Philippines Confectionery Market Outlook to 2030

Region:Philippines

Author(s):Aashi and Manan

Product Code:KR1517

Region:Philippines

Author(s):Aashi and Manan

Product Code:KR1517

July 2025

80

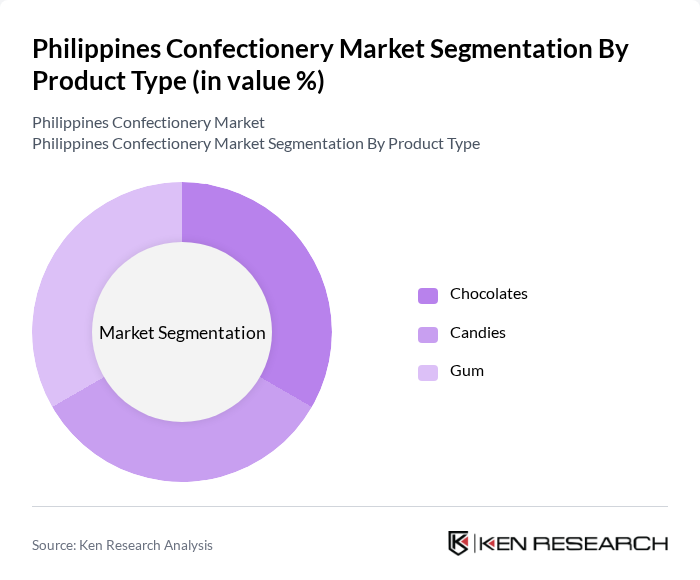

By Product Type: The confectionery market is segmented into chocolates, sugar confectionery (candies), and gums. Chocolates maintain the largest share, driven by their popularity for gifting and everyday consumption. The rise of premium and artisanal chocolate brands, along with increased demand for healthier and innovative chocolate products, has further solidified chocolates' leading position in the market. Sugar confectionery, including hard candies and chewy sweets, appeals to a broad demographic, while gum remains popular among younger consumers seeking novelty and functional benefits .

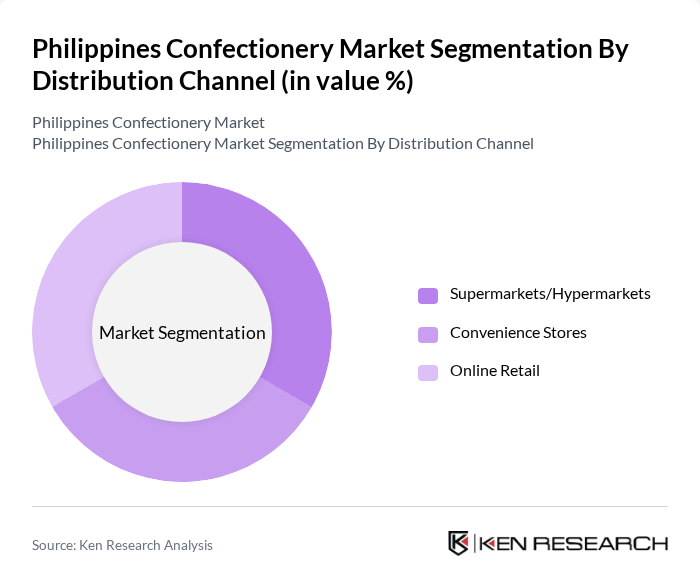

By Distribution Channel: The market is segmented into supermarkets/hypermarkets, convenience stores, online retail, and others. Supermarkets and hypermarkets are the leading distribution channels, offering a wide product range and the convenience of one-stop shopping. Convenience stores are also significant, particularly in urban areas with high foot traffic. Online retail is gaining traction, especially among younger, digitally savvy consumers who value convenience and access to a broader assortment of products .

The Philippines Confectionery Market is characterized by a competitive landscape with several key players, including multinational corporations and local manufacturers. Major companies such as Mondelez Philippines, Nestlé Philippines, and Universal Robina Corporation are prominent in this market, leveraging their extensive distribution networks and strong brand recognition to capture consumer attention. The market is moderately concentrated, with these companies continuously innovating to meet changing consumer preferences .

The Philippines confectionery market is poised for dynamic growth, driven by evolving consumer preferences and technological advancements. As disposable incomes rise, consumers are expected to increasingly favor premium and artisanal products. Additionally, the shift towards online shopping will continue to reshape the retail landscape, providing brands with new avenues for reaching consumers. Companies that innovate and adapt to these trends will likely thrive, while those that fail to respond may struggle to maintain relevance in this competitive market.

| By Type |

Chocolate Candies Gum Others |

| By End-User |

Children Teenagers Adults Seniors Others |

| By Distribution Channel |

Supermarkets/Hypermarkets Convenience Stores Online Retail Others |

| By Occasion |

Festivals Birthdays Holidays Everyday Consumption Others |

| By Packaging Type |

Rigid Packaging Flexible Packaging Bulk Packaging Others |

| By Flavor |

Chocolate Fruit Mint Spicy Others |

| By Price Range |

Premium Mid-range Economy Others |

| By Health Attribute |

Sugar-free Organic Gluten-free Functional Others |

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the Philippines Confectionery Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

In this phase, we will compile and analyze historical data pertaining to the Philippines Confectionery Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

The final phase involves direct engagement with multiple manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the Philippines Confectionery Market.

