North America Smart Grid Market Outlook to 2030

Region:North America

Author(s):Vijay Kumar

Product Code:KROD7642

November 2024

80

About the Report

North America Smart Grid Market Overview

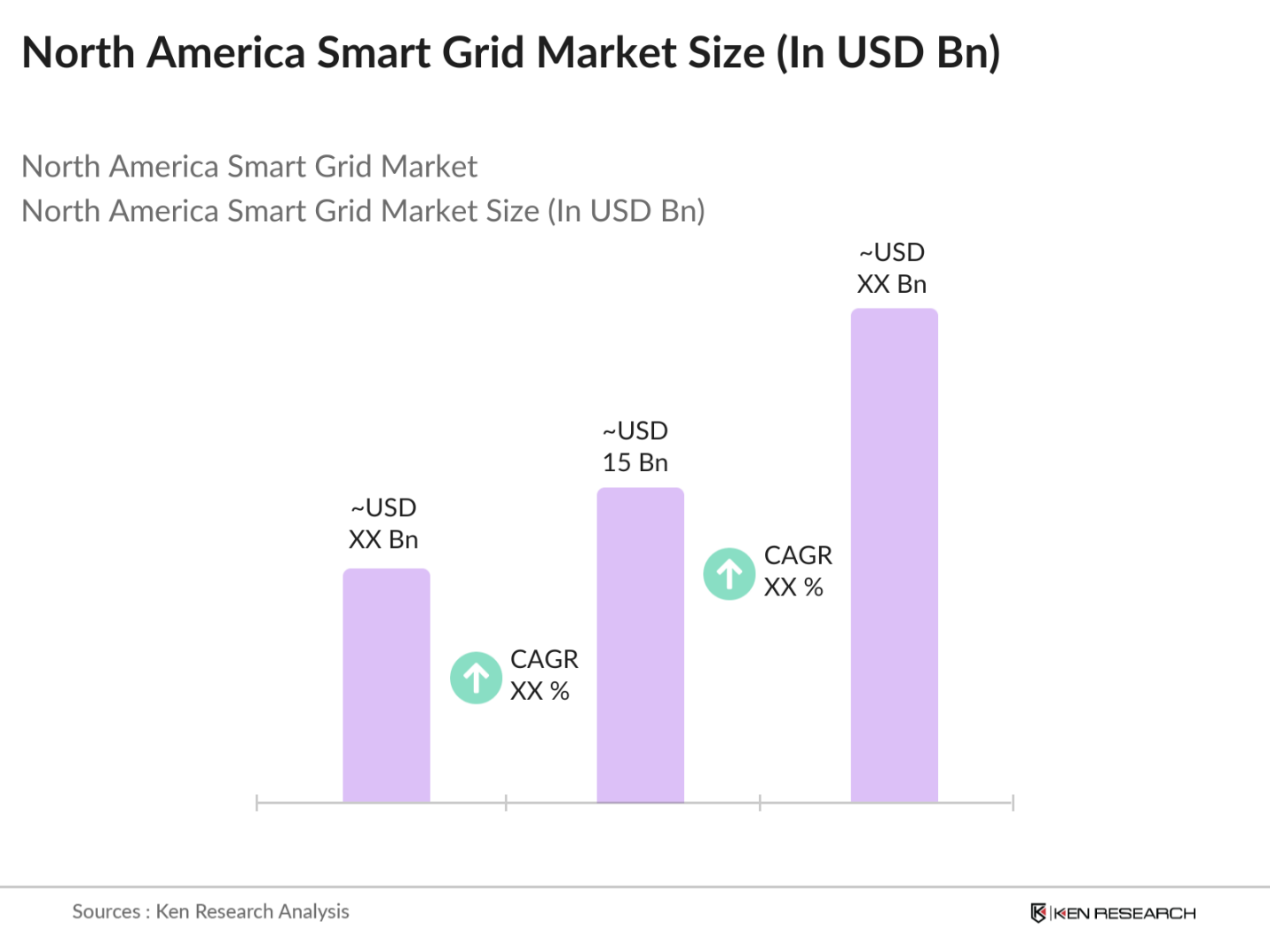

- The North America Smart Grid market is valued at USD 15 billion, based on a five-year historical analysis. This market is primarily driven by the growing adoption of renewable energy sources, increasing investments in grid modernization, and government initiatives promoting energy efficiency. With the integration of smart meters, advanced communication networks, and demand response systems, the smart grid is playing a critical role in optimizing electricity consumption and reducing energy wastage, particularly in urban centers and key industrial regions across the U.S. and Canada.

