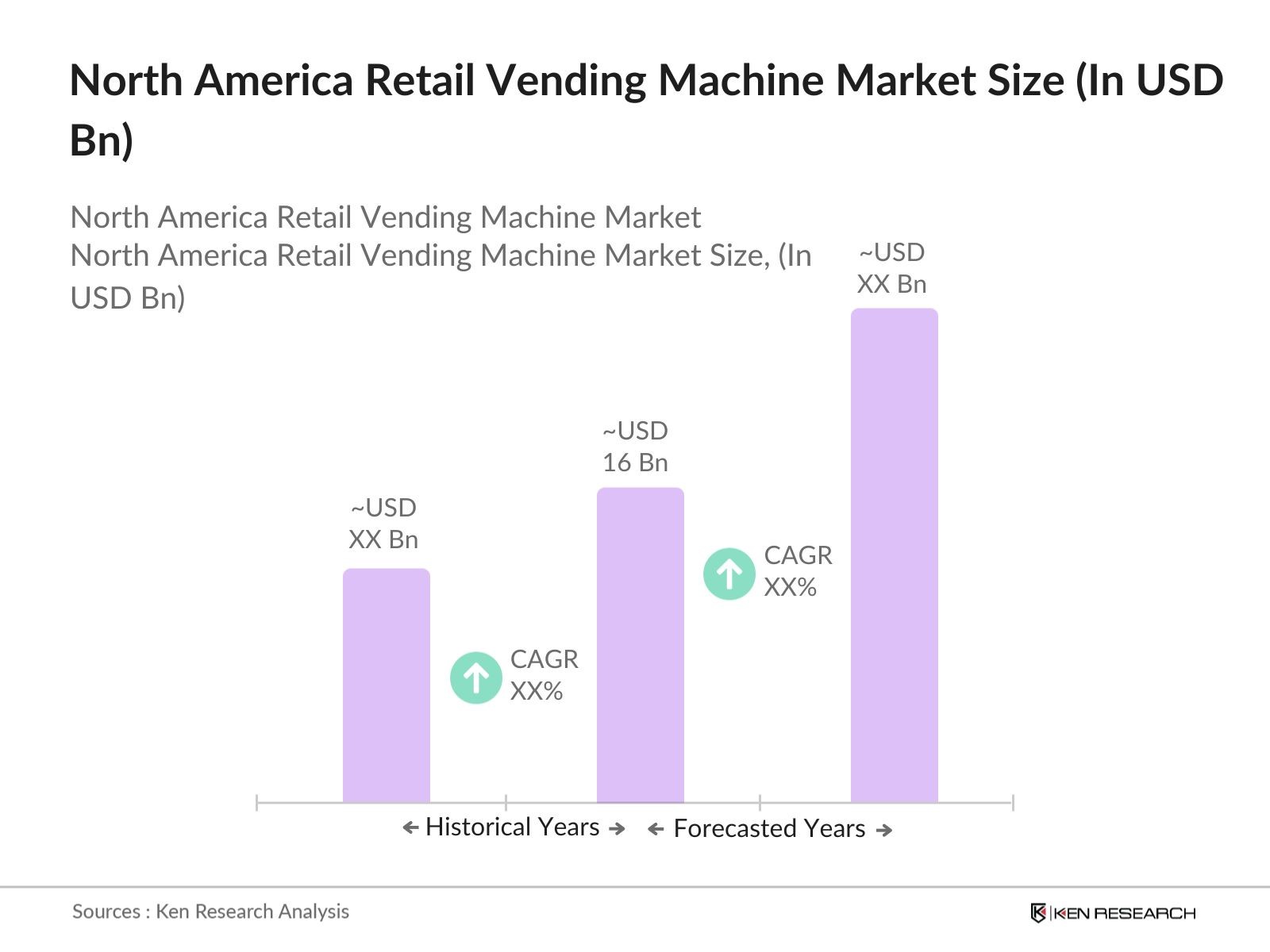

The North America retail vending machine market is valued at USD 16 billion, driven by the increasing demand for convenience, coupled with the rise of cashless payment options and technological innovations. The market has experienced strong growth over the past five years due to the expansion of vending services into new sectors such as healthcare, public transportation, and retail environments. Consumers increasingly prefer quick, automated access to products like snacks, beverages, and even personal care items, which has significantly contributed to the market’s robust growth.

