North America Self Checkout System Market Outlook to 2030

Region:North America

Author(s):Meenakshi Bisht

Product Code:KROD7595

November 2024

81

About the Report

North America Self Checkout System Market Overview

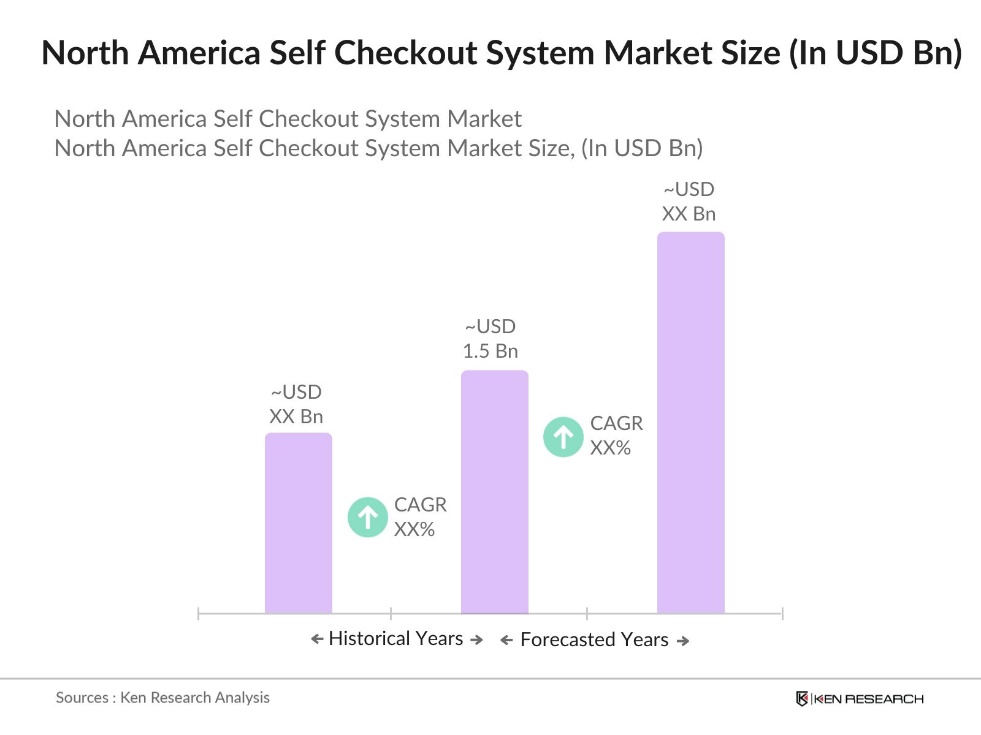

- The North America Self Checkout System Market is valued at USD 1.5 billion, according to the latest reports. This growth is driven by several factors, including the increased adoption of automated solutions in the retail sector, a need for reduced labor costs, and rising consumer preference for contactless shopping experiences. The expansion of major retail chains and technological advancements such as AI and IoT have also contributed to the rise in self checkout systems across supermarkets and hypermarkets in the region, solidifying the market's growth trajectory.

- In terms of dominant cities and countries within North America, the United States remains the leading country in the market. This is largely due to its advanced retail infrastructure, wide adoption of digital payment solutions, and the increasing preference for self-service technologies in major cities like New York, Los Angeles, and Chicago. The presence of major retailers such as Walmart and Target, who have integrated self checkout systems as part of their omnichannel strategy, further supports the dominance of the U.S. in this market.

- Point of Sale (POS) systems, including self-checkout, are subject to a variety of regulations in North America. In 2023, the U.S. saw the introduction of new consumer protection laws, focusing on transparency in digital payments. Retailers must ensure that their self-checkout systems comply with these regulations to avoid fines or litigation. Compliance with emerging digital payment regulations is particularly important as North American governments push for stronger consumer protections.

