Saudi Arabia Digital Media Market Outlook to 2030

Region:Saudi Arabia

Author(s):Sanjeev

Product Code:KROD4600

Region:Saudi Arabia

Author(s):Sanjeev

Product Code:KROD4600

November 2024

90

Listen to the audio summary

The Saudi Arabia digital media market is dominated by several key players that influence content creation, distribution, and digital advertising. These companies, both local and international, play a pivotal role in shaping the market landscape. Companies like Shahid (a local favorite), Netflix, YouTube, and STC Digital Media have established strong positions due to their ability to cater to local preferences, as well as their integration with global content networks.

|

Company Name |

Establishment Year |

Headquarters |

Market Reach |

Subscribers (M) |

Revenue (USD Bn) |

Local Content Ratio |

Ad Revenue (USD M) |

Partnerships |

Influence on Content Creation |

|

STC Digital Media |

1998 |

Riyadh |

|||||||

|

Netflix Saudi Arabia |

1997 |

Los Gatos, CA |

|||||||

|

Shahid (MBC Group) |

1991 |

Dubai |

|||||||

|

YouTube Saudi Arabia |

2005 |

San Bruno, CA |

|||||||

|

Twitter MENA |

2006 |

Dubai |

Over the next five years, Saudi Arabia's digital media market is expected to experience substantial growth, driven by continuous government efforts to support digital transformation, advancements in technology like 5G, and increased consumer demand for localized digital content. With a rising youth population, higher mobile internet penetration, and the diversification of digital media platforms, this market is poised to see significant development across OTT platforms, social media, and digital advertising. The country's ongoing investment in infrastructure, such as smart cities and enhanced digital services, will further accelerate the expansion of the digital media sector.

