Saudi Arabia Bus Market Outlook to 2030

Region:Middle East

Author(s):Sanjeev

Product Code:KROD4782

November 2024

93

About the Report

Saudi Arabia Bus Market Overview

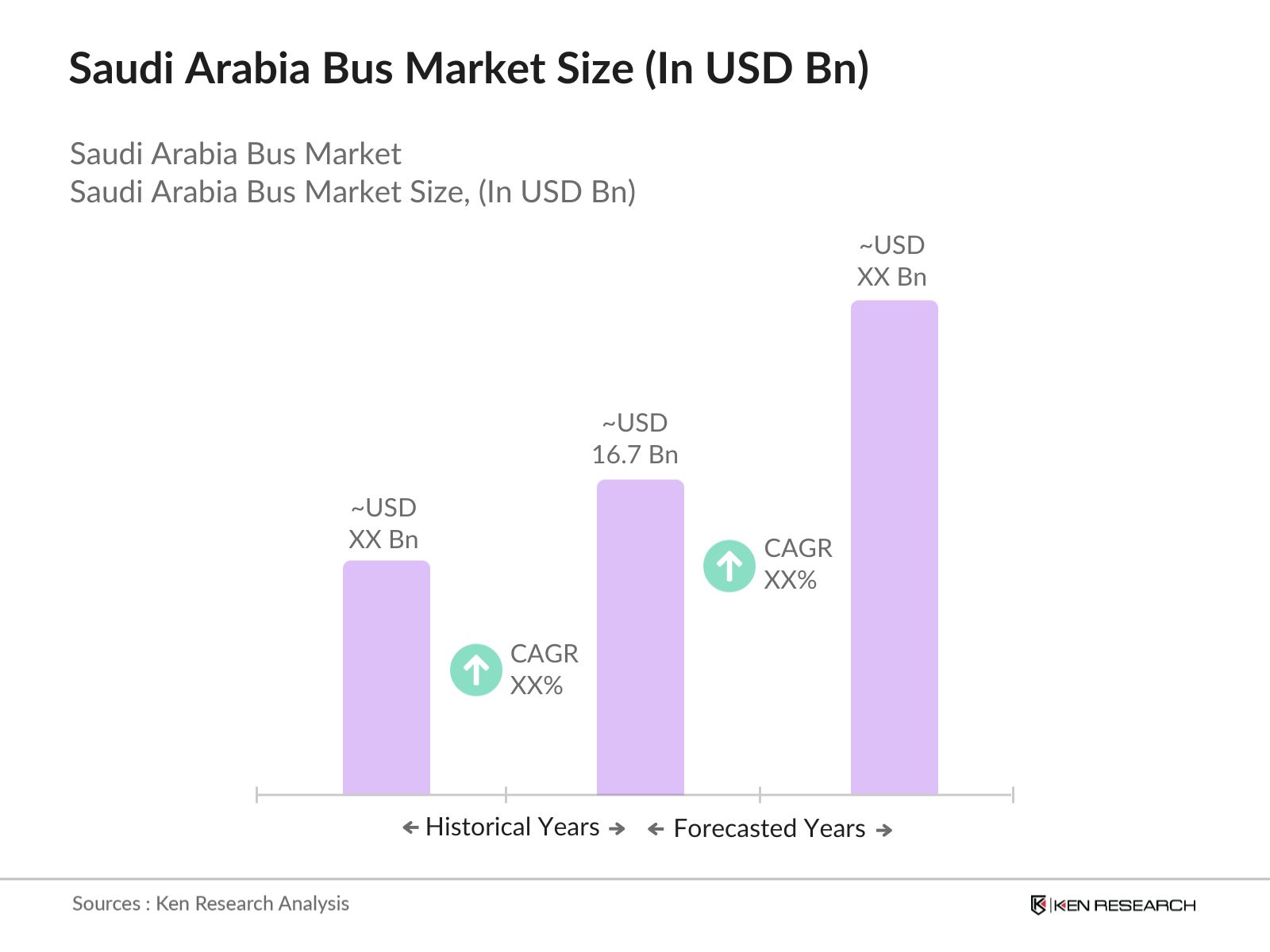

- The Saudi Arabia bus market is valued at USD 16.7 billion, driven by increasing demand for public transportation and government-led infrastructure projects as part of Vision 2030. The growth in urbanization, especially in major cities like Riyadh and Jeddah, has contributed to the need for efficient public transport systems, including buses. The demand for electric buses is also accelerating, backed by initiatives aimed at reducing the countrys carbon footprint and supporting green mobility.