-

Major metropolitan areas in the United States and Canada, including New York City, Los Angeles, Toronto, and Chicago, dominate the vending machine market. This dominance can be attributed to the higher population density, increased consumer demand for convenient, on-the-go services, and favorable regulatory environments that support cashless payments and technology-driven vending solutions. These cities are also tech hubs, encouraging the adoption of smart vending technologies, further boosting market presence in these regions.

-

The increasing shift toward cashless payments in vending machines has prompted regulatory oversight. In 2023, the U.S. Department of Treasury issued guidelines for contactless payments to ensure data security and consumer protection. The guidelines require operators to comply with cybersecurity standards to safeguard payment information, affecting vending machine operators who must upgrade their systems to remain compliant.

North America Retail Vending Machine Market Segmentation

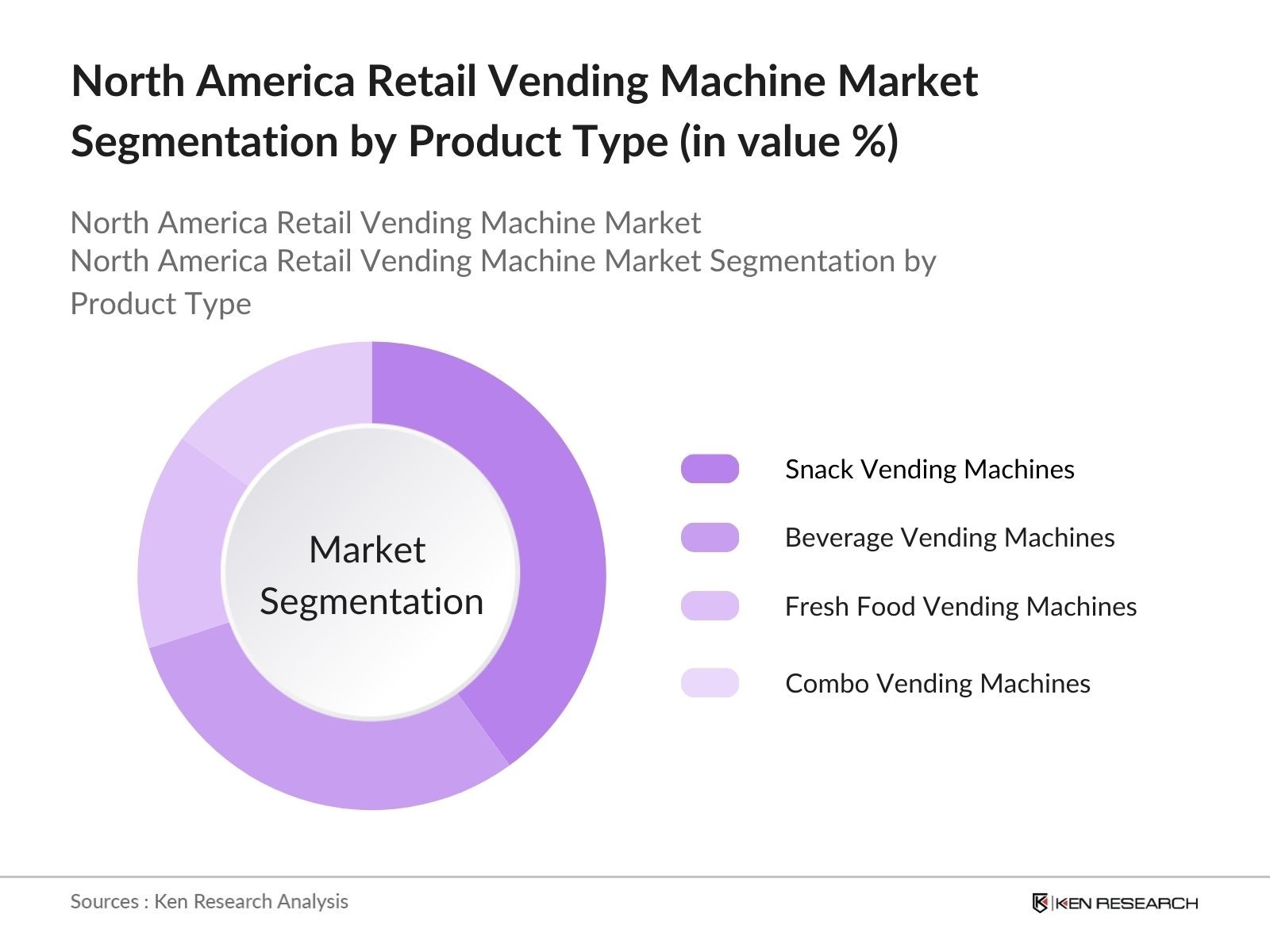

By Product Type: The market is segmented by product type into snack vending machines, beverage vending machines, fresh food vending machines, and combo vending machines. Snack vending machines have a dominant market share under the product type segmentation due to the sustained popularity of pre-packaged snacks, such as chips, candy, and granola bars, among a wide range of consumers. The convenience of obtaining these products at transport hubs, schools, and office spaces continues to drive this segment’s growth. Additionally, the ability to stock non-perishable items ensures that snack vending machines are operational with fewer supply chain challenges compared to fresh food options.

