North America Satellite Internet Market Outlook to 2030

Region:North America

Author(s):Yogita Sahu

Product Code:KROD7598

November 2024

94

About the Report

North America Satellite Internet Market Overview

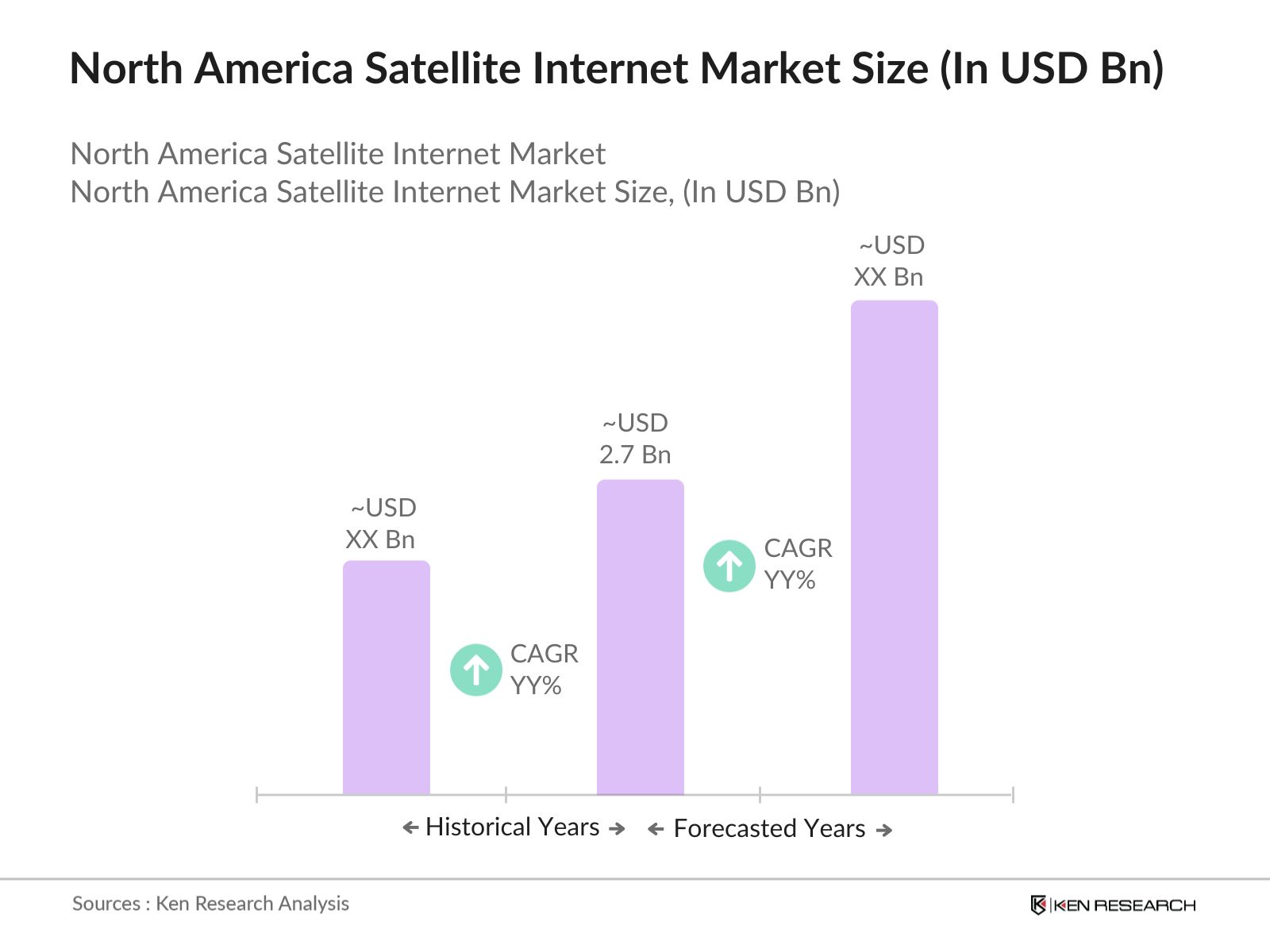

- The North America Satellite Internet market is valued at USD 2.7 billion, based on a five-year historical analysis. This growth is driven by increasing demand for reliable high-speed internet in rural and underserved areas. The deployment of large satellite constellations such as SpaceXs Starlink has significantly expanded the market's coverage, addressing the demand for uninterrupted service across vast regions.

- Dominant players in the market include the United States and Canada. These countries dominate due to their vast geographic areas with underserved rural regions and strong government backing to improve internet accessibility. The U.S., through the FCC, has been instrumental in fostering growth by offering subsidies for satellite internet services, while Canadas push to improve rural connectivity has also driven adoption.

