North America Traffic Management Market Outlook to 2030

Region:North America

Author(s):Naman Rohilla

Product Code:KROD2532

December 2024

90

About the Report

North America Traffic Management Market Overview

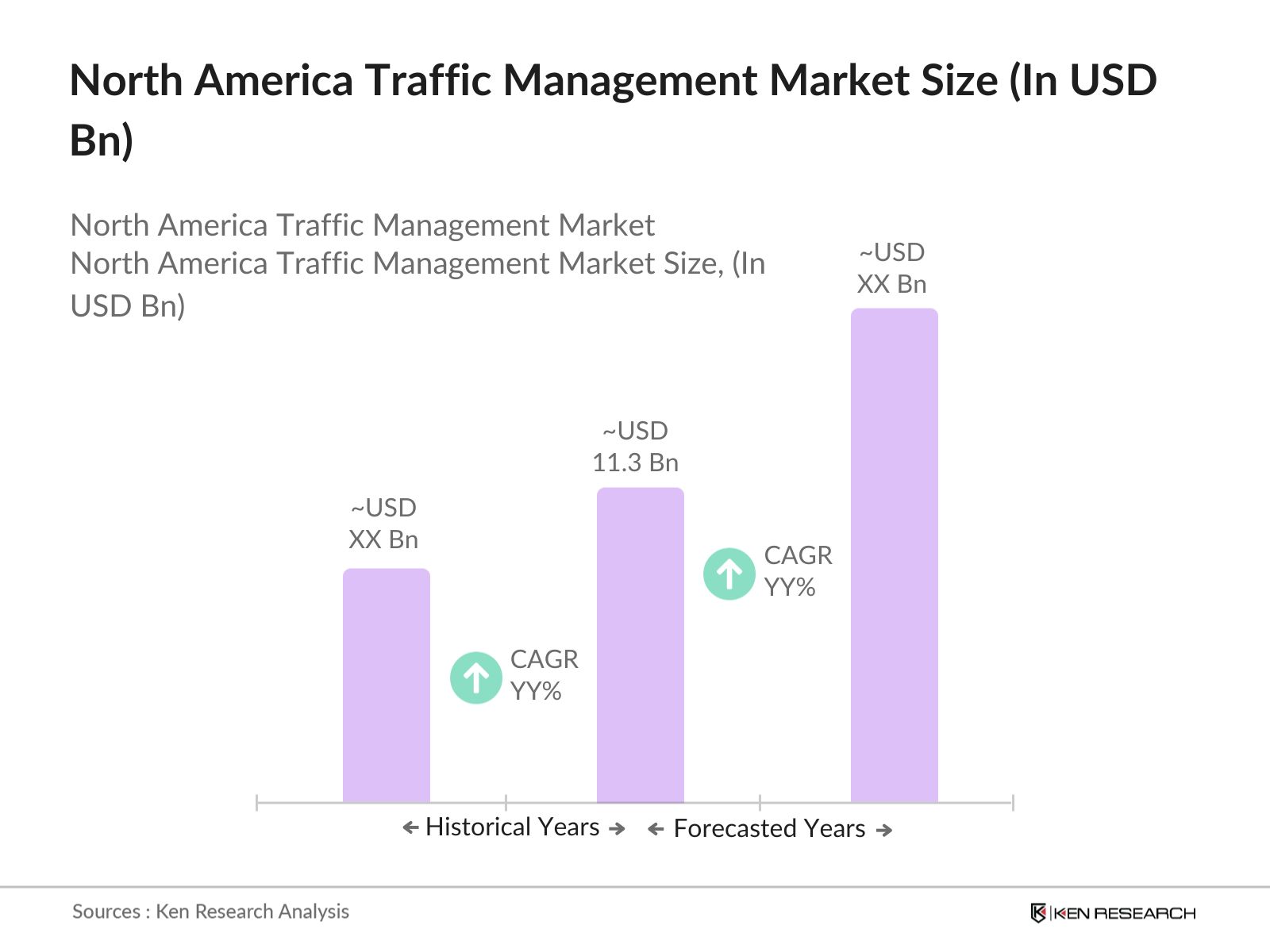

- The North America Traffic Management Market is valued at USD 11.3 billion, based on a five-year historical analysis. This substantial valuation is driven by rapid urbanization, increasing vehicle ownership, and significant investments in smart city initiatives. The integration of advanced technologies such as IoT and AI into traffic systems has further propelled market growth, enhancing traffic flow efficiency and safety measures.

