North America Semiconductor Market Outlook to 2030

Region:Mexico

Author(s):Naman Rohilla

Product Code:KROD4753

Region:Mexico

Author(s):Naman Rohilla

Product Code:KROD4753

December 2024

98

The North America semiconductor market is dominated by several key players, including large multinational corporations with extensive R&D capabilities and innovative technologies. These companies maintain strong positions due to their robust supply chain networks, partnerships with major OEMs, and continuous investment in new technologies such as advanced node manufacturing, AI chips, and quantum computing components.

|

Company |

Establishment Year |

Headquarters |

Revenue (USD Bn) |

R&D Spend (USD Bn) |

No. of Patents |

Fab Ownership |

Technology Node Capability |

Major Partnerships |

|

Intel Corporation |

1968 |

Santa Clara, CA, USA |

- |

- |

- |

- |

- |

- |

|

NVIDIA Corporation |

1993 |

Santa Clara, CA, USA |

- |

- |

- |

- |

- |

- |

|

Qualcomm Technologies, Inc. |

1985 |

San Diego, CA, USA |

- |

- |

- |

- |

- |

- |

|

Texas Instruments |

1930 |

Dallas, TX, USA |

- |

- |

- |

- |

- |

- |

|

Advanced Micro Devices, Inc. |

1969 |

Santa Clara, CA, USA |

- |

- |

- |

- |

- |

- |

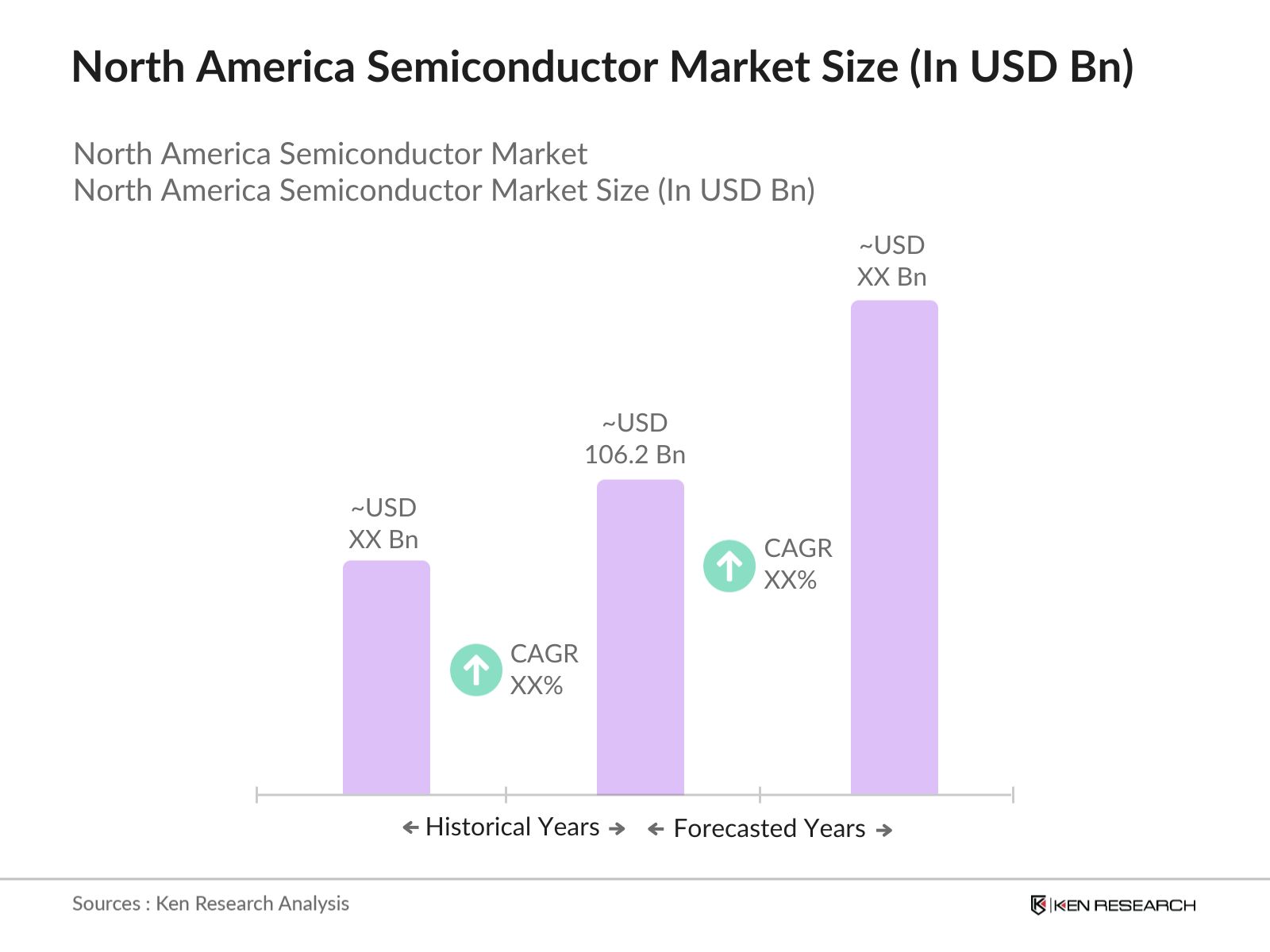

Over the next five years, the North America semiconductor market is expected to experience sustained growth, driven by the increasing integration of semiconductors into emerging technologies such as electric vehicles, autonomous driving, AI-driven applications, and IoT-enabled devices. The demand for high-performance chips in data centers and AI applications will continue to fuel market expansion, alongside government incentives to bolster local manufacturing.

