Saudi Arabia Data Center Market Outlook 2030

Region:Middle East

Author(s):Shivani Mehra

Product Code:KROD1100

November 2024

86

About the Report

Saudi Arabia Data Center Market Overview

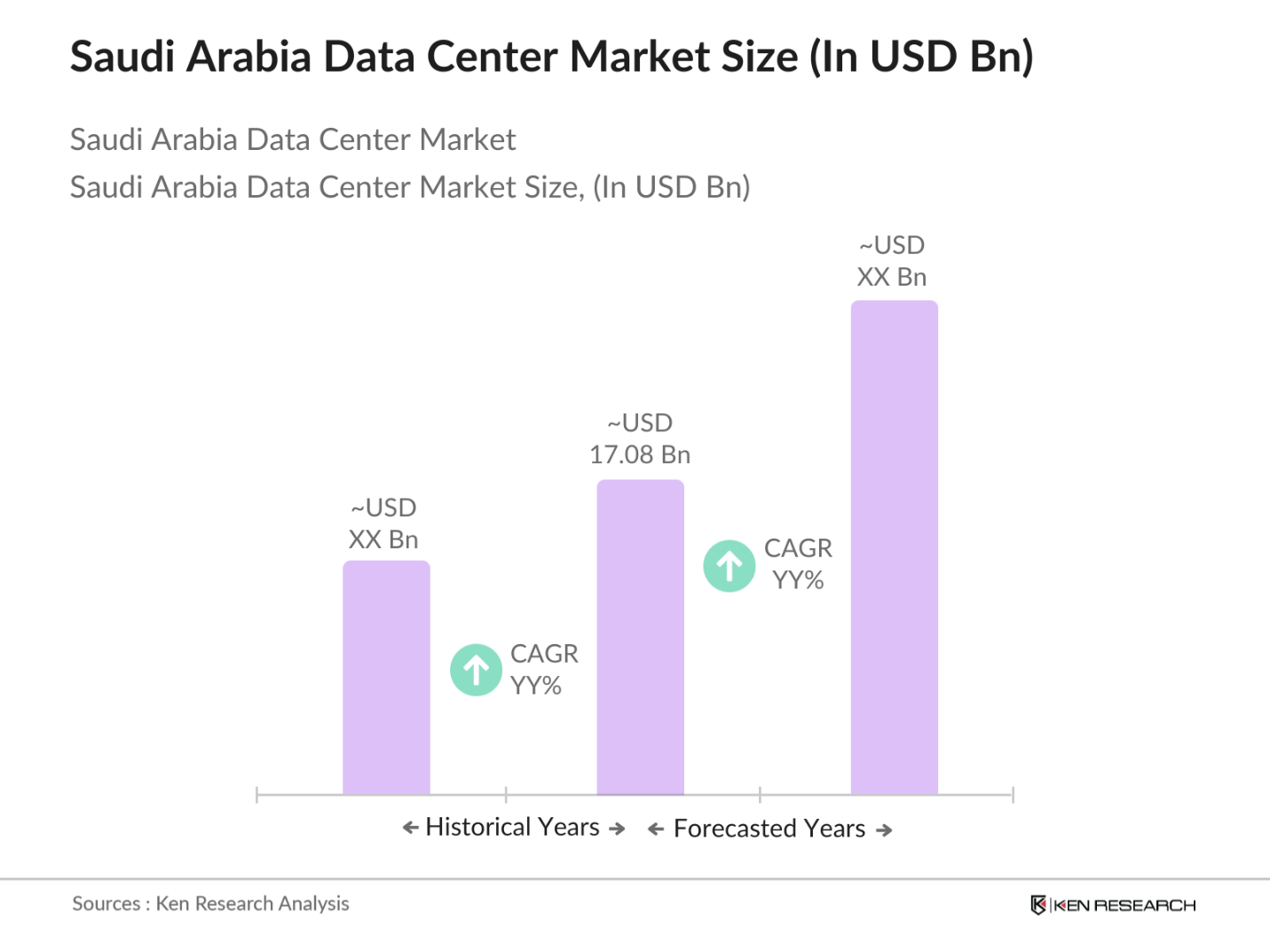

- The Saudi Arabia Data Center market reached a valuation of approximately USD 17.08 billion. This growth is propelled by rapid digital transformation, increasing adoption of cloud services, and investments in 5G technology. Saudi Arabia's initiative is a driving factor, encouraging data localization and stringent cybersecurity policies that prioritize local data storage. These advancements underscore the growing demand for data centers, bolstering infrastructure development and investment in next-generation data centers to cater to expanding data traffic.