- Within North America, the United States stands as the dominant contributor to the traffic management market. This dominance is attributed to the country's extensive urban infrastructure, high vehicle density, and proactive government policies promoting intelligent transportation systems. Additionally, substantial federal funding and public-private partnerships have facilitated the deployment of advanced traffic management solutions across major U.S. cities.

- In 2024, the U.S. enacted the Transportation Equity Act, providing $70 billion to improve infrastructure, with a portion dedicated to traffic management improvements. State-level initiatives in California and Texas include strict policies on traffic system modernization, requiring updated standards to improve safety and flow. Similarly, Canadian provinces like Ontario are implementing stringent policies for traffic infrastructure compliance, setting benchmarks for technology adoption in urban centers.

North America Traffic Management Market Segmentation

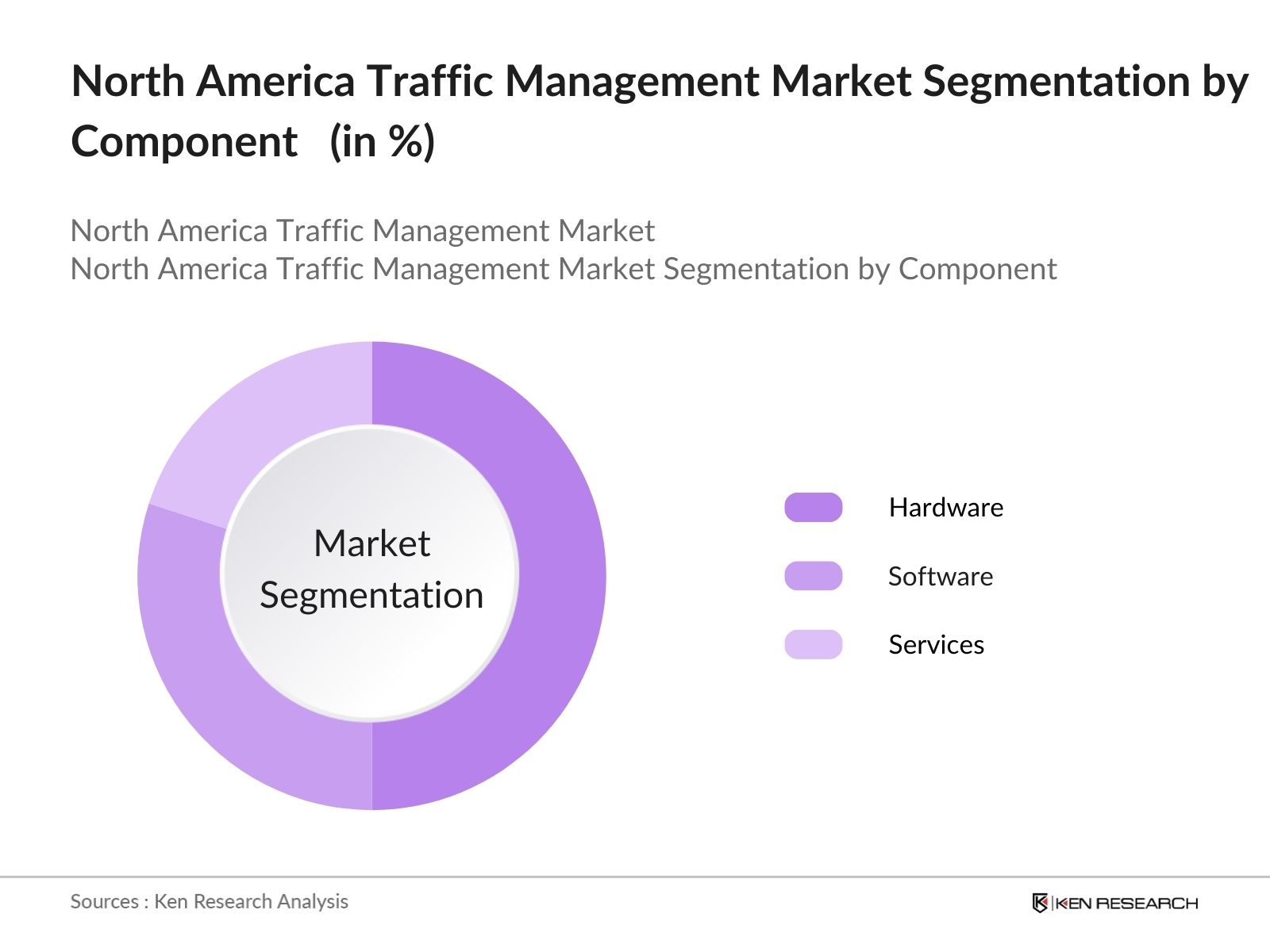

By Component: The market is segmented by component into hardware, software, and services. Among these, hardware components hold a dominant market share. This is due to the widespread deployment of surveillance cameras, sensors, and display boards essential for real-time traffic monitoring and control. The increasing adoption of these devices across urban centers underscores their critical role in enhancing traffic management efficiency.