|

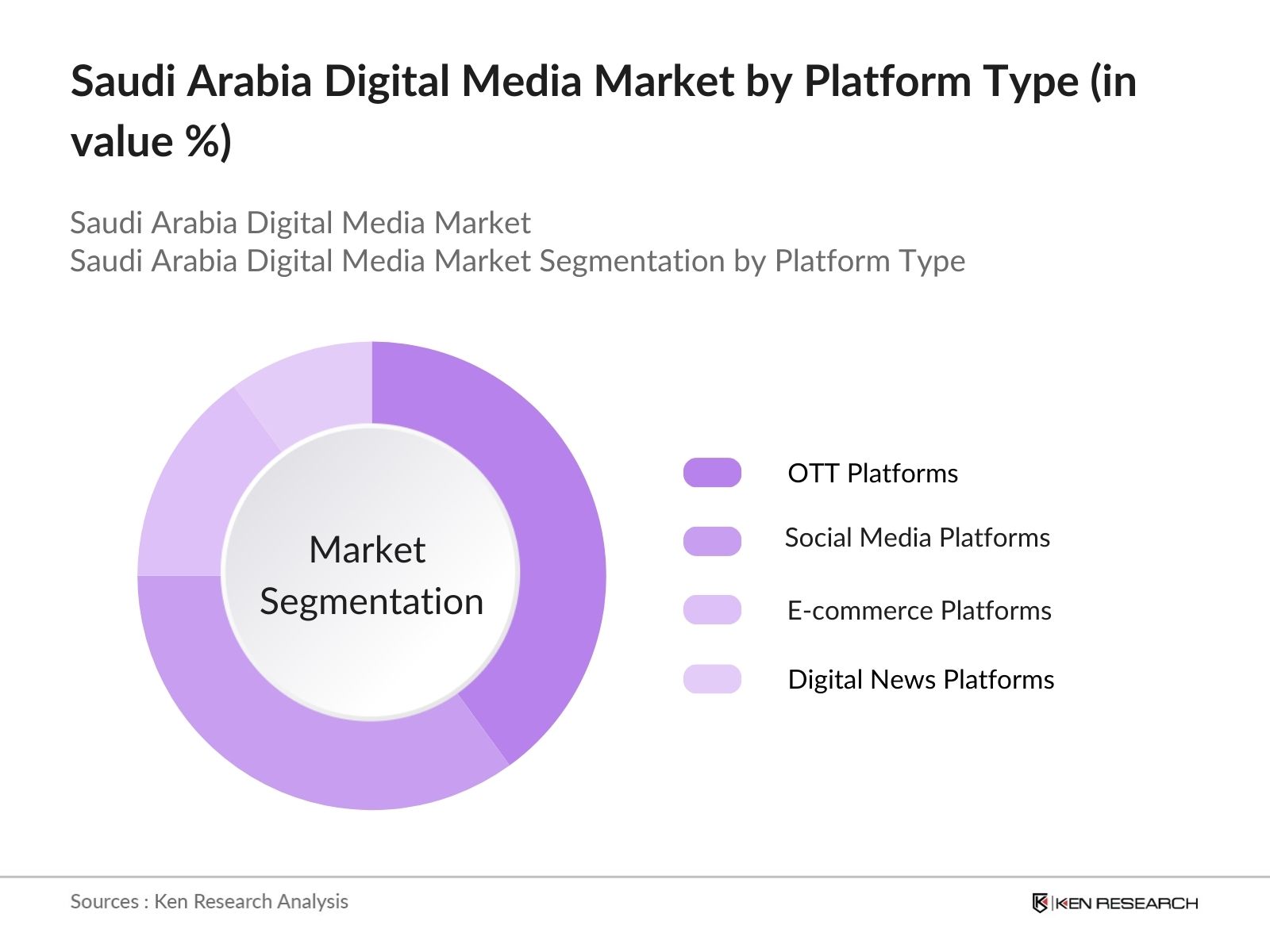

By Platform Type |

Over-the-Top (OTT) Platforms Social Media Platforms E-commerce Platforms Digital News Platforms |