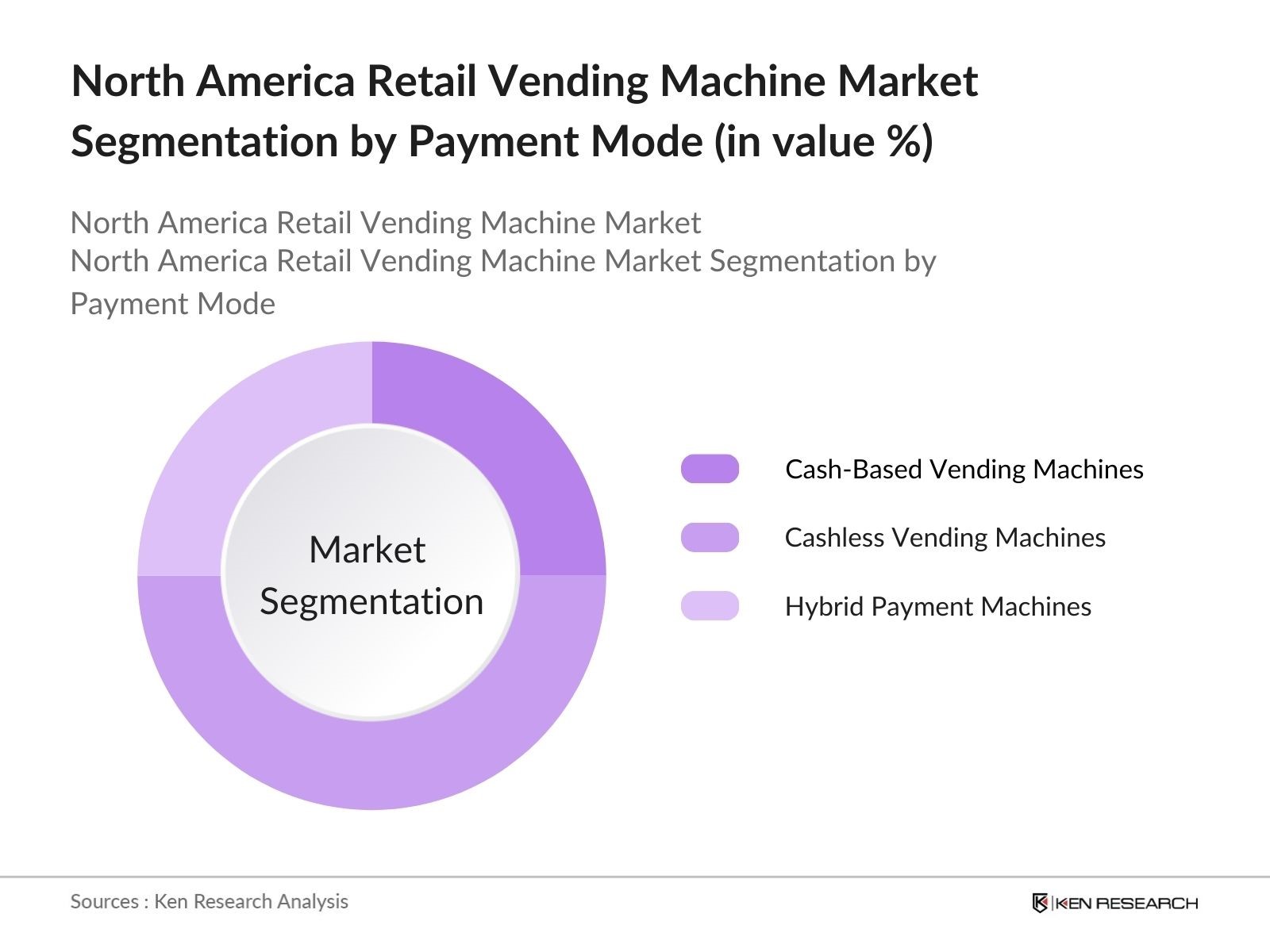

By Payment Mode: The market is also segmented by payment mode into cash-based vending machines, cashless vending machines, and hybrid payment machines. Cashless vending machines dominate this segment due to the growing preference for contactless and card-based payments, driven by advancements in payment technology and the need for hygiene post-pandemic. Consumers’ adoption of mobile wallets and credit card payments has further driven the penetration of cashless vending machines in both urban and suburban areas, offering greater convenience and faster transaction processing.

North America Retail Vending Machine Market Competitive Landscape

The North America retail vending machine market is dominated by a few major players, including Crane Co., Fuji Electric Co., Ltd., and Sanden Holdings Corporation, among others. These companies leverage their large distribution networks, established supply chains, and technological innovation to maintain a stronghold in the market. Key players are increasingly focusing on smart vending solutions that incorporate AI for better stock management and customer experience.

The competitive landscape is shaped by companies investing in automation, AI, and IoT integration for real-time machine management and consumer engagement. Increasing consolidation in the market through mergers and acquisitions also highlights the growing influence of leading companies in expanding their product portfolios and global footprint.

|

Company Name |

Establishment Year |

Headquarters |

Product Range |

Revenue (Global) |

R&D Spending |

Product Innovations |

Partnerships |

Market Share (North America) |

|

Crane Co. |

1855 |

Stamford, Connecticut |

- |

- |

- |

- |

- |

- |

|

Fuji Electric Co., Ltd. |

1923 |

Tokyo, Japan |

- |

- |

- |

- |

- |

- |

|

Sanden Holdings Corporation |

1943 |

Gunma, Japan |

- |

- |

- |

- |

- |

- |

|

Cantaloupe Systems, Inc. |

2002 |

Malvern, Pennsylvania |

- |

- |

- |

- |

- |

- |

|

Selecta Group |

1957 |

Cham, Switzerland |

- |

- |

- |

- |

- |

- |

North America Retail Vending Machine Industry Analysis

Growth Drivers

