North America Transformers Market Outlook to 2030

Region:North America

Author(s):Yogita Sahu

Product Code:KROD4989

October 2024

83

About the Report

North America Transformers Market Overview

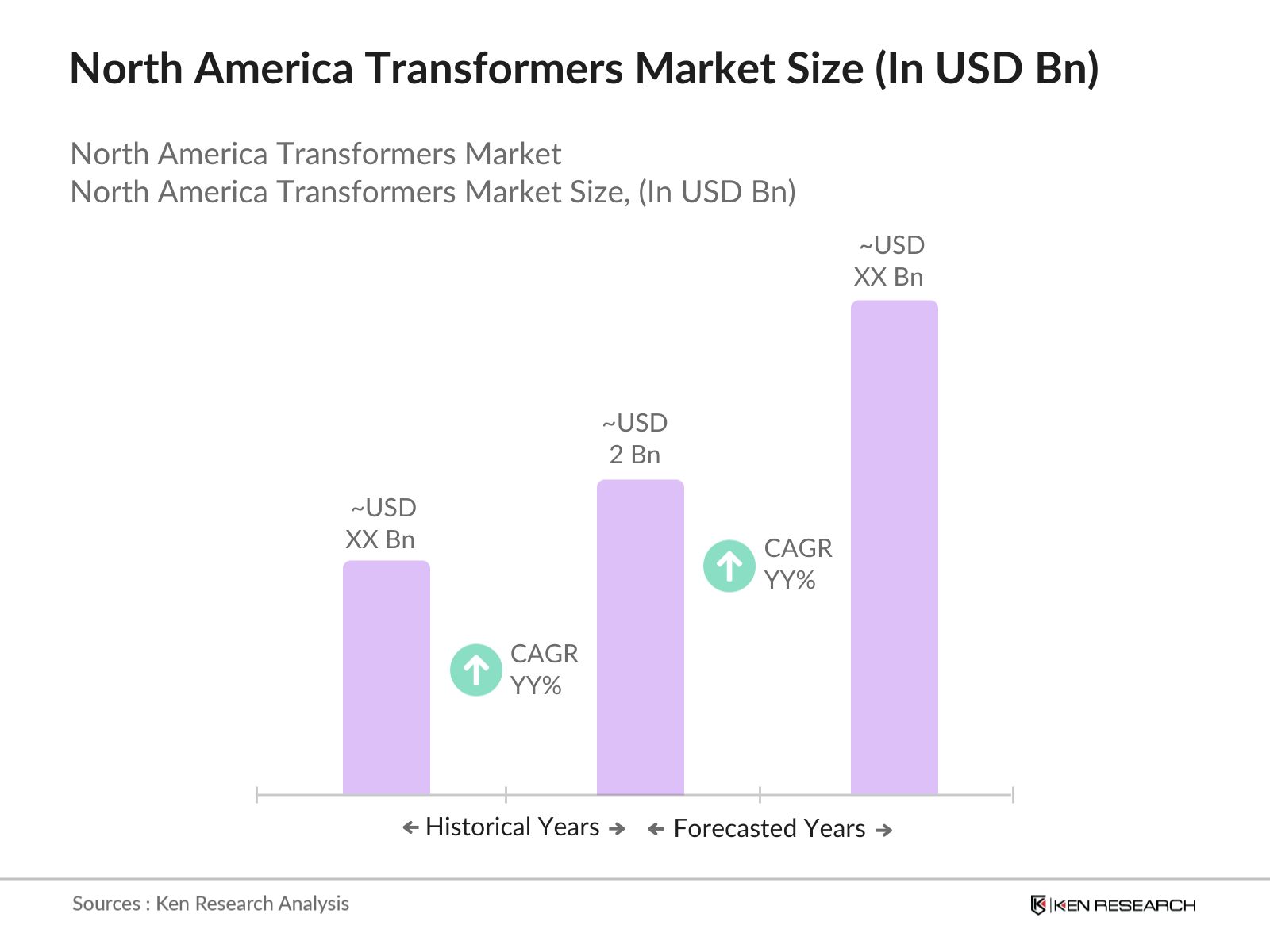

- The North America Transformers market is valued at USD 2 billion, based on a five-year historical analysis. This valuation is primarily driven by increasing demand for energy and ongoing investments in grid infrastructure. The rising energy consumption in residential, commercial, and industrial sectors has led to an upsurge in the demand for transformers.