- Riyadh and Jeddah dominate Saudi Arabia's data center landscape due to their robust ICT infrastructure and strategic importance within the region. Riyadh, as the capital, hosts the majority of government-backed data center projects, driven by regulatory frameworks favoring data localization. Jeddah, a major port city, serves as a hub for international businesses and logistical support, making it a key area for data center investments aimed at enhancing connectivity and data storage capabilities.

- The National Data Management Office (NDMO) plays a pivotal role in establishing data governance and enhancing data management practices across Saudi Arabia. The NDMO implements policies that promote data localization and ensure compliance with data sovereignty regulations. As part of its initiatives, the office has developed frameworks for data sharing and usage that encourage businesses to invest in local data centers. By 2023, the NDMO indicated that compliance with these regulations could drive significant investments in domestic data infrastructure, thereby bolstering the data center market and ensuring the secure management of sensitive information.

Saudi Arabia Data Center Market Segmentation

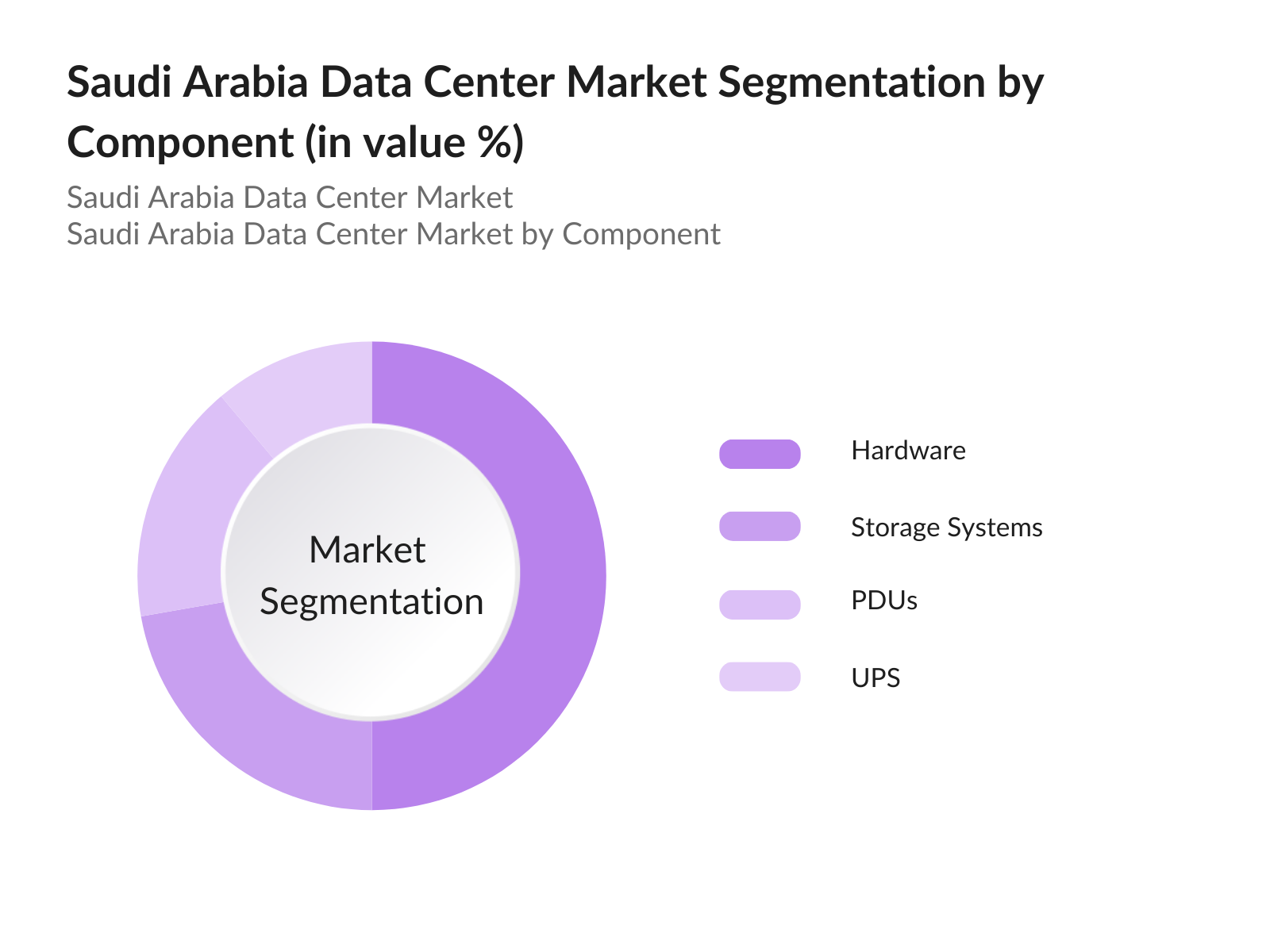

By Component: The Saudi Arabia's data center market is segmented by component into Hardware, Software, and Services. Hardware holds the dominant position due to essential components such as servers, storage systems, and power management equipment. Servers are crucial for managing and processing data, making them a priority for infrastructure investment. Power distribution units (PDUs) and uninterruptible power supply (UPS) systems support uptime and reliability, contributing to the hardware segment's prominence.

By Data Center Type: The Segmentation by type includes Colocation, On-Premise, Hyperscale, and Edge data centers. Colocation facilities currently lead this segmentation, given their cost-effectiveness for businesses seeking reliable data storage without extensive capital expenditure. Colocation centers provide shared space for multiple companies, often including high-security measures and redundant power systems to maintain operational efficiency.

Saudi Arabia Data Center Market Competitive Landscape

The Saudi Arabia data center market is marked by a few major players who dominate through extensive investments, technological capabilities, and strategic partnerships with government entities.

Saudi Arabia Data Center Market Analysis

Market Growth Drivers