- In 2024, the U.S. government launched the BEAD program, providing over $42.5 billion in funding to expand broadband access across the country, including satellite internet. This program specifically targets rural and underserved areas where traditional broadband infrastructure is lacking. Satellite providers are eligible to apply for this funding, enabling them to expand their services significantly in the coming years.

North America Satellite Internet Market Segmentation

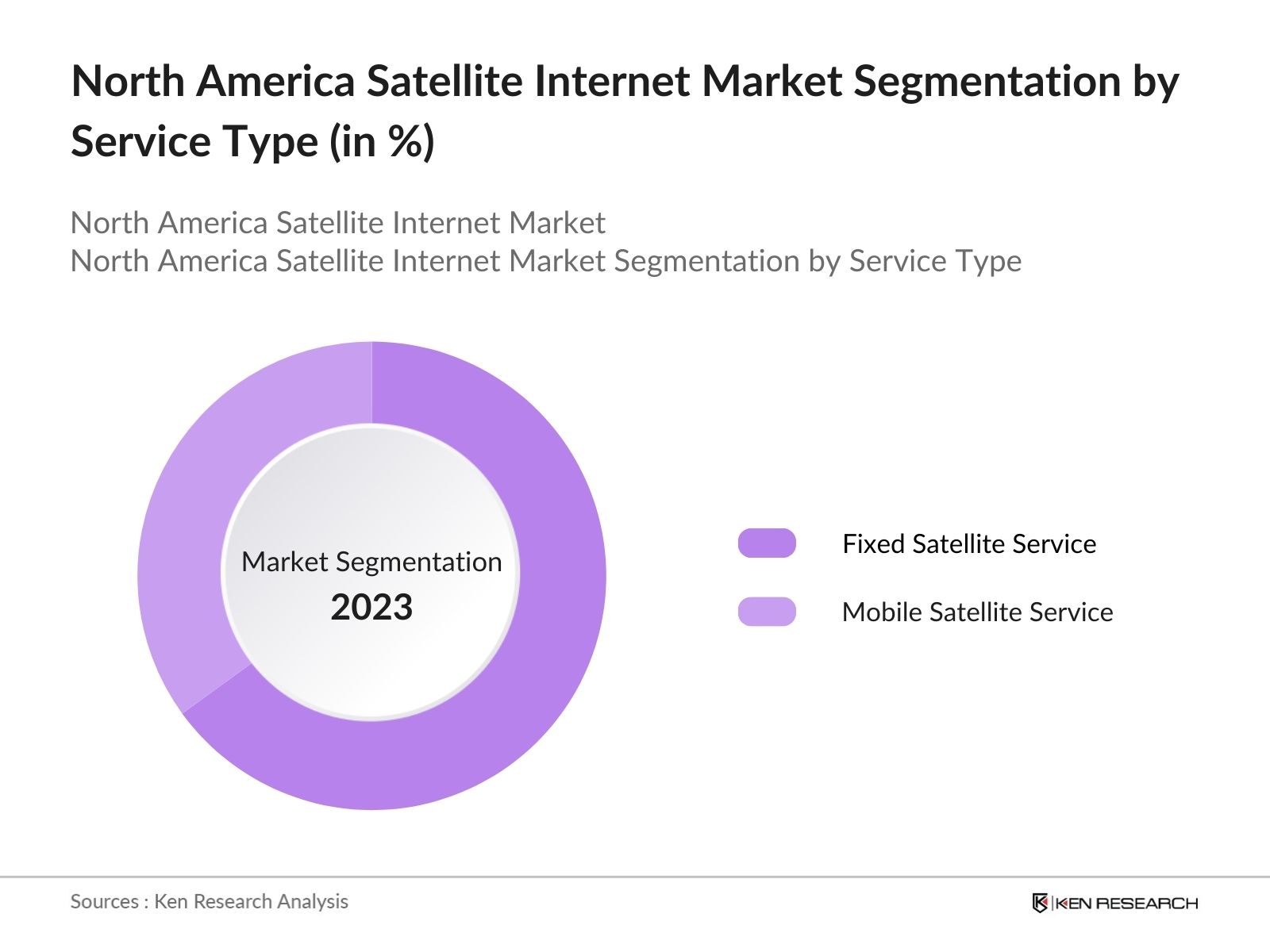

By Service Type: The market is segmented by service type into Fixed Satellite Service and Mobile Satellite Service. Fixed Satellite Service dominates the market share under the service type segmentation. This dominance is largely due to its established presence in providing stable internet connectivity to rural and remote areas, where traditional broadband infrastructure is either too expensive or impossible to implement.

