North America Robotic Welding Market Outlook to 2030

Region:North America

Author(s):Sanjeev

Product Code:KROD9139

December 2024

91

About the Report

North America Robotic Welding Market Overview

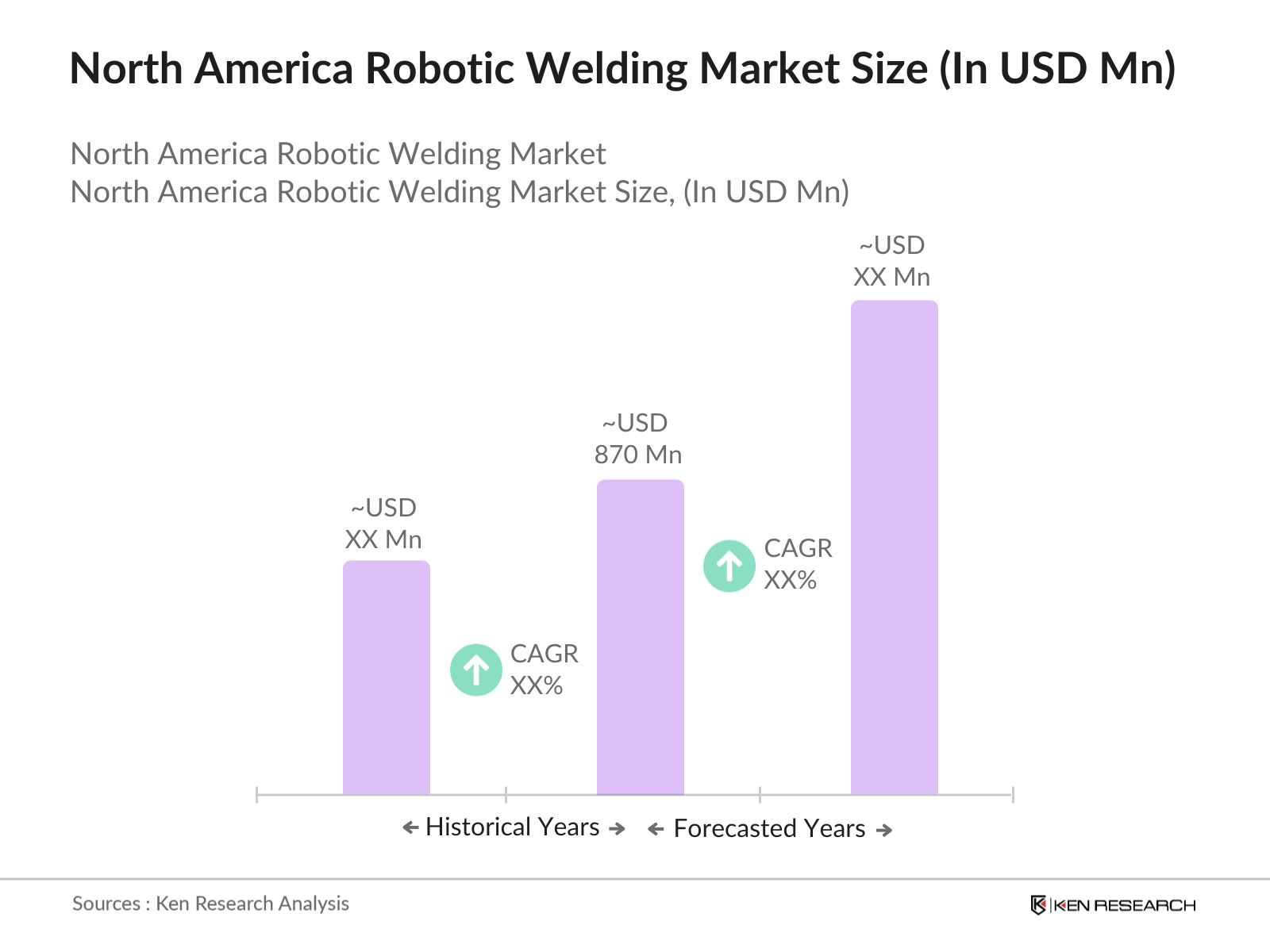

- The North America robotic welding market is valued at approximately USD 870 million, driven by the significant demand for automation in various industries, particularly in automotive and heavy machinery sectors. This market's growth is fueled by technological advancements in welding robots, which offer precision, speed, and cost efficiency. The integration of robotics and welding has resulted in improved productivity, reduced human errors, and minimized waste, making it an attractive investment for industries facing labor shortages and cost pressures. The market is further driven by an increasing push toward Industry 4.0 adoption, leading to a higher uptake of smart manufacturing solutions.

