North America Solar Panel Market Outlook to 2030

Region:North America

Author(s):Naman Rohilla

Product Code:KROD5892

December 2024

92

About the Report

North America Solar Panel Market Overview

- The North America Solar Panel Market, valued at USD 350 billion, has experienced substantial growth due to rising demand for renewable energy and government support for clean energy initiatives. Driven by the declining cost of solar technology and the expansion of large-scale solar farms, this market's growth is also bolstered by the increasing adoption of solar power in residential, commercial, and industrial sectors. The investment in solar energy infrastructure and advancements in energy storage technologies further solidify the market's potential.

- Key cities and countries in North America dominating the solar panel market include the United States and Canada. The dominance of the U.S. is attributed to its favourable regulatory environment, particularly in states like California and Texas, which offer incentives for solar adoption. Canadas position is strengthened by the countrys focus on reducing carbon emissions and transitioning to renewable energy, supported by both federal and provincial initiatives. Mexico, although smaller in solar adoption, is emerging as a major player due to its increasing investments in renewable energy projects.

- The U.S. federal government continues to support solar energy adoption through the Investment Tax Credit (ITC), which provides a 30% deduction for solar system costs. This policy, extended through the Inflation Reduction Act of 2022, has resulted in solar adoption across the U.S. with more than 1.4 million new residential solar installations in 2023 alone. The ITC applies to both residential and commercial sectors, and its impact has been pivotal in making solar energy more accessible.

