North America Telephone Company Market Outlook to 2030

Region:Global

Author(s):Sanjna

Product Code:KROD10258

November 2024

93

About the Report

North America Telephone Company Market Overview

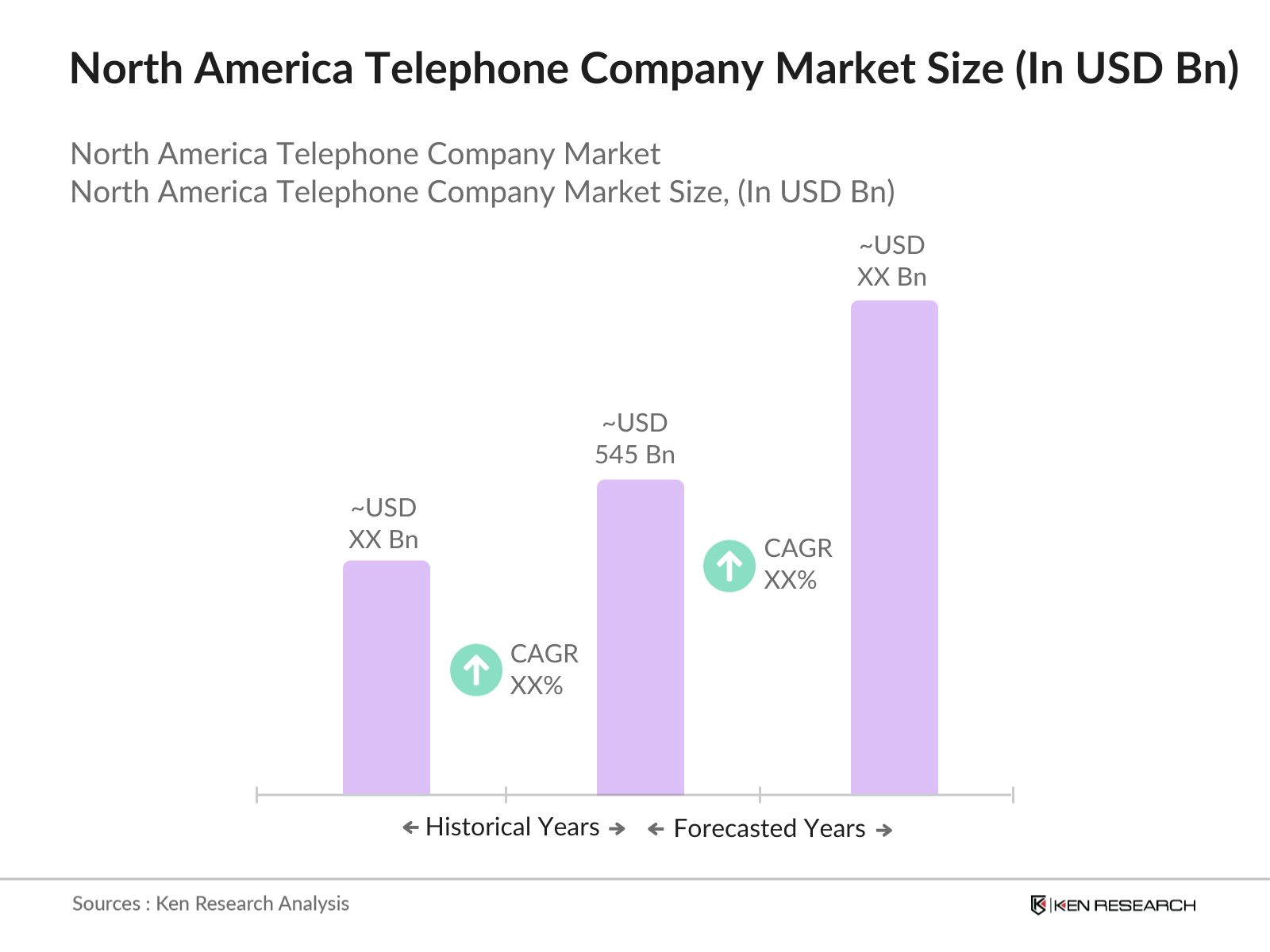

- The North America Telephone Company market is valued at USD 545 billion, primarily driven by continuous investment in network infrastructure, the increasing adoption of 5G technology, and a growing demand for mobile data services. Large telecommunication providers are expanding fiber optic networks to meet the rising data consumption needs, driven by remote work, online streaming, and smart devices.