- Countries such as the United States and Canada dominate the robotic welding market in North America. The dominance of the United States is attributed to its robust automotive and aerospace sectors, which are early adopters of automation and robotics. The country also benefits from the presence of leading robotic manufacturers and high R&D investments in advanced manufacturing technologies. Canadas dominance is driven by its strong manufacturing base and government initiatives supporting automation in the industrial sector.

North America Robotic Welding Market Segmentation

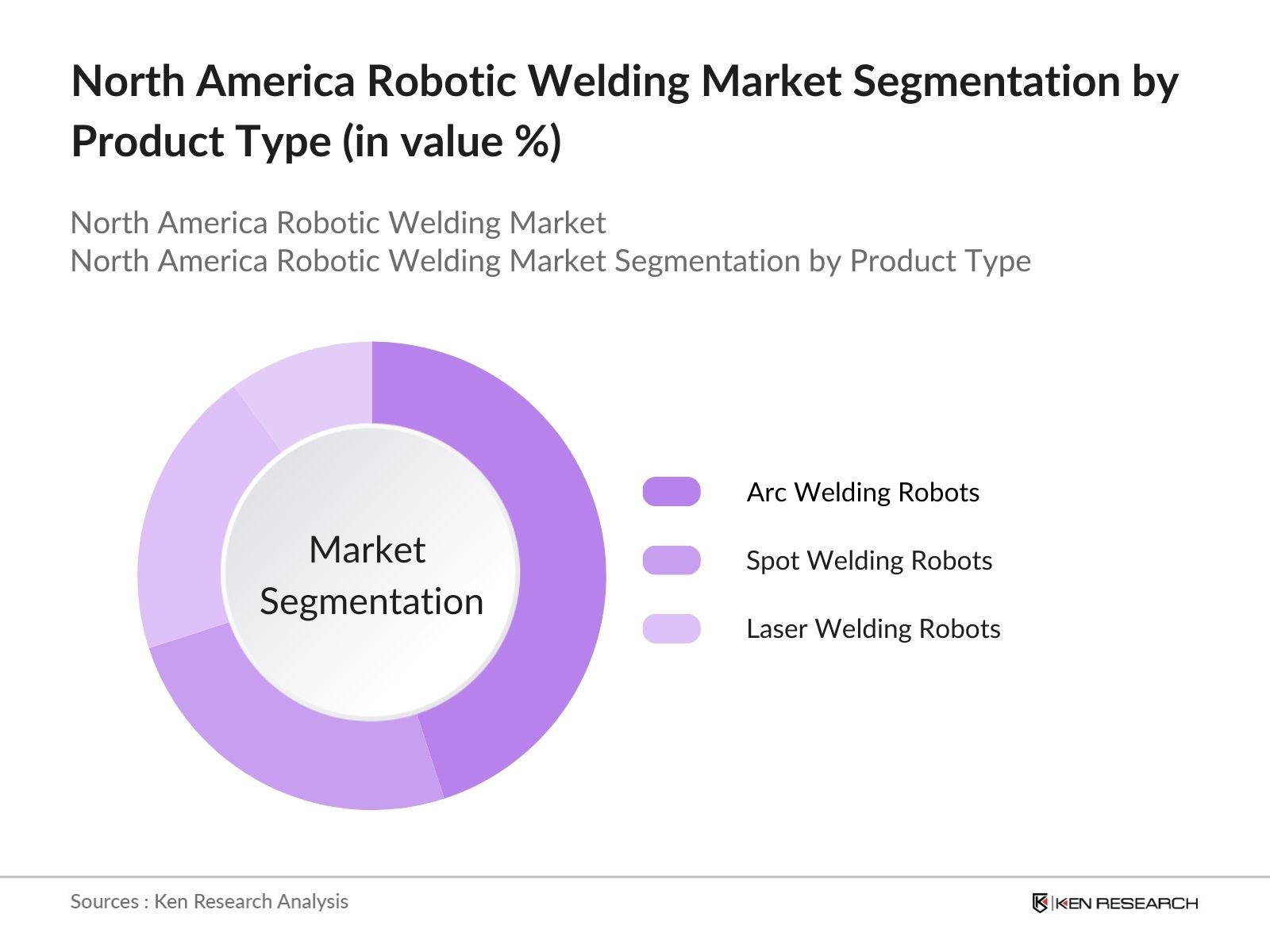

- By Product Type: The North America robotic welding market is segmented by product type into arc welding robots, spot welding robots, laser welding robots, and others (such as resistance and TIG welding).