- The market is dominated by the United States and Canada, which lead in the market due to their extensive infrastructure development and robust energy consumption. The United States is the largest market owing to its high industrialization rate, urbanization, and heavy investment in upgrading its transmission and distribution networks.

- Under the 2021 bipartisan infrastructure law, over USD 62 billion has been allocated to enhance the renewable energy transmission network, including grid modernization projects across New England states, aimed at integrating offshore wind energy into the national grid.

North America Transformers Market Segmentation

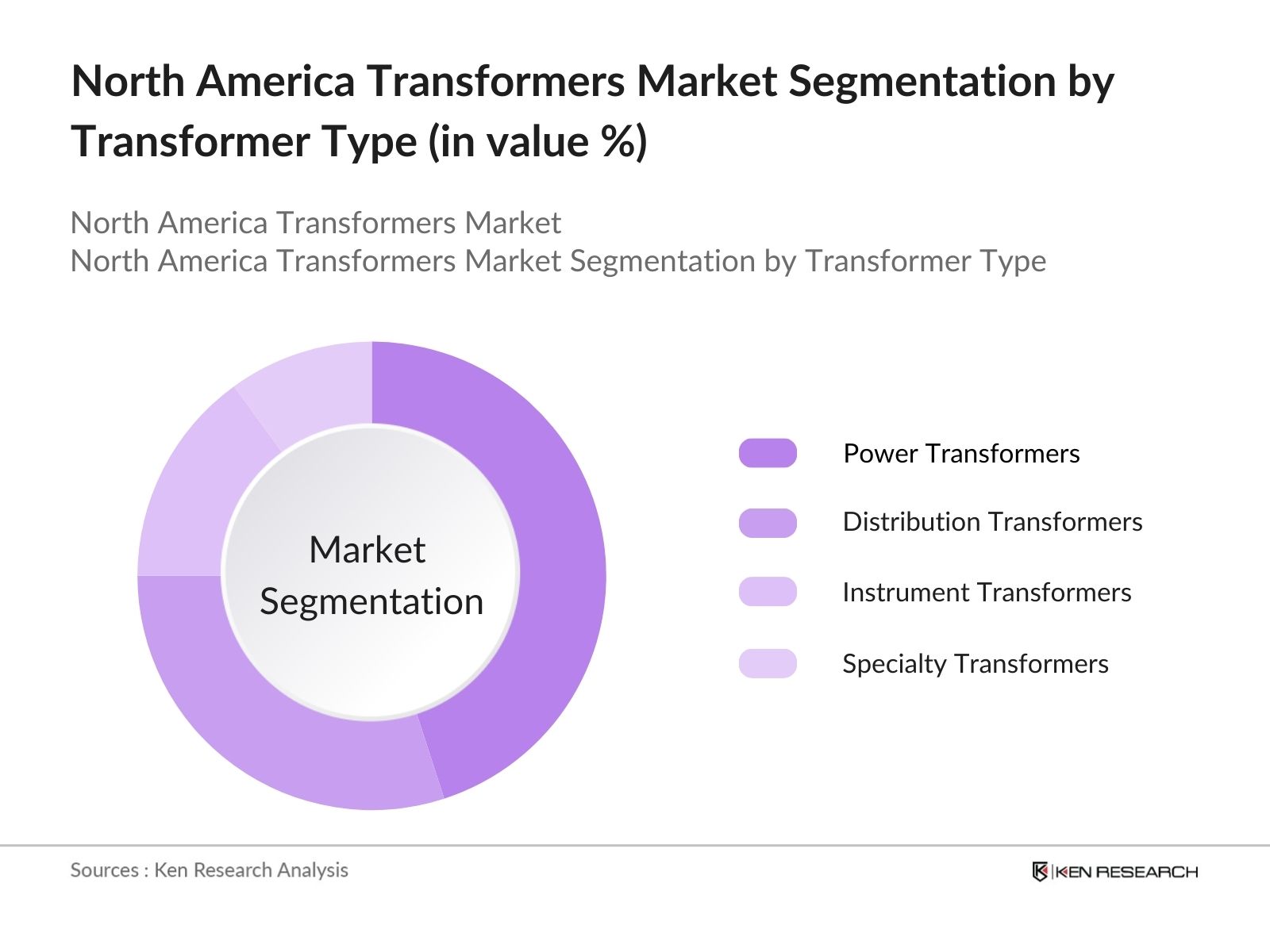

By Transformer Type: The market is segmented by transformer type into Power Transformers, Distribution Transformers, Instrument Transformers, and Specialty Transformers. Recently, Power Transformers have a dominant market share in the region, driven by their extensive use in high-voltage transmission networks. Power transformers are critical for long-distance energy transmission, where voltage needs to be stepped up or down efficiently.