- 5G Deployment: The extensive rollout of 5G technology in Saudi Arabia is a pivotal growth driver for the data center market. As of 2023, the Kingdom has established over 1,000 5G towers, significantly enhancing mobile connectivity. The telecommunications market is projected to reach approximately $14.5 billion by 2025, driven largely by the increased mobile data consumption resulting from 5G. The demand for faster and more reliable internet services necessitates robust data center capabilities to process and store vast amounts of data efficiently.

- IoT Expansion: The rapid expansion of the Internet of Things (IoT) in Saudi Arabia is accelerating the growth of the data center market. As of 2023, there are an estimated 16 million connected IoT devices in the Kingdom, with plans to scale this number to 50 million by 2025. The National IoT Strategy underlines the government's commitment to enhancing connectivity across sectors such as healthcare, transportation, and energy. Investments in IoT technologies are projected to be around $100 billion, further driving the need for data centers to manage the increasing volume of data generated by these connected devices.

- Digital Transformation Initiatives: Saudi Arabia's ongoing digital transformation initiatives are a crucial driver for the data center market's growth. The government has allocated over $10 billion for enhancing digital infrastructure, which is vital for service delivery across public and private sectors. In 2023, many Saudi enterprises reported being engaged in digital transformation initiatives, which rely heavily on cloud services and data management systems. The digital economy, contributing significantly to the GDP, underscores the importance of data centers in supporting this transition and ensuring that organizations can efficiently store, process, and analyze data.

Market Challenges:

- High Operational Costs: The operational costs of running data centers in Saudi Arabia pose a significant challenge. As of 2023, the average electricity cost for commercial use was reported at SAR 0.18 per kWh, making energy consumption a critical factor for data center operators. Additionally, high initial investments in advanced cooling technologies, essential for managing heat generated by data servers, further elevate operational expenses. The International Energy Agency estimates that data centers in the Middle East consume around 3.3 terawatt-hours of electricity annually, emphasizing the need for cost-effective solutions to maintain profitability in this sector.

