Philippines Charcoal Market Outlook to 2030

Region:Philippines

Author(s):Sanjeev

Product Code:KROD10434

Region:Philippines

Author(s):Sanjeev

Product Code:KROD10434

November 2024

94

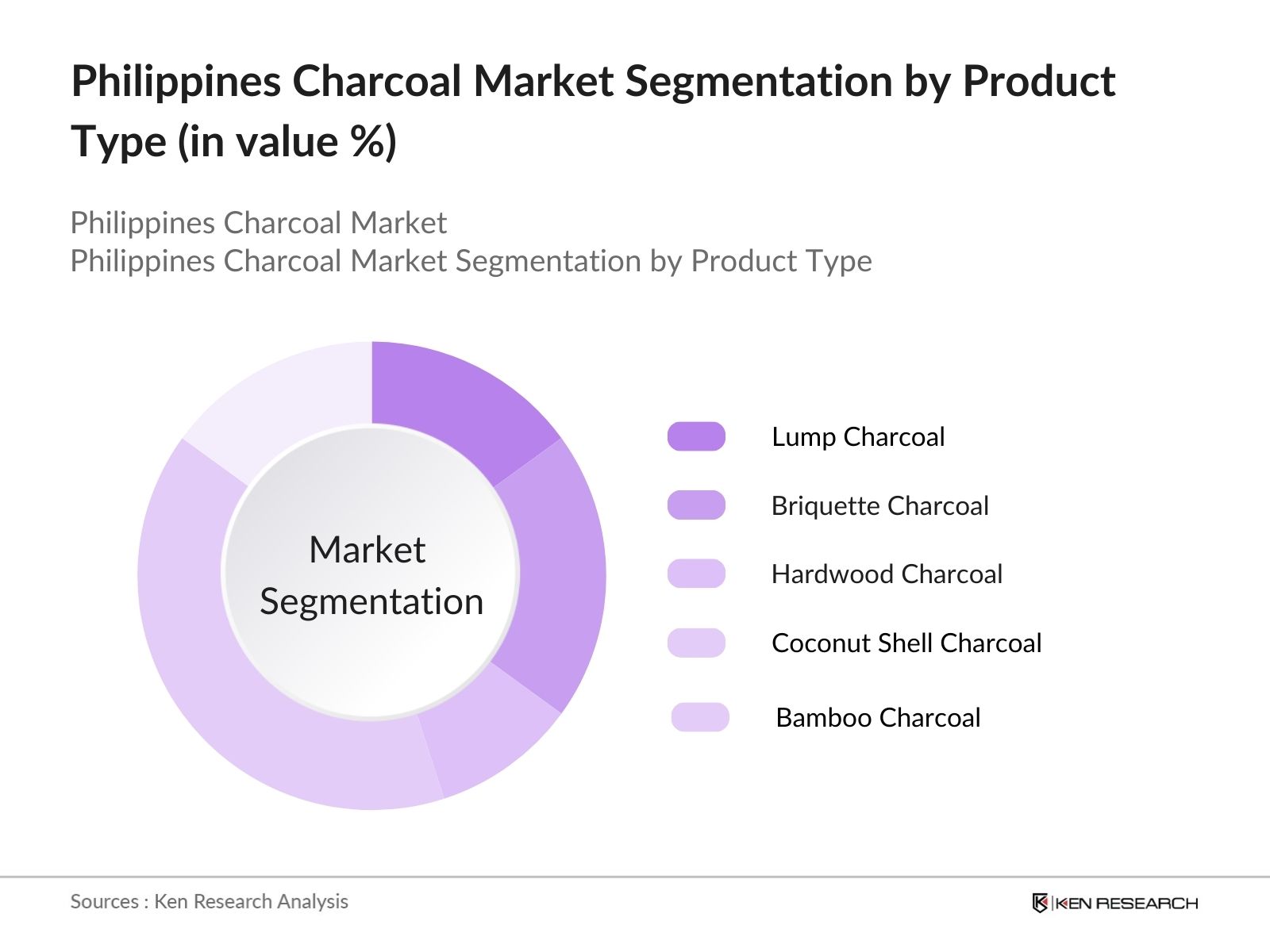

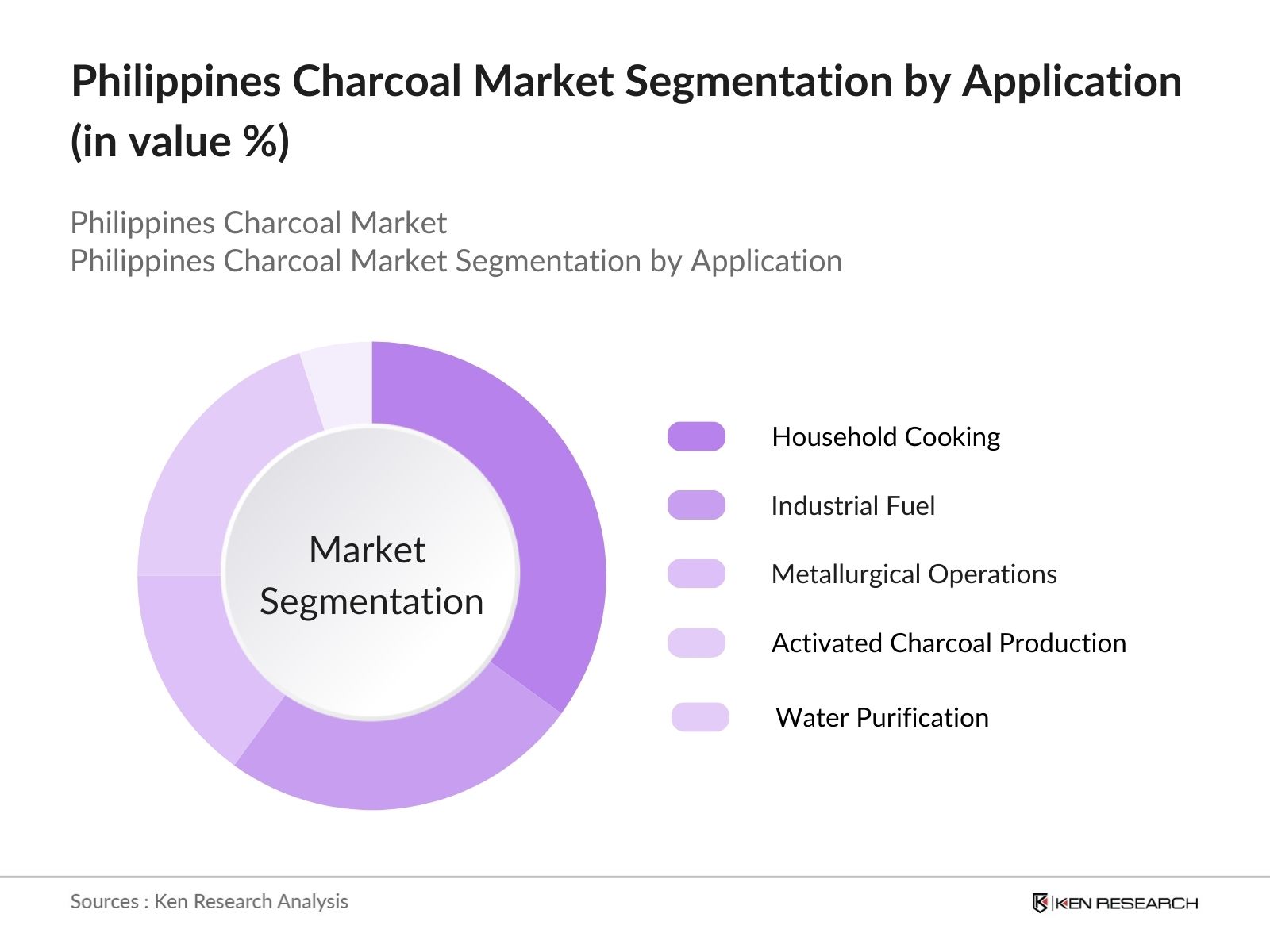

The Philippines Charcoal Market is segmented by product type and by application.

