North America Rigid Plastic Market Outlook to 2030

Region:North America

Author(s):Shubham Kashyap

Product Code:KROD3236

November 2024

89

About the Report

North America Rigid Plastic Market Overview

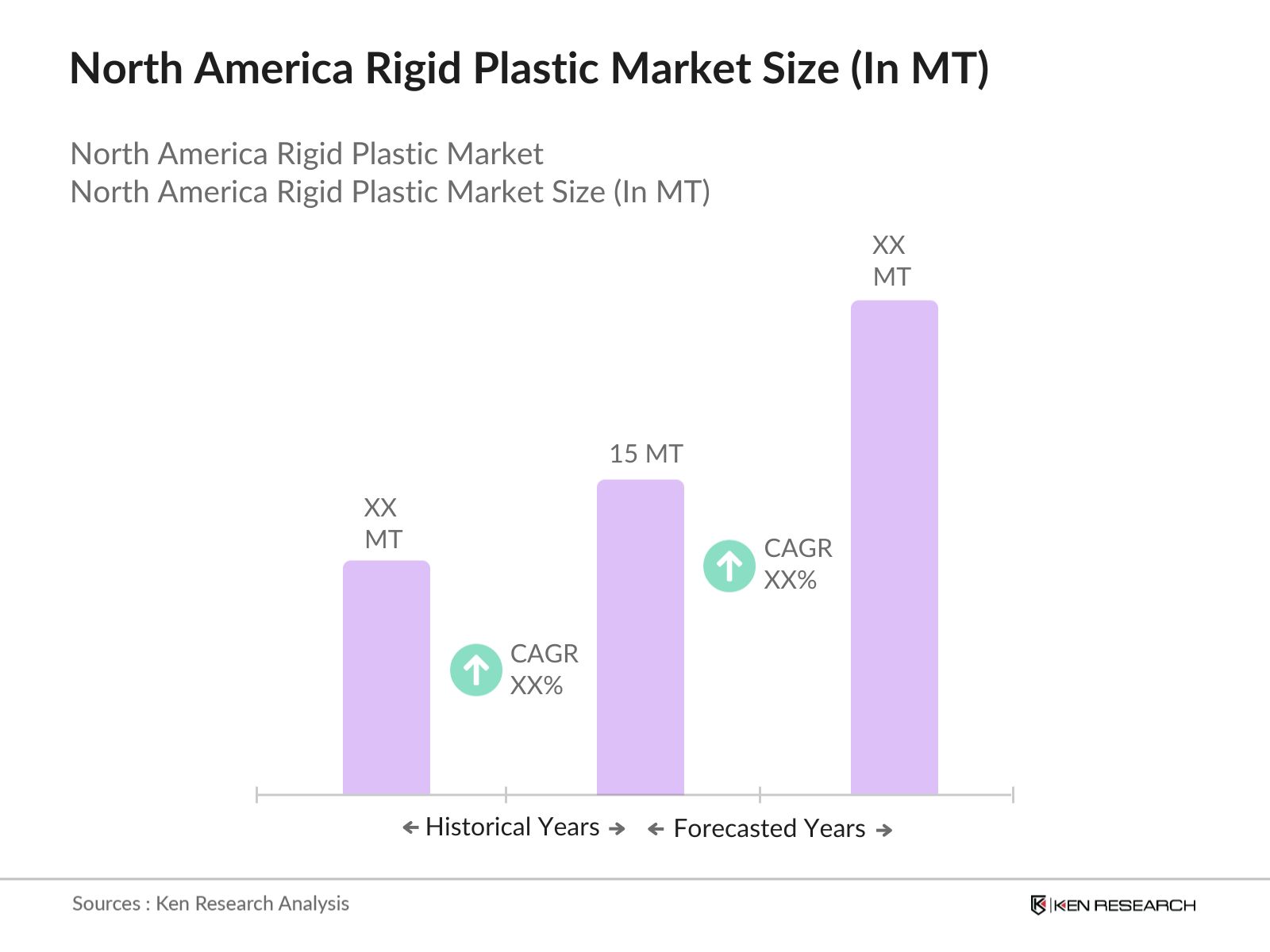

- The North America Rigid Plastic Market was valued at 15 million tonnes, driven by the rising demand for durable and lightweight packaging solutions across industries such as food and beverage, healthcare, and consumer goods. The increasing emphasis on sustainability and recyclability of plastics has contributed substantially to market growth.