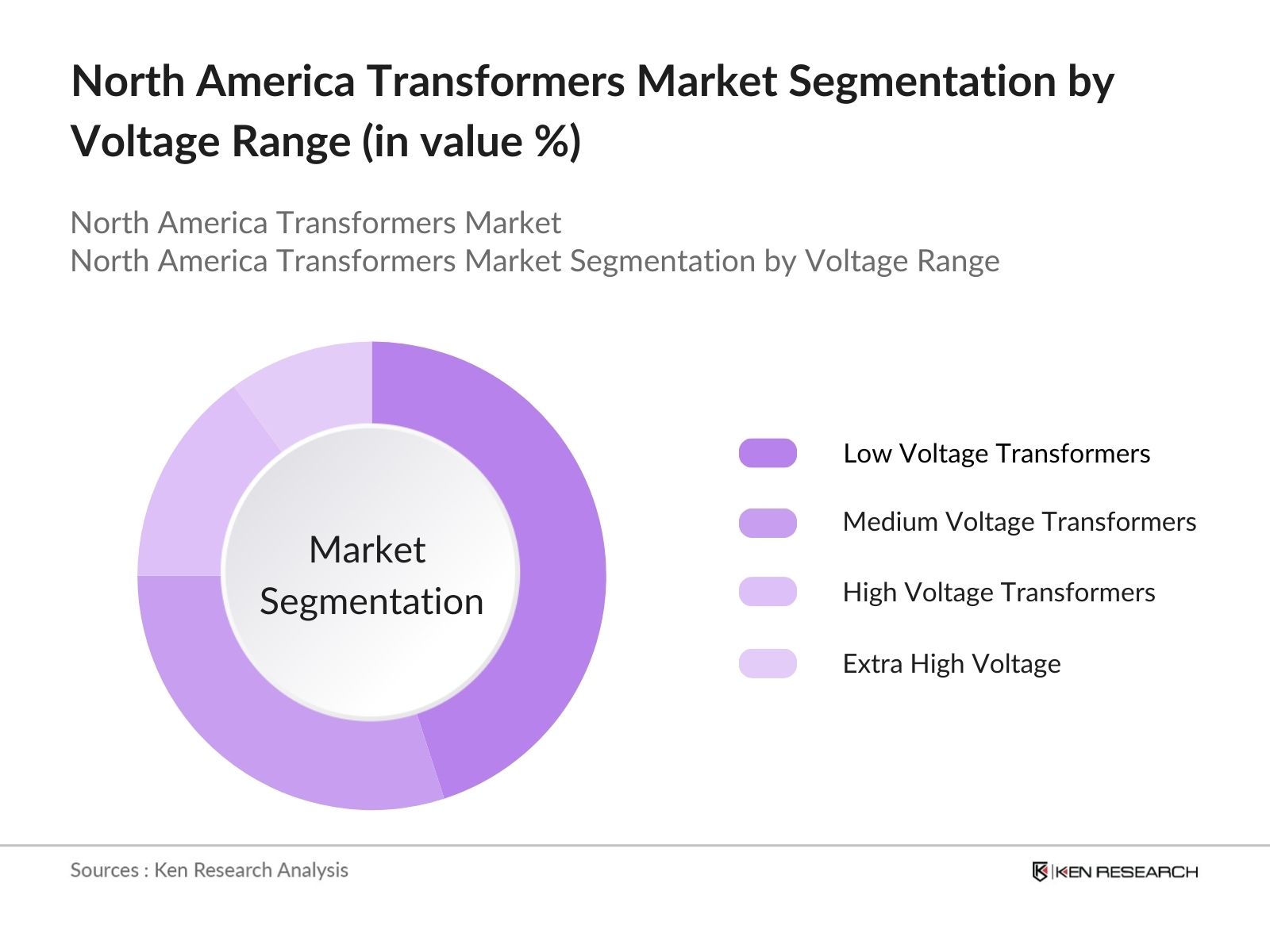

By Voltage Range: The market is further segmented by voltage range into Low Voltage (LV), Medium Voltage (MV), High Voltage (HV), and Extra High Voltage (EHV) transformers. High Voltage transformers account for the largest share of the market due to their widespread application in transmission networks. The increasing demand for high-voltage transformers is fueled by the modernization of aging power infrastructure and the expansion of renewable energy projects, particularly in the United States and Canada, which require high-voltage transformers to integrate large amounts of renewable energy into the grid efficiently.