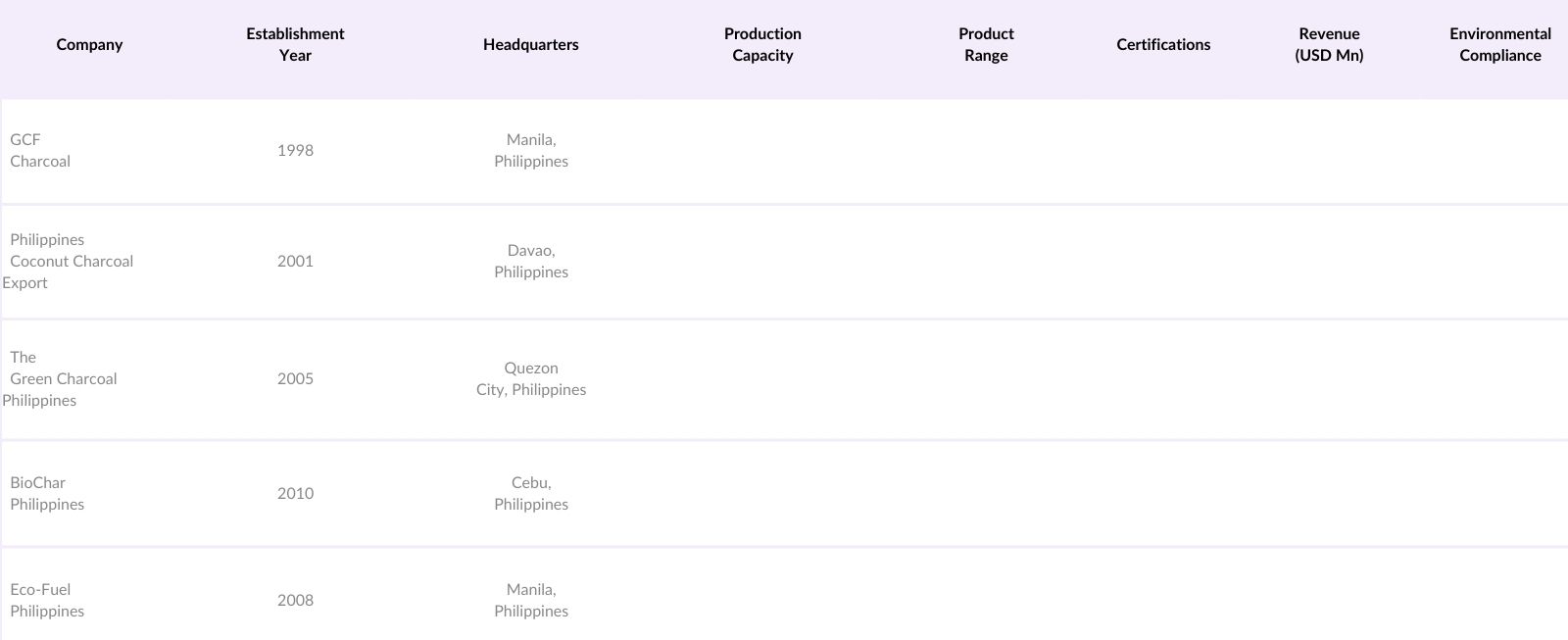

The Philippines Charcoal Market is dominated by a few major players, whose market presence emphasizes both local and export-oriented operations. The competitive landscape showcases the influence of these key players on production capacity, revenue generation, and market expansion initiatives.

Over the next few years, the Philippines Charcoal Market is expected to grow due to expanded applications in water purification, industrial fuel demand, and the increasing use of activated charcoal in various industries. Government incentives and support for sustainable charcoal production, alongside production technique innovations, are likely to enhance the market. In particular, a continued focus on environmental compliance and the availability of government grants for sustainable initiatives will shape market growth, with anticipated improvements in export capabilities, particularly for coconut shell and activated charcoal.

|

Lump Charcoal Briquette Charcoal Hardwood Charcoal Coconut Shell Charcoal Bamboo Charcoal |

|

|

By Application |

Household Cooking Industrial Fuel Metallurgical Operations Activated Charcoal Production Water Purification |

|

By Production Method |

Traditional Kilns Metal Drum Kilns Brick Kilns Retort Kilns |

|

By Distribution Channel |

Retail Stores Wholesale Markets E-commerce Export |

|

By Region |

North East West South |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Drivers