- The United States leads the North America Rigid Plastic Market due to its well-established manufacturing sector, high demand for consumer goods, and robust logistics infrastructure. The presence of global manufacturers and innovative packaging companies in the U.S. reinforces its market dominance. Canada is another key player, driven by increasing demand for sustainable packaging solutions and government initiatives promoting plastic recycling and waste management.

- The U.S. government has introduced several initiatives aimed at reducing plastic waste, such as the Save Our Seas 2.0 Act passed in 2020, which aims to enhance waste management and recycling programs. These initiatives are expected to create opportunities for the development and adoption of more sustainable rigid plastic packaging solutions.

North America Rigid Plastic Market Segmentation

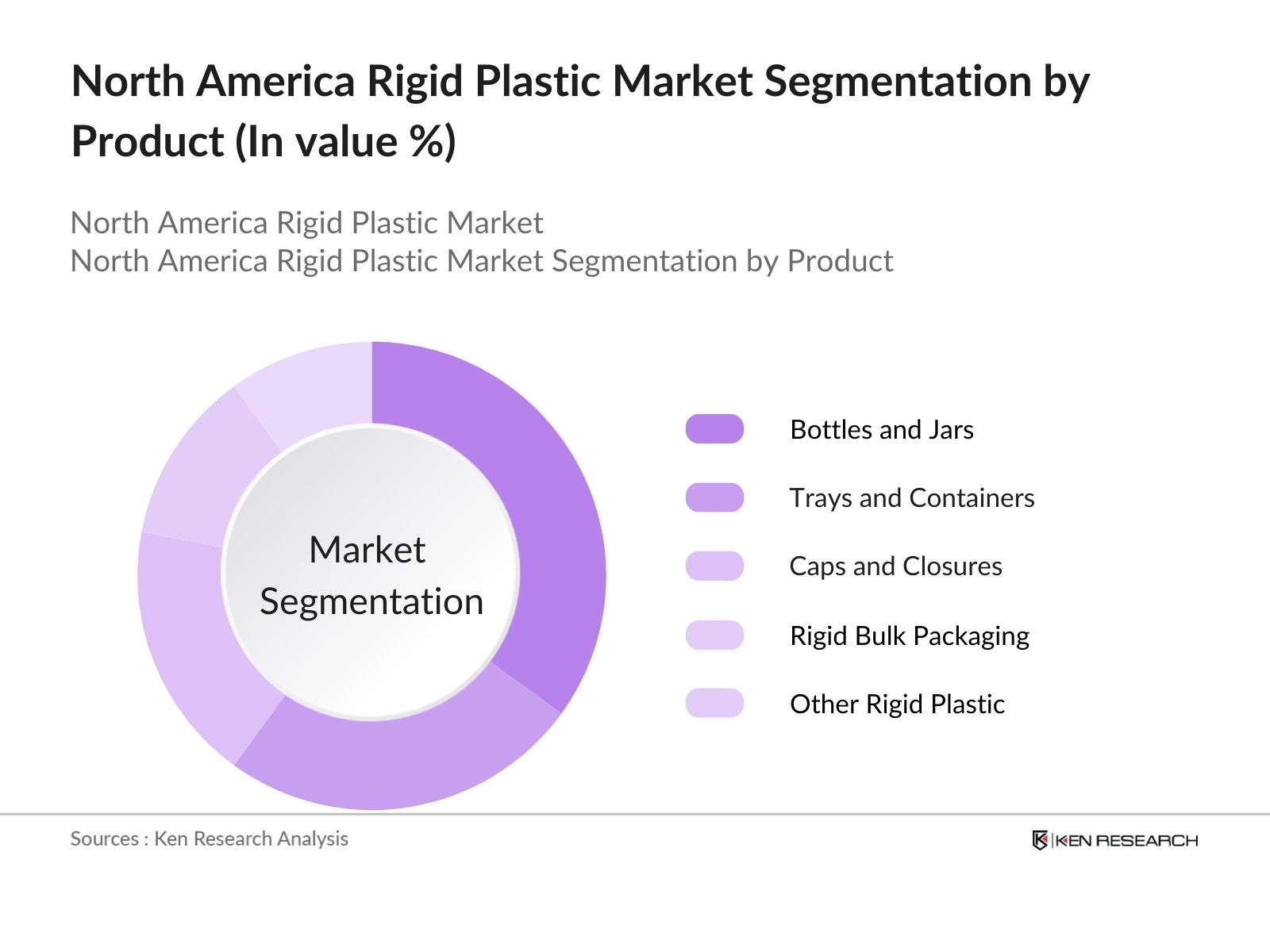

- By Product Type: The market is segmented by product type into bottles and jars, trays and containers, caps and closures, rigid bulk packaging, and other rigid plastic products. Bottles and Jars hold a dominant market share in this segment due to their widespread usage in the food, beverage, and personal care sectors. Lightweight, durable, and recyclable PET bottles are increasingly preferred for packaging solutions, particularly in the beverage industry. Companies like Coca-Cola and PepsiCo have adopted PET bottles due to their cost-efficiency and recyclability, strengthening the market for bottles and jars in North America.