|

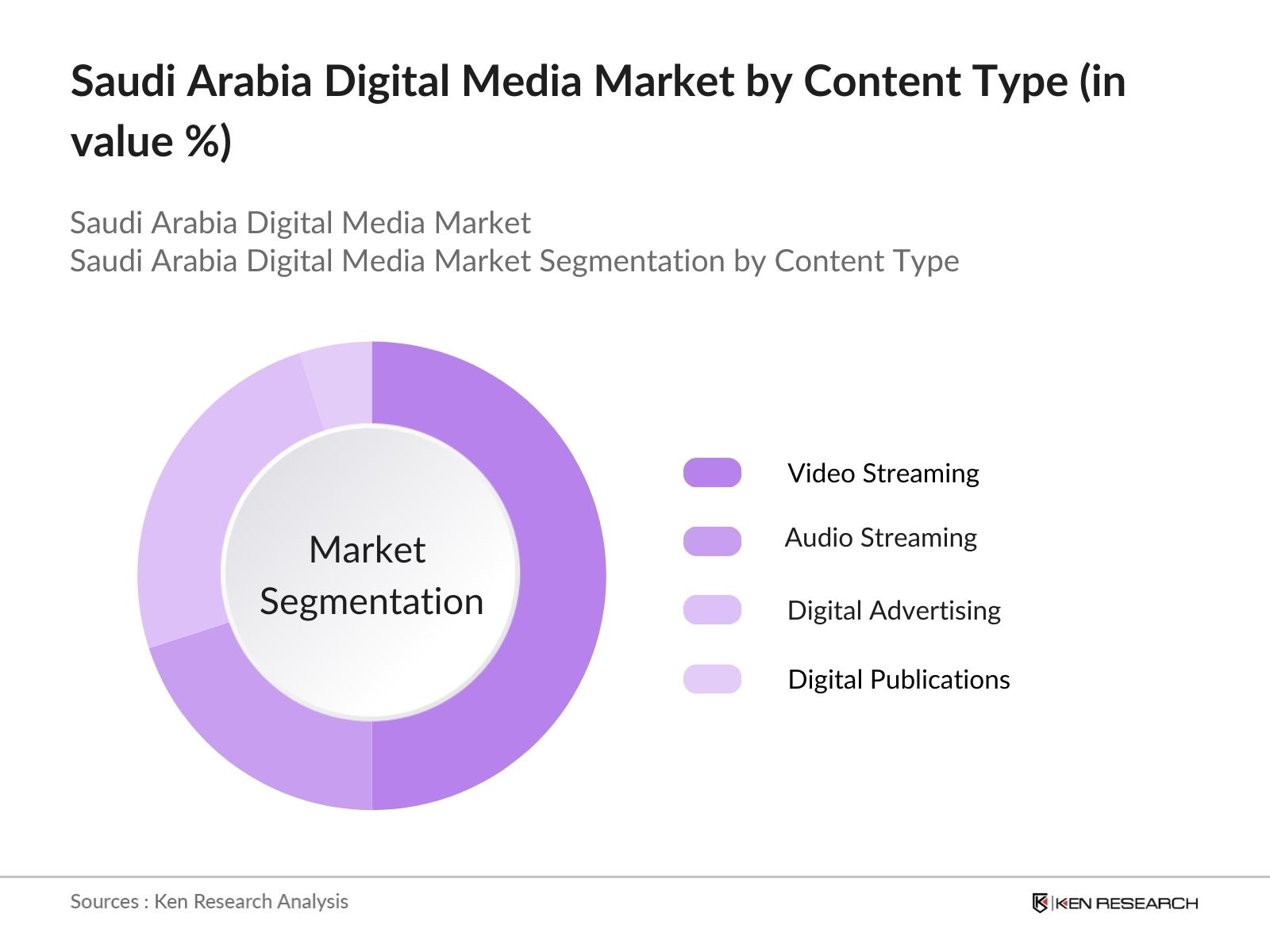

By Content Type |

Video Streaming Audio Streaming Digital Advertising E-books and Digital Publications |

|

By Revenue Model |

Subscription-Based Advertisement-Based Freemium |

|

By End-User |

Individual Consumers Enterprises and SMEs Educational Institutions Government Organizations |

|

By Region |

North East West South |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers (Saudi Arabias Vision 2030, Digital Transformation, Internet Penetration, Youth Population)

3.1.1 High Internet and Mobile Penetration

3.1.2 Growth in E-commerce and OTT Platforms

3.1.3 Shift Toward Digital Advertising

3.1.4 Government Support for Digital Initiatives

3.2 Market Challenges (Low Local Content Creation, Cultural Sensitivities, Limited Data Regulation Framework)

3.2.1 Limited Monetization of Digital Content

3.2.2 Data Privacy and Cybersecurity Concerns

3.2.3 Reliance on International Content Creators

3.3 Opportunities (Content Localization, 5G Rollout, Partnerships with Global Digital Platforms)

3.3.1 Growth in Arabic Content Creation

3.3.2 Expanding Usage of Social Media for Business

3.3.3 Increased Investment in Online Learning Platforms

3.4 Trends (Rise in Influencer Marketing, Short-form Content, Growth of Podcasting)

3.4.1 Increase in Consumption of Social Video Content

3.4.2 Expansion of Digital Advertising into Emerging Sectors

3.4.3 Integration of AI and Data Analytics in Digital Media

3.5 Government Regulation (Vision 2030 Policies, Local Content Quotas, Privacy Law Implementation)

3.5.1 Introduction of Digital Content Development Programs

3.5.2 Mandatory Local Content Quota for OTT Platforms

3.5.3 Cybersecurity Laws for Digital Platforms

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem (Content Creators, OTT Platforms, Digital Ad Agencies, Regulatory Bodies)