- Dominant regions in the Saudi Arabia bus market include Riyadh, Jeddah, and the Eastern Province. Riyadh leads the market due to its population density, government investments in public transport systems, and ongoing infrastructure projects. Jeddah and the Eastern Province follow closely due to their economic importance and large-scale industrial developments that increase the need for intercity and intra-city transport options.

- Saudi Arabias Vision 2030 outlines ambitious transportation goals, including expanding the share of public transport in urban areas to 20% by 2030. The government is working toward electrifying 10% of the countrys bus fleet by 2025, as part of its broader strategy to meet green fleet standards and reduce carbon emissions. In addition to fleet expansion, the government has committed to improving public transport accessibility across all major cities, reducing traffic congestion, and supporting the adoption of low-emission vehicles.

Saudi Arabia Bus Market Segmentation

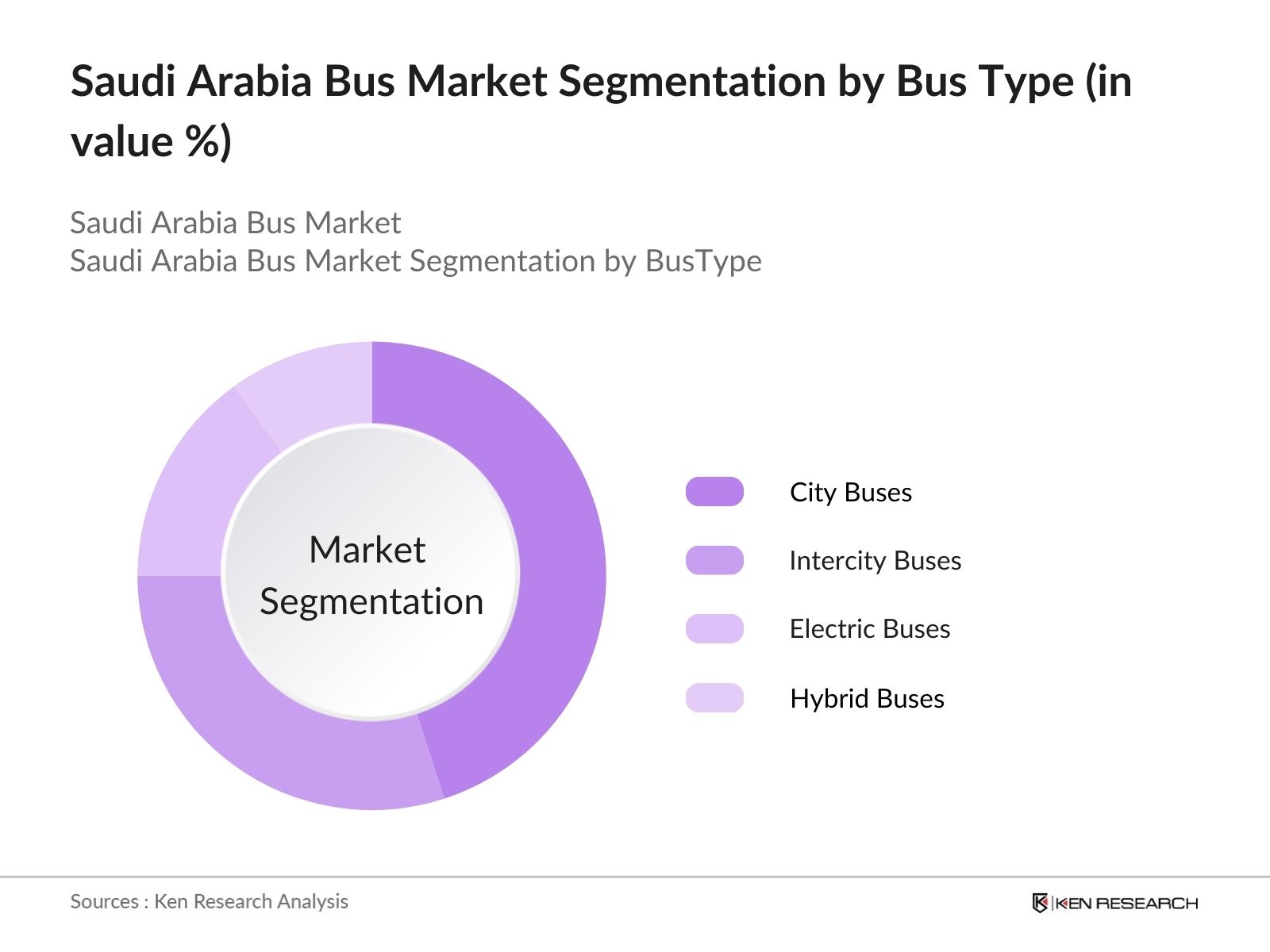

- By Bus Type: The market is segmented by type into city buses, intercity buses, electric buses, and hybrid buses. Recently, city buses held a dominant market share due to the surge in demand for public transportation in urban areas. Government initiatives focusing on improving public transport infrastructure in cities like Riyadh and Jeddah have bolstered the demand for city buses. Additionally, the push toward reducing congestion and the growing need for reliable, affordable transportation options for the working population have further propelled this segment.