|

By Product Type |

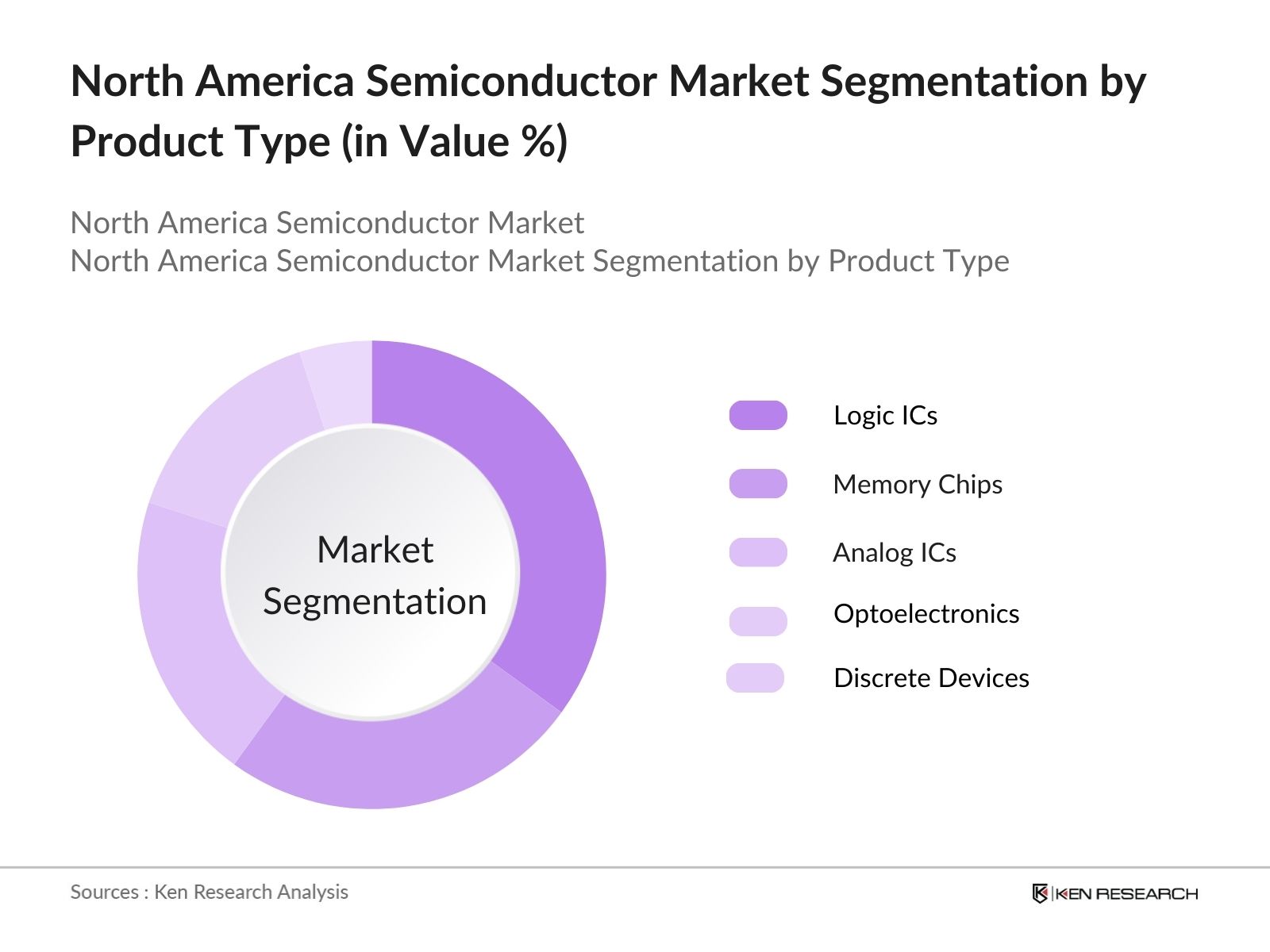

Memory Chips Logic ICs Analog ICs Optoelectronics Discrete Devices |

|

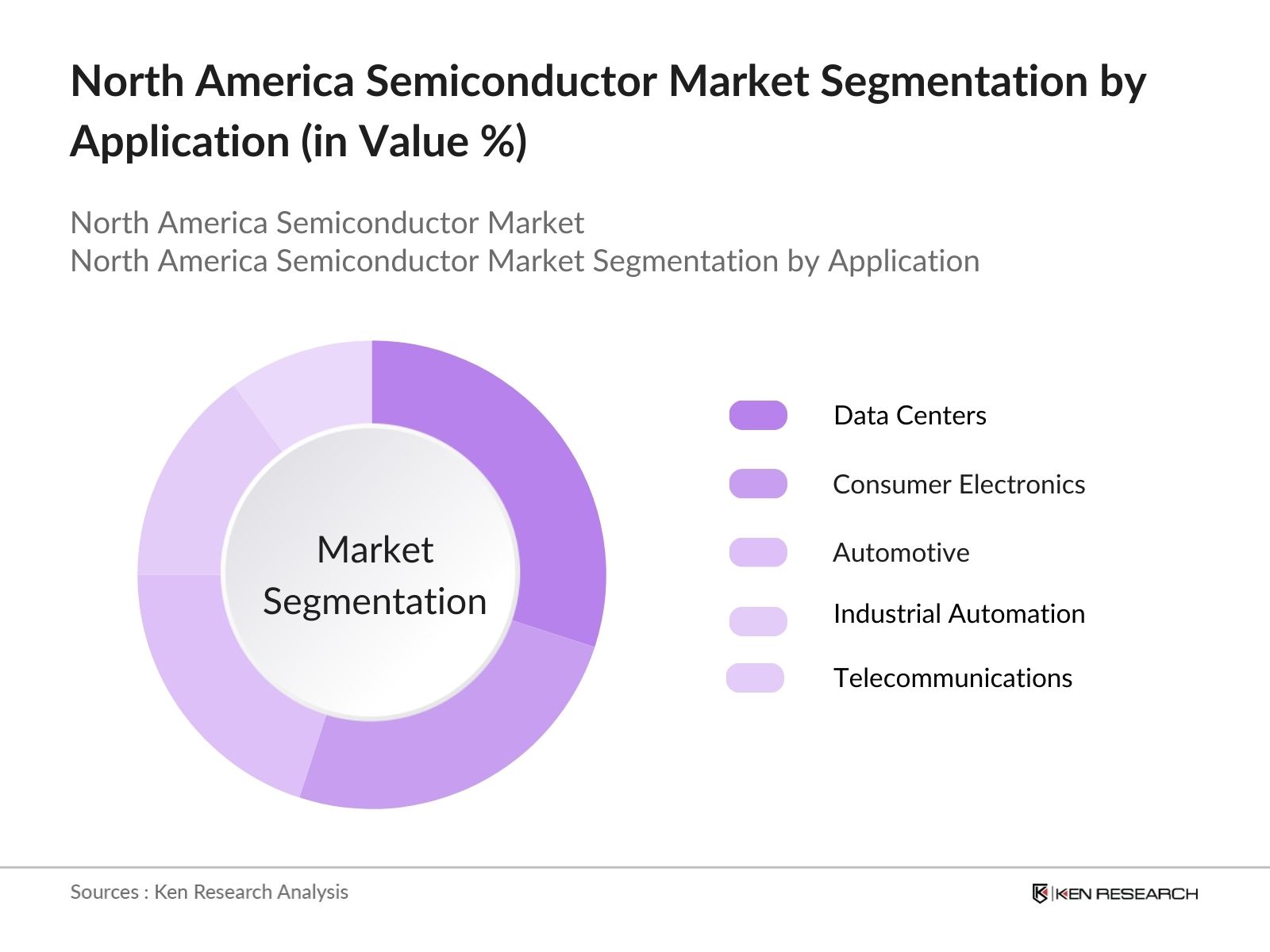

By Application |

Automotive Consumer Electronics Industrial Automation Telecommunications Data Centers |

|

By Material Type |

Silicon Gallium Nitride Silicon Carbide Germanium |

|

By Technology Node |

5nm and Below 7nm to 14nm 28nm and Above |

|

By Region |

United States Canada Mexico |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Technological Advancements (AI, IoT, 5G, Quantum Computing)