North America Transformers Market Competitive Landscape

The market is consolidated, with a few key players dominating the landscape. Major companies such as General Electric, Siemens Energy, ABB Ltd., Schneider Electric, and Eaton Corporation lead the market. This consolidation reflects the significant technological expertise and investment capabilities of these companies.

|

Company |

Year Established |

Headquarters |

Revenue |

Market Share |

Product Range |

R&D Investment |

Global Reach |

Technology Focus |

Sustainability Initiatives |

|

General Electric |

1892 |

Boston, USA |

|||||||

|

Siemens Energy |

1866 |

Munich, Germany |

|||||||

|

ABB Ltd. |

1988 |

Zurich, Switzerland |

|||||||

|

Schneider Electric |

1836 |

Rueil-Malmaison, France |

|||||||

|

Eaton Corporation |

1911 |

Dublin, Ireland |

North America Transformers Market Analysis

Market Growth Drivers

- Grid Modernization Initiatives: Governments and utility companies in North America are heavily investing in upgrading their aging power infrastructure. Over 70% of the transmission and distribution (T&D) infrastructure in the U.S. has exceeded 25 years, necessitating refurbishment and new transformer installations. Major utilities in the U.S. alone spent big amount on transmission operations in 2022, signaling the high demand for transformers.

- Renewable Energy Integration: With North America's renewable energy capacity exceeding 489 GW in 2022, the need for transformers capable of integrating renewable energy sources into the grid has surged. The increasing deployment of wind and solar power projects, particularly in the U.S., necessitates specialized transformers for stable power transmission.

- Rising Energy Consumption: North America's electricity demand continues to grow, with the U.S. Energy Information Administration reporting that electricity generation in the U.S. is expected to rise. This heightened demand for electricity drives the need for efficient transformers, essential for reliable transmission and distribution of power across the grid.

Market Challenges

- High Capital Expenditure: One of the barriers for transformer projects in North America is the high initial cost. The replacement of old equipment and installation of advanced transformers require substantial investments, with costs often running into millions for large-scale grid modernization.

- Dependency on Aging Infrastructure: A major portion of the North American power grid is aging, with some infrastructure operating beyond its designed capacity. Replacing or upgrading these systems with new transformer installations is not only expensive but also logistically complex.

North America Transformers Future Outlook

Over the next five years, the North America Transformers industry is expected to experience growth driven by continuous infrastructure development, renewable energy integration, and technological advancements. The increasing adoption of smart grids and digital transformers will also drive demand, as utilities seek to enhance grid reliability and efficiency.

Future Market Opportunities

- Adoption of Digital Transformers: The demand for digital and smart transformers, equipped with IoT capabilities, is expected to rise, improving real-time monitoring and predictive maintenance. This trend will lead to enhanced grid efficiency and reliability.

- Focus on Energy Efficiency and Sustainability: By 2030, governments and utility providers will place greater emphasis on energy efficiency in transformer designs. The push toward reducing greenhouse gas emissions and adopting carbon-neutral technologies will drive innovations in transformer production.

Scope of the Report

|

By Type |

Power Transformers Distribution Transformers Instrument Transformers Isolation Transformers Specialty Transformers |

|

By Voltage Range |

Low Voltage Medium Voltage High Voltage Extra High Voltage |

|

By Installation Type |

Indoor Outdoor |

|

By Phase |

Single Phase Three Phase |

|

By End-Use Industry |

Utilities Industrial Commercial Residential Transportation |

|

By Region |

USA |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Utility Companies (e.g., National Grid, Duke Energy)

Government and Regulatory Bodies (e.g., U.S. Department of Energy, Environmental Protection Agency)

Banks and Financial Institutions

Electric Vehicle Infrastructure Companies

EPC (Engineering, Procurement, and Construction) Firms

Private Equity Firms

Investment and Venture Capital Firms

Companies

Players Mentioned in the Report:

General Electric

Siemens Energy

ABB Ltd.