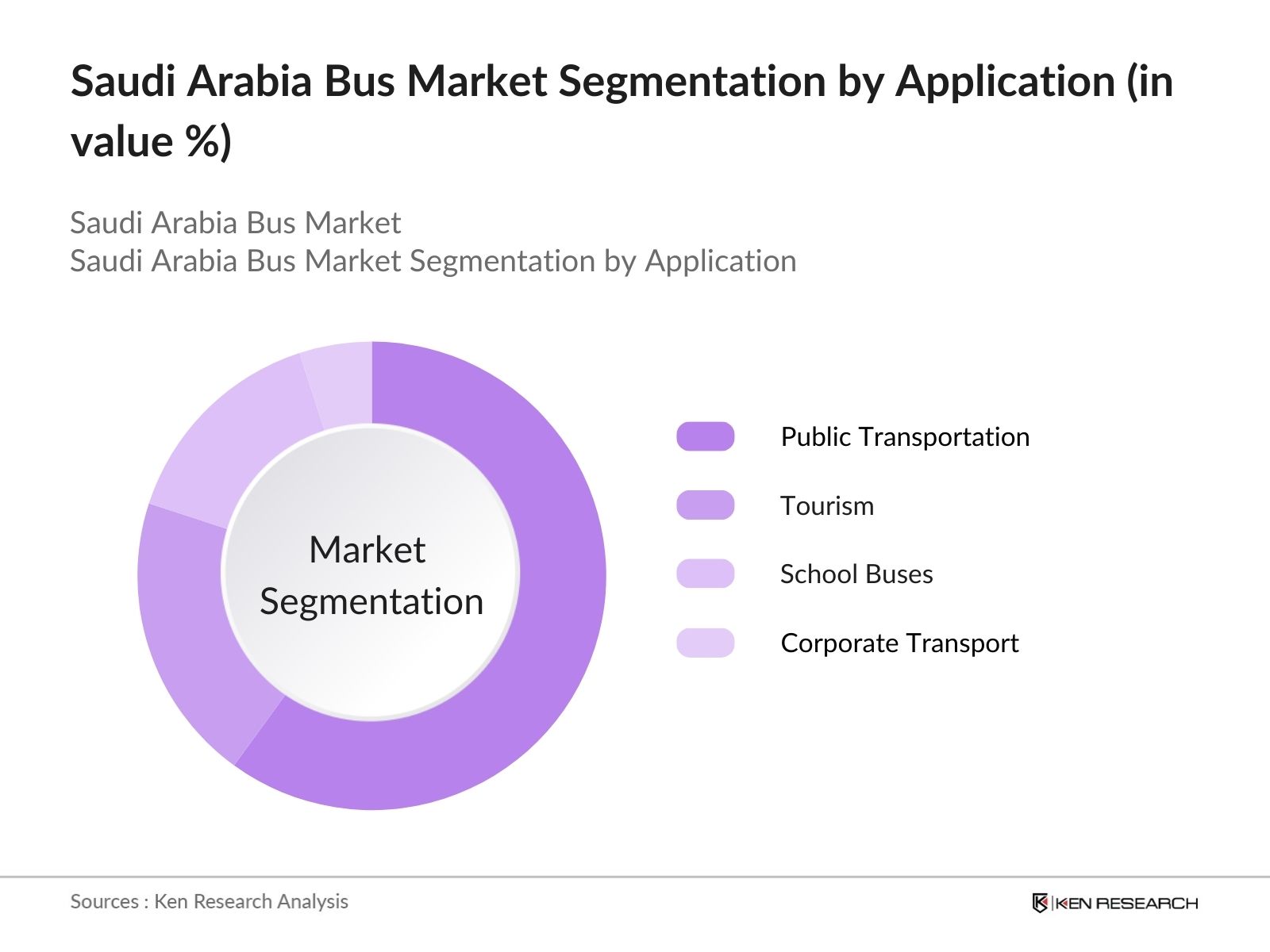

- By Application: The market is also segmented by application into public transportation, tourism, school buses, and corporate transport. Public transportation dominates the application segment, driven by the expansion of city bus networks and government funding in metro and bus rapid transit (BRT) systems. The increasing reliance on buses for commuting in major cities has bolstered this segment. Public transportation in Saudi Arabia is undergoing a transformation, with a focus on increasing accessibility, which has further boosted the growth of this sub-segment.

Saudi Arabia Bus Market Competitive Landscape

The Saudi Arabia bus market is dominated by several key players, both local and international. Leading companies in the market include Hafil Transport, SAPTCO, and global players like Volvo Buses and King Long. This consolidation highlights the influence of both local transport providers and international bus manufacturers in shaping the market. The presence of well-established local companies, alongside global manufacturers with advanced technologies, is critical for addressing the increasing demand for public transport.

|

Company Name |

Establishment Year |

Headquarters |

Fleet Size |

Market Presence |

Technology Adoption |

Strategic Initiatives |

Local Partnerships |

Sustainability Initiatives |

|

Hafil Transport |

1999 |

Jeddah, Saudi Arabia |

||||||

|

SAPTCO |

1979 |

Riyadh, Saudi Arabia |

||||||

|

Volvo Buses |

1968 |