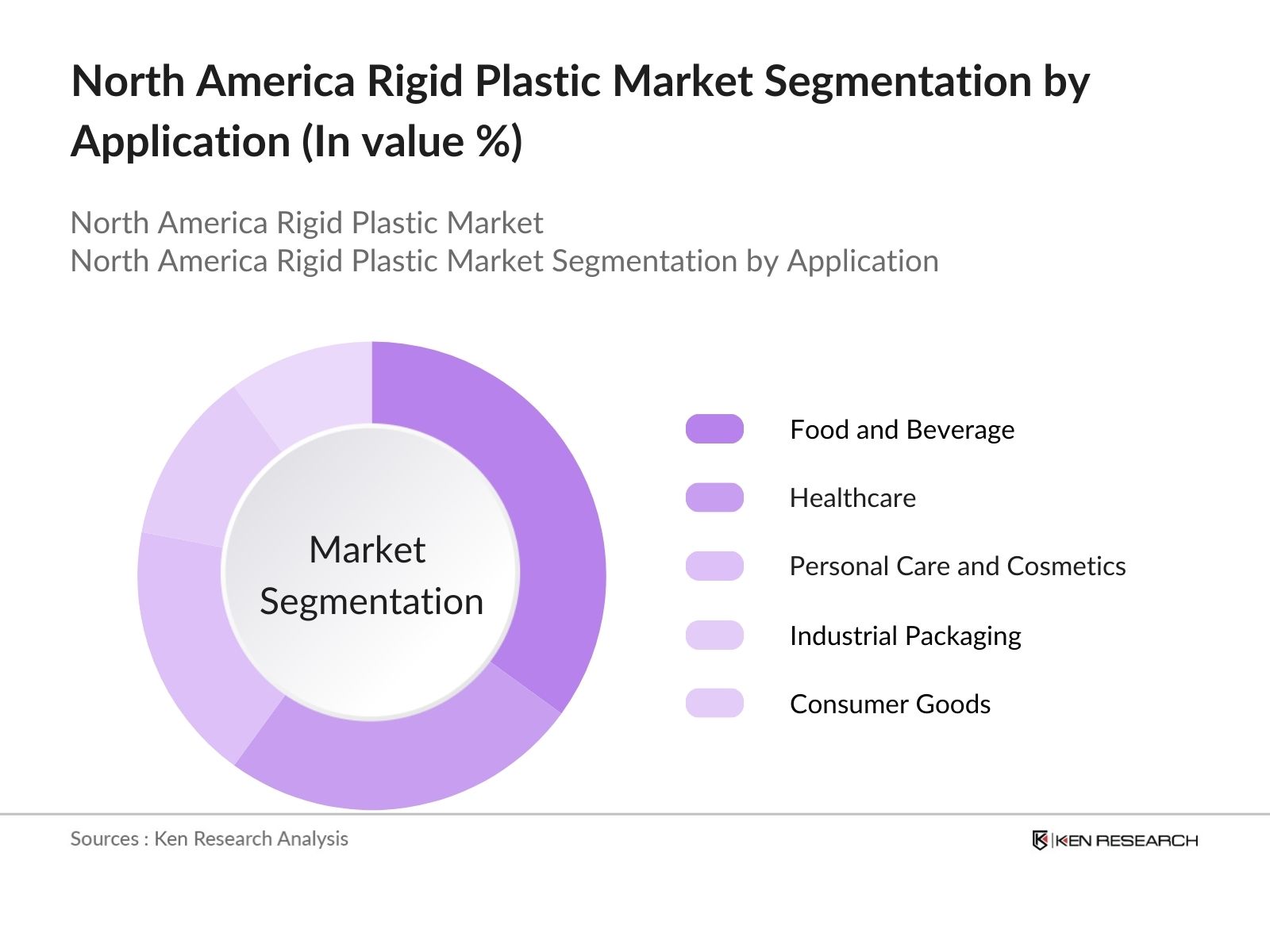

- By Application: The market is further segmented by application into food and beverage, healthcare, personal care and cosmetics, industrial packaging, and consumer goods. The food and beverage industry dominated the North America Rigid Plastic Market, with manufacturers increasingly turning to rigid plastic packaging for its ability to preserve product freshness and extend shelf life. The rise in demand for ready-to-eat meals and packaged beverages is contributing to the sustained growth of this segment.

North America Rigid Plastic Market Competitive Landscape

The North America Rigid Plastic Market is highly competitive, with major players focused on sustainability initiatives, innovations in bio-based materials, and expanding their recycling infrastructure. Dominated by key global manufacturers, the market sees consolidation, particularly in the food and beverage packaging sector, where companies like Amcor and Berry Global lead with their advanced rigid plastic solutions.

|

Company |

Establishment Year |

Headquarters |

Revenue (USD Bn) |

Product Portfolio |

Sustainability Initiatives |

Regional Presence |

Technology Innovations |

Mergers & Acquisitions |

|

Amcor |

1860 |

Zurich, Switzerland |

12.5 |

Rigid Plastic Packaging |

Focus on Recyclable Materials |

Strong North America |

Advanced Manufacturing |

Acquired Bemis |

|

Berry Global |

1967 |

Evansville, Indiana, USA |

||||||

|

Sonoco |

1899 |

Hartsville, South Carolina, USA |

||||||

|

Silgan Holdings |

1987 |

Stamford, Connecticut, USA |

||||||

|

Sealed Air |

1960 |

Charlotte, North Carolina, USA |

North America Rigid Plastic Market Analysis

Growth Drivers