3.1.2. Increasing Demand in Automotive Industry (EVs, ADAS)

3.1.3. Government Initiatives (CHIPS Act, Supply Chain Resilience)

3.1.4. Demand in Data Centers (Cloud Computing, AI Workloads)

3.2. Market Challenges

3.2.1. Supply Chain Disruptions (Geopolitical Tensions, Natural Disasters)

3.2.2. High R&D and Production Costs

3.2.3. Shortage of Skilled Workforce

3.3. Opportunities

3.3.1. Growth in 5G Infrastructure Deployment

3.3.2. Expansion in Emerging Markets (Wearables, Smart Devices)

3.3.3. Rise in AI and Machine Learning Applications

3.4. Trends

3.4.1. Shift Towards Advanced Packaging and Miniaturization

3.4.2. Increase in Semiconductor Foundry Investments

3.4.3. Collaboration in R&D and Innovation (Chiplet Technology, Advanced Lithography)

3.5. Government Regulations

3.5.1. North American Free Trade Agreements (USMCA, Tariff Structures)

3.5.2. Export Control Regulations (Semiconductor Equipment and Technology)

3.5.3. Environmental Regulations (Sustainable Manufacturing Practices)

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.7.1. Suppliers (Raw Material, Equipment)

3.7.2. Manufacturers (IDMs, Foundries)

3.7.3. Distributors and OEMs

3.8. Porters Five Forces Analysis

3.8.1. Bargaining Power of Suppliers

3.8.2. Bargaining Power of Buyers

3.8.3. Threat of New Entrants

3.8.4. Threat of Substitutes

3.8.5. Industry Rivalry

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Memory Chips (DRAM, NAND)

4.1.2. Logic ICs (Microprocessors, SoCs)

4.1.3. Analog ICs (Power Management, Signal Processing)

4.1.4. Optoelectronics (LEDs, Image Sensors)

4.1.5. Discrete Devices (Transistors, Diodes)

4.2. By Application (In Value %)

4.2.1. Automotive

4.2.2. Consumer Electronics

4.2.3. Industrial Automation

4.2.4. Telecommunications

4.2.5. Data Centers

4.3. By Material Type (In Value %)

4.3.1. Silicon

4.3.2. Gallium Nitride (GaN)

4.3.3. Silicon Carbide (SiC)

4.3.4. Germanium

4.4. By Technology Node (In Value %)

4.4.1. 5nm and Below

4.4.2. 7nm to 14nm

4.4.3. 28nm and Above

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5.1. Detailed Profiles of Major Companies

5.1.1. Intel Corporation

5.1.2. NVIDIA Corporation

5.1.3. Qualcomm Technologies, Inc.

5.1.4. Texas Instruments

5.1.5. Advanced Micro Devices, Inc. (AMD)

5.1.6. Micron Technology, Inc.

5.1.7. Broadcom Inc.

5.1.8. ON Semiconductor Corporation

5.1.9. Marvell Technology Group Ltd.

5.1.10. Analog Devices, Inc.

5.1.11. GlobalFoundries

5.1.12. Lam Research Corporation

5.1.13. Applied Materials, Inc.

5.1.14. Skyworks Solutions, Inc.

5.1.15. Synopsys, Inc.

5.2. Cross Comparison Parameters (Revenue, Market Cap, R&D Expenditure, No. of Patents, Fab Ownership, Technology Node Capability, Geographic Reach, Major Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants and Incentives

6.1. Environmental Compliance (Emissions Control, Waste Management)

6.2. Trade Compliance (Import/Export Licensing, Tariffs)

6.3. Certification and Standards (ISO, JEDEC, IPC Standards)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Material Type (In Value %)

8.4. By Technology Node (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial phase involves identifying critical market variables, including product segments, key application industries, and technology adoption rates across the North America Semiconductor Market. Extensive desk research is conducted to gather relevant data and create a market map.

In this phase, historical market data is analyzed to determine growth rates, market penetration, and demand fluctuations. Additionally, the research focuses on identifying key growth areas within product segments like memory chips and logic ICs.

Consultations with industry experts from major semiconductor firms and OEMs provide firsthand insights into production cycles, market trends, and technology investments. This information is cross-verified through market reports and databases.

The final synthesis involves corroborating primary and secondary research findings to present a validated and accurate market forecast. This ensures that the report provides comprehensive insights into the North America Semiconductor Market, focusing on key drivers, challenges, and opportunities.

The North America semiconductor market is valued at USD 106.2 billion, driven by technological advancements in AI, IoT, and 5G. The increasing demand from industries such as automotive and consumer electronics significantly contributes to the market size.

Key challenges in the North America semiconductor market include supply chain disruptions, rising production costs, and a shortage of skilled labor. These factors have constrained the industry's ability to meet increasing demand, leading to significant market strain.

The North America semiconductor market is dominated by companies like Intel, NVIDIA, Qualcomm, Texas Instruments, and AMD, which maintain significant market influence through innovation and strategic partnerships.

The North America semiconductor market growth drivers include increasing demand for semiconductor applications in AI, 5G networks, automotive electronics, and data centers. Government initiatives like the CHIPS Act also support market expansion.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.