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Milestones and Developments

3.1 Growth Drivers (e.g., Demand Surge in Domestic Fuel, Industrial Applications) - Urban Energy Demand

- Rural Household Usage

- Increasing Export Demand

- Agricultural Waste Utilization

3.2 Market Challenges (e.g., Supply Chain Bottlenecks, Environmental Policies) - Transportation and Logistics

- Regulatory Compliance

- Supply and Price Volatility

- Competition from Alternative Fuels

3.3 Opportunities (e.g., Technological Advancements, Export Markets) - Eco-Friendly Charcoal Production

- Expansion in High-Energy-Demand Regions

- Carbon Credit Incentives

- Regional Export Market Growth

3.4 Industry Trends (e.g., Sustainable Sourcing, Biomass Utilization) - Sustainable Charcoal Production

- Enhanced Biomass Utilization

- Technological Innovations

- Shift to Value-Added Charcoal Products

3.5 Government Regulation (e.g., Emission Standards, Export Controls) - Department of Environment and Natural Resources (DENR) Compliance

- Emission Control Regulations

- Export Policy and Restrictions

- Forest Preservation Initiatives

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem Overview

3.8 Porters Five Forces Analysis

3.9 Competition and Market Structure Analysis

4.1 By Product Type (in Value %)

4.1.1 Lump Charcoal

4.1.2 Briquette Charcoal

4.1.3 Hardwood Charcoal

4.1.4 Coconut Shell Charcoal

4.1.5 Bamboo Charcoal

4.2 By Application (in Value %)

4.2.1 Household Cooking

4.2.2 Industrial Fuel

4.2.3 Metallurgical Operations

4.2.4 Activated Charcoal Production

4.2.5 Water Purification

4.3 By Production Method (in Value %)

4.3.1 Traditional Kilns

4.3.2 Metal Drum Kilns

4.3.3 Brick Kilns

4.3.4 Retort Kilns

4.4 By Distribution Channel (in Value %)

4.4.1 Retail Stores

4.4.2 Wholesale Markets

4.4.3 E-commerce

4.4.4 Export

4.5 By Region (in Value %)

4.5.1 North

4.5.2 East

4.5.3 West

4.5.4 South

5.1 Detailed Profiles of Major Companies

5.1.1 GCF Charcoal

5.1.2 Philippines Coconut Charcoal Export

5.1.3 The Green Charcoal Philippines

5.1.4 Philippine Bio-Charcoal

5.1.5 Philippine Charcoal and Briquettes

5.1.6 Eco-Fuel Philippines

5.1.7 CJ Charcoal Export Philippines

5.1.8 BioChar Philippines

5.1.9 Filipino Charcoal Processing

5.1.10 Agrichar Philippines

5.1.11 Green Flame Charcoal

5.1.12 Charcoal Philippines International

5.1.13 Asia Bio-Carbon Philippines

5.1.14 Cocogreen Philippines

5.1.15 CocoChar Philippines

5.2 Cross-Comparison Parameters (Production Capacity, Export Percentage, Certifications, Revenue, Market Share, Product Range, Supply Chain Integration, Environmental Compliance)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Government Grants and Subsidies

5.8 Private Equity Investments

5.9 Export Market Strategies

6.1 Environmental Protection Laws

6.2 Forestry Regulations

6.3 Export Compliance and Standards

6.4 Tax Incentives for Sustainable Practices

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 TAM/SAM/SOM Analysis

8.2 Market Expansion Strategies

8.3 Consumer Demographic Insights

8.4 Eco-Friendly Production Recommendations

8.5 Potential for New Product Development

Disclaimer Contact UsThis phase involves mapping all major stakeholders in the Philippines Charcoal Market ecosystem. Secondary research is conducted to identify critical variables influencing market dynamics, such as production techniques and market trends.

Historical data on market volume, production capacity, and export ratios are analyzed to understand sectoral performance. This includes product utilization in both domestic and international markets, alongside revenue generation metrics.

Market hypotheses are validated through expert consultations with stakeholders across the charcoal supply chain, which confirms production and sales data and clarifies operational practices, ensuring a reliable dataset.

The final synthesis involves engaging with charcoal manufacturers to acquire insights on consumer preferences, environmental compliance, and product innovation. This ensures comprehensive and validated analysis of the market, which provides accurate insights for stakeholders.