3.8 Porters Five Forces

3.9 Competition Ecosystem

4.1 By Platform Type (In Value %)

4.1.1 Over-the-Top (OTT) Platforms

4.1.2 Social Media Platforms

4.1.3 E-commerce Platforms

4.1.4 Digital News Platforms

4.2 By Content Type (In Value %)

4.2.1 Video Streaming

4.2.2 Audio Streaming

4.2.3 Digital Advertising

4.2.4 E-books and Digital Publications

4.3 By Revenue Model (In Value %)

4.3.1 Subscription-Based

4.3.2 Advertisement-Based

4.3.3 Freemium

4.4 By End-User (In Value %)

4.4.1 Individual Consumers

4.4.2 Enterprises and SMEs

4.4.3 Educational Institutions

4.4.4 Government Organizations

4.5 By Region (In Value %)

4.5.1 North

4.5.2 South

4.5.3 West

4.5.4 East

5.1 Detailed Profiles of Major Companies

5.1.1. STC Digital Media

5.1.2. Mobily

5.1.3. Shahid (MBC Group)

5.1.4. YouTube Saudi Arabia

5.1.5. Twitter MENA

5.1.6. Anghami

5.1.7. OSN Streaming

5.1.8. Starzplay

5.1.9. Noon

5.1.10. Souq (Amazon Saudi Arabia)

5.1.11. Saudi Research and Media Group

5.1.12. Rotana Digital Media

5.1.13. Snap Inc. (Saudi Arabia)

5.1.14. TikTok Saudi Arabia

5.1.15. Netflix Saudi Arabia

5.2 Cross Comparison Parameters (Revenue, Subscriber Base, Market Share, Digital Content Partnerships, Social Media Following, Localization Initiatives, Headquarter Locations, Strategic Investments)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers And Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 Digital Content Regulation

6.2 Compliance with Cultural Guidelines

6.3 Certification and Licensing for Digital Content Providers

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Platform Type (In Value %)

8.2 By Content Type (In Value %)

8.3 By Revenue Model (In Value %)

8.4 By End-User (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

In this initial phase, we map out all the key stakeholders within the Saudi Arabia digital media market ecosystem. This step involves conducting thorough desk research using secondary sources and proprietary databases to capture industry-level data. Key variables such as digital platform usage, subscriber data, and content consumption trends are identified to understand market dynamics.

This phase involves analyzing historical data to evaluate the market's performance. Factors like content localization, platform penetration, and revenue generated from digital media are examined. Additionally, the impact of digital advertising and the consumer shift toward streaming services are evaluated for accuracy and reliability.

Market hypotheses are developed and validated through interviews with industry experts. These consultations include key personnel from top digital media companies, telecommunications firms, and government bodies, ensuring that market insights are robust and accurate.

In the final step, we engage directly with digital media platform providers to collect detailed insights into their content strategies, user base, and revenue streams. This data is cross-referenced with our bottom-up market approach to ensure a comprehensive and validated analysis of the Saudi Arabia digital media market.