North America Solar Panel Market Segmentation

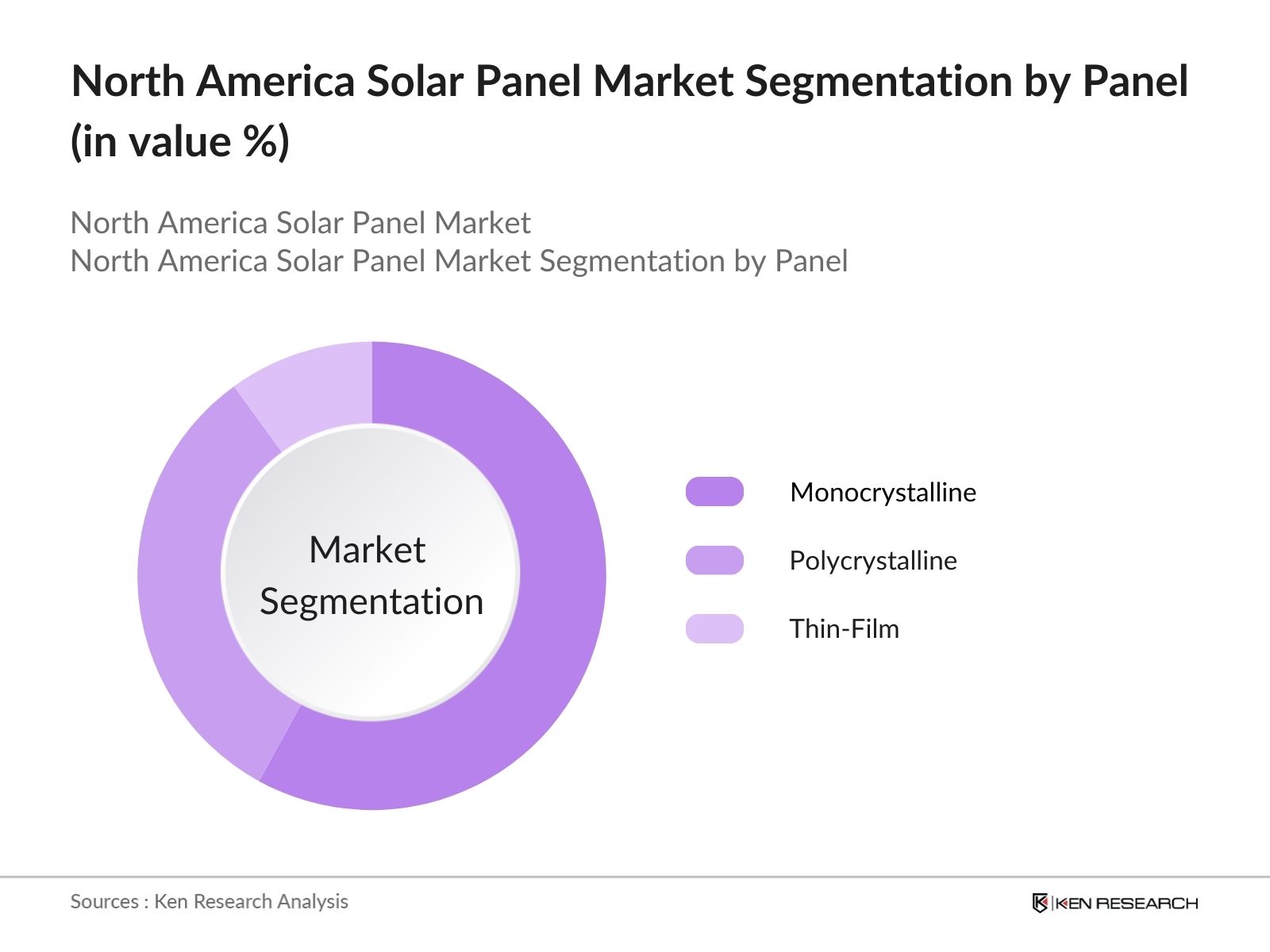

- By Panel Type: The market is segmented by panel type into monocrystalline, polycrystalline, and thin-film. Monocrystalline panels have a dominant market share due to their higher efficiency and longer lifespan, making them more suitable for high-efficiency solar power generation. These panels are particularly favoured in residential and commercial projects where space constraints necessitate maximum energy output from limited installation areas. Additionally, advancements in monocrystalline technology have further increased their appeal among large-scale solar farm developers.