-

Rising Consumer Demand for Convenience: The demand for vending machines is increasing as consumers seek quicker and more convenient purchasing methods. As of 2024, U.S. consumer spending on non-durable goods reached $2.3 trillion, driven by increasing disposable income and urbanization. Vending machines offer a solution to the fast-paced lifestyles, contributing to the retail automation trend. Government statistics show a rise in urbanization rates, with 83.6% of the U.S. population living in urban areas in 2024, supporting the demand for automated retail solutions.

-

Cashless Payment Trends: The growing adoption of cashless payments is pushing the retail vending machine market to incorporate more advanced payment systems. In 2023, the number of active digital payment users in the U.S. surpassed 311 million, according to government data. The U.S. Federal Reserve reports that 42 billion cashless transactions were processed in 2023, reflecting the shift toward digital payment methods. This trend is aligning vending machines with consumer preferences for speed and convenience.

-

Expanding Automated Retail Solutions: Automated retail, including vending machines, is seeing robust growth due to increasing operational efficiency and labor shortages in the retail sector. With the U.S. facing a labor gap, the U.S. Bureau of Labor Statistics recorded over 9 million unfilled jobs in early 2024. This has incentivized businesses to turn to vending machines and other automated retail solutions to fill gaps in retail staffing. This trend is also visible in Canada, where automation is seen as a solution to a 5.8% job vacancy rate in retail.

Market Challenges

-

High Maintenance Costs: Vending machines require regular maintenance and the cost of maintaining these machines is rising. In the U.S., labor and service costs increased by 5.4% in 2024, according to the Bureau of Labor Statistics. This impacts the operational costs of vending machine operators, as the need for frequent restocking, technical repairs, and general upkeep can strain profitability. With over 5 million vending machines in operation across North America, this is a significant challenge.