Gothenburg, Sweden |

||||||

|

King Long |

1988 |

Xiamen, China |

||||||

|

Tata Motors |

1945 |

Mumbai, India |

Saudi Arabia Bus Industry Analysis

Market Growth Drivers

- Increasing Urbanization (Public Transit Expansion, Demand for Buses in Urban Areas): Saudi Arabia has experienced rapid urbanization, with over 84% of its population residing in urban areas by 2024, up from 82% in 2020, according to the World Bank. The government is prioritizing urban public transit systems to accommodate this shift, leading to an increased demand for buses in cities such as Riyadh and Jeddah. Riyadhs metro and bus network project, which is part of the citys $23 billion public transport plan, aims to have 1,000 buses operational by 2024. These efforts are aligned with Vision 2030 goals to reduce traffic congestion and provide efficient mass transit.

- Government Investments (Public Transport Projects, Vision 2030 Initiatives): The Saudi government has committed over $150 billion toward infrastructure projects under its Vision 2030 framework, including investments in public transport. In 2022, $3 billion was allocated to expanding bus fleets across major urban centers. As part of Vision 2030, the government aims to increase public transit usage from 2% to 20% by 2030, driving demand for buses, especially in growing urban centers. Projects such as the Riyadh Metro and Jeddahs public transport initiatives are directly contributing to this shift, with hundreds of buses expected to be integrated into these systems.