Arc welding robots hold the dominant market share within this segment due to their widespread application in the automotive and construction industries, where the demand for high-strength welds is crucial. Arc welding technology is preferred for its versatility, allowing it to be used in diverse environments ranging from steel fabrication to repair welding. The availability of automated systems that can perform complex arc welding tasks with minimal human intervention has increased its adoption, particularly in large-scale manufacturing setups.

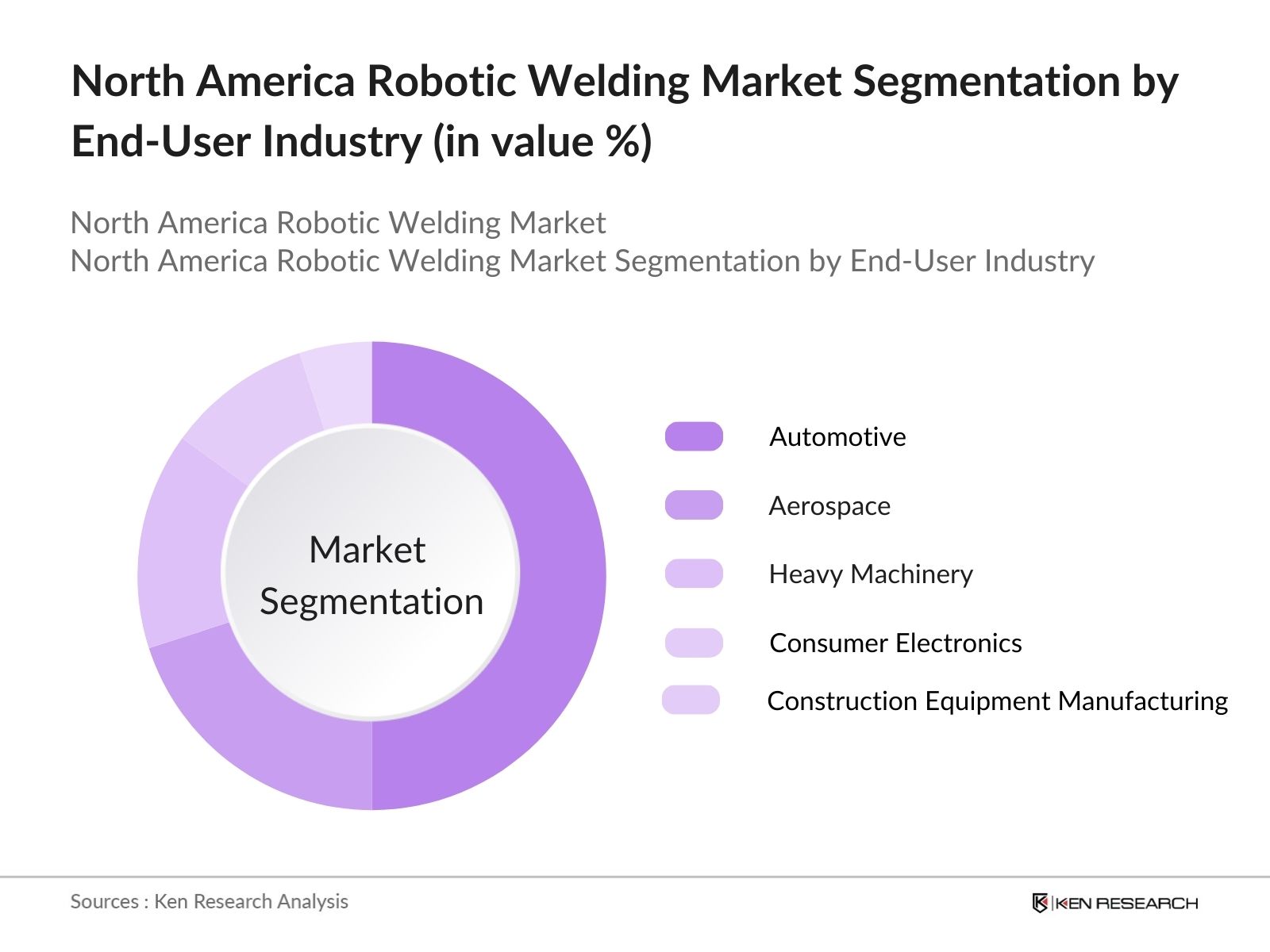

- By End-User Industry: The market is segmented into automotive, aerospace, heavy machinery, consumer electronics, and construction equipment manufacturing.