- The dominant countries in the North American market are the United States and Canada. The U.S. dominates due to large-scale investments in energy infrastructure upgrades, coupled with government initiatives aimed at increasing energy efficiency and reducing carbon emissions. Canada follows closely, benefiting from government policies promoting renewable energy integration and smart grid development, especially in major urban centers like Toronto and Vancouver. Both countries have well-developed energy infrastructures, making them key players in the regional market.

- Governments in North America, particularly in the U.S. and Canada, are implementing policies to modernize the electrical grid. In 2024, the U.S. government continues to fund grid modernization through initiatives like the Grid Modernization Initiative (GMI), which received $3 billion under the Bipartisan Infrastructure Law. Meanwhile, state-level policies, such as Californias 100% Clean Energy Act, mandate a transition to renewable energy by 2045, pushing utilities to adopt smart grid technologies.

North America Smart Grid Market Segmentation

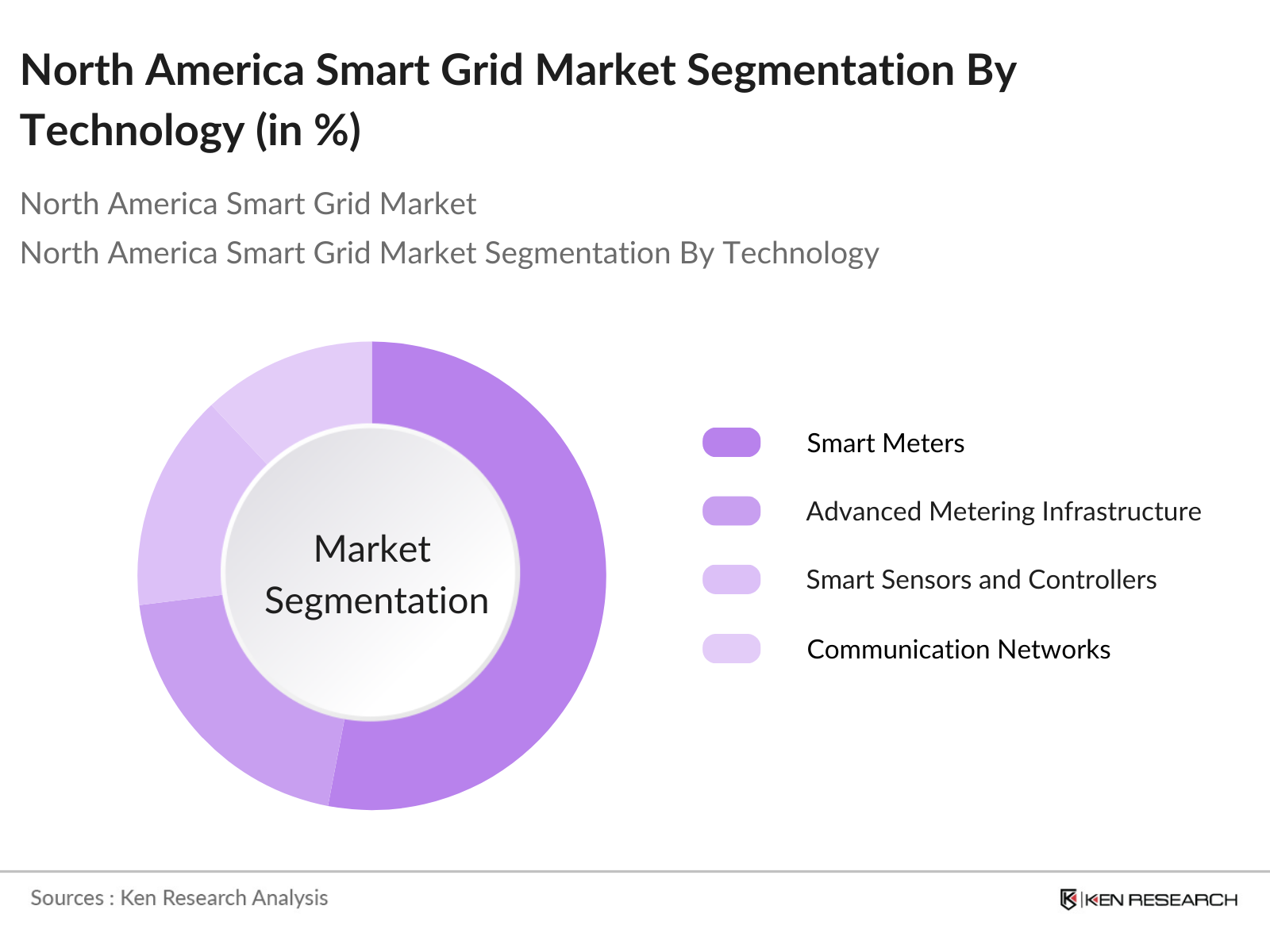

By Technology: The North America Smart Grid market is segmented by technology into Smart Meters, Advanced Metering Infrastructure (AMI), Smart Sensors and Controllers, Communication Networks, and Grid-Edge Technologies. Among these, Smart Meters hold a dominant market share in 2023. Their widespread adoption is primarily due to government mandates and incentive programs that promote energy efficiency.

