Saudi Arabia Frozen and Retail Bakery Market Outlook to 2030

Region:Saudi Arabia

Author(s):Sanjeev

Product Code:KROD2580

Region:Saudi Arabia

Author(s):Sanjeev

Product Code:KROD2580

December 2024

94

Listen to the audio summary

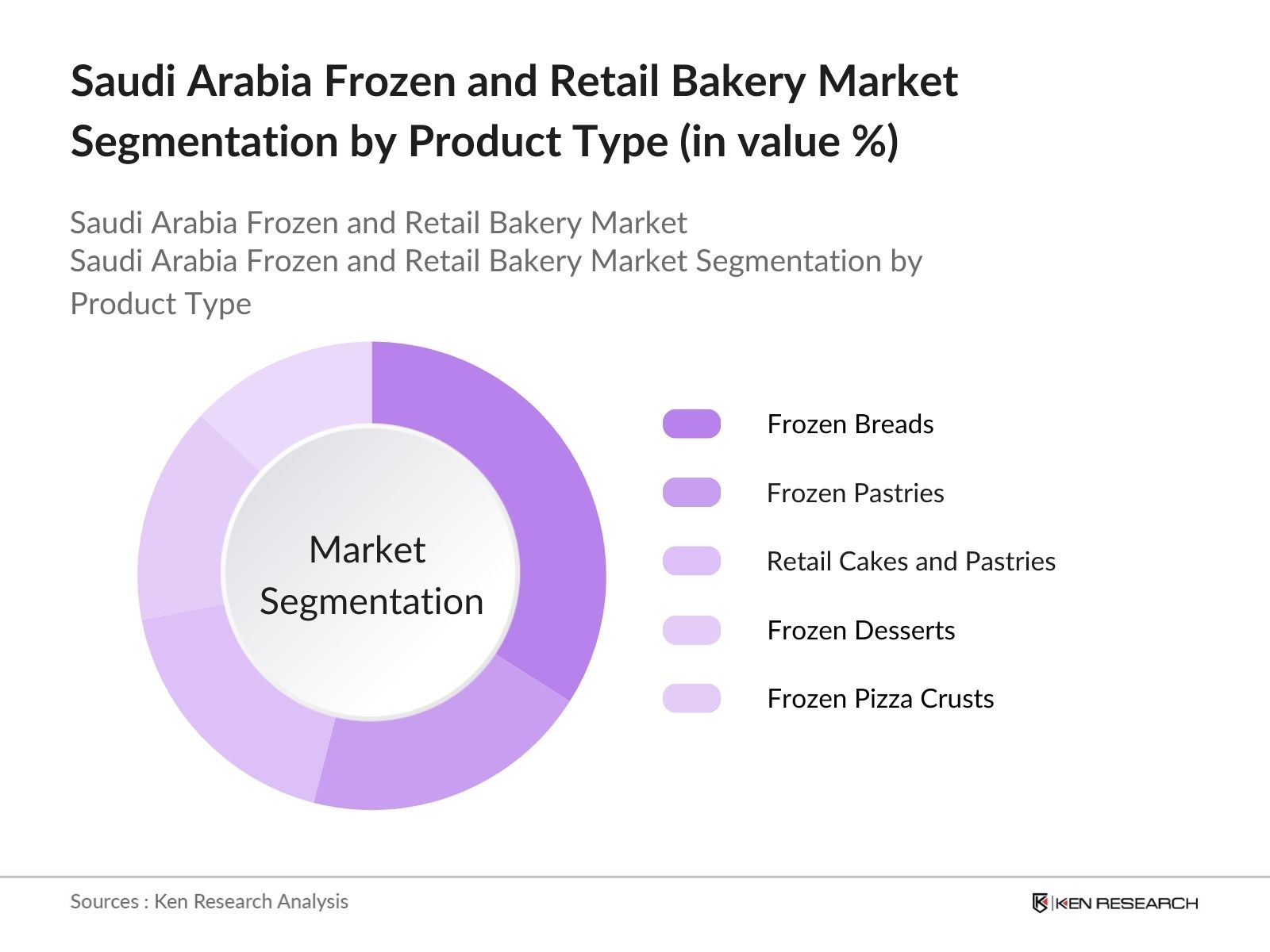

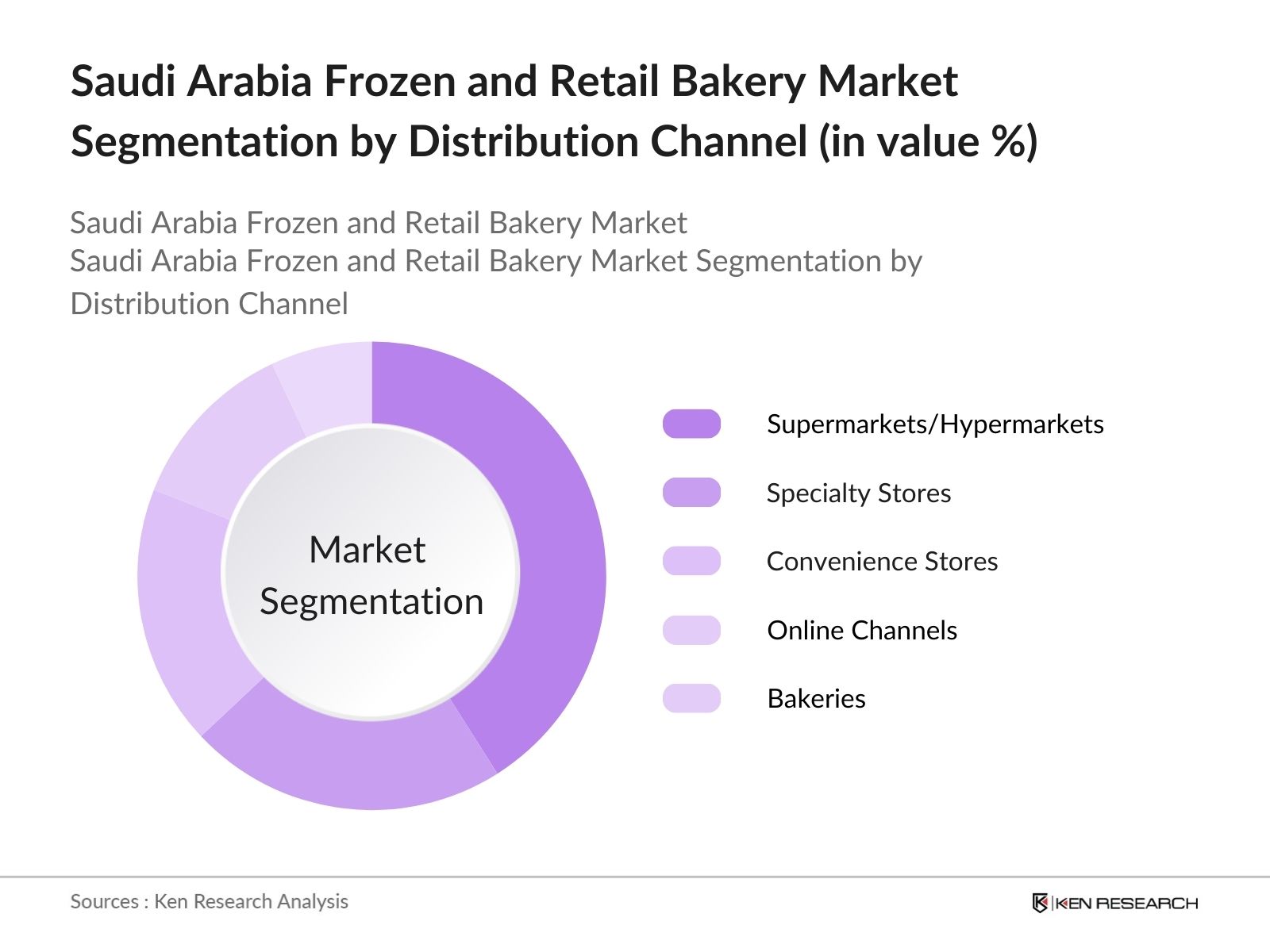

The Saudi bakery market is segmented by product type and by distribution channel.

The Saudi Arabia frozen and retail bakery market is characterized by a mix of local and international companies, each aiming to capture a significant market share through innovative product offerings and strategic distribution channels. Major players, such as Almarai and SADAFCO, lead the market due to their extensive distribution networks and robust brand recognition. The presence of both established domestic brands and multinational corporations highlights the competitive nature of the market, with players investing heavily in marketing and product innovation to retain customer loyalty.

The Saudi Arabia frozen and retail bakery market is expected to expand steadily over the coming years, driven by a continuous rise in consumer demand for convenient, ready-to-eat food options and a broader range of innovative product offerings. As the retail sector modernizes and consumer preferences shift towards health-conscious and diverse products, opportunities for premium and organic bakery items are anticipated to grow. Furthermore, advancements in food processing and storage technologies are likely to support this trend, ensuring product quality and availability for a wider audience.

|

Frozen Breads Frozen Pastries Retail Cakes and Pastries Frozen Desserts Frozen Pizza Crusts |