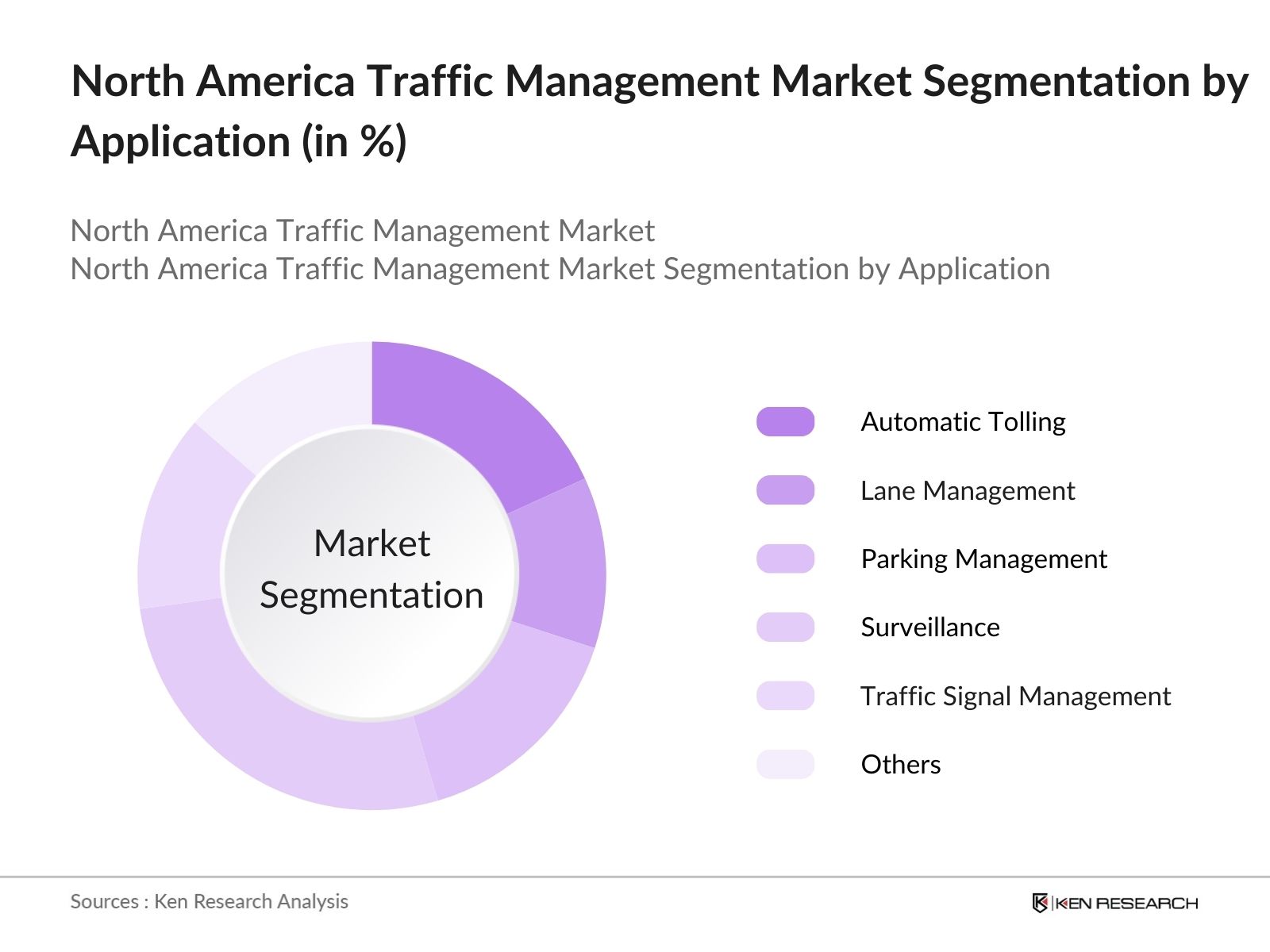

By Application: The market is further segmented by application into automatic tolling, lane management, parking management, surveillance, traffic signal management, and others. Surveillance applications dominate the market share, driven by the need for real-time monitoring to ensure road safety and compliance with traffic regulations. The integration of advanced surveillance systems enables authorities to effectively manage traffic flow and respond promptly to incidents.

North America Traffic Management Market Competitive Landscape

The North America Traffic Management Market is characterized by the presence of several key players who contribute significantly to market dynamics. These companies leverage technological advancements and strategic partnerships to maintain a competitive edge.

|

Company Name |

Establishment Year |

Headquarters |

Number of Employees |

Revenue (USD Billion) |

Product Portfolio |

Recent Developments |

Market Share (%) |

|

Cisco Systems, Inc. |

1984 |

San Jose, CA, USA |

|||||

|

Siemens AG |

1847 |

Munich, Germany |

|||||

|

IBM Corporation |

1911 |

Armonk, NY, USA |

|||||

|

Kapsch TrafficCom AG |

1892 |

Vienna, Austria |

|||||

|

Cubic Corporation |

1951 |

San Diego, CA, USA |

North America Traffic Management Market Analysis

Market Growth Drivers