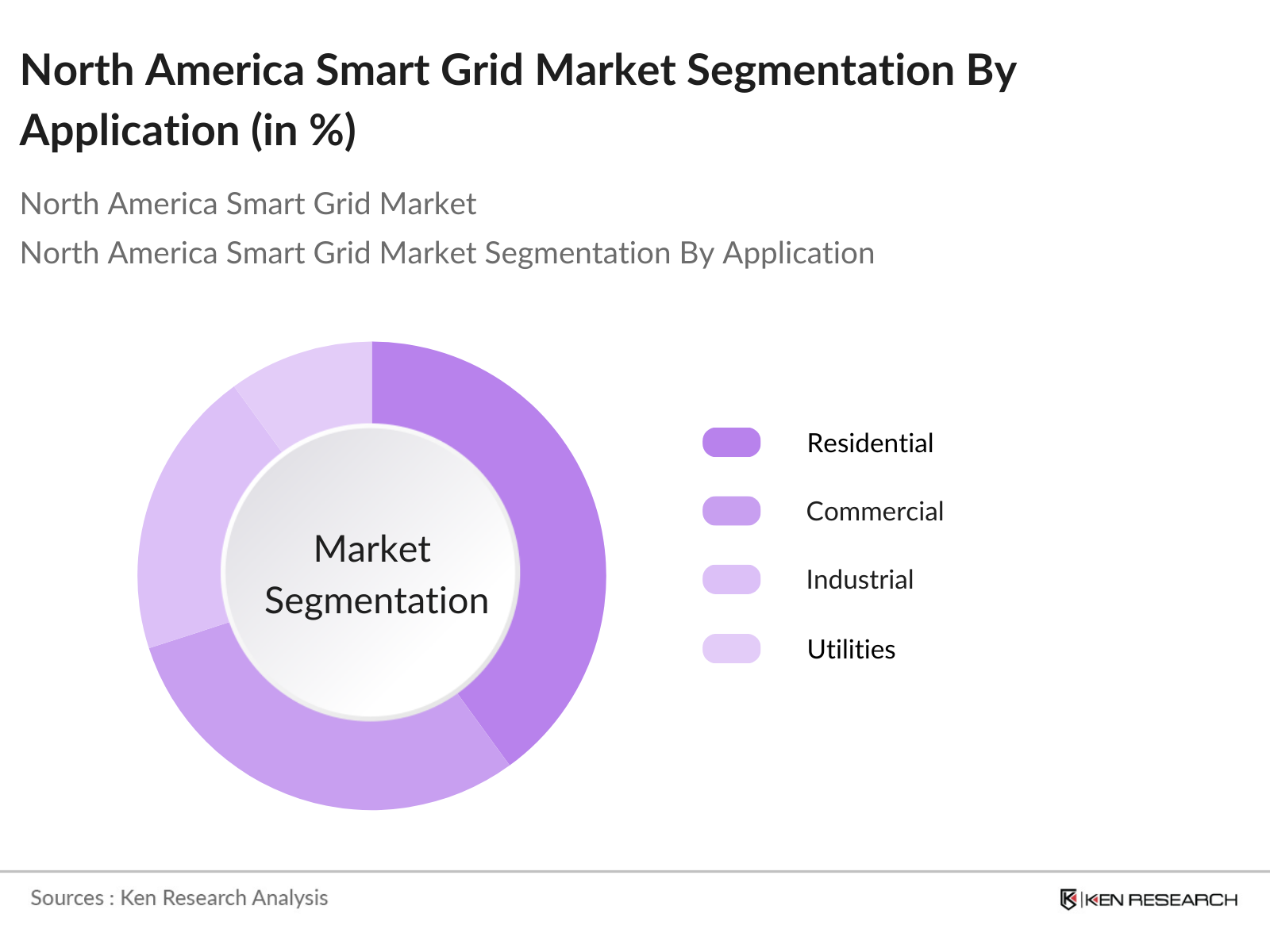

By Application: The North America Smart Grid market is also segmented by application into Residential, Commercial, Industrial, and Utilities. The Residential sector dominates the market share in 2023. This is attributed to the increasing number of smart homes equipped with connected devices and smart energy management systems. Homeowners are increasingly adopting smart meters, driven by a desire for greater control over their energy consumption, as well as growing awareness of energy conservation.

North America Smart Grid Market Competitive Landscape

The North America Smart Grid market is dominated by a few key players, which include both regional and global companies. These companies leverage their technological expertise and large-scale deployment capabilities to maintain a competitive edge in the market. Notable players include General Electric, Siemens AG, and ABB Ltd., who offer a wide range of smart grid solutions.

North America Smart Grid Industry Analysis

Growth Drivers

- Integration of Renewable Energy Sources: The shift toward integrating renewable energy sources such as solar and wind into the North American energy grid is accelerating, driven by government mandates and increasing public awareness of environmental sustainability. In 2024, the U.S. renewable energy generation is projected to account for 24% of total electricity generation, up from 22% in 2022, according to the U.S. Energy Information Administration (EIA). Moreover, Canada has been a leader in renewable energy, with 82% of its electricity generated from renewable sources, particularly hydropower, as of 2023.