- Increasing Demand for Sustainable Packaging: The demand for sustainable packaging in North America is growing due to environmental concerns and consumer preferences for eco-friendly products. According to the U.S. Environmental Protection Agency (EPA), 14.5 million tons of plastic containers and packaging waste were generated in 2018, with ongoing efforts to reduce this. Government policies, such as the Canadian governments plan to ban harmful single-use plastics by 2025, further push companies to adopt sustainable materials. This shift is supported by macroeconomic stability in the U.S. and Canada, reflected in GDP growth, which reached USD 29.8 trillion in 2024.

- Growth in E-commerce and Consumer Goods: The expansion of the e-commerce sector has driven the demand for rigid plastic packaging due to its durability and lightweight nature. In 2024, the U.S. e-commerce market expanded remarkably, highlighting the growing need for efficient packaging solutions. Rigid plastic packaging is commonly used for shipping goods due to its protective properties. The boom in logistics and warehousing, which grew substantially in 2024, further bolstered demand, particularly for food, beverages, and consumer goods that require robust packaging materials.

- Increasing demand for Lightweight Packaging Solutions: Rigid plastic packaging is highly sought after for its lightweight yet durable properties, which help reduce transportation costs and carbon emissions. In 2023, the U.S. plastic packaging industry produced millions of tons of rigid plastics, a large portion of which was used in the food and beverage sector. The shift towards lighter packaging is reinforced by environmental concerns and stringent regulatory standards aimed at reducing the carbon footprint. In 2024, the U.S. reported a GDP of USD 27.5 trillion, with the logistics and packaging sectors contributing to this figure.