- Urbanization and Population Growth: North America is experiencing rapid urbanization, with over 82% of the population now residing in urban areas as of 2023, according to the United Nations. The U.S. population grew to approximately 334 million in 2024, with more than 70 million people residing in the top 10 largest metropolitan areas, intensifying the need for improved traffic management. Canadas urban population also surpassed 80% in 2023, particularly concentrated in cities like Toronto, Vancouver, and Montreal. This increase in population density directly escalates traffic congestion, making efficient traffic management systems essential for urban centers.

- Technological Advancements in Traffic Management Systems: Technological innovations, especially in AI and IoT, are enhancing traffic management capabilities. In 2024, the North American region saw over 1,500 cities implementing AI-based traffic monitoring systems, supported by real-time data collected from over 3 million IoT-enabled devices installed on roadways and intersections. These technologies reduce congestion times by up to 20% in cities like Los Angeles and Toronto, improving commuter efficiency significantly. Such advancements underscore the critical role of technology in transforming traffic management across urban areas.

- Increasing Vehicle Ownership: Vehicle ownership in North America remains high, with the United States reporting approximately 276 million registered vehicles in 2023, an increase from previous years as personal mobility gains importance. Canada also saw vehicle ownership rise, reaching over 26 million registered vehicles in 2023. This surge in vehicle numbers exacerbates road congestion and highlights the pressing demand for efficient traffic management systems to manage the increased load on urban and suburban roads.