- Rising Electricity Demand: Electricity demand in North America is projected to rise significantly due to increasing population and electrification trends. The U.S. alone saw a 2.6% increase in electricity consumption in 2023, according to the EIA, driven by economic growth and greater adoption of electric vehicles (EVs). Canada also projects increased energy consumption by 2030, with much of this demand being met through the integration of renewable energy into the grid.

- Grid Modernization Projects: The U.S. and Canada are investing heavily in grid modernization to improve grid resilience, reduce outages, and integrate renewable energy. In 2024, the U.S. government has allocated $10.5 billion toward modernizing the grid as part of its broader infrastructure strategy. These investments include upgrading substations, deploying advanced distribution management systems, and integrating distributed energy resources (DERs).

Market Challenges

- High Infrastructure Investment Costs: The cost of implementing smart grid technologies is a significant challenge. Upgrading the grid requires substantial investments in advanced metering infrastructure, automation systems, and cybersecurity protocols. In the U.S., the Department of Energy estimated that over $400 billion is needed to fully modernize the grid by 2035. Canada faces similar challenges, with estimated costs of $2.5 billion for key infrastructure upgrades as part of its Smart Grid Program.

- Data Privacy and Security Concerns: As smart grids integrate more IoT devices and digital communication systems, the risk of cyberattacks and data breaches increases. In 2023, the U.S. Department of Homeland Security recorded a 30% rise in cyberattacks targeting energy infrastructure, reflecting the growing need for enhanced grid cybersecurity. Canada also reported increased cyber threats to its energy sector, with over 100 attempted attacks on its grid infrastructure in 2023 alone.