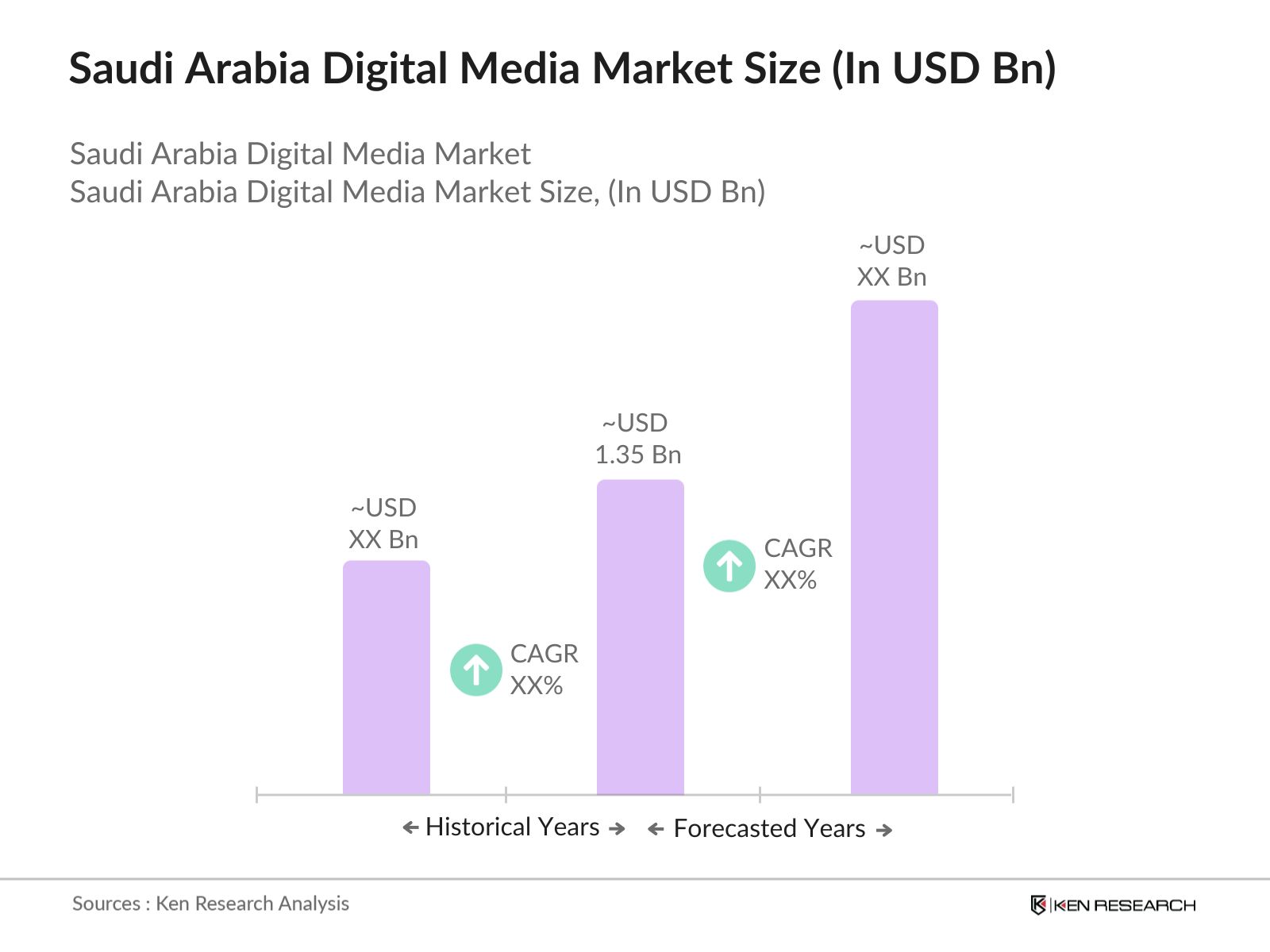

The Saudi Arabia digital media market is valued at USD 1.35 billion, driven by a combination of factors including high internet penetration, growing consumption of OTT content, and robust government support for digital transformation as part of Vision 2030.

Challenges in the Saudi Arabia digital media market include the need for greater content localization, data privacy concerns, and the limited monetization options for digital content creators. Cultural sensitivities also play a role in shaping content strategies for international platforms.

Key players in the Saudi Arabia digital media market include STC Digital Media, Shahid, YouTube Saudi Arabia, Netflix, and Twitter MENA. These companies dominate due to their strong content offerings, localized strategies, and large user bases.

Growth is driven by increasing internet and mobile penetration, the popularity of OTT platforms, and rising investments in digital advertising in the Saudi Arabia digital media market. Government initiatives under Vision 2030 are also propelling the market forward.

Key trends in the Saudi Arabia digital media market include the rise of influencer marketing, the adoption of short-form video content, and the expansion of digital advertising into new sectors such as e-commerce and education platforms.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.