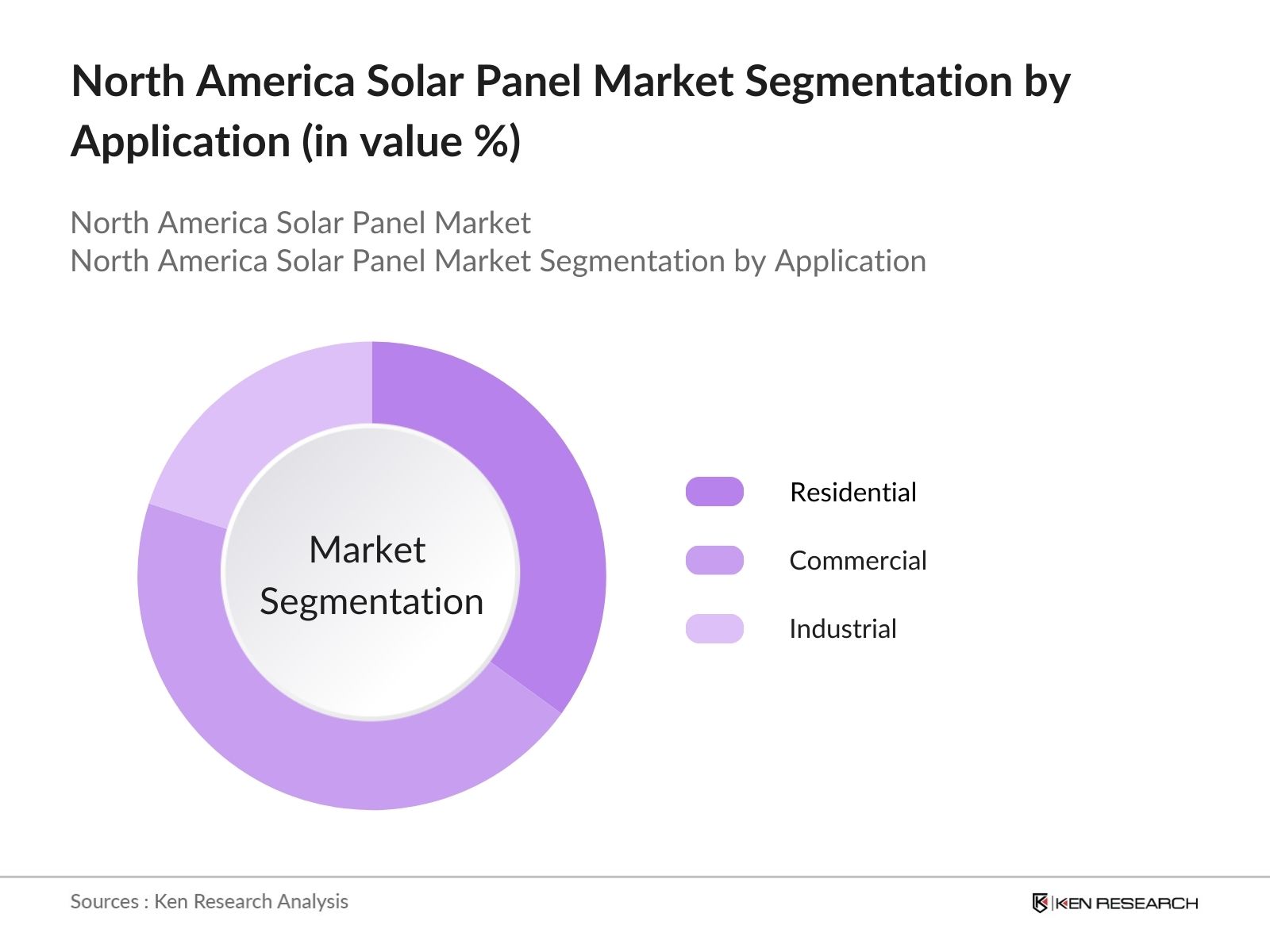

- By Application: The market is also segmented by application into residential, commercial, and industrial. Commercial installations lead the market due to increasing investments in solar infrastructure by businesses seeking to reduce energy costs and improve sustainability. Large corporations are integrating solar panels to offset operational energy consumption and meet sustainability goals, contributing to the dominance of this segment. Additionally, commercial projects often benefit from government incentives, further driving their adoption.

North America Solar Panel Market Competitive Landscape

The North America Solar Panel Market is dominated by several key players that have established themselves as leaders in the industry. The competitive landscape is characterized by companies offering high-efficiency panels, integrated solutions with energy storage, and a focus on sustainability. These players maintain market influence through strategic partnerships, technological innovations, and an extensive distribution network. The market features strong competition from both global manufacturers and local companies. The U.S. leads the region, with players such as Tesla and First Solar dominating the market. Companies like Canadian Solar have expanded their presence by leveraging their international expertise in solar manufacturing.

Company Name | Year Established | Headquarters | Installed Capacity (GW) | R&D Investments (USD mn) | Patents Held | Global Reach (No. of Countries) | Revenue (USD bn) | Strategic Partnerships |

First Solar, Inc. | 1999 | Arizona, USA | - | - | - | - | - | - |

SunPower Corporation | 1985 | California, USA | - | - | - | - | - | - |

Canadian Solar Inc. | 2001 | Ontario, Canada | - | - | - | - | - | - |

Tesla, Inc. (SolarCity) | 2006 | California, USA | - | - | - | - | - | - |

JinkoSolar Holding Co., Ltd. | 2006 | Shanghai, China | - | - | - | - | - | - |

North America Solar Panel Market Analysis

North America Solar Panel Market Growth Drivers

- Increasing Solar Energy Adoption: The adoption of solar energy in North America has surged substantially, with the United States alone generating over 146,000 GWh of solar electricity in 2023, according to the U.S. Energy Information Administration (EIA). This growing output is driven by environmental concerns, the need for clean energy, and national goals to reduce carbon emissions. Canada, for example, generated 7,000 GWh of solar power in 2022, focusing on transitioning towards renewable energy sources, as reported by Canada Energy Regulator. The rising use of solar power is propelled by government-backed programs promoting renewable energy sources.

- Declining Solar Panel Costs: The declining costs of solar panels have been a pivotal driver in market growth. From 2010 to 2023, the average price of solar photovoltaic modules decreased by more than 80%, as per the International Renewable Energy Agency (IRENA). This reduction in cost is attributed to advancements in technology and increased manufacturing efficiency, making solar energy more accessible. The average installed cost for solar systems in the U.S. was $1,500 per kW in 2023, while the global average reached an all-time low.

- Energy Storage Integration: The integration of energy storage with solar systems is growing rapidly, with the total installed capacity of battery storage in the U.S. reaching over 10 GW by mid-2023, according to the EIA. The rise of lithium-ion batteries has been crucial in pairing with solar panels for increased energy efficiency. This allows for better energy management, particularly in regions like California, where the state aims for 100% clean energy by 2045. Storage integration supports grid stability and allows users to store excess solar energy.