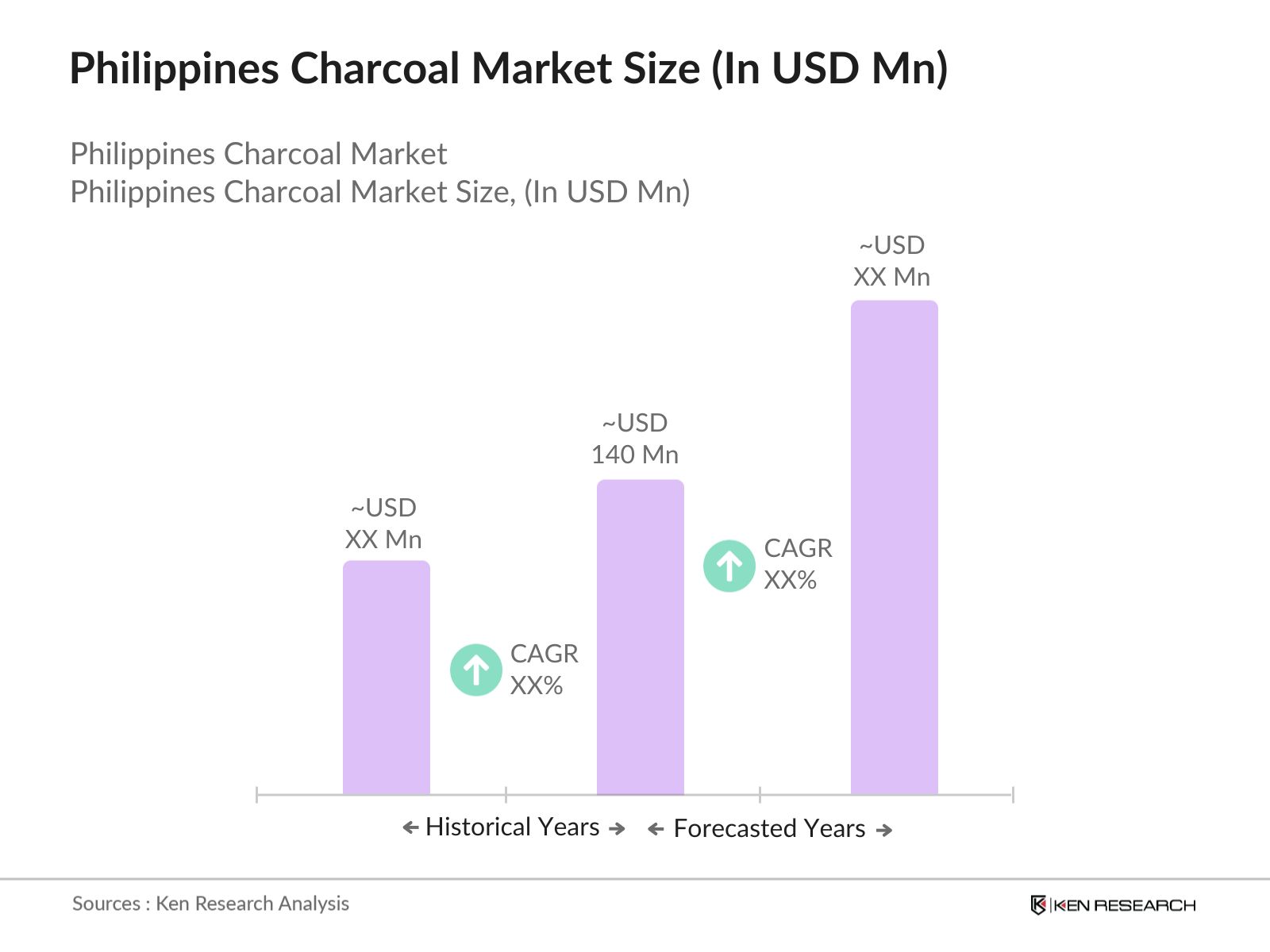

The Philippines Charcoal Market is valued at USD 140 million, driven by high demand in industrial fuel and activated charcoal production.

Key challenges in Philippines Charcoal Market include limited availability of high-quality raw materials, stringent environmental regulations, and labor-intensive production, impacting production scalability.

Leading players in Philippines Charcoal Market include GCF Charcoal, The Green Charcoal Philippines, Philippine Bio-Charcoal, Eco-Fuel Philippines, and CJ Charcoal Export Philippines, noted for their product diversity and export focus.

Growth drivers in Philippines Charcoal Market include the increasing demand for eco-friendly fuels, charcoals high calorific value, and government incentives for sustainable production methods.

Luzon and Mindanao are dominant due to their abundance of coconut plantations, favorable climate for charcoal processing, and efficient export channels, enhancing their production and supply capabilities.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.