- The market is dominated by key regions such as the United States and Canada. The dominance of the United States is due to its well-established telecommunication infrastructure, ongoing technological advancements, and a large population with high internet penetration. Major cities like New York, Los Angeles, and Chicago lead in data consumption and are home to headquarters of significant telecommunication companies. Canada is also contributing due to its strong network of rural and urban connectivity and the government's push for rural digitalization projects.

- Spectrum allocation remains a critical regulatory focus in North America. In 2024, the U.S. government auctioned additional spectrum licenses to support the rollout of 5G services, generating over $23 billion in revenue. These auctions are essential for telecom companies to acquire the necessary bandwidth to expand their networks. Canada also conducted spectrum auctions, raising USD 7.2 billion for 5G development. These efforts ensure that telecom providers have access to sufficient spectrum to meet the growing demand for high-speed mobile data services.

North America Telephone Company Market Segmentation

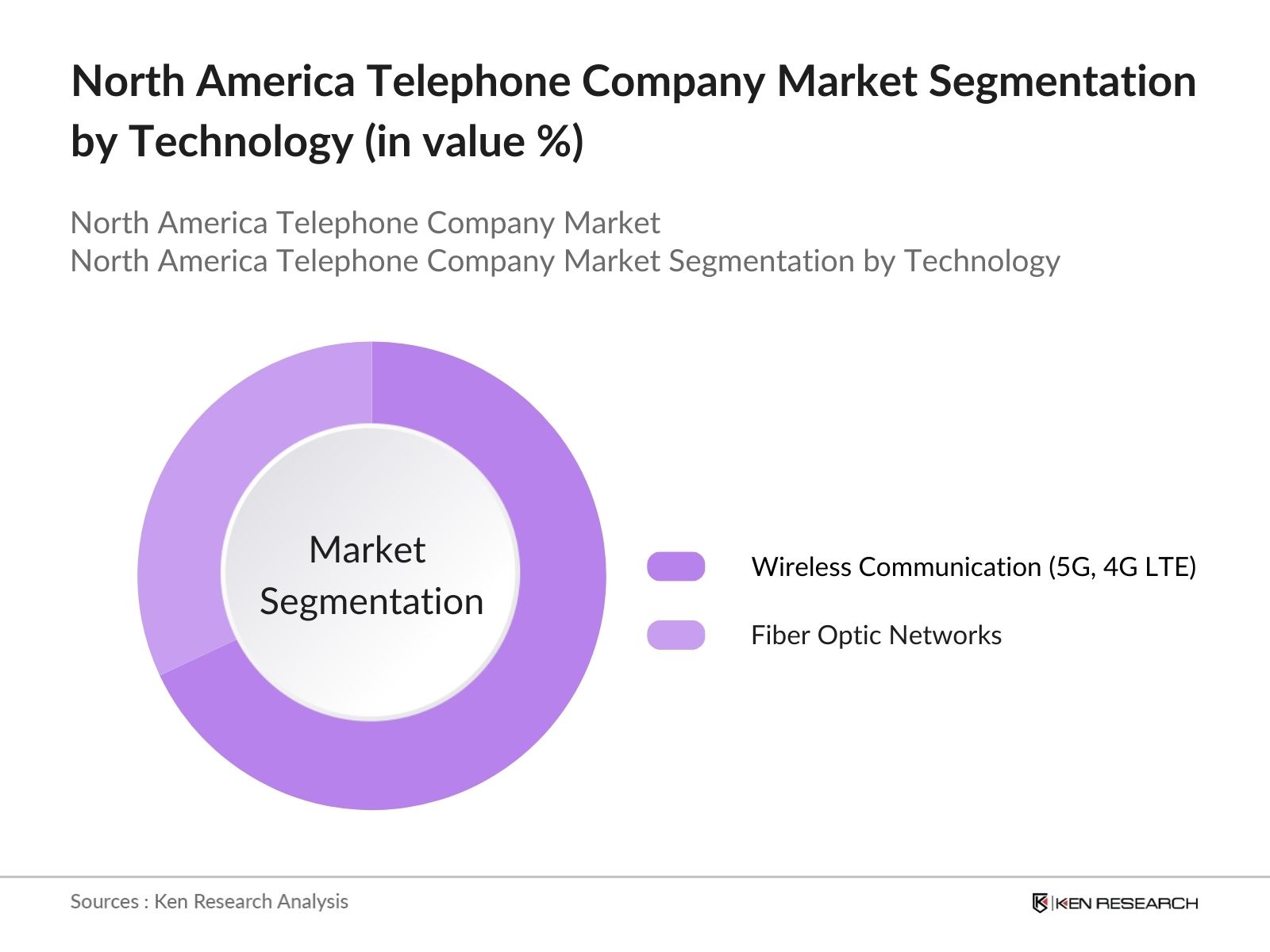

By Technology: The North America Telephone Company market is segmented by technology into Wireless Communication (5G, 4G LTE) and Fiber Optic Networks. Recently, Wireless Communication (5G, 4G LTE) has captured a dominant market share, driven by the surge in mobile data usage, the proliferation of smart devices, and increasing investments in the 5G rollout. Consumers demand faster and more reliable mobile internet, prompting telecommunication providers to prioritize wireless infrastructure.