North America Solar Panel Market Challenges

- Supply Chain Disruptions: Supply chain disruptions, primarily caused by the COVID-19 pandemic and ongoing geopolitical tensions, have negatively impacted the availability of essential components like photovoltaic cells and inverters. According to the U.S. Department of Energy (DOE), solar projects faced delays of 6-12 months in 2023, largely due to disruptions in global trade and semiconductor shortages. The continued dependency on imports from Asia for critical raw materials, such as polysilicon, has exacerbated these delays, affecting installation timelines across North America.

- Regulatory Variations Across States: The disparity in solar policies between U.S. states creates a challenging regulatory environment for companies operating across multiple regions. For instance, while California mandates solar panels on all new homes as part of its 2020 Building Standards, states like Florida offer less aggressive policies. These differences can create hurdles for businesses and consumers who face inconsistent permitting processes and grid access fees. As of 2024, only 31 U.S. states have a mandatory Renewable Portfolio Standard (RPS), creating a fragmented market for solar energy adoption.

North America Solar Panel Market Future Outlook

Over the next five years, the North America Solar Panel Market is expected to exhibit growth driven by ongoing technological advancements, increasing government support, and growing demand for renewable energy sources. The expansion of utility-scale solar farms, coupled with the rising adoption of solar panels in residential and commercial spaces, will contribute to this growth. Moreover, the integration of energy storage systems, such as lithium-ion batteries, will further enhance the viability of solar energy in balancing grid demand.

North America Solar Panel Market Opportunities

- Expansion of Solar Farms: The expansion of large-scale solar farms presents opportunities for growth in the North America solar panel market. The U.S. currently has over 2,500 utility-scale solar projects generating around 60,000 MW of energy as of 2023, a number expected to increase as states and private companies invest in renewable energy to meet federal climate goals. Canadas growing interest in solar farms, particularly in Ontario, which accounts for more than 98% of the countrys solar power capacity, further demonstrates potential for large-scale solar investments.

- Integration of AI and IoT in Solar Panel Efficiency: AI and IoT technologies are increasingly being integrated into solar panel systems to optimize energy output and efficiency. Smart inverters and monitoring systems powered by AI have demonstrated a 10-15% increase in solar panel efficiency by 2023, as reported by the U.S. DOE. AI is also being used to predict weather patterns and optimize solar energy production, reducing energy losses and improving the return on investment for solar installations across residential, commercial, and industrial sectors.

Scope of the Report

By Panel Type | Monocrystalline Polycrystalline Thin-Film |

By Application | Residential Commercial Industrial |

By Grid Connectivity | On-Grid Off-Grid |

By Installation Type | Ground-Mounted Rooftop-Mounted |

By Region | USA Canada Mexico |

Products

Key Target Audience

Solar Panel Manufacturers

Solar Energy Developers

Solar Panel Distributors and Retailers

Utility Companies

Commercial and Industrial Solar Consumers

Government and Regulatory Bodies (U.S. Department of Energy, Natural Resources Canada)

Investor and Venture Capitalist Firms

Energy Storage and Grid Infrastructure Providers

Companies

Players Mentioned in the Report

First Solar, Inc.

SunPower Corporation

Canadian Solar Inc.

Tesla, Inc. (SolarCity)

JinkoSolar Holding Co., Ltd.

Hanwha Q CELLS

Trina Solar Limited

LG Electronics, Inc. (Solar Division)

Sharp Corporation (Sharp Solar)

Vivint Solar

Table of Contents

1. North America Solar Panel Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Solar Panel Market Size (In USD Billion)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Solar Panel Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Solar Energy Adoption