The automotive sector commands the largest market share in robotic welding, as this industry heavily relies on automation to meet mass production needs, improve precision, and reduce operational costs. Robotic welding is integral to the manufacturing processes of vehicle frames, engine parts, and safety-critical components, where consistency and quality are paramount. The sector's push for electrification and lightweight vehicle materials further necessitates the use of robotic welding systems to meet specific material handling and assembly requirements.

North America Robotic Welding Market Competitive Landscape

The North America robotic welding market is dominated by a few major global players, which reflects the high level of consolidation in the industry. Companies like ABB Ltd., Fanuc Corporation, Yaskawa Electric Corporation, and KUKA AG are some of the leading players that have a significant presence due to their cutting-edge technology, wide service networks, and extensive R&D capabilities. These companies compete on the basis of innovation, product performance, after-sales service, and customization to meet client-specific requirements. Additionally, local players such as Lincoln Electric and Miller Electric are well-positioned, especially in niche sectors where welding precision and customization are essential.

|

Company Name |

Year Established |

Headquarters |

Revenue (USD Billion) |

No. of Employees |

Global Presence |

|

ABB Ltd. |

1988 |

Zurich, Switzerland |

|||

|

Fanuc Corporation |

1956 |

Oshino, Japan |

|||

|

Yaskawa Electric Corporation |

1915 |

Kitakyushu, Japan |

|||

|

KUKA AG |

1898 |

Augsburg, Germany |

|||

|

Lincoln Electric Holdings |

1895 |

Ohio, USA |

North America Robotic Welding Market Future Outlook

The North America robotic welding market is expected to experience significant growth in the coming years, driven by factors such as the ongoing labor shortages in manufacturing, advancements in robotic systems, and the increasing integration of artificial intelligence and machine learning into robotic solutions. As industries continue to automate, the demand for efficient and precise welding systems will only increase. Additionally, sectors like automotive, aerospace, and construction are set to witness strong growth, which will further drive the adoption of robotic welding solutions. The push toward lightweight materials and the rise of electric vehicles in the automotive industry are also expected to create new opportunities for robotic welding technologies, as they are uniquely positioned to handle specialized welding tasks required for these new materials.

Scope of the Report

|

Arc Welding Robots Spot Welding Robots Laser Welding Robots |

|

|

By Payload Capacity |

Less than 50 kg 50-150 kg Above 150 kg |

|

By Application |

Automotive Aerospace Heavy Machinery Consumer Electronics, Construction Equipment |

|

By End User Industry |

Automotive Electronics & Electrical Heavy Industry |

|

By Region |

North East West South |

Products

Key Target Audience

Automotive Manufacturers

Aerospace Companies

Construction Equipment Manufacturers

Industrial Automation Companies

Heavy Machinery Manufacturers

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., Occupational Safety and Health Administration - OSHA, U.S. Department of Commerce)

Industrial Robotics Suppliers

Companies

Players mention in the Report:

ABB Ltd.

Fanuc Corporation

Yaskawa Electric Corporation

KUKA AG

Lincoln Electric Holdings, Inc.

Panasonic Corporation

Miller Electric Manufacturing LLC

Kawasaki Heavy Industries

DAIHEN Corporation

Comau SpA

Universal Robots A/S

Staubli International AG

Hypertherm, Inc.

NACHI-FUJIKOSHI Corp.

Siasun Robot & Automation Co., Ltd.

Table of Contents

1. North America Robotic Welding Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Robotic Welding Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Robotic Welding Market Analysis

3.1. Growth Drivers

3.1.1. Automation in Manufacturing

3.1.2. Labor Shortage and Rising Labor Costs

3.1.3. Technological Advancements in Robotics

3.1.4. Demand for Precision in Welding

3.1.5. Adoption of Industry 4.0

3.2. Market Challenges

3.2.1. High Initial Capital Investment

3.2.2. Technical Complexity in Deployment

3.2.3. Limited Skilled Workforce for Robotic Operation

3.3. Opportunities

3.3.1. Integration with Artificial Intelligence and Machine Learning

3.3.2. Expansion in Small and Medium Enterprises (SMEs)

3.3.3. Increasing Demand in the Automotive and Aerospace Sectors

3.4. Trends

3.4.1. Rise of Collaborative Robots (Cobots) in Welding

3.4.2. Utilization of IoT in Robotic Welding Systems

3.4.3. Increasing Use of Laser Welding Robotics

3.5. Government Regulation

3.5.1. Industry Safety Standards for Robotic Systems

3.5.2. Regulations on Industrial Robotics Deployment

3.5.3. Worker Safety Guidelines and Standards

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. North America Robotic Welding Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Arc Welding Robots