North America Smart Grid Market Future Outlook

Over the next five years, the North America Smart Grid market is expected to experience significant growth driven by continuous advancements in smart grid technologies, increasing adoption of renewable energy, and ongoing government investments in grid modernization. The integration of electric vehicles (EVs) and distributed energy resources (DERs) is anticipated to further boost the market, along with innovations in data analytics and artificial intelligence (AI) for grid management.

Market Opportunities

- Increased Adoption of Smart Meters: Smart meter installations continue to rise across North America, enabling better energy management and grid efficiency. In 2024, over 115 million smart meters were deployed in the U.S., covering 70% of households, according to the U.S. Energy Information Administration (EIA). Canada has also seen widespread adoption, with smart meters installed in 60% of households as of 2023. These devices provide real-time data on electricity usage, helping utilities manage demand and consumers optimize their energy consumption, leading to lower costs and improved grid reliability.

- Demand for Energy Efficiency and Sustainability: With increasing demand for energy efficiency, smart grid technologies are playing a pivotal role in reducing carbon emissions and promoting sustainability. In 2024, the U.S. Department of Energy projected that smart grid initiatives could reduce annual carbon dioxide emissions by 150 million metric tons, equivalent to taking 32 million cars off the road. Canada's focus on sustainability has led to government-funded projects aimed at reducing greenhouse gas emissions by 30% by 2030, further driving demand for smart grid technologies that optimize energy consumption.

Scope of the Report

|

By Technology |

Smart Meters, Advanced Metering Infrastructure (AMI) Smart Sensors Communication Networks Grid-Edge Technologies |

|

By Application |

Residential Commercial Industrial Utilities |

|

By Component |

Hardware Software Services |

|

By Deployment |

On-Premise Cloud-Based |

|

By Region |

U.S. Canada Mexico |

Products

Key Target Audience

Utilities and Energy Providers

Smart Grid Technology Providers

Energy Management System Providers

Telecommunications Companies

Government and Regulatory Bodies (U.S. Department of Energy, Natural Resources Canada)

Investors and Venture Capital Firms

Electric Vehicle Charging Infrastructure Providers

Renewable Energy Developers

Companies

Players Mentioned in the Report

General Electric

Siemens AG

ABB Ltd.

Cisco Systems Inc.

IBM Corporation

Schneider Electric

Itron Inc.

Landis+Gyr

Honeywell International Inc.

Oracle Corporation

Table of Contents

1. North America Smart Grid Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Smart Grid Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Smart Grid Market Analysis