-

Vandalism and Security Concerns: Security remains a concern, especially in urban areas. The FBI reported a rise in petty crimes involving property damage in 2023, which includes vandalism targeting vending machines. Reports indicate that vending machines are frequent targets due to their outdoor locations, with an estimated 100,000 machines vandalized annually across the U.S. and Canada, resulting in financial losses and higher insurance premiums for operators.

North America Retail Vending Machine Market Future Outlook

Over the next five years, the North America retail vending machine market is expected to see strong growth driven by technological advancements in smart vending solutions, the rising adoption of cashless and mobile payment technologies, and increased consumer demand for convenience across various industries. The expansion of vending services beyond traditional snacks and beverages to include fresh food, pharmaceuticals, and even personal care products is projected to create new market opportunities. Additionally, the integration of AI and IoT in vending machines will enhance real-time stock monitoring, predictive maintenance, and personalized product offerings.

Future Market Opportunities

- Technological Advancements in Smart Vending Machines: Smart vending machines equipped with IoT sensors and AI are rapidly emerging, allowing operators to track inventory and optimize sales in real-time. In 2023, the U.S. Department of Commerce reported a 24% increase in the adoption of IoT-enabled devices in retail, supporting the rise of smart vending solutions. These innovations reduce maintenance costs and improve operational efficiency, creating substantial growth opportunities for operators.

- Increasing Adoption of Contactless Payments: Contactless payments in vending machines have gained traction due to consumer demand for hygiene and convenience. According to the Federal Reserve, contactless transactions grew by 36 billion in 2023, with retail vending machines seeing a significant portion of this volume. This shift offers vending operators a way to attract tech-savvy consumers while reducing transaction friction, boosting machine profitability.

Scope of the Report

|

By Product Type |

Beverage Vending Machines Snack Vending Machines Fresh Food Vending Machines Combo Vending Machines Specialty Vending Machines |

|

By Application |

Commercial Buildings Retail Stores Transport Hubs Educational Institutions Public Spaces |

|

By Payment Mode |

Cash-Based Vending Machines Cashless Vending Machines Hybrid Payment Vending Machines |

|

By Technology |

Basic Vending Machines Smart Vending Machines |

|

By Region |

United States Canada Mexico |

Products

Key Target Audience

- Retail Chains and Outlets

- Airports and Transport Hubs

- Office and Commercial Building Operators

- Educational Institutions

- Healthcare Facilities

- Banks and Financial Institutes

- Government and Regulatory Bodies (Federal Trade Commission, U.S. Food and Drug Administration)

- Investments and Venture Capitalist Firms

- Public Spaces (Parks, Stadiums)

Companies

Major Players in the Market

- Crane Co.

- Fuji Electric Co., Ltd.

- Sanden Holdings Corporation

- Selecta Group

- Cantaloupe Systems, Inc.

- American Vending Machines

- Seaga Manufacturing, Inc.

- Royal Vendors

- Automated Merchandising Systems

- Wittern Group

- FAS International

- Jofemar Corporation

- Vend-Rite Manufacturing

- Vending Group

- Vending.com

Table of Contents

North America Retail Vending Machine Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

North America Retail Vending Machine Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

North America Retail Vending Machine Market Analysis

3.1. Growth Drivers (Rising Consumer Demand for Convenience, Cashless Payment Trends, Expanding Automated Retail Solutions, Health & Wellness Trends in Vending Products)

3.2. Market Challenges (High Maintenance Costs, Vandalism and Security Concerns, Increasing Energy Costs, Inventory Management Difficulties)

3.3. Opportunities (Technological Advancements in Smart Vending Machines, Increasing Adoption of Contactless Payments, Expanding Product Offerings in Healthy Foods, Untapped Markets in Rural and Suburban Areas)

3.4. Trends (Adoption of AI and IoT in Vending, Expansion of Vending Beyond Traditional Locations, Rise of Customized Vending Solutions, Integration with Mobile Apps for Customer Convenience)

3.5. Government Regulations (Regulations for Cashless Payments, Energy Efficiency Standards, Health and Safety Regulations for Food Vending, Local Compliance for Machine Installation)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porter’s Five Forces

3.9. Competition Ecosystem

North America Retail Vending Machine Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Beverage Vending Machines

