North America Tractor Market Outlook to 2030

Region:North America

Author(s):Yogita Sahu

Product Code:KROD2559

Region:North America

Author(s):Yogita Sahu

Product Code:KROD2559

October 2024

81

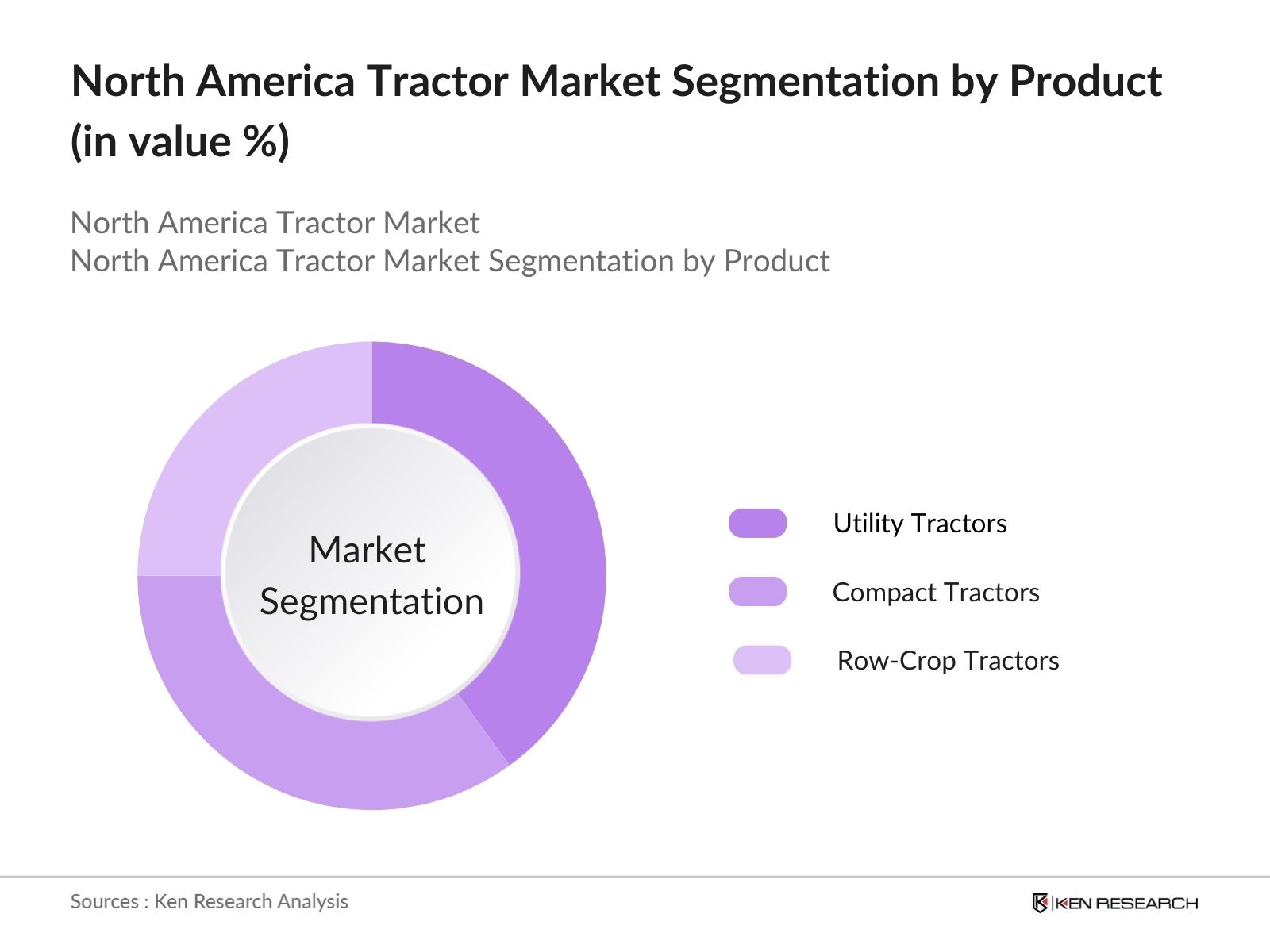

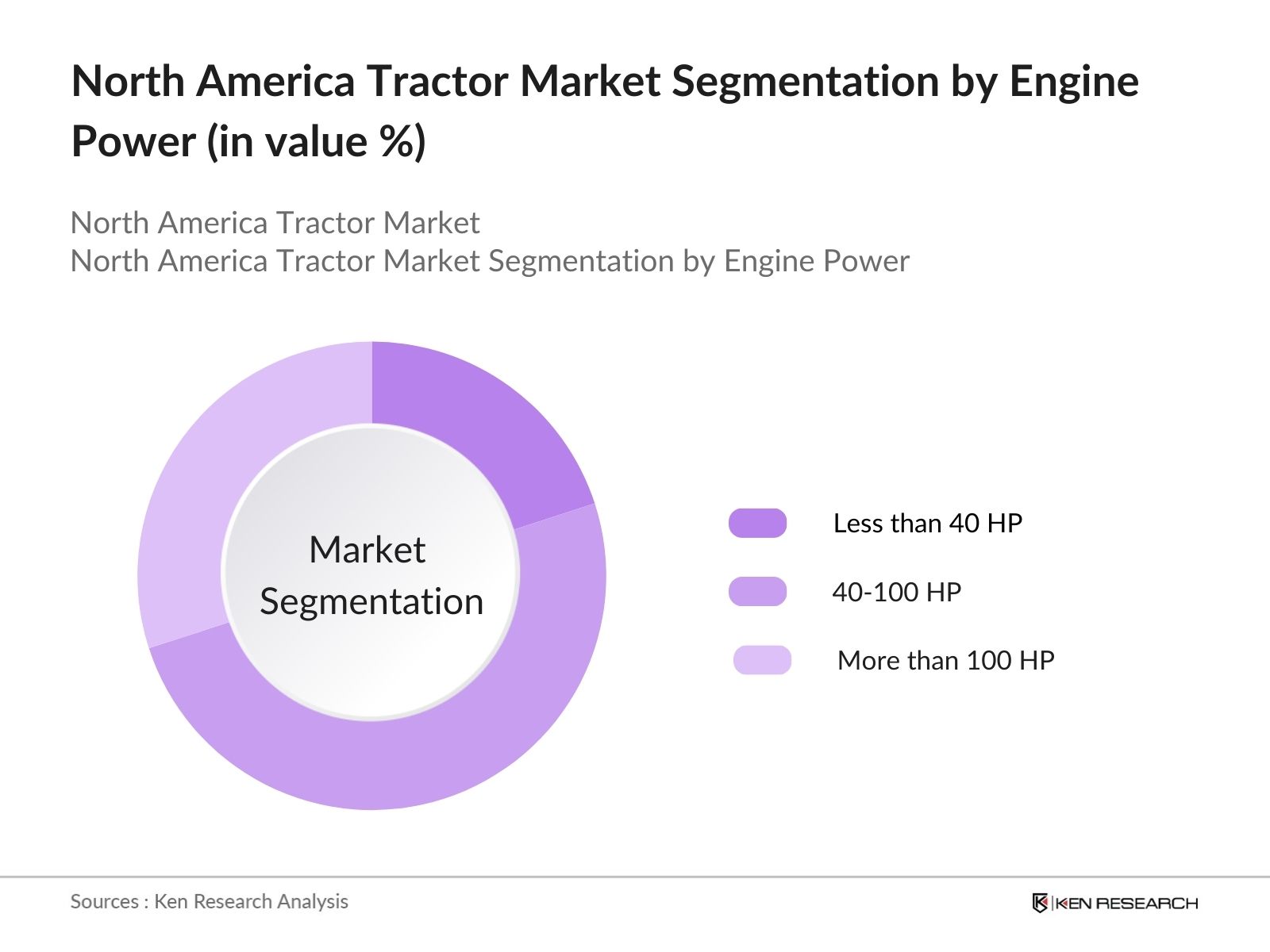

The market is segmented into various factors like product, engine power, and region.

By Product: The market is segmented by product into compact tractors, utility tractors, and row-crop tractors. Utility tractors dominated the market, by their versatility across a range of agricultural applications and affordability for small to mid-sized farms have contributed to their widespread adoption.

By Engine Power: The market is segmented by engine power into less than 40 HP, 40-100 HP, and more than 100 HP tractors. Tractors with 40-100 HP held a dominant market share as they offered the best balance between power and affordability, catering to both small and large-scale farms.