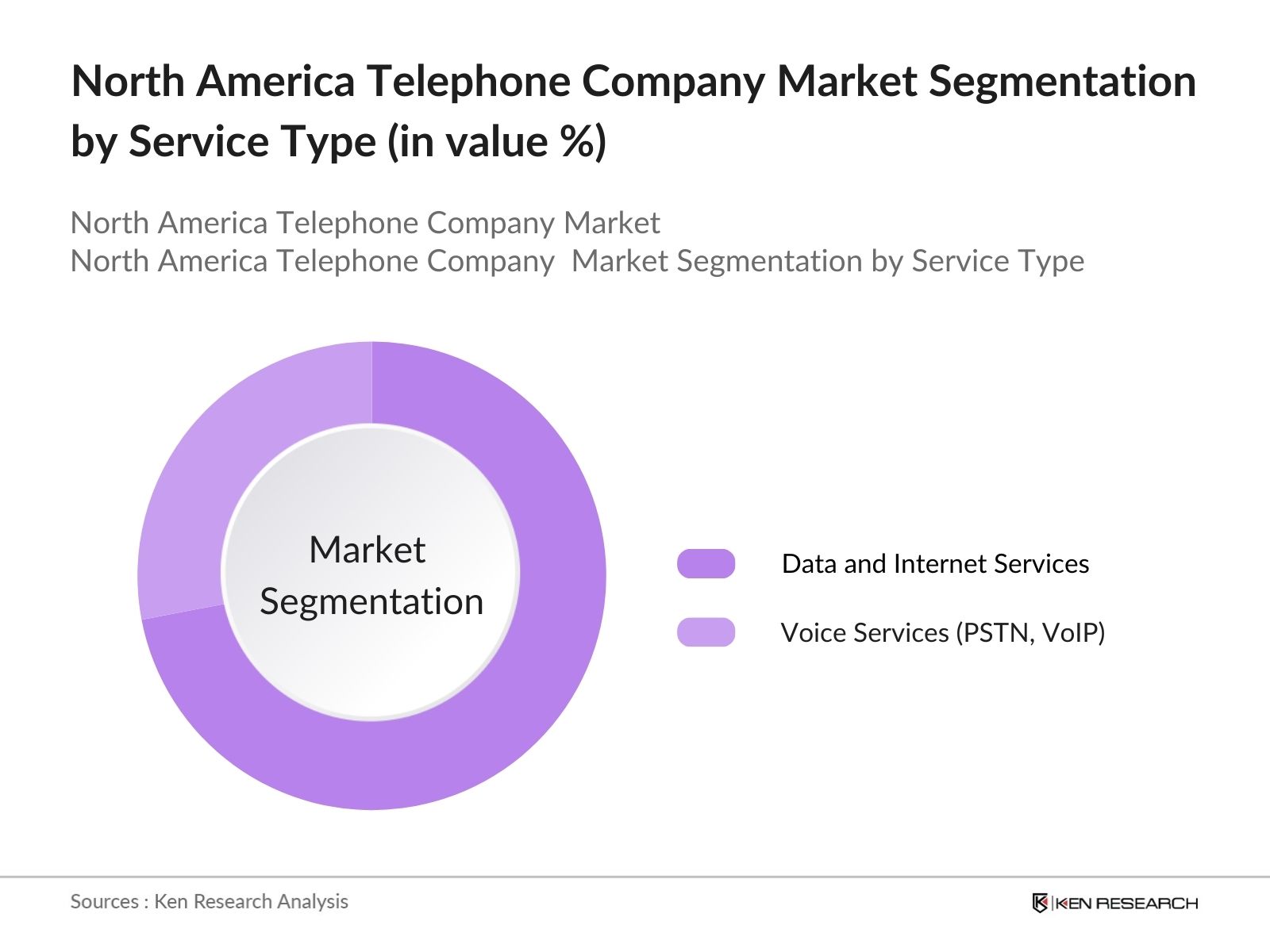

By Service Type: The North America Telephone Company market is further segmented by service type into Voice Services (PSTN, VoIP) and Data and Internet Services. The Data and Internet Services sub-segment currently holds the dominant market share due to the exponential growth in data consumption, the popularity of streaming services, and the rise in cloud-based solutions. Consumers and businesses are increasingly relying on high-speed internet for essential activities such as video conferencing, streaming, and cloud computing, making data services critical for telecom operators.

By Service Type: The North America Telephone Company market is further segmented by service type into Voice Services (PSTN, VoIP) and Data and Internet Services. The Data and Internet Services sub-segment currently holds the dominant market share due to the exponential growth in data consumption, the popularity of streaming services, and the rise in cloud-based solutions. Consumers and businesses are increasingly relying on high-speed internet for essential activities such as video conferencing, streaming, and cloud computing, making data services critical for telecom operators.

North America Telephone Company Market Competitive Landscape

The North America Telephone Company market is characterized by the presence of a few dominant players. These companies control significant portions of the market through their extensive infrastructure, innovative service offerings, and strategic partnerships. The market is led by both domestic giants and global players, which underscores the consolidated nature of this industry. These companies continually invest in upgrading their technology and expanding their coverage to maintain competitive advantages.

North America Telephone Company Market Analysis

Growth Drivers