4.1.2. Snack Vending Machines

4.1.3. Fresh Food Vending Machines

4.1.4. Combo Vending Machines (Beverage & Snack)

4.1.5. Specialty Vending Machines (Non-Food Items, Pharma, etc.)

4.2. By Application (In Value %)

4.2.1. Commercial Buildings

4.2.2. Retail Stores

4.2.3. Transport Hubs (Airports, Bus Stations, etc.)

4.2.4. Educational Institutions

4.2.5. Public Spaces (Parks, Streets, etc.)

4.3. By Payment Mode (In Value %)

4.3.1. Cash-Based Vending Machines

4.3.2. Cashless Vending Machines (Cards, Mobile Payments)

4.3.3. Hybrid Payment Vending Machines

4.4. By Technology (In Value %)

4.4.1. Basic Vending Machines (Manual Restocking)

4.4.2. Smart Vending Machines (Real-Time Monitoring, Inventory Control)

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

North America Retail Vending Machine Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Crane Co.

5.1.2. Fuji Electric Co., Ltd.

5.1.3. Azkoyen Group

5.1.4. Sanden Holdings Corporation

5.1.5. Selecta Group

5.1.6. Royal Vendors

5.1.7. Cantaloupe Systems, Inc.

5.1.8. Seaga Manufacturing, Inc.

5.1.9. American Vending Machines

5.1.10. FAS International

5.1.11. Automated Merchandising Systems

5.1.12. Vend-Rite Manufacturing

5.1.13. Jofemar Corporation

5.1.14. Vending Group

5.1.15. Wittern Group

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Product Portfolio, Payment Technology Adoption, Expansion in New Markets, Sustainability Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

North America Retail Vending Machine Market Regulatory Framework

6.1. Food Safety Regulations for Vending Machines

6.2. Payment System Compliance (PCI DSS Standards)

6.3. Environmental and Energy Efficiency Regulations

6.4. Local Installation Regulations for Vending Machines

North America Retail Vending Machine Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

North America Retail Vending Machine Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Payment Mode (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

North America Retail Vending Machine Market Analyst’s Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Segmentation Analysis

9.3. Go-To-Market Strategy

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase of research involves mapping the ecosystem of the North America Retail Vending Machine Market. Key stakeholders such as vending machine manufacturers, retail operators, payment system providers, and end consumers are identified through extensive desk research utilizing secondary databases and industry reports. This step is crucial to define and understand the critical variables driving the market, including consumer preferences and technological advancements.

Step 2: Market Analysis and Construction

In this step, historical data on vending machine penetration, payment technology adoption, and revenue generation are compiled to assess market growth patterns. Further, an analysis of product demand in key segments such as beverages and snacks is performed, providing insights into market dynamics. The accuracy of revenue estimates is ensured by cross-referencing data from different sources.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses regarding growth drivers and market challenges are validated through direct consultations with industry experts, including vending machine manufacturers and technology providers. These consultations are conducted using computer-assisted telephone interviews (CATIs) to gather in-depth insights on market trends and technological developments.

Step 4: Research Synthesis and Final Output

The final step involves synthesizing data from multiple sources, including primary research, to provide a comprehensive and validated analysis of the North America Retail Vending Machine Market. This ensures the inclusion of relevant data on market segmentation, competitive landscape, and future growth projections.

Frequently Asked Questions

01. How big is the North America Retail Vending Machine Market?

The North America retail vending machine market is valued at USD 16 billion, driven by technological advancements and growing consumer demand for convenient and contactless product access.

02. What are the challenges in the North America Retail Vending Machine Market?

Challenges in North America retail vending machine market include high maintenance costs, the need for constant technological upgrades, and security concerns related to vandalism and theft, which impact operational efficiency and profitability.

03. Who are the major players in the North America Retail Vending Machine Market?

Key players in the North America retail vending machine market include Crane Co., Fuji Electric Co., Ltd., Sanden Holdings Corporation, Selecta Group, and Cantaloupe Systems, Inc. These companies dominate due to their focus on smart vending technologies and extensive distribution networks.

04. What are the growth drivers of the North America Retail Vending Machine Market?

The North America retail vending machine market is propelled by the increasing adoption of cashless payment systems, the integration of AI and IoT in vending machines, and rising consumer demand for convenient product access in public spaces and workplaces.

05. What are the trends in the North America Retail Vending Machine Market?

Key trends in North America retail vending machine market include the expansion of vending services into new sectors like healthcare and public transportation, as well as the growing adoption of sustainable vending solutions and eco-friendly machines.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.