4.1.2. Spot Welding Robots

4.1.3. Laser Welding Robots

4.1.4. Others (Resistance Welding, TIG Welding)

4.2. By Payload Capacity (In Value %)

4.2.1. Less than 50 kg

4.2.2. 50-150 kg

4.2.3. Above 150 kg

4.3. By Application (In Value %)

4.3.1. Automotive

4.3.2. Aerospace

4.3.3. Heavy Machinery

4.3.4. Consumer Electronics

4.3.5. Construction Equipment Manufacturing

4.4. By End User Industry (In Value %)

4.4.1. Automotive

4.4.2. Electronics & Electrical

4.4.3. Heavy Industry

4.4.4. Others (Energy, Shipbuilding)

4.5. By Region (In Value %)

4.5.1. USA

4.5.2. Canada

4.5.3. Mexico

5. North America Robotic Welding Market Competitive Analysis

5.1. Detailed Profiles of Major Competitors

5.1.1. ABB Ltd.

5.1.2. Fanuc Corporation

5.1.3. Yaskawa Electric Corporation

5.1.4. KUKA AG

5.1.5. Panasonic Corporation

5.1.6. Kawasaki Heavy Industries

5.1.7. DAIHEN Corporation

5.1.8. Comau SpA

5.1.9. Lincoln Electric Holdings, Inc.

5.1.10. Universal Robots A/S

5.1.11. Staubli International AG

5.1.12. Miller Electric Manufacturing LLC

5.1.13. Hypertherm, Inc.

5.1.14. NACHI-FUJIKOSHI Corp.

5.1.15. Siasun Robot & Automation Co., Ltd.

5.2. Cross Comparison Parameters (Revenue, Number of Installations, Global Presence, Market Share, Technological Innovations, Strategic Alliances, Product Portfolio, Service & Support Infrastructure)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. North America Robotic Welding Market Regulatory Framework

6.1. Occupational Safety Regulations

6.2. Industrial Robotics Certification Standards

6.3. Compliance with ISO 10218 for Robot Safety

7. North America Robotic Welding Market Future Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Robotic Welding Market Future Segmentation

8.1. By Product Type (In Value %)

8.2. By Payload Capacity (In Value %)

8.3. By Application (In Value %)

8.4. By End User Industry (In Value %)

8.5. By Region (In Value %)

9. North America Robotic Welding Market Analyst Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

This phase involves mapping all relevant stakeholders within the North America robotic welding market ecosystem. Secondary sources such as industry reports, trade journals, and proprietary databases were used to identify critical market variables influencing the industry's structure and performance.

Step 2: Market Analysis and Construction

We collected and analyzed historical market data pertaining to robotic welding deployment, market penetration rates, and revenue generated across key industries. Our analysis focused on identifying the ratio of service providers to manufacturing sectors and the resultant revenue impact.

Step 3: Hypothesis Validation and Expert Consultation

We conducted interviews with industry experts through CATIs to validate our market hypotheses. These experts provided operational insights that refined our revenue forecasts and helped ensure the reliability of our market projections.

Step 4: Research Synthesis and Final Output

In this final step, detailed inputs were gathered from multiple robotics manufacturers. This input complemented our bottom-up approach, helping to verify market data and providing an accurate, comprehensive analysis of the North America robotic welding market.

Frequently Asked Questions

01. How big is the North America robotic welding market?

The North America robotic welding market is valued at USD 870 million, driven by increased automation in industries such as automotive, aerospace, and construction.

02. What are the challenges in the North America robotic welding market?

Challenges in North America robotic welding market include the high initial capital investment, the complexity of integrating robotic welding systems, and the shortage of skilled labor to operate advanced systems.

03. Who are the major players in the North America robotic welding market?

Key players in the North America robotic welding market include ABB Ltd., Fanuc Corporation, Yaskawa Electric Corporation, KUKA AG, and Lincoln Electric Holdings. These companies dominate due to their technological innovation and strong customer bases.

04. What are the growth drivers of the North America robotic welding market?

The North America robotic welding market is driven by the need for precision and efficiency in manufacturing, labor shortages, and advancements in welding technology, particularly the integration of AI and IoT into robotic systems.

05. Which industries use robotic welding the most?

The automotive and aerospace sectors are the largest adopters of robotic welding technology due to their high production volumes and the need for high precision and quality in welds.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.