Challenges

- Compliance with Environmental Regulations: The Indian government has introduced stringent environmental regulations to control volatile organic compound (VOC) emissions, pushing companies to shift towards water-based or low-VOC coatings. The Central Pollution Control Board (CPCB) enforces these standards, which are challenging for manufacturers due to the high cost of compliance. For instance, coatings with VOC levels above 250 grams per liter face penalties. These regulations, while environmentally necessary, create hurdles for manufacturers in terms of cost and product formulation.

- High Costs of Sustainable Materials: The Indian industrial coatings market faces volatility in raw material prices, particularly for key inputs like titanium dioxide, resins, and pigments. This price instability makes it challenging for coating manufacturers to maintain their profit margins. Additionally, fluctuations in oil prices, which impact resin production, further contribute to cost pressures. In response, Indian manufacturers are exploring local sourcing or alternative materials to mitigate the financial burden. However, concerns about the quality and availability of these alternatives persist, posing ongoing challenges for the industry.

North America Rigid Plastic Market Future Outlook

Over the next five years, the North America Rigid Plastic Market is expected to experience growth due to increasing demand for eco-friendly and sustainable packaging solutions. Innovations in bio-based plastics and enhanced recycling infrastructure will play a pivotal role in market expansion. Furthermore, growing e-commerce and demand for lightweight packaging in sectors such as food and beverage will continue to fuel the adoption of rigid plastic packaging solutions.

Future Market Opportunities

- Expanding Market in Tier-2 and Tier-3 Cities: The growth of manufacturing hubs in tier-2 and tier-3 cities presents new opportunities for the industrial coatings market. Cities like Coimbatore, Vadodara, and Ludhiana are becoming focal points for manufacturing and infrastructure development, driven by government incentives for regional industrialization. In 2023, investments in these cities totaled billions, primarily in infrastructure projects and manufacturing plants, boosting demand for protective coatings.

- Rising Investments in Manufacturing and Infrastructure Projects: India continues to attract large-scale investments in both manufacturing and infrastructure projects. In 2023, foreign direct investment (FDI) inflows in the manufacturing sector reached USD 9.3 billion. Investments in mega infrastructure projects such as the Delhi-Mumbai Industrial Corridor (DMIC) are spurring demand for industrial coatings used in machinery, steel structures, and concrete. These developments indicate a robust growth trajectory for industrial coatings.

Scope of the Report

|

By Product |

Bottles and Jars Trays and Containers Caps and Closures Rigid Bulk Packaging Other Rigid Plastic Products |

|

By Application |

Food and Beverage Healthcare Personal Care and Cosmetics Industrial Packaging Consumer Goods |

|

By Polymer |

Polyethylene Terephthalate (PET) Polypropylene (PP) High-Density Polyethylene (HDPE) Polystyrene (PS) Polyvinyl Chloride (PVC) |

|

By End-User |

Food and Beverage Pharmaceuticals Industrial Goods Automotive Electronics |

|

By Region |

United States Canada Mexico |

Products

Key Target Audience

Packaging Manufacturers

Food and Beverage Companies

Healthcare Packaging Companies

Consumer Goods Manufacturers

Government and Regulatory Bodies (U.S. Environmental Protection Agency, Canada Plastics Industry Association)

Investors and Venture Capitalist Firms

Recycling and Waste Management Companies

E-commerce Retailers

Banks and Financial Institutions

Companies

Major Players Mentioned in the Report

Amcor

Berry Global

Sonoco

Silgan Holdings

Sealed Air

AptarGroup

Plastipak Holdings

Alpla Group

Reynolds Group Holdings

Pactiv Evergreen

Graham Packaging

Greif Inc.

WestRock Company

Huhtamaki Group

CCL Industries

Table of Contents

1. North America Rigid Plastic Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Rigid Plastic Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Rigid Plastic Market Analysis