- Tourism Sector Growth (Demand for Intercity Buses, Transport Infrastructure): Saudi Arabia's tourism sector witnessed a boost in 2023, with 18 million international visitors, driven by the opening of NEOM and other tourism projects. This influx has created a growing demand for intercity bus services. In 2022, the tourism sector contributed nearly $42 billion to the Saudi economy, making the expansion of bus networks crucial for connecting tourist hubs such as Riyadh, Jeddah, and Makkah. The countrys growing intercity bus fleet is expected to serve not only tourists but also residents as the domestic tourism industry flourishes under the Vision 2030 objectives.

Market Challenges

- High Initial Cost of Electric Buses (Battery Costs, Infrastructure Investment): Despite the push for electric buses, their high upfront costs remain a challenge. The average price of an electric bus is about $300,000, more than twice the cost of a traditional diesel bus. The high cost is largely driven by battery technology, with batteries making up nearly 40% of the total bus cost. In addition, Saudi Arabia needs substantial infrastructure investment to build charging stations, with an estimated $4 billion needed by 2025 to meet the charging requirements of a growing fleet. These financial burdens are slowing widespread adoption, despite government incentives for green technology.

- Dependency on Imports (Component Supply Chain, Spare Parts Availability): Saudi Arabia heavily depends on imported buses and bus components, which has created challenges in maintaining a steady supply of vehicles and parts. In 2023, nearly 90% of buses were imported, primarily from China and Europe, making the market vulnerable to international supply chain disruptions. The global semiconductor shortage has exacerbated delays in the delivery of electric buses. Additionally, the reliance on foreign spare parts limits the local markets ability to maintain and repair bus fleets promptly, which is further complicated by the lack of local manufacturing capabilities for critical components.

Saudi Arabia Bus Market Future Outlook

Over the next five years, the Saudi Arabia bus market is expected to witness substantial growth, driven by government-backed transportation projects, technological advancements in electric and hybrid buses, and the increasing demand for efficient public transport systems. With Vision 2030 emphasizing the need for green and sustainable transport solutions, the adoption of electric buses is set to increase . Infrastructure improvements, such as the expansion of bus rapid transit (BRT) systems, will also play a key role in shaping the future landscape of the market.

Market Opportunities

- Technological Advancements (Telematics, Smart Bus Technologies): The introduction of telematics and smart bus technologies presents an opportunity to enhance the operational efficiency of bus fleets in Saudi Arabia. In 2023, the government initiated a pilot program for integrating telematics in over 500 public buses in Riyadh, allowing for real-time monitoring, route optimization, and predictive maintenance. By leveraging these technologies, bus operators can reduce downtime and maintenance costs while improving passenger experience. The smart bus market is expected to expand as part of the Vision 2030 digital transformation goals, which aim to modernize the public transport sector.

- Infrastructure Development (Bus Rapid Transit Systems, Charging Stations for EV Buses): Saudi Arabia is actively investing in the development of Bus Rapid Transit (BRT) systems in major cities. Riyadhs BRT system, expected to be operational by 2025, will feature 34 stations, and is designed to transport over 500,000 passengers daily. Additionally, the country plans to deploy over 2,000 electric vehicle charging stations by 2025, facilitating the growth of electric bus fleets. These infrastructure developments are part of the government's broader strategy to modernize the transport sector, create jobs, and support the countrys carbon reduction targets.

Scope of the Report

|

By Bus Type |

|

|

|

By Application |

Public Transportation Tourism, School Buses Corporate and Private Transport |

|

|

By Fuel Type |

Diesel Buses Electric Buses Hybrid Buses CNG Buses |

|

|

By Seating Capacity |

Up to 30 Seats 3150 Seats Above 50 Seats |

|

|

By Region |

North East West South |

Products

Key Target Audience

Public Transport Operators

Bus Fleet Owners

Government and Regulatory Bodies (Ministry of Transport, Saudi Public Transport Authority)

Bus Manufacturers

Banks and Financial Institutes

Private Transport Providers

Tourism Agencies

School Transportation Providers

Investment and Venture Capitalist Firms

Companies

Saudi Arabia Bus Market Major Players

Hafil Transport

SAPTCO (Saudi Public Transport Company)