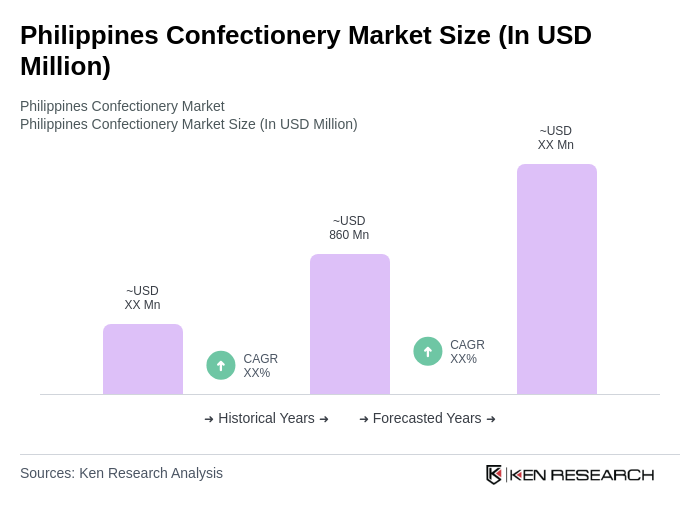

The Philippines Confectionery Market is valued at approximately USD 860 million, reflecting a five-year historical analysis. This growth is attributed to rising disposable incomes, urbanization, and a preference for indulgent snacks among younger consumers.

Metro Manila, Cebu, and Davao are the leading cities in the Philippines Confectionery Market. Metro Manila, as the capital, has a high concentration of retail outlets, while Cebu and Davao benefit from expanding urban populations and strategic locations.

The market is segmented into chocolates, sugar confectionery (candies), and gums. Chocolates hold the largest market share, driven by gifting and everyday consumption, while sugar confectionery appeals to a broad demographic, and gum is popular among younger consumers.

The Philippine government enforces Sugar Regulatory Administration (SRA) guidelines to regulate sugar production and pricing. These measures aim to stabilize the sugar market, ensure fair pricing, and promote local sugar production, supporting the domestic confectionery industry.

Key growth drivers include increasing disposable incomes, rising demand for premium confectionery products, and the expansion of e-commerce platforms. These factors enable consumers to spend more on indulgent and high-quality confectionery items.

The market faces challenges such as intense competition among over 200 local and international brands, fluctuating raw material prices, and health concerns related to sugar consumption. These factors can impact profit margins and market stability.

Opportunities include the growing trend for healthier confectionery options, expansion into untapped rural markets, and innovation in product offerings. Brands can capture market share by catering to health-conscious consumers and reaching underserved populations.

The market is primarily segmented into supermarkets/hypermarkets, convenience stores, online retail, and specialty stores. Supermarkets and hypermarkets lead in distribution, while online retail is gaining traction among younger, digitally savvy consumers.

The market is expected to experience dynamic growth, driven by rising disposable incomes and evolving consumer preferences. The shift towards online shopping and premium products will reshape the retail landscape, benefiting innovative brands.

Key players include Mondelez Philippines, Nestlé Philippines, Universal Robina Corporation, Hershey's Philippines, and Ferrero Philippines. These companies leverage extensive distribution networks and strong brand recognition to capture consumer attention in the competitive market.

Trends include the increasing popularity of artisanal and handmade products, a shift towards sustainable packaging, and a growing interest in local flavors. These trends reflect changing consumer preferences and a demand for unique, high-quality offerings.

E-commerce is projected to grow significantly, facilitating easier access to a wide range of confectionery products. The convenience of online shopping, combined with social media marketing, boosts sales for both established brands and new entrants.

There is a rising consumer interest in healthier confectionery options, such as sugar-free and organic products. This trend is expected to grow, presenting opportunities for brands to innovate and cater to health-conscious consumers.

Packaging types in the market include rigid packaging, flexible packaging, and bulk packaging. These options cater to various consumer preferences and product types, ensuring convenience and appeal in retail settings.

The SRA plays a crucial role in regulating sugar production and pricing in the Philippines. Its guidelines aim to stabilize the sugar market, promote local production, and ensure fair pricing for both producers and consumers in the confectionery industry.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.