3.1.2. Government Incentives and Subsidies

3.1.3. Declining Solar Panel Costs

3.1.4. Energy Storage Integration (battery storage for solar systems)

3.2. Market Challenges

3.2.1. Supply Chain Disruptions

3.2.2. Regulatory Variations Across States

3.2.3. High Installation Costs for Residential Consumers

3.3. Opportunities

3.3.1. Expansion of Solar Farms

3.3.2. Integration of AI and IoT in Solar Panel Efficiency

3.3.3. Adoption of Thin-Film Solar Panels

3.4. Trends

3.4.1. Rise in Distributed Solar Power Generation

3.4.2. Increased Usage of Bifacial Solar Panels

3.4.3. Solar-Powered Electric Vehicle Charging Stations

3.5. Government Regulations

3.5.1. Federal Tax Incentives (Investment Tax Credit)

3.5.2. Renewable Portfolio Standards (RPS)

3.5.3. State-Level Solar Incentive Programs

3.6. SWOT Analysis

3.7. Stake Ecosystem (Manufacturers, Installers, Distributors, and End-users)

3.8. Porters Five Forces Analysis

3.9. Competitive Ecosystem

4. North America Solar Panel Market Segmentation

4.1. By Panel Type (In Value %)

4.1.1. Monocrystalline

4.1.2. Polycrystalline

4.1.3. Thin-Film

4.2. By Application (In Value %)

4.2.1. Residential

4.2.2. Commercial

4.2.3. Industrial

4.3. By Grid Connectivity (In Value %)

4.3.1. On-Grid

4.3.2. Off-Grid

4.4. By Installation Type (In Value %)

4.4.1. Ground-Mounted

4.4.2. Rooftop-Mounted

4.5. By Region (In Value %)

4.5.1. USA

4.5.2. Canada

4.5.3. Mexico

5. North America Solar Panel Market Competitive Analysis

5.1. Detailed Profiles of Major Competitors

5.1.1. First Solar, Inc.

5.1.2. SunPower Corporation

5.1.3. Canadian Solar Inc.

5.1.4. Tesla, Inc. (SolarCity)

5.1.5. Hanwha Q CELLS

5.1.6. Trina Solar Limited

5.1.7. JinkoSolar Holding Co., Ltd.

5.1.8. Sunrun Inc.

5.1.9. Vivint Solar

5.1.10. LG Electronics, Inc. (Solar Division)

5.1.11. Yingli Green Energy Holding Company Limited

5.1.12. Sharp Corporation (Sharp Solar)

5.1.13. JA Solar Technology Co., Ltd.

5.1.14. REC Group

5.1.15. Panasonic Corporation (Panasonic Solar)

5.2. Cross Comparison Parameters (Revenue, Solar Capacity Installed, Technology Focus, No. of Patents, Production Capacity, Global Reach, Sustainability Initiatives, Market Share)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, Collaborations, Product Innovations)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants and Subsidies

5.9. Private Equity Investments

6. North America Solar Panel Market Regulatory Framework

6.1. Solar Energy Standards and Certifications

6.2. Compliance Requirements for Installers

6.3. Permitting and Zoning Regulations

7. North America Solar Panel Future Market Size (In USD Billion)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Solar Panel Future Market Segmentation

8.1. By Panel Type (In Value %)

8.2. By Application (In Value %)

8.3. By Grid Connectivity (In Value %)

8.4. By Installation Type (In Value %)

8.5. By Region (In Value %)

9. North America Solar Panel Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives and Go-to-Market Strategies

9.4. White Space Opportunity Analysis

Research Methodology

Step 2: Market Analysis and Construction

In this step, historical data was compiled to analyze market penetration, solar capacity installed, and revenue generation by the North American solar industry. This analysis considered the balance between the number of manufacturers, project developers, and service providers to estimate market size and growth.

Step 3: Hypothesis Validation and Expert Consultation

The data collected was validated through consultations with industry experts via phone interviews. Insights from these interviews were used to verify operational challenges, financial strategies, and technological advancements. This expert consultation played a vital role in refining the market projections.

Step 4: Research Synthesis and Final Output

The final research step involved synthesizing information from multiple sources, including manufacturers and industry experts, to provide a complete picture of the North American solar market. This stage also ensured that data accuracy was verified through a combination of top-down and bottom-up approaches.

Frequently Asked Questions

01. How big is the North America Solar Panel Market?

The North America Solar Panel Market is valued at USD 350 billion. This growth is driven by increasing demand for renewable energy, government incentives, and advancements in solar technology.

02. What are the challenges in the North America Solar Panel Market?

Challenges in the North America Solar Panel Market include regulatory differences across states, high installation costs for residential consumers, and the ongoing supply chain disruptions affecting key solar components.

03. Who are the major players in the North America Solar Panel Market?

Key players in the North America Solar Panel Market include First Solar, Inc., SunPower Corporation, Canadian Solar Inc., Tesla, Inc. (SolarCity), and JinkoSolar Holding Co., Ltd. These companies lead the market through innovation, production capacity, and sustainability initiatives.

04. What are the growth drivers of the North America Solar Panel Market?

The North America Solar Panel Market is driven by declining solar panel costs, increasing adoption of solar energy by residential and commercial consumers, and supportive government policies such as tax incentives and renewable portfolio standards.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.