- Network Infrastructure Investments: The North American telecommunications sector is witnessing significant investments in network infrastructure to support advanced technologies like 5G and fiber optics. In 2024, U.S. network providers committed over $40 billion in capital expenditures to enhance and expand their networks. Fiber optic deployments reached 80 million miles in the U.S., according to the Federal Communications Commission (FCC), to improve broadband connectivity, particularly in underserved regions. These investments are key to driving network reliability and increasing capacity for next-gen services.

- Increasing Demand for Mobile Data: Mobile data consumption is surging in North America, driven by the rise in smart devices and the ongoing shift toward digital services. In 2024, mobile data traffic in the U.S. is projected to reach 82 exabytes per month, according to the International Telecommunication Union (ITU). This trend is further fueled by the increase in video streaming, online gaming, and cloud services. Canada also reports substantial growth, with mobile data traffic expected to hit 18 exabytes by year-end. These figures underline the urgent need for expanded network capabilities to support rising demand.

- Adoption of 5G and Fiber Optic Technology: The adoption of 5G and fiber optic technology is a critical driver of market expansion in North America. As of 2024, over 65% of the U.S. population has access to 5G networks, with over 200,000 5G towers deployed nationwide. In Canada, the governments Universal Broadband Fund has allocated CAD 2.75 billion to support the rollout of 5G and fiber broadband services. These technologies are key to improving mobile data speeds, reducing latency, and supporting the growth of IoT and cloud-based services.

Challenges

- Price Wars among Major Players: Price competition among major telecom providers in North America has intensified in 2024, leading to a decrease in service profitability. For instance, Verizon and AT&T have been forced to reduce prices on several data plans in response to aggressive pricing from competitors like T-Mobile. In Canada, pricing pressures have prompted regional telecom companies to lower costs for both broadband and mobile services. This price war has resulted in diminished revenues for some providers, creating a challenging financial landscape despite growing service demand.