3.1. Growth Drivers

3.1.1. Demand for Sustainable Packaging

3.1.2. Technological Innovations in Plastic Manufacturing

3.1.3. Growth in E-commerce and Logistics

3.1.4. Increasing Demand for Lightweight Packaging Solutions

3.2. Market Challenges

3.2.1. Regulatory Pressures on Plastic Use

3.2.2. High Costs of Sustainable Alternatives

3.2.3. Fluctuations in Raw Material Prices

3.2.4. Recycling Infrastructure Limitations

3.3. Opportunities

3.3.1. Expansion in Healthcare Packaging

3.3.2. Growing Adoption of Recycled Plastics

3.3.3. Increasing Usage of Bio-based Rigid Plastics

3.3.4. Emerging Demand from Food and Beverage Industry

3.4. Trends

3.4.1. Circular Economy Initiatives

3.4.2. Rise of Biodegradable Plastics

3.4.3. Adoption of Advanced Manufacturing Techniques

3.4.4. Use of Recycled Content in Packaging

3.5. Government Regulation

3.5.1. Plastic Waste Reduction Regulations

3.5.2. Extended Producer Responsibility (EPR) Schemes

3.5.3. National and Regional Recycling Standards

3.5.4. Sustainable Packaging Initiatives

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. North America Rigid Plastic Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Bottles and Jars

4.1.2. Trays and Containers

4.1.3. Caps and Closures

4.1.4. Rigid Bulk Packaging

4.1.5. Other Rigid Plastic Products

4.2. By Application (In Value %)

4.2.1. Food and Beverage

4.2.2. Healthcare

4.2.3. Personal Care and Cosmetics

4.2.4. Industrial Packaging

4.2.5. Consumer Goods

4.3. By Polymer Type (In Value %)

4.3.1. Polyethylene Terephthalate (PET)

4.3.2. Polypropylene (PP)

4.3.3. High-Density Polyethylene (HDPE)

4.3.4. Polystyrene (PS)

4.3.5. Polyvinyl Chloride (PVC)

4.4. By End-Use Industry (In Value %)

4.4.1. Food and Beverage

4.4.2. Pharmaceuticals

4.4.3. Industrial Goods

4.4.4. Automotive

4.4.5. Electronics

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5. North America Rigid Plastic Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Amcor

5.1.2. Berry Global

5.1.3. Sonoco

5.1.4. Silgan Holdings

5.1.5. Sealed Air

5.1.6. AptarGroup

5.1.7. Plastipak Holdings

5.1.8. Alpla Group

5.1.9. Reynolds Group Holdings

5.1.10. Pactiv Evergreen

5.1.11. Graham Packaging

5.1.12. Greif Inc.

5.1.13. WestRock Company

5.1.14. Huhtamaki Group

5.1.15. CCL Industries

5.2. Cross Comparison Parameters (Revenue, Product Portfolio, Sustainability Initiatives, Production Capacity, Market Share, Regional Presence, Technology Adoption, Strategic Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. North America Rigid Plastic Market Regulatory Framework

6.1. Plastic Waste Reduction Laws

6.2. Compliance and Certification Standards

6.3. Extended Producer Responsibility Policies

7. North America Rigid Plastic Market Future Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Rigid Plastic Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Polymer Type (In Value %)

8.4. By End-Use Industry (In Value %)

8.5. By Region (In Value %)

9. North America Rigid Plastic Market Analysts' Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Product Portfolio Optimization

9.3. Strategic Entry and Expansion Recommendations

9.4. Innovation and Technology Roadmap

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the North America Rigid Plastic Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we will compile and analyze historical data pertaining to the North America Rigid Plastic Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATIS) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple packaging manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the North America Rigid Plastic Market.

Frequently Asked Questions

01 How big is the North America Rigid Plastic Market?

The North America Rigid Plastic Market was valued at USD 15 million tonnes, driven by the increasing demand for sustainable and durable packaging solutions across sectors such as food and beverage, healthcare, and consumer goods.

02 What are the challenges in the North America Rigid Plastic Market?

Challenges in the North America Rigid Plastic market include regulatory pressures on the use of single-use plastics, high production costs of sustainable alternatives, and limitations in recycling infrastructure across the region.

03 Who are the major players in the North America Rigid Plastic Market?

Major players in the North America Rigid Plastic market include Amcor, Berry Global, Sonoco, Silgan Holdings, and Sealed Air, who dominate due to their innovations in recyclable rigid plastics and strong regional presence.

04 What are the growth drivers of the North America Rigid Plastic Market?

The North America Rigid Plastic market is propelled by the rising demand for sustainable packaging, growth in the food and beverage industry, and technological advancements in the production of bio-based and recyclable plastics.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.