Schneider Electric

Eaton Corporation

Mitsubishi Electric Corporation

Hitachi Energy

Toshiba Corporation

SPX Transformer Solutions

SGB-SMIT Group

Hyundai Electric & Energy Systems

WEG Industries

Bharat Heavy Electricals Limited (BHEL)

CG Power and Industrial Solutions

Siemens AG

Table of Contents

1. North America Transformers Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (CAGR, Market Penetration Rate, Market Maturity)

1.4. Market Segmentation Overview

2. North America Transformers Market Size (In USD Bn)

2.1. Historical Market Size (Demand Volume, Installed Base, Market Value)

2.2. Year-On-Year Growth Analysis (Y-o-Y Growth, Capacity Expansion, Volume Growth)

2.3. Key Market Developments and Milestones (Major Installations, Technological Advancements, Key Partnerships)

3. North America Transformers Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Energy Demand (Electricity Consumption Growth, Grid Modernization)

3.1.2. Infrastructure Expansion (Investment in Transmission and Distribution Networks, Smart Grid Deployment)

3.1.3. Regulatory Mandates (Energy Efficiency Standards, Environmental Compliance, Renewable Energy Integration)

3.1.4. Rise in Industrialization (Heavy Industry Power Requirements, Urbanization, Commercial Development)

3.2. Market Challenges

3.2.1. High Capital Expenditure (Cost of Raw Materials, Installation Costs, Maintenance)

3.2.2. Technological Limitations (Power Losses, Voltage Drop, Efficiency Challenges)

3.2.3. Supply Chain Constraints (Raw Material Shortages, Transportation Delays)

3.3. Opportunities

3.3.1. Smart Transformer Integration (Digitalization, Remote Monitoring, Predictive Maintenance)

3.3.2. Renewable Energy Projects (Offshore Wind Farms, Solar Energy Infrastructure)

3.3.3. Expansion into Emerging Sectors (EV Charging Infrastructure, Data Centers)

3.4. Trends

3.4.1. Shift Towards Green Transformers (Eco-Friendly Transformers, Use of Natural Ester Fluids)

3.4.2. Adoption of Digital Transformers (IoT-enabled Transformers, Smart Grids)

3.4.3. Miniaturization of Transformers (Compact Transformers for Urban Applications)

3.5. Government Regulations

3.5.1. Energy Efficiency Programs (Energy Star, DOE Regulations)

3.5.2. Emission Reduction Policies (GHG Emission Norms, Net Zero Targets)

3.5.3. Support for Renewable Integration (Tax Credits, Green Energy Incentives)

3.5.4. Infrastructure Stimulus Packages (Investment in T&D Networks, Infrastructure Revitalization)

3.6. SWOT Analysis

3.6.1. Strengths (Market Demand, Technological Advancements, Government Support)

3.6.2. Weaknesses (Cost Barriers, Competitive Landscape, Long Project Cycles)

3.6.3. Opportunities (Smart Grid Integration, Sustainability Demand)

3.6.4. Threats (Supply Chain Disruptions, Regulatory Risks)

3.7. Stakeholder Ecosystem (Utility Companies, Industrial Consumers, OEMs, Regulatory Bodies)

3.8. Porters Five Forces

3.8.1. Supplier Power (Raw Material Suppliers, Component Suppliers)

3.8.2. Buyer Power (Utility Providers, Industrial End-users, Contractors)

3.8.3. Threat of Substitutes (Alternatives to Transformers, Distributed Generation)

3.8.4. Threat of New Entrants (Market Entry Barriers, Technological Knowledge)

3.8.5. Industry Rivalry (Level of Competition, Market Concentration)

3.9. Competition Ecosystem (OEMs, EPCs, Independent Transformer Manufacturers)

4. North America Transformers Market Segmentation

4.1. By Type (In Value %)

4.1.1. Power Transformers

4.1.2. Distribution Transformers

4.1.3. Instrument Transformers

4.1.4. Isolation Transformers

4.1.5. Specialty Transformers

4.2. By Voltage Range (In Value %)

4.2.1. Low Voltage (<600V)

4.2.2. Medium Voltage (600V 69kV)

4.2.3. High Voltage (69kV 230kV)

4.2.4. Extra High Voltage (>230kV)

4.3. By Installation Type (In Value %)

4.3.1. Indoor

4.3.2. Outdoor

4.4. By Phase (In Value %)

4.4.1. Single Phase

4.4.2. Three Phase

4.5. By End-Use Industry (In Value %)

4.5.1. Utilities

4.5.2. Industrial

4.5.3. Commercial

4.5.4. Residential

4.5.5. Transportation (EV Charging, Railways)

4.6. By Region (In Value %)

4.6.1 USA

4.6.2. Canada

5. North America Transformers Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. General Electric

5.1.2. Siemens Energy

5.1.3. ABB Ltd.

5.1.4. Schneider Electric

5.1.5. Eaton Corporation

5.1.6. Mitsubishi Electric Corporation

5.1.7. Hitachi Energy

5.1.8. Toshiba Corporation

5.1.9. Hyundai Electric & Energy Systems

5.1.10. CG Power and Industrial Solutions