By Region: The market is segmented by region into the United States and Canada. The United States dominated the market with its large-scale agriculture, higher adoption of advanced technologies, and government support for precision farming.

|

Company Name |

Establishment Year |

Headquarters |

|

John Deere |

1837 |

Moline, Illinois |

|

CNH Industrial |

2013 |

London, UK |

|

AGCO Corporation |

1990 |

Duluth, Georgia |

|

Kubota Corporation |

1890 |

Osaka, Japan |

|

Mahindra & Mahindra |

1945 |

Mumbai, India |

Future trends include a surge in electric tractor adoption, increased integration of AI and IoT in tractors, a rise in demand for high-horsepower autonomous tractors, and stricter sustainability regulations shaping the market.

|

By Product |

Utility Tractors Compact Tractors Row-Crop Tractors |

|

By Engine Power |

Less than 40 HP 40-100 HP More than 100 HP |

|

By Region |

USA Canda |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics (Growth Drivers, Restraints, Opportunities)

1.4. Value Chain Analysis

2.1. Historical Market Size (Operational, Financial Data)

2.2. Year-on-Year Growth Analysis (Units Sold, Revenue Generated)

2.3. Key Market Milestones and Developments

3.1. Growth Drivers

3.1.1. Increased Demand for Autonomous Tractors

3.1.2. Government Initiatives Supporting Mechanization

3.1.3. Expansion of Large-Scale Farming

3.1.4. Electric and Low-Emission Tractor Adoption

3.2. Restraints

3.2.1. High Initial Investment in Smart Tractors

3.2.2. Shortage of Skilled Labor

3.2.3. Maintenance Challenges for Advanced Machinery

3.2.4. Regulatory Pressures on Emissions

3.3. Opportunities

3.3.1. Technological Innovation in Tractor Automation

3.3.2. Expansion into Precision Agriculture

3.3.3. Partnerships for Smart Farming Solutions

3.3.4. Sustainable Agriculture Practices

3.4. Market Trends

3.4.1. Integration of AI and IoT in Tractors

3.4.2. Transition Towards Electric Tractors

3.4.3. Increased Adoption of High-Horsepower Models

3.4.4. Expansion of Leasing Programs for Small Farms

3.5. Government Regulations

3.5.1. Emission Standards for Agricultural Machinery

3.5.2. Subsidies for Electric Tractors

3.5.3. Precision Agriculture Funding Programs

3.5.4. Import Regulations on Tractor Components

3.6. SWOT Analysis

3.7. Ecosystem Stakeholders (Suppliers, Distributors, Farmers)

3.8. Competitive Ecosystem Analysis

4.1. By Product Type (in value %)

4.1.1. Utility Tractors

4.1.2. Row-Crop Tractors

4.1.3. Compact Tractors

4.2. By Engine Power (in value %)

4.2.1. Less than 40 HP

4.2.2. 40-100 HP

4.2.3. More than 100 HP

4.3. By Region (in value %)

4.3.1. United States

4.3.2. Canada

5.1. Market Share Analysis (Financial and Operational)

5.2. Detailed Profiles of Major Players

5.2.1. John Deere

5.2.2. CNH Industrial

5.2.3. AGCO Corporation

5.2.4. Kubota Corporation

5.2.5. Mahindra & Mahindra

5.2.6. Fendt

5.2.7. Massey Ferguson

5.2.8. Case IH

5.2.9. Valtra

5.2.10. Versatile

5.2.11. Yanmar

5.2.12. New Holland

5.2.13. TYM Tractors

5.2.14. LS Tractor

5.2.15. Claas

5.3. Cross Comparison (Inception Year, Revenue, Employees, Key Strategies)

5.4. Mergers and Acquisitions

5.5. Strategic Partnerships and Collaborations

5.6. New Product Launches and Innovations

6.1. Emission Standards

6.2. Safety and Compliance Regulations

6.3. Import and Export Laws

6.4. Certification Requirements for Smart and Electric Tractors

7.1. Projections for the Next Five Years (Operational, Financial Data)

7.2. Key Drivers of Future Market Growth

7.3. Technological Disruptions and Future Trends

7.4. Sustainability and Environmental Impact Considerations

8.1. Market Entry Strategies for New Players

8.2. Expansion Opportunities for Existing Players

8.3. Product Differentiation Strategies

8.4. Recommendations for Technological Adoption and Investment

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Collating statistics on this industry over the years, penetration of marketplaces and service providers ratio to compute revenue generated for North America Tractor industry. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Building market hypothesis and conducting CATIs with industry experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Our team will approach multiple tractor manufacturers companies and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from such tractor manufacturers companies.