Market Challenges

- High Implementation and Maintenance Costs: Implementing advanced traffic management solutions incurs substantial expenses, with smart traffic signals costing up to $50,000 per intersection in the U.S. Maintaining these systems further escalates costs, as regular upgrades are required to keep pace with evolving technologies. In Canada, maintenance and repair costs for similar systems can reach up to CA$30,000 annually per unit. These high costs present a challenge, especially for smaller municipalities that may struggle to secure funding.

- Integration with Existing Infrastructure: Integrating new traffic management systems with existing, often outdated infrastructure is a major hurdle. In the U.S., over 40% of traffic lights and related equipment were installed more than 20 years ago, requiring extensive retrofitting for compatibility with modern systems. In Canadian cities, similar issues exist, with nearly 35% of existing traffic infrastructure needing updates to accommodate digital systems. These compatibility challenges complicate modernization efforts, delaying implementation.

North America Traffic Management Market Future Outlook

Over the next five years, the North America Traffic Management Market is expected to experience growth. This expansion will be driven by continuous government support, advancements in traffic management technologies, and increasing urbanization. The integration of AI and IoT in traffic systems is anticipated to enhance real-time data analytics, leading to more efficient traffic flow and reduced congestion. Additionally, the development of smart cities and the adoption of autonomous vehicles are expected to create new opportunities within the market.

Market Opportunities

- Adoption of AI and IoT in Traffic Management: AI and IoT are rapidly transforming traffic management in North America. By 2024, over 1,000 cities in the U.S. and Canada had adopted AI-driven traffic systems, enabling real-time traffic adjustments. In cities like Chicago, these AI systems have improved traffic flow by nearly 25%, reducing commute times. IoT-enabled sensors installed at intersections gather data for predictive analytics, improving planning and traffic predictions for urban management. The widespread adoption of these technologies is poised to enhance traffic efficiency and reduce congestion.

- Development of Smart Cities: Smart city initiatives are accelerating traffic management advancements. In the U.S., cities like New York and Los Angeles received federal funding exceeding $2 billion between 2022 and 2024 to develop smart infrastructure, focusing on traffic solutions. Canadas Smart City Challenge awarded CA$300 million to support similar initiatives, driving innovation in urban traffic systems. These initiatives leverage digital solutions, including adaptive signal controls, which reduce travel times by up to 20% in urban centers.

Scope of the Report

|

Segment |

Sub-Segments |

|

Component |

Hardware |

|

System |

Urban Traffic Management and Control (UTMC) Systems |

|

Application |

Automatic Tolling |

|

Deployment Model |

On-Premise |

|

Country |

United States |

Products

Key Target Audience

Urban Planning Departments (e.g., New York City Department of Transportation)

Transportation Agencies (e.g., Federal Highway Administration)

Smart City Developers

Traffic Management Solution Providers

Automotive Manufacturers

Technology Integrators

Investor and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., U.S. Department of Transportation)

Companies

Players Mentioned in the Report

Cisco Systems, Inc.

Siemens AG

IBM Corporation

Kapsch TrafficCom AG

Cubic Corporation

Thales Group

TransCore, LP

Q-Free ASA

Iteris, Inc.

TomTom International BV

Table of Contents

1. North America Traffic Management Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. North America Traffic Management Market Size (In USD Billion)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. North America Traffic Management Market Analysis