5.1.11. SPX Transformer Solutions

5.1.12. SGB-SMIT Group

5.1.13. WEG Industries

5.1.14. Siemens AG

5.1.15. Bharat Heavy Electricals Limited (BHEL)

5.2. Cross Comparison Parameters (Revenue, Market Share, Installed Base, R&D Investment, No. of Employees, Service Network, Market Presence, Technological Focus)

5.3. Market Share Analysis (Market Share by Company, Segment, and Region)

5.4. Strategic Initiatives (Expansion Strategies, Partnerships, Joint Ventures, Mergers)

5.5. Mergers and Acquisitions (M&A Analysis, Key Deals, Impact on Market)

5.6. Investment Analysis (Venture Capital Funding, Private Equity Investments, Corporate Investments)

5.7. Venture Capital and Private Equity Investments (Active Investments, Key Market Players)

6. North America Transformers Market Regulatory Framework

6.1. Energy Standards (Compliance with DOE Standards, IEEE, NEMA Guidelines)

6.2. Environmental Regulations (EPA, Clean Energy Standards, Lifecycle Emissions)

6.3. Certification Requirements (ISO, UL Certifications)

7. North America Transformers Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Transformers Future Market Segmentation

8.1. By Transformer Type

8.2. By Voltage Range

8.3. By Installation Type

8.4. By End-Use Industry

8.5. By Region

9. North America Transformers Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis (Utility Customers, Industrial Consumers)

9.3. Marketing Initiatives (Product Positioning, Market Expansion Strategies)

9.4. White Space Opportunity Analysis (Geographical Gaps, Technology Gaps, Market Gaps

Research Methodology

Step 1: Identification of Key Variables

The research begins by mapping the ecosystem of the North America Transformers market, focusing on major stakeholders like utility companies, industrial consumers, and transformer manufacturers. A comprehensive desk research approach is used, involving secondary databases and proprietary data sources, to gather crucial industry-level information.

Step 2: Market Analysis and Construction

We collect and analyze historical data on transformer demand, supply, and revenue generation. This includes evaluating transformer penetration across end-use industries and compiling statistics on installed transformer capacity across North America.

Step 3: Hypothesis Validation and Expert Consultation

To validate the market data, we conduct computer-assisted telephone interviews (CATIs) with industry experts from transformer manufacturing companies, utilities, and grid operators. These insights are essential in refining market estimates and projections.

Step 4: Research Synthesis and Final Output

We consolidate the findings by engaging with transformer manufacturers and utilities to cross-check product performance data, transformer installations, and market trends. This step ensures the accuracy and comprehensiveness of the market report.

Frequently Asked Questions

01. How big is the North America Transformers market?

The North America Transformers market is valued at USD 2 billion, driven by infrastructure development and renewable energy integration across the United States and Canada.

02. What are the key challenges in the North America Transformers market?

Key challenges in the North America Transformers market include high capital expenditure for advanced transformer solutions, supply chain disruptions affecting raw material availability, and regulatory compliance for environmental and energy efficiency standards.

03. Who are the major players in the North America Transformers market?

Leading players in the North America Transformers market include General Electric, Siemens Energy, ABB Ltd., Schneider Electric, and Eaton Corporation. These companies dominate the market due to their extensive product portfolios and technological advancements in smart transformers.

04. What is driving the growth of the North America Transformers market?

Growth in the North America Transformers market is driven by increased energy consumption, grid modernization efforts, renewable energy integration, and advancements in smart grid technology.

05. How is the future outlook for the North America Transformers market?

The future looks promising, with continuous infrastructure investments, government support for renewable energy projects, and the rising demand for electric vehicle charging infrastructure expected to drive North America Transformers market growth.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.