- Complex Regulatory Environment: Telecom companies face significant regulatory challenges in North America, with stringent rules imposed by authorities like the FCC in the U.S. and the Canadian Radio-television and Telecommunications Commission (CRTC). The introduction of net neutrality regulations and stringent privacy laws in 2024 requires companies to comply with new data protection standards. Additionally, spectrum licensing fees continue to rise, with recent U.S. spectrum auctions generating over $81 billion. This complex regulatory landscape adds operational costs and limits the flexibility of service providers.

North America Telephone Company Market Future Outlook

North America Telephone Company market is expected to witness steady growth, driven by ongoing investments in 5G technology, fiber optic networks, and the expanding role of IoT and cloud-based services. Telecom providers are expected to enhance their infrastructure to support increased mobile and data traffic, particularly in urban and rural areas. Furthermore, government initiatives promoting rural connectivity and network expansions will likely boost market opportunities.

Market Opportunities

- Expansion of Cloud-based Communication Services: The demand for cloud-based communication services continues to rise, providing telecom companies with lucrative opportunities. In 2024, North American enterprises spent over $120 billion on cloud services, including voice over IP (VoIP) and unified communication services. Telecom providers are increasingly integrating cloud platforms to offer scalable, flexible communication solutions that cater to remote and hybrid work environments. This shift is transforming traditional telecom services and opening new revenue streams.

- Opportunities in Rural and Underdeveloped Areas: With government initiatives to bridge the digital divide, telecom providers have significant opportunities in rural and underserved areas across North America. In 2024, U.S. telecom companies received over $8 billion in federal funding to improve broadband services in rural regions. Canada has similarly allocated USD 1.29 billion to connect rural and northern communities. These investments provide telecom companies with the chance to expand their networks and customer bases in areas that were previously under-served.

Scope of the Report

|

Segment |

Sub-Segment |

|

Technology |

Wireless Communication (5G, 4G LTE) |

|

Fiber Optic Networks |

|

|

Traditional Wireline (PSTN, ISDN) |

|

|

Application |

Residential |

|

Commercial |

|

|

Industrial |

|

|

Service Type |

Voice Services (PSTN, VoIP) |

|

Data and Internet Services |

|

|

Cloud and Hosting Services |

|

|

End-User |

Enterprises |

|

Small and Medium Businesses (SMBs) |

|

|

Consumers |

|

|

Region |

United States |

|

Canada |

|

|

Mexico |

Products

Key Target Audience

Telecom Service Providers

Network Infrastructure Companies

Data and Internet Service Providers

Mobile Device Manufacturers

IoT Solution Providers

Rural Connectivity Solution Providers

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (FCC, Industry Canada)

Companies

Players Mentioned in the Report

AT&T Inc.

Verizon Communications Inc.

T-Mobile US, Inc.

Rogers Communications

Bell Canada Enterprises (BCE)

CenturyLink (Lumen Technologies)

Frontier Communications

Windstream Communications

Comcast Corporation

Telus Corporation

Table of Contents

1. North America Telephone Company Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. North America Telephone Company Market Size (In USD Mn)

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. North America Telephone Company Market Analysis