- Limited Skilled Workforce: The shortage of skilled professionals in the IT sector is a considerable challenge for the data center market in Saudi Arabia. As of 2023, the Saudi Ministry of Human Resources reported that approximately 5,000 IT positions remain unfilled, particularly in specialized areas such as cybersecurity, cloud computing, and data management. This skills gap hampers the ability of data centers to operate efficiently and securely. To address this issue, the government has initiated training programs, investing SAR 1.5 billion to enhance workforce capabilities, yet the challenge remains pressing as demand continues to outpace supply.

Saudi Arabia Data Center Market Future Outlook

Over the coming years, the Saudi Arabian data center market is anticipated to continue its upward trajectory, driven, technological advancements in data processing, and a significant push for data sovereignty. With growing demand for edge computing and cloud-based solutions, the market will see more investments from both public and private sectors to support large-scale projects like NEOM and other smart city developments.

Market Opportunities:

- Edge Computing Expansion: The expansion of edge computing presents a significant opportunity for the data center market in Saudi Arabia. As of 2023, enterprises increasingly recognize the need for localized data processing to reduce latency and enhance service delivery. Investments in edge computing solutions are projected to reach SAR 1 billion, driven by the demand for real-time data analytics in sectors such as transportation, healthcare, and smart cities. This shift allows data centers to develop specialized facilities closer to users, improving efficiency and responsiveness while catering to the growing IoT ecosystem that requires rapid data processing capabilities.

- Smart City Development: Saudi Arabia's commitment to developing smart cities, such as NEOM and the Red Sea Project, represents a crucial opportunity for data centers. The government has allocated SAR 500 billion for these initiatives, focusing on integrating advanced technologies such as AI, IoT, and big data. By 2023, there were plans to establish 20 smart cities, each requiring extensive data infrastructure to support interconnected systems and real-time data processing. This ambitious development not only enhances the demand for data centers but also encourages investment in innovative data management solutions tailored for urban environments.

Scope of the Report

|

By Component |

Hardware (Servers, Networking Equipment, Power Systems) Software (DCIM, Virtualization) Services (Managed Infrastructure, Support, Hosting) |

|

By Type |

On-Premise Hyperscale Edge Colocation |

|

By Rack Density |

<10kW 10-19kW 20-29kW 30-39kW 40-49kW >50kW |

|

By End-Use Vertical |

BFSI Government IT & Telecom Healthcare Manufacturing |

|

By Region |

North-East Midwest West Coast Southern States |

Products

Key Target Audience

Government and Regulatory Bodies (Saudi Data and Artificial Intelligence Authority, National Cybersecurity Authority)

Telecom and IT Service Providers

Cloud Service Providers

Infrastructure and Real Estate Developers

Data Security Providers

Private Equity and Venture Capital Firms

Financial Institutions and Banks

Technology and IT Equipment Manufacturers

Companies

Players Mention in the Report

Amazon Web Services (AWS)

Google Cloud

Microsoft Azure

Saudi Telecom Company (STC)

IBM

Oracle Corporation

Alibaba Cloud

Equinix

NTT Data Corporation

Mobily

Etisalat

Tencent Cloud

Digital Realty

TAWAL

Vantage Data Centers

Table of Contents

01. Saudi Arabia Data Center Market Overview

Definition and Scope

Market Taxonomy

Market Growth Rate

Market Segmentation Overview

02. Saudi Arabia Data Center Market Size

Historical Market Size (Revenue and Volume)

Year-on-Year Growth Analysis

Key Market Developments and Milestones

03. Saudi Arabia Data Center Market Dynamics

Market Drivers (5G Deployment, IoT Expansion, Digital Transformation Initiatives)

Market Challenges (High Operational Costs, Limited Skilled Workforce)

Market Opportunities (Edge Computing Expansion, Smart City Development)

Emerging Trends (Data Sovereignty, Data Localization Requirements)

04. Saudi Arabia Data Center Market Analysis

Porter's Five Forces Analysis

PESTLE Analysis

Key Stakeholder Ecosystem

Scope of the Report

(Tabular representation of segmentations as detailed below)