North America Self Checkout System Market Segmentation

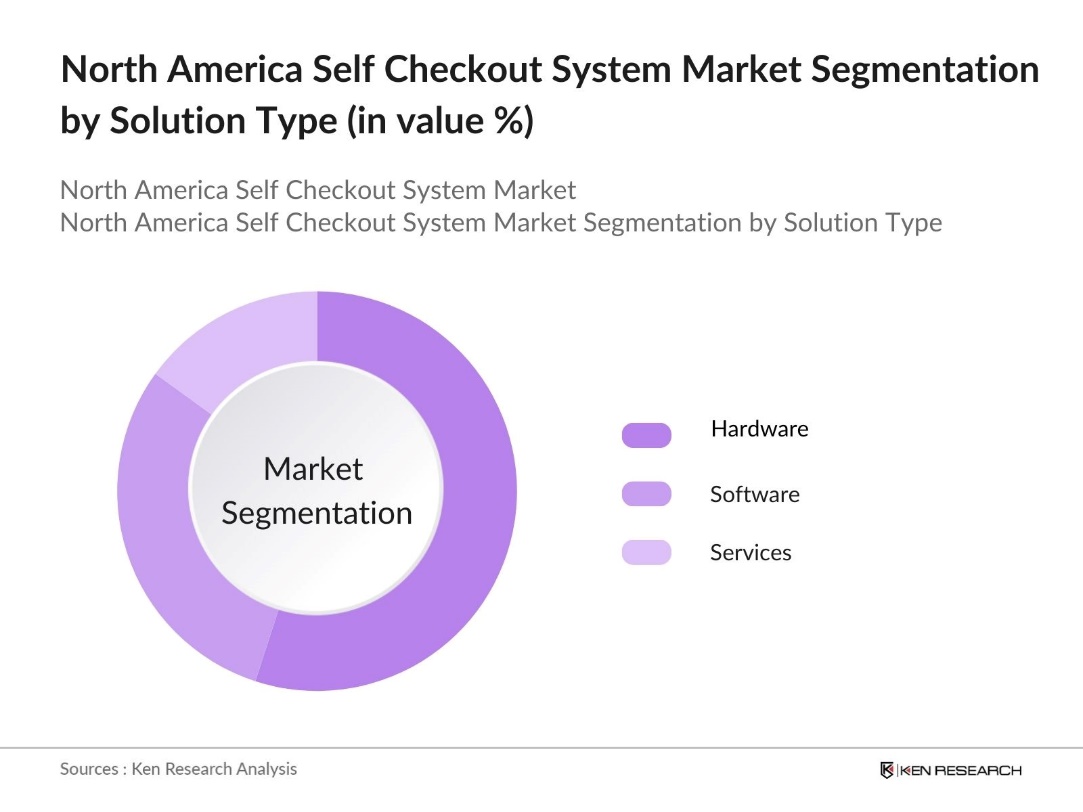

By Solution Type: The North America self checkout system market is segmented by solution type into hardware, software, and services. The hardware segment holds the dominant market share due to the necessity of physical equipment like barcode scanners, cash registers, and payment terminals in the deployment of self checkout systems. Retailers, especially large supermarket chains, rely on this hardware to enable seamless customer experiences, making this segment crucial to the market's structure.