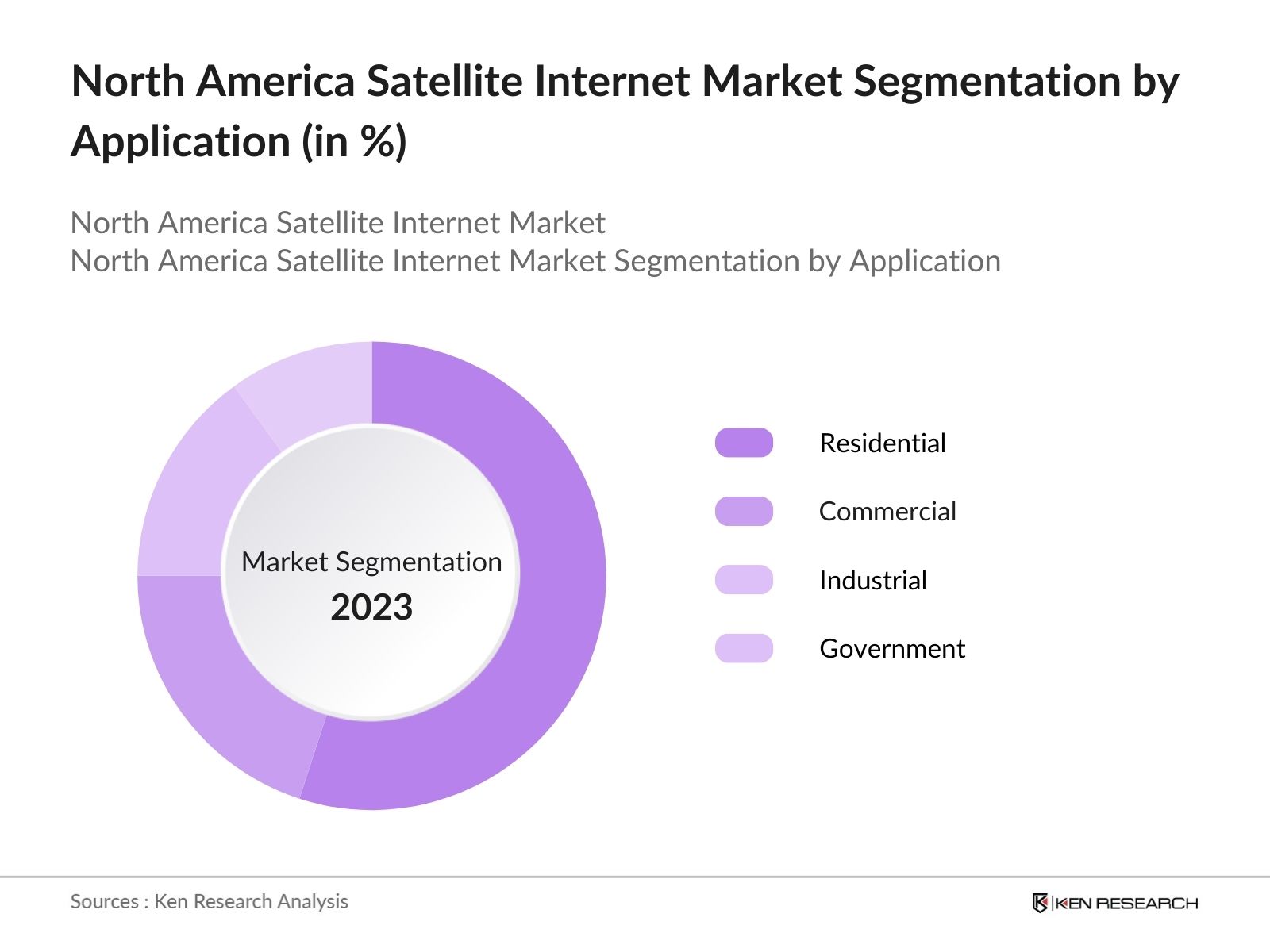

By Application: The market is segmented by application into Residential, Commercial, Industrial, and Government. Residential applications hold the dominant market share due to the rising demand for internet connectivity in rural and remote households. Satellite internet is a preferred solution for regions lacking fiber-optic or traditional broadband networks. The adoption of satellite internet for residential use has soared, especially with the increase in remote working and schooling, which has amplified the need for reliable home internet services.