05. Saudi Arabia Data Center Market Segmentation

By Component:

Hardware (Servers, Networking, Power Distribution Units, UPS)

Software (DCIM, Virtualization)

Services (Managed Infrastructure, Hosting, Support Services)

By Type:

On-Premise, Hyperscale, Edge, Colocation

By Rack Density:

<10kW, 10-19kW, 20-29kW, 30-39kW, 40-49kW, >50kW

By End-Use Vertical:

BFSI, Government, IT & Telecom, Healthcare, Media, Manufacturing, Retail

By Tier Level:

Tier I, Tier II, Tier III, Tier IV

06. Saudi Arabia Data Center Market Competitive Landscape

Market Share Analysis (Top Companies by Revenue Share)

Detailed Company Profiles:

Amazon Web Services (AWS)

Google Cloud

Microsoft Azure

IBM Corporation

Alibaba Cloud

Saudi Telecom Company (STC)

Etisalat

Mobily

Equinix Inc.

Digital Realty

AT&T

Oracle Corporation

Tencent Cloud

NTT Data Corporation

TAWAL

Cross-Comparison Parameters (Headquarters, No. of Data Centers, Regional Presence, Service Offerings, Revenue Share, Customer Base Size, Technical Specifications, Market Positioning)

07. Saudi Arabia Data Center Market Regulatory Environment

Data Localization Laws (Saudi Data and Artificial Intelligence Authority (SDAIA) Guidelines)

Cybersecurity Standards (National Cybersecurity Authority Regulations)

Compliance Requirements for Critical Sectors (Finance, Government Services)

Environmental and Efficiency Standards (Green Data Center Certifications)

08. Saudi Arabia Data Center Market Key Performance Indicators

Power Usage Effectiveness (PUE)

Rack Utilization Rate

Network Latency Benchmarks

Availability and Redundancy Metrics (Uptime Institute Standards)

09. Saudi Arabia Data Center Future Market Size

Future Market Size Projections

Key Factors Driving Future Market Growth

10. Saudi Arabia Data Center Market Analyst Recommendations

TAM/SAM/SOM Analysis

Strategic Initiatives for Investment

Emerging White Space Opportunities

Recommendations for International Market Entry

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial step involved mapping key market stakeholders in the Saudi Arabian data center industry, leveraging proprietary and secondary databases to collect comprehensive data, with a focus on factors like 5G deployment, regulatory influences, and data localization.

Step 2: Market Analysis and Construction

Historical market data was collated and analyzed, focusing on revenue growth, market volume, and the rate of data center expansion. This analysis provided insights into the role of technological adoption and policy frameworks shaping market trends.

Step 3: Hypothesis Validation and Expert Consultation

Interviews with industry professionals and technology experts validated market hypotheses, offering nuanced perspectives on operational practices and investment patterns. Insights from these consultations enriched the analysis, particularly in high-demand areas like edge computing and colocation services.

Step 4: Research Synthesis and Final Output

The final analysis incorporated a detailed synthesis of data from leading data center operators in Saudi Arabia, including investment strategies, technological adoptions, and infrastructure expansion plans, ensuring a robust and accurate market report.

Frequently Asked Questions

01. How big is the Saudi Arabia Data Center Market?

The Saudi Arabia data center market is valued at USD 17.08 billion, propelled by government support for data localization and a surge in cloud service adoption across sectors.

02. What are the main drivers in the Saudi Arabia Data Center Market?

Key drivers include government-backed digital transformation initiatives, widespread 5G deployment, and an increase in IoT-connected devices, which together heighten the demand for robust data storage solutions.

03. Who are the major players in the Saudi Arabia Data Center Market?

The markets leading companies include Amazon Web Services, Google Cloud, Microsoft Azure, Saudi Telecom Company, and IBM, each bringing advanced data management and cloud computing capabilities to the region.

04. What challenges does the Saudi Arabia Data Center Market face?

Challenges include high energy costs, the need for skilled technical staff, and stringent data localization regulations, all of which impact operational efficiency and expansion capabilities.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.