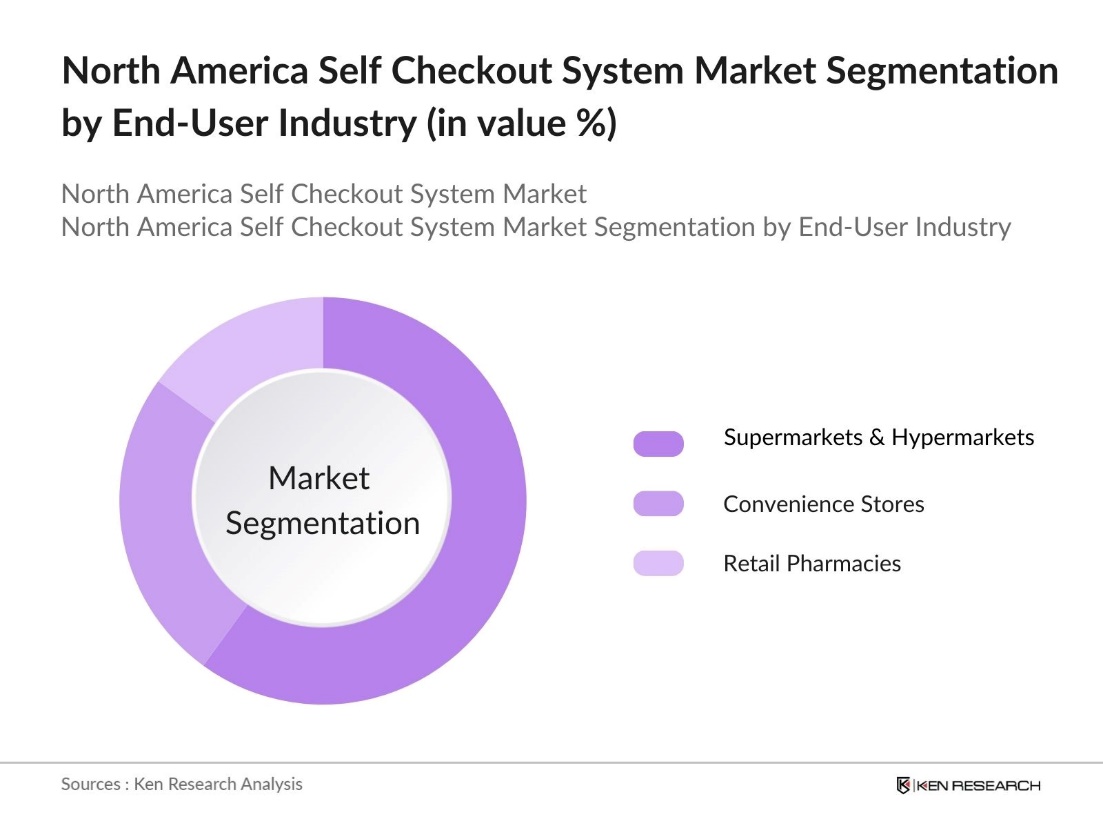

By End-User Industry: The North America self checkout system market is segmented into supermarkets and hypermarkets, convenience stores, and retail pharmacies. Supermarkets and hypermarkets are the dominant players in the end-user industry due to the high volume of transactions and large footfall. These retail spaces prioritize speed and efficiency in their checkout processes, leading to widespread adoption of self checkout systems. Furthermore, the ability to handle a high volume of customers with minimal human interaction has made this segment a key driver for market growth.

North America Self Checkout System Market Competitive Landscape

The market is dominated by several key players. These companies have established themselves by offering cutting-edge technology, comprehensive customer service, and strong distribution networks. The major players have leveraged their technological expertise to provide innovative solutions such as AI integration, mobile payments, and enhanced security features, which continue to push the boundaries of self checkout systems.

|

Company Name |

Year of Establishment |

Headquarters |

Revenue (USD Mn) |

R&D Expenditure |

Regional Presence |

Product Portfolio |

Key Customers |

Recent M&A Activity |

|

NCR Corporation |

1884 |

Atlanta, GA |

||||||

|

Diebold Nixdorf, Inc. |

1859 |

Hudson, OH |

||||||

|

Toshiba Global Commerce Solutions |

2012 |

Durham, NC |

||||||

|

Fujitsu Limited |

1935 |

Tokyo, Japan |

||||||

|

ITAB Group |

1972 |

Jnkping, Sweden |

North America Self Checkout System Industry Analysis

Growth Drivers

- Retail Store Automation: The North American retail sector has been increasingly automating to improve operational efficiency. By 2023, the retail industry in the U.S. employed over 15.43 million people, but labor shortages due to shifts in employment preferences have driven the need for automated solutions like self-checkout systems. Retailers in major markets such as the U.S. and Canada have implemented automation of stores, enhanced efficiency and reducing manual workload. The rise of retail e-commerce, also pushes physical stores toward automation to stay competitive.

- Technological Advancements (AI, IoT): Technological advancements such as AI and IoT are revolutionizing the self-checkout systems market. AI-driven solutions enhance customer experience by predicting purchasing behaviors, while IoT enables real-time inventory monitoring, reducing stockouts by up to 15%. For instance, smart mirrors and RFID tags are being utilized to improve product interaction and personalize shopping experiences. The retail tech sector in North America is expected to continue leveraging these technologies for sustained growth.