|

|

By Distribution Channel |

Supermarkets/Hypermarkets Specialty Stores Convenience Stores Online Channels Bakeries |

|

By Customer Segment |

Household Consumers Food Service Industry Institutional Buyers |

|

By Category |

Conventional Bakery Products Premium and Artisanal Products Health-Oriented Bakery Products |

|

By Region |

North East West South |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Increased Urbanization (Population Density Impact)

3.1.2 Changing Consumer Preferences (Convenience Foods Demand)

3.1.3 Rise in Disposable Income (Income Bracket Distribution)

3.1.4 Tourism Sector Expansion (Visitor Spending Influence)

3.2 Market Challenges

3.2.1 Regulatory Standards (Halal Certification Compliance)

3.2.2 High Production Costs (Supply Chain Inflation)

3.2.3 Limited Cold Storage Facilities (Infrastructure Constraints)

3.3 Opportunities

3.3.1 Demand for Health-Focused Products (Gluten-Free, Organic Products)

3.3.2 Technological Advancements (Automated Production Equipment)

3.3.3 Expansion in Online Distribution Channels (E-commerce Growth)

3.4 Trends

3.4.1 Rising Popularity of Frozen Bakery Items (Consumer Preference Shift)

3.4.2 Introduction of Premium and Gourmet Products (Product Innovation)

3.4.3 Increasing Demand for Single-Serve Packaging (Convenience Factor)

3.5 Government Regulation

3.5.1 Food Safety Standards (SASO Compliance)

3.5.2 Halal Product Certification (Saudi Food and Drug Authority)

3.5.3 Taxation Policies on Frozen Goods (VAT and Import Tariffs)

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competitive Landscape Overview

4.1 By Product Type (in Value %)

4.1.1 Frozen Breads

4.1.2 Frozen Pastries