3.1. Growth Drivers

3.1.1. Integration of Renewable Energy Sources

3.1.2. Government Initiatives and Regulations (Federal and State-Level Policies)

3.1.3. Rising Electricity Demand

3.1.4. Grid Modernization Projects

3.2. Market Challenges

3.2.1. High Infrastructure Investment Costs

3.2.2. Data Privacy and Security Concerns

3.2.3. Lack of Interoperability Standards

3.2.4. Aging Grid Infrastructure

3.3. Opportunities

3.3.1. Increased Adoption of Smart Meters

3.3.2. Demand for Energy Efficiency and Sustainability

3.3.3. Expanding Electric Vehicle (EV) Infrastructure

3.3.4. Growing Role of Distributed Energy Resources (DERs)

3.4. Trends

3.4.1. Integration of IoT and AI in Grid Systems

3.4.2. Increasing Use of Advanced Distribution Management Systems (ADMS)

3.4.3. Adoption of Blockchain for Grid Transactions

3.4.4. Digital Twins and Predictive Maintenance Technologies

3.5. Government Regulation

3.5.1. Federal Energy Regulatory Commission (FERC) Guidelines

3.5.2. Energy Policy Act

3.5.3. State-Level Renewable Energy Standards

3.5.4. Smart Grid Investment Grant Program

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.7.1. Utilities

3.7.2. Government and Regulatory Bodies

3.7.3. Technology Providers

3.7.4. Consumers and End-Users

3.8. Porters Five Forces

3.9. Competitive Ecosystem

4. North America Smart Grid Market Segmentation

4.1. By Technology (In Value %)

4.1.1. Smart Meters

4.1.2. Advanced Metering Infrastructure (AMI)

4.1.3. Smart Sensors and Controllers

4.1.4. Communication Networks

4.1.5. Grid-Edge Technologies

4.2. By Application (In Value %)

4.2.1. Residential

4.2.2. Commercial

4.2.3. Industrial

4.2.4. Utilities

4.3. By Component (In Value %)

4.3.1. Hardware

4.3.2. Software

4.3.3. Services

4.4. By Deployment (In Value %)

4.4.1. On-Premise

4.4.2. Cloud-Based

4.5. By Region (In Value %)

4.5.1. U.S.

4.5.2. Canada

4.5.3. Mexico

5. North America Smart Grid Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. General Electric

5.1.2. Siemens AG

5.1.3. ABB Ltd.

5.1.4. Schneider Electric

5.1.5. Itron Inc.

5.1.6. Landis+Gyr

5.1.7. Cisco Systems Inc.

5.1.8. IBM Corporation

5.1.9. Honeywell International Inc.

5.1.10. Oracle Corporation

5.1.11. Eaton Corporation

5.1.12. S&C Electric Company

5.1.13. Silver Spring Networks

5.1.14. Mitsubishi Electric Corporation

5.1.15. Aclara Technologies LLC

5.2. Cross Comparison Parameters (Revenue, R&D Expenditure, Product Portfolio, Market Share, Patents, Strategic Alliances, Geographical Presence, Employee Count)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. North America Smart Grid Market Regulatory Framework

6.1. Smart Grid Interoperability Standards

6.2. Cybersecurity Requirements

6.3. Compliance with NERC (North American Electric Reliability Corporation)

6.4. Environmental and Energy Efficiency Standards

7. North America Smart Grid Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Smart Grid Future Market Segmentation

8.1. By Technology (In Value %)

8.2. By Application (In Value %)

8.3. By Component (In Value %)

8.4. By Deployment (In Value %)

8.5. By Region (In Value %)

9. North America Smart Grid Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The first step in the research process involves mapping the ecosystem of stakeholders in the North America Smart Grid market. This process includes desk research using a mix of proprietary databases and publicly available sources to gather industry-level data. Key variables such as market drivers, challenges, and growth opportunities are identified at this stage.

Step 2: Market Analysis and Construction

In this step, historical market data for the North America Smart Grid market is compiled and analyzed. This includes reviewing market penetration trends, adoption rates of smart meters and grid technologies, and revenue generation from various market segments. Additional parameters like service quality and customer satisfaction are assessed to ensure accurate revenue forecasting.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are formed and validated through interviews with industry experts, including professionals from utilities, grid technology providers, and energy consultants. These interviews help corroborate the research findings and refine market estimates.

Step 4: Research Synthesis and Final Output

The final step involves synthesizing the data collected from multiple sources and producing a comprehensive analysis of the market. This includes validation of product segment insights, sales performance, and future market projections, ensuring the accuracy of the final report.

Frequently Asked Questions

01. How big is the North America Smart Grid Market?

The North America Smart Grid market is valued at USD 15 billion, based on a five-year historical analysis. This market is primarily driven by the growing adoption of renewable energy sources, increasing investments in grid modernization, and government initiatives promoting energy efficiency.

02. What are the challenges in the North America Smart Grid Market?

Challenges include high infrastructure investment costs, cybersecurity concerns, and the need for interoperability standards to ensure seamless integration of new technologies into existing grid systems.

03. Who are the major players in the North America Smart Grid Market?

Major players include General Electric, Siemens AG, ABB Ltd., Cisco Systems, and IBM Corporation, all of which dominate the market due to their extensive product portfolios, technological expertise, and strong global presence.

04. What are the growth drivers of the North America Smart Grid Market?

The market is driven by the integration of renewable energy sources, increasing demand for reliable power, government policies promoting energy efficiency, and advancements in smart meter technologies.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.