King Long

Volvo Buses

MAN Truck & Bus

Yutong Bus

Tata Motors

Ashok Leyland

Scania

Zhongtong Bus

Mercedes-Benz Buses

IVECO

Isuzu Motors

Daewoo Bus

Hyundai Motors

Table of Contents

1. Saudi Arabia Bus Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Market Penetration, Fleet Expansion, Adoption of EV Buses)

1.4. Market Segmentation Overview

2. Saudi Arabia Bus Market Size (In SAR Mn)

2.1. Historical Market Size (Fleet Size, Bus Sales Volume)

2.2. Year-On-Year Growth Analysis (Revenue Growth, Fleet Growth)

2.3. Key Market Developments and Milestones (Bus Electrification, Public Transport Initiatives)

3. Saudi Arabia Bus Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Urbanization (Public Transit Expansion, Demand for Buses in Urban Areas)

3.1.2. Government Investments (Public Transport Projects, Vision 2030 Initiatives)

3.1.3. Tourism Sector Growth (Demand for Intercity Buses, Transport Infrastructure)

3.1.4. Adoption of Electric and Hybrid Buses (Regulatory Push for Green Transport)

3.2. Market Challenges

3.2.1. High Initial Cost of Electric Buses (Battery Costs, Infrastructure Investment)

3.2.2. Dependency on Imports (Component Supply Chain, Spare Parts Availability)

3.2.3. Maintenance and After-Sales Support (Lack of Skilled Workforce, Service Infrastructure)

3.3. Opportunities

3.3.1. Technological Advancements (Telematics, Smart Bus Technologies)

3.3.2. Infrastructure Development (Bus Rapid Transit Systems, Charging Stations for EV Buses)

3.3.3. Private Sector Participation (Public-Private Partnerships, Ride-Hailing Services Integration)

3.4. Trends

3.4.1. Growth in Electric Bus Segment (Battery Innovation, Charging Infrastructure)

3.4.2. Integration of Smart Mobility Solutions (Digital Ticketing, Route Optimization)

3.4.3. Rising Demand for Intercity and Luxury Coaches (Tourism, High-Income Population Demand)

3.5. Government Regulation

3.5.1. Vision 2030 Transportation Goals (Public Transport Targets, Green Fleet Standards)

3.5.2. Emission Reduction Policies (Adoption of EV Buses, Pollution Control Measures)

3.5.3. Public-Private Partnerships in Transport (Incentives for Private Bus Operators)

3.5.4. Road Safety and Transport Standards (Safety Certifications, Bus Licensing)

3.6. SWOT Analysis (Strengths: Growing Tourism; Weaknesses: Infrastructure Gaps; Opportunities: Public Transport Funding; Threats: Global Supply Chain Disruptions)