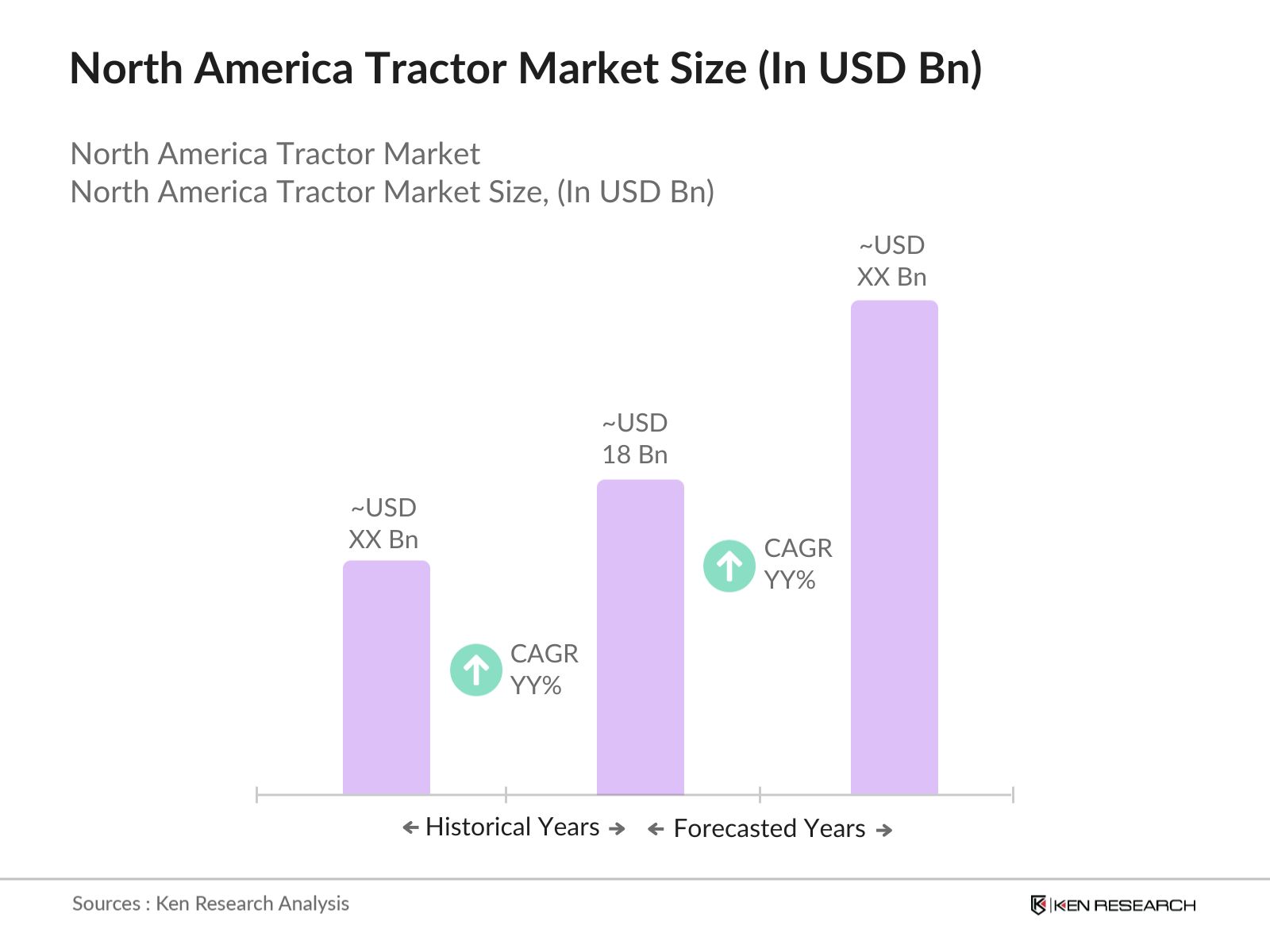

The North America Tractor Market was valued at USD 18 billion is driven by increased demand for agricultural mechanization, advances in tractor technology, and government initiatives supporting farmers.

Challenges in the North America Tractor market include the high cost of advanced tractors, lack of skilled workers, regulatory pressures on emissions, and slow technology adoption among smaller farms.

Key players in the North America Tractor market include John Deere, CNH Industrial, AGCO Corporation, Kubota Corporation, and Mahindra & Mahindra.

The growth of the North America Tractor market is driven by the adoption of autonomous tractors, government support for precision farming, rising demand for high-horsepower tractors, and the shift toward electric tractors for sustainability.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.