North America Satellite Internet Market Competitive Landscape

The market is dominated by both global giants and innovative new players. Companies like SpaceX (Starlink) and Hughes Network Systems have leveraged advanced satellite technology to secure a significant market share.

|

Company Name |

Year of Establishment |

Headquarters |

No. of Satellites |

Global Constellation Size |

Customer Reach |

Bandwidth Capacity (Gbps) |

Service Area Coverage |

Technology Innovation |

|

SpaceX (Starlink) |

2002 |

Hawthorne, California |

||||||

|

Hughes Network Systems |

1971 |

Germantown, Maryland |

||||||

|

Viasat |

1986 |

Carlsbad, California |

||||||

|

OneWeb |

2012 |

London, UK |

||||||

|

Amazon (Project Kuiper) |

2019 |

Seattle, Washington |

North America Satellite Internet Market Analysis

Market Growth Drivers

- Rising Demand in Remote Areas: As of 2024, North America has around 10 million people living in rural and remote areas without reliable access to broadband internet. The growing demand for connectivity in these underserved regions is driving the adoption of satellite internet services. Satellite providers like Starlink are rapidly expanding coverage to meet this demand, with plans to cover an additional 3 million households by 2025.

- Increasing Government Funding for Infrastructure: The U.S. federal government allocated over $10 billion in funding for broadband infrastructure development in 2023, which includes provisions for satellite internet services. This financial backing has enabled satellite providers to enhance infrastructure and launch more satellites, with over 200 new satellites planned for 2024. This funding initiative is designed to bridge the digital divide in North America, particularly in regions where fiber-optic and terrestrial connections are not viable.

- Expanding Business and Enterprise Use: In 2024, over 500,000 small and medium enterprises (SMEs) in North America are increasingly relying on satellite internet for their business operations, particularly in remote locations where other internet services are either unreliable or non-existent. The rapid adoption of cloud-based services, video conferencing, and real-time data applications among these businesses has led to a surge in demand for satellite internet.

Market Challenges

- Regulatory Challenges and Spectrum Allocation: The allocation of spectrum for satellite internet is a complex process involving multiple regulatory bodies in North America. In 2024, there were still ongoing disputes over the distribution of satellite spectrum, particularly in the Ku-band and Ka-band frequencies. This has delayed the expansion of satellite internet services in certain regions and has created uncertainty for providers looking to scale their operations.

- Competition from Terrestrial and Wireless Providers: While satellite internet offers unique advantages in rural areas, it faces stiff competition from terrestrial broadband providers and 5G services, particularly in semi-urban and suburban regions. In 2024, around 70% of North American households have access to fiber-optic internet, and the expansion of 5G networks, which offer comparable speeds, poses a direct threat to the satellite internet market.

North America Satellite Internet Market Future Outlook

The North America Satellite Internet industry is expected to show substantial growth over the next five years, driven by continued advancements in satellite technology and increasing demand for high-speed internet in remote and rural regions.

Future Market Opportunities

- Growing Use of Satellite Internet in Disaster Recovery: In the future, satellite internet will play an increasingly important role in disaster recovery and emergency response operations. By 2028, it is estimated that over 10,000 government agencies and first responders will rely on satellite internet for communications in disaster-stricken areas where traditional infrastructure is damaged.

- Partnerships with 5G Networks for Enhanced Coverage: By 2027, satellite internet providers are expected to form strategic partnerships with 5G network operators to provide hybrid connectivity solutions. These partnerships will enhance coverage in hard-to-reach areas, providing seamless transitions between satellite and 5G networks.

Scope of the Report

|

Service Type |

Fixed Satellite Service Mobile Satellite Service |

|

Application |

Residential Commercial Industrial Government |

|

Frequency Band |

C-band Ku-band Ka-band |

|

End-User |

Individuals Enterprises Defense & Aerospace |

|

Region |

United States Canada Mexico |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Satellite Technology Providers

Internet Service Providers (ISPs)

Government and Regulatory Bodies (Federal Communications Commission)

Telecommunications Companies

Venture Capital Firms and Investors

Banks and Financial Institution

IT Infrastructure Providers

Satellite Manufacturing Companies

Companies

Players Mentioned in the Report:

SpaceX (Starlink)

Hughes Network Systems

Viasat

OneWeb

Amazon (Project Kuiper)

SES S.A.