3.7. Stakeholder Ecosystem (Government Bodies, Manufacturers, Service Providers, Public-Private Partnerships)

3.8. Porters Five Forces (Supplier Power, Buyer Power, Threat of Substitution, Industry Rivalry, Barriers to Entry)

3.9. Competitive Landscape (Local and International Bus Manufacturers, Emerging Players)

4. Saudi Arabia Bus Market Segmentation

4.1. By Type (In Value %)

4.1.1. City Buses

4.1.2. Intercity Buses

4.1.3. Electric Buses

4.1.4. Hybrid Buses

4.2. By Application (In Value %)

4.2.1. Public Transportation

4.2.2. Tourism

4.2.3. School Buses

4.2.4. Corporate and Private Transport

4.3. By Fuel Type (In Value %)

4.3.1. Diesel Buses

4.3.2. Electric Buses

4.3.3. Hybrid Buses

4.3.4. CNG Buses

4.4. By Seating Capacity (In Value %)

4.4.1. Up to 30 Seats

4.4.2. 3150 Seats

4.4.3. Above 50 Seats

4.5. By Region (In Value %)

4.5.1. North

4.5.2. West

4.5.3. East

4.5.4. South

5. Saudi Arabia Bus Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Hafil Transport

5.1.2. SAPTCO (Saudi Public Transport Company)

5.1.3. King Long

5.1.4. MAN Truck & Bus

5.1.5. Yutong Bus

5.1.6. Volvo Buses

5.1.7. Tata Motors

5.1.8. Ashok Leyland

5.1.9. Scania

5.1.10. Zhongtong Bus

5.1.11. Mercedes-Benz Buses

5.1.12. IVECO

5.1.13. Isuzu Motors

5.1.14. Daewoo Bus

5.1.15. Hyundai Motors

5.2. Cross Comparison Parameters (Fleet Size, Market Presence, Revenue, Manufacturing Capacity, Local Partnerships, Product Innovation, Technology Adoption, Cost Competitiveness)

5.3. Market Share Analysis (By Company, By Segment)

5.4. Strategic Initiatives (Product Launches, Green Initiatives, Service Network Expansion)

5.5. Mergers and Acquisitions (Local and Global Deals)

5.6. Investment Analysis (Domestic and International Investments in Fleet Expansion)

5.7. Venture Capital Funding (For Startups in EV Bus Space)

5.8. Government Grants (Subsidies for Electric Buses)

5.9. Private Equity Investments (Investments in Bus Manufacturing and Infrastructure)

6. Saudi Arabia Bus Market Regulatory Framework

6.1. Environmental Standards (Fuel Emission Norms, Green Transport Policies)

6.2. Compliance Requirements (Safety Regulations, Licensing and Certification)

6.3. Certification Processes (Manufacturing Standards, Import Regulations)

7. Saudi Arabia Bus Market Future Size (In SAR Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (EV Adoption, Government Investments, Tourism Growth)

8. Saudi Arabia Bus Market Future Segmentation

8.1. By Type (In Value %)

8.2. By Application (In Value %)

8.3. By Fuel Type (In Value %)

8.4. By Seating Capacity (In Value %)

8.5. By Region (In Value %)

9. Saudi Arabia Bus Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis (Public Sector, Private Sector, Tourism)

9.3. Marketing Initiatives (B2B Campaigns, Public Awareness Programs)

9.4. White Space Opportunity Analysis (EV Buses, Smart Bus Infrastructure)

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the Saudi Arabia Bus Market. Extensive desk research, including the use of secondary and proprietary databases, helps to identify the critical variables influencing market dynamics.

Step 2: Market Analysis and Construction

In this phase, we analyze historical data pertaining to the Saudi Arabia bus market, including market penetration and fleet size statistics. We assess the ratio of buses to population in major cities and the resulting revenue generation to evaluate the markets performance.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through consultations with industry experts, including bus manufacturers, fleet operators, and government authorities. These consultations provide valuable insights into operational and financial challenges, which help in refining market data.

Step 4: Research Synthesis and Final Output

The final phase includes direct engagement with multiple bus manufacturers and public transport authorities to verify data accuracy. Insights from these interactions are used to validate the revenue estimates derived from the bottom-up approach, ensuring a comprehensive analysis of the market.

Frequently Asked Questions

1. How big is the Saudi Arabia bus market?

The Saudi Arabia bus market is valued at USD 16.7 billion, driven by the increasing demand for public transportation and government initiatives focused on improving infrastructure.

2. What are the challenges in the Saudi Arabia bus market?

Challenges in Saudi Arabia bus market include the high initial cost of electric buses, dependency on imports for key components, and the lack of sufficient maintenance infrastructure to support an expanding bus fleet.

3. Who are the major players in the Saudi Arabia bus market?

Key players in the Saudi Arabia bus market include Hafil Transport, SAPTCO, King Long, Volvo Buses, and Tata Motors. These companies dominate the market due to their extensive fleet sizes, government contracts, and investments in electric bus technologies.

4. What are the growth drivers of the Saudi Arabia bus market?

The Saudi Arabia bus market is driven by the expansion of public transport systems, government support for sustainable mobility under Vision 2030, and the growing demand for green transportation solutions, such as electric and hybrid buses.

5. What is the future outlook for the Saudi Arabia bus market?

The Saudi Arabia bus market is expected to grow over the next five years, with increased government spending on public transport infrastructure and the adoption of electric buses as part of environmental sustainability goals.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.