- Labor Cost Savings: Self-checkout systems help retailers significantly reduce labor costs by minimizing the need for staff. With ongoing labor shortages in North America, businesses are increasingly adopting automated solutions to operate efficiently with fewer employees. These systems allow retailers to cut wage expenses while maintaining service quality, improving overall operational efficiency. This shift helps businesses manage costs and resources more effectively, especially in large retail environments.

Market Challenges

- Data Privacy and Security Concerns: As self-checkout systems become more widespread, concerns around data privacy and security grow. Retailers must implement strong security measures to protect consumer information, but many struggle with compliance due to evolving regulations like PCI-DSS and GDPR. Failure to meet these standards can lead to penalties, making it especially challenging for smaller retailers to adopt such systems, as the risks of non-compliance are significant.

- Complex Integration into Existing Systems: Retailers often face difficulties when integrating self-checkout systems into their existing infrastructure. Older systems may require expensive upgrades to support new technology, complicating the process. Smaller retailers, in particular, may hesitate to adopt self-checkout systems due to concerns about technical challenges and the complexities involved in ensuring compatibility with their current systems.

North America Self Checkout System Market Future Outlook

Over the next five years, the North America self checkout system market is poised for significant growth, driven by advancements in automation, increasing adoption by small and medium-sized retailers, and rising consumer demand for contactless shopping experiences. The ongoing digital transformation across various industries, coupled with the integration of artificial intelligence and machine learning in retail technology, will further enhance the capabilities of self checkout systems, leading to broader adoption and market expansion.

Market Opportunities

- Integration with Mobile Payment Solutions: The expansion of mobile payment solutions offers significant opportunities for the self-checkout market. Retailers integrating these options with self-checkout systems can enhance transaction speeds and improve customer convenience. This also allows for seamless integration with loyalty programs, encouraging repeat business. Small and medium retailers, who previously lacked the infrastructure for mobile payments, are increasingly adopting these systems to remain competitive and cater to evolving consumer preferences.

- Expansion into Small and Medium Retailers: Self-checkout systems present a growing opportunity for small and medium-sized retailers. With more affordable and simplified solutions becoming available, these retailers are beginning to recognize the operational efficiencies self-checkout provides. By adopting this technology, they can reduce staffing needs, serve customers more quickly, and improve overall business performance, making it an appealing solution for retailers aiming to optimize their operations.

Scope of the Report

|

By Solution Type |

Hardware Software Services |

|

By End-User Industry |

Supermarkets Convenience Stores Pharmacies |

|

By Mode of Payment |

Card Payments Digital Wallets Mobile Payments |

|

By Technology |

Barcode Scanners RFID NFC |

|

By Region |

United States Canada Mexico |

Products

Key Target Audience

Self Checkout System Manufacturers

Technology Integrators and Providers

Large Retail Pharmacies

Retail Facility Management Companies

Retail Design and Infrastructure Firms

Government and Regulatory Bodies (e.g., Federal Trade Commission)

Investors and venture capital Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

NCR Corporation

Diebold Nixdorf, Inc.

Toshiba Global Commerce Solutions

Fujitsu Limited

ITAB Group

StrongPoint

ECR Software Corporation

Pan-Oston Co.

Gilbarco Veeder-Root

Olea Kiosks Inc.

Table of Contents

1. North America Self Checkout System Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Self Checkout System Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Self Checkout System Market Analysis

3.1. Growth Drivers [Retail Expansion, Labor Shortages, Digital Transformation]

3.1.1. Retail Store Automation

3.1.2. Technological Advancements (AI, IoT)

3.1.3. Labor Cost Savings

3.1.4. Customer Preference for Contactless Payment

3.2. Market Challenges [Cybersecurity, High Initial Costs]

3.2.1. Data Privacy and Security Concerns

3.2.2. Complex Integration into Existing Systems

3.2.3. High Capital Investment for Deployment

3.3. Opportunities [Emerging Technologies, Small Retailers Adoption]

3.3.1. Integration with Mobile Payment Solutions

3.3.2. Expansion into Small and Medium Retailers

3.3.3. Enhanced AI-Driven Customer Insights

3.4. Trends [Omnichannel Retail, AI, and Machine Learning]

3.4.1. Growing Adoption of Cloud-Based Checkout Systems

3.4.2. Increased Use of AI for Personalization

3.4.3. Rise in Contactless Shopping Technologies

3.5. Government Regulation [Consumer Protection, Payment Regulations]

3.5.1. PCI-DSS Compliance

3.5.2. GDPR and Data Privacy Regulations

3.5.3. Regulatory Compliance for POS Systems

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. North America Self Checkout System Market Segmentation