Telesat

EchoStar Corporation

Globalstar

Iridium Communications

Table of Contents

North America Satellite Internet Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

North America Satellite Internet Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

North America Satellite Internet Market Analysis

3.1. Growth Drivers (High latency reduction, Improved bandwidth, Network resilience, Geographical reach)

3.2. Market Challenges (High initial infrastructure costs, Regulatory barriers, Weather disruptions, High competition from terrestrial services)

3.3. Opportunities (5G integration, Expanding rural connectivity, Government subsidies, Technological innovations)

3.4. Trends (Larger satellite constellations, Enhanced data speed, Satellite miniaturization, Increased government initiatives)

3.5. Government Regulations (Federal Communications Commission policies, Satellite frequency spectrum allocation, Space debris management, Compliance requirements)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape

North America Satellite Internet Market Segmentation

4.1. By Service Type (In Value %)

4.1.1. Fixed Satellite Service

4.1.2. Mobile Satellite Service

4.2. By Application (In Value %)

4.2.1. Residential

4.2.2. Commercial

4.2.3. Industrial

4.2.4. Government

4.3. By Frequency Band (In Value %)

4.3.1. C-band

4.3.2. Ku-band

4.3.3. Ka-band

4.4. By End-User (In Value %)

4.4.1. Individuals

4.4.2. Enterprises

4.4.3. Defense & Aerospace

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

North America Satellite Internet Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. SpaceX (Starlink)

5.1.2. Hughes Network Systems

5.1.3. Viasat

5.1.4. OneWeb

5.1.5. Amazon (Project Kuiper)

5.1.6. SES S.A.

5.1.7. Telesat

5.1.8. EchoStar Corporation

5.1.9. Globalstar

5.1.10. Iridium Communications

5.1.11. Inmarsat

5.1.12. AST SpaceMobile

5.1.13. ViaSat Inc.

5.1.14. Intelsat

5.1.15. Eutelsat Communications

Cross Comparison Parameters

(Market-specific parameters: No. of Satellites, Average Bandwidth per Customer, Customer Reach, Global Constellation Size, Service Availability, Speed Range, Satellite Lifespan, Market Share by Region)

North America Satellite Internet Market Regulatory Framework

6.1. Environmental Standards (Space debris, Satellite decommissioning)

6.2. Licensing and Compliance Requirements (Regulatory bodies, Frequency licensing)

6.3. Certification Processes

North America Satellite Internet Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

North America Satellite Internet Future Market Segmentation

8.1. By Service Type (In Value %)

8.2. By Application (In Value %)

8.3. By Frequency Band (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

North America Satellite Internet Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase of the research involved creating a comprehensive map of the satellite internet market ecosystem. Extensive desk research was conducted to identify key stakeholders, industry trends, and regulatory developments impacting the North America market. The aim was to define the variables influencing market growth and to develop a framework for the subsequent analysis.

Step 2: Market Analysis and Construction

We compiled historical data on satellite launches, satellite internet adoption rates, and the average bandwidth provided by key service providers. The data was analyzed to determine the markets penetration in underserved regions and the evolving role of satellite technology in the broader telecommunications ecosystem. Market statistics were cross-verified with company filings and government reports to ensure accuracy.

Step 3: Hypothesis Validation and Expert Consultation

To validate our market assumptions, we conducted interviews with key industry experts, including representatives from major satellite internet providers and technology consultants. These consultations offered critical insights into market drivers, challenges, and technological innovations shaping the future of satellite internet services.

Step 4: Research Synthesis and Final Output

The final step involved synthesizing all the gathered data and expert insights to produce a comprehensive market report. Detailed market segmentation, company profiles, and projections for future growth were compiled, ensuring that the analysis was data-driven and aligned with industry expectations.

Frequently Asked Questions

01. How big is the North America Satellite Internet Market?

The North America Satellite Internet market is valued at USD 2.7 billion. The growth is driven by rising demand for reliable broadband access in underserved rural areas and the continued expansion of satellite constellations like SpaceXs Starlink.

02. What are the challenges in the North America Satellite Internet Market?

Key challenges in the North America Satellite Internet market include the high initial cost of deploying satellite infrastructure, weather-related disruptions to satellite services, and regulatory hurdles imposed by government agencies on satellite launches and spectrum allocation.

03. Who are the major players in the North America Satellite Internet Market?

Major players in the North America Satellite Internet market include SpaceX (Starlink), Hughes Network Systems, Viasat, OneWeb, and Amazons Project Kuiper. These companies lead due to their investment in satellite technology and their ability to offer competitive internet speeds and coverage.

04. What are the growth drivers of the North America Satellite Internet Market?

Growth in the North America Satellite Internet market is propelled by the demand for high-speed internet in remote areas, government initiatives to bridge the digital divide, and advancements in low Earth orbit (LEO) satellite technology, which offers lower latency and better bandwidth compared to traditional satellites.

05. What are the future trends in the North America Satellite Internet Market?

The North America Satellite Internet market is expected to benefit from the expansion of LEO satellite constellations, increased integration with 5G networks, and partnerships between satellite internet providers and terrestrial telecom operators to improve service offerings and market reach.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.