3.1 Growth Drivers (Market Expansion, Network Infrastructure, 5G Adoption)

3.1.1 Network Infrastructure Investments

3.1.2 Increasing Demand for Mobile Data

3.1.3 Adoption of 5G and Fiber Optic Technology

3.1.4 Regulatory Push for Rural Connectivity

3.2 Market Challenges (Pricing Pressures, Regulatory Constraints, Operational Costs)

3.2.1 Price Wars among Major Players

3.2.2 Complex Regulatory Environment

3.2.3 High Operational and Maintenance Costs

3.3 Opportunities (Digital Transformation, IoT, Cloud Services Integration)

3.3.1 Growth in IoT Connectivity Solutions

3.3.2 Expansion of Cloud-based Communication Services

3.3.3 Opportunities in Rural and Underdeveloped Areas

3.4 Trends (VoIP Adoption, Hybrid Workforce Solutions, AI Integration)

3.4.1 Rise in VoIP Solutions and Unified Communication

3.4.2 AI and Machine Learning in Customer Support

3.4.3 Increasing Demand for Hybrid Workforce Communication Solutions

3.5 Government Regulations (FCC Guidelines, Spectrum Allocation, Privacy Laws)

3.5.1 FCC Regulations on Network Neutrality

3.5.2 Spectrum Auctions and Allocation

3.5.3 Data Privacy and Cybersecurity Mandates

3.6 SWOT Analysis

3.7 Stake Ecosystem

3.8 Porters Five Forces

3.9 Competition Ecosystem

4. North America Telephone Company Market Segmentation

4.1 By Technology (In Value %)

4.1.1 Wireless Communication (5G, 4G LTE)

4.1.2 Fiber Optic Networks

4.1.3 Traditional Wireline (PSTN, ISDN)

4.2 By Application (In Value %)

4.2.1 Residential

4.2.2 Commercial

4.2.3 Industrial

4.3 By Service Type (In Value %)

4.3.1 Voice Services (PSTN, VoIP)

4.3.2 Data and Internet Services

4.3.3 Cloud and Hosting Services

4.4 By End-User (In Value %)

4.4.1 Enterprises

4.4.2 Small and Medium Businesses (SMBs)

4.4.3 Consumers

4.5 By Region (In Value %)

4.5.1 United States

4.5.2 Canada

4.5.3 Mexico

5. North America Telephone Company Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 AT&T Inc.

5.1.2 Verizon Communications Inc.

5.1.3 T-Mobile US, Inc.

5.1.4 CenturyLink (Lumen Technologies)

5.1.5 Rogers Communications

5.1.6 Bell Canada Enterprises (BCE)

5.1.7 Telus Corporation

5.1.8 Frontier Communications

5.1.9 Windstream Communications

5.1.10 Comcast Corporation

5.2 Cross Comparison Parameters (Revenue, Network Coverage, Subscriber Base, ARPU, CapEx)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. North America Telephone Company Market Regulatory Framework

6.1 Spectrum Regulations

6.2 Telecommunications Act Compliance

6.3 Licensing and Spectrum Auctions

6.4 Privacy Regulations and Data Protection Laws

7. North America Telephone Company Future Market Size (In USD Mn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. North America Telephone Company Future Market Segmentation

8.1 By Technology (In Value %)

8.2 By Application (In Value %)

8.3 By Service Type (In Value %)

8.4 By End-User (In Value %)

8.5 By Region (In Value %)

9. North America Telephone Company Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

In this phase, a comprehensive map of all stakeholders in the North America Telephone Company market was constructed. This step involved in-depth desk research, relying on secondary sources such as industry reports, financial disclosures, and proprietary databases. The objective was to identify and define critical variables affecting market growth and competition.

Step 2: Market Analysis and Construction

We then analyzed historical market data, focusing on key metrics such as network expansion rates, service adoption levels, and mobile data consumption. The analysis included evaluating how these variables influenced market revenue and growth trends in key regions across North America.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were validated through direct consultations with industry experts via computer-assisted telephone interviews (CATIs). These experts, representing key companies and service providers, offered insights into current and future trends, helping refine the research findings.

Step 4: Research Synthesis and Final Output

In the final phase, all data was synthesized into a comprehensive analysis that was reviewed and cross-verified with multiple telecom providers. This final output ensures the reliability and accuracy of market projections, offering an in-depth view of the North America Telephone Company market.

Frequently Asked Questions

01. How big is the North America Telephone Company market?

The North America Telephone Company market is valued at USD 545 billion, driven by investments in 5G technology, fiber optic networks, and a growing demand for data services.

02. What are the challenges in the North America Telephone Company market?

Key challenges in North America Telephone Company market include pricing pressures due to intense competition, high operational and maintenance costs for network infrastructure, and navigating complex regulatory frameworks in the region.

03. Who are the major players in the North America Telephone Company market?

The major players in North America Telephone Company market include AT&T Inc., Verizon Communications Inc., T-Mobile US, Inc., Rogers Communications, and Bell Canada Enterprises (BCE), who dominate due to their infrastructure and expansive service offerings.

04. What are the growth drivers of the North America Telephone Company market?

Growth drivers in North America Telephone Company market include the increasing demand for mobile data, the rapid adoption of 5G technology, and government initiatives aimed at expanding rural connectivity in North America.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.