3.1 Growth Drivers

3.1.1 Urbanization and Population Growth

3.1.2 Government Initiatives and Investments

3.1.3 Technological Advancements in Traffic Management Systems

3.1.4 Increasing Vehicle Ownership

3.2 Market Challenges

3.2.1 High Implementation and Maintenance Costs

3.2.2 Integration with Existing Infrastructure

3.2.3 Data Privacy and Security Concerns

3.3 Opportunities

3.3.1 Adoption of AI and IoT in Traffic Management

3.3.2 Development of Smart Cities

3.3.3 Public-Private Partnerships

3.4 Trends

3.4.1 Shift Towards Cloud-Based Traffic Management Solutions

3.4.2 Emphasis on Sustainable and Green Transportation

3.4.3 Integration with Autonomous and Connected Vehicles

3.5 Government Regulations

3.5.1 Federal and State Transportation Policies

3.5.2 Environmental and Emission Standards

3.5.3 Funding Programs for Infrastructure Development

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competitive Landscape

4. North America Traffic Management Market Segmentation

4.1 By Component (In Value %)

4.1.1 Hardware

4.1.1.1 Cameras

4.1.1.2 Display Boards

4.1.1.3 Sensors

4.1.2 Software

4.1.2.1 On-Premise

4.1.2.2 Cloud-Based

4.1.3 Services

4.1.3.1 Consulting Services

4.1.3.2 Implementation Services

4.1.3.3 Support and Maintenance Services

4.2 By System (In Value %)

4.2.1 Urban Traffic Management and Control (UTMC) Systems

4.2.2 Adaptive Traffic Control Systems (ATCS)

4.2.3 Journey Time Measurement Systems (JTMS)

4.2.4 Predictive Traffic Modeling Systems (PTMS)

4.2.5 Incident Detection and Location Systems (IDLS)

4.2.6 Dynamic Traffic Management Systems (DTMS)

4.3 By Application (In Value %)

4.3.1 Automatic Tolling

4.3.2 Lane Management

4.3.3 Parking Management

4.3.4 Surveillance

4.3.5 Traffic Signal Management

4.3.6 Others

4.4 By Deployment Model (In Value %)

4.4.1 On-Premise

4.4.2 Cloud-Based

4.5 By Country (In Value %)

4.5.1 United States

4.5.2 Canada

4.5.3 Mexico

5. North America Traffic Management Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Cisco Systems, Inc.

5.1.2 Siemens AG

5.1.3 IBM Corporation

5.1.4 Kapsch TrafficCom AG

5.1.5 Cubic Corporation

5.1.6 Thales Group

5.1.7 TransCore, LP

5.1.8 Q-Free ASA

5.1.9 Iteris, Inc.

5.1.10 TomTom International BV

5.1.11 Hitachi Vantara Corporation

5.1.12 SNC-Lavalin Group (Atkins)

5.1.13 General Electric Company

5.1.14 Kapsch TrafficCom AG

5.1.15 Siemens Mobility

5.2 Cross Comparison Parameters (Number of Employees, Headquarters, Inception Year, Revenue, Market Share, Product Portfolio, Recent Developments, Strategic Initiatives)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. North America Traffic Management Market Regulatory Framework

6.1 Transportation Infrastructure Policies

6.2 Compliance Requirements

6.3 Certification Processes

7. Future Market Size (In USD Billion)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. Future Market Segmentation

8.1 By Component (In Value %)

8.2 By System (In Value %)

8.3 By Application (In Value %)

8.4 By Deployment Model (In Value %)

8.5 By Country (In Value %)

9. North America Traffic Management Market Analysts Recommendations

9.1 Total Addressable Market (TAM), Serviceable Available Market (SAM), and Serviceable Obtainable Market (SOM) Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the North America Traffic Management Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the North America Traffic Management Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics is conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple traffic management solution providers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction serves to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the North America Traffic Management Market.

Frequently Asked Questions

01. How big is the North America Traffic Management Market?

The North America Traffic Management Market is valued at USD 11.3 billion, based on a five-year historical analysis. This valuation reflects the region's significant investments in traffic infrastructure and smart city initiatives.

02. What are the challenges in the North America Traffic Management Market?

Challenges include high implementation and maintenance costs, integration with existing infrastructure, and data privacy and security concerns. Additionally, the rapid pace of technological advancements necessitates continuous updates and training.

03. Who are the major players in the North America Traffic Management Market?

Key players in the market include Cisco Systems, Inc., Siemens AG, IBM Corporation, Kapsch TrafficCom AG, and Cubic Corporation. These companies dominate due to their extensive product portfolios and strategic partnerships.

04. What are the growth drivers of the North America Traffic Management Market?

The market is propelled by factors such as rapid urbanization, increasing vehicle ownership, government initiatives, and technological advancements in traffic management systems. The development of smart cities also contributes to market growth.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.