4.1. By Solution Type (In Value %)

4.1.1. Hardware

4.1.2. Software

4.1.3. Services

4.2. By End-User Industry (In Value %)

4.2.1. Supermarkets and Hypermarkets

4.2.2. Convenience Stores

4.2.3. Retail Pharmacies

4.3. By Mode of Payment (In Value %)

4.3.1. Card Payments

4.3.2. Digital Wallets

4.3.3. Mobile Payments

4.4. By Technology (In Value %)

4.4.1. Barcode Scanners

4.4.2. RFID Technology

4.4.3. NFC Technology

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5. North America Self Checkout System Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. NCR Corporation

5.1.2. Diebold Nixdorf, Inc.

5.1.3. Toshiba Global Commerce Solutions

5.1.4. Fujitsu Limited

5.1.5. ITAB Group

5.1.6. ECR Software Corporation

5.1.7. Gilbarco Veeder-Root

5.1.8. StrongPoint

5.1.9. Pan-Oston Co.

5.1.10. Cass Information Systems

5.1.11. Olea Kiosks Inc.

5.1.12. Slabb Inc.

5.1.13. Zebra Technologies Corporation

5.1.14. Versatile Credit

5.1.15. Aila Technologies

5.2. Cross Comparison Parameters [Revenue, Employee Count, Headquarters, Regional Presence, Product Portfolio, R&D Expenditure, Customer Base, Partnerships]

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Private Equity Investments

6. North America Self Checkout System Market Regulatory Framework

6.1. Data Privacy and Security Compliance

6.2. Payment System Regulations

6.3. Certification and Testing Requirements

7. North America Self Checkout System Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Self Checkout System Future Market Segmentation

8.1. By Solution Type (In Value %)

8.2. By End-User Industry (In Value %)

8.3. By Mode of Payment (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

9. North America Self Checkout System Market Analysts' Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Segmentation Strategy

9.3. Product Development and Innovation Opportunities

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

This phase includes a comprehensive ecosystem analysis of the North America self checkout system market. Extensive secondary research, involving data from credible sources such as industry reports and government databases, is conducted to identify key market dynamics and stakeholder roles.

Step 2: Market Analysis and Construction

Historical data related to market penetration and system adoption rates is compiled and analyzed. Additionally, a detailed assessment of the revenue generated by different segments of the market helps construct an accurate market forecast.

Step 3: Hypothesis Validation and Expert Consultation

Interviews with industry experts and business leaders in retail, technology, and automation fields are conducted to validate market assumptions. These insights are essential to refine our understanding of the market dynamics and customer preferences.

Step 4: Research Synthesis and Final Output

The research synthesis involves verifying data through primary and secondary channels. This step ensures the accuracy of revenue and market share estimates, providing a comprehensive understanding of the North America self checkout system market.

Frequently Asked Questions

01 How big is the North America Self Checkout System Market?

The North America Self Checkout System Market is valued at USD 1.5 billion, driven by rising automation in the retail sector and a growing preference for contactless transactions.

02 What are the challenges in the North America Self Checkout System Market?

Challenges in North America Self Checkout System Market include high initial costs for system deployment, integration complexity, and concerns over data privacy and security, particularly with evolving regulations.

03 Who are the major players in the North America Self Checkout System Market?

Key players in the North America Self Checkout System Market include NCR Corporation, Diebold Nixdorf, Toshiba Global Commerce Solutions, Fujitsu Limited, and ITAB Group, who dominate through technological innovation and strategic partnerships.

04 What are the growth drivers of the North America Self Checkout System Market?

The North America Self Checkout System Market growth drivers include advancements in retail technology, increasing labor costs, and consumer preference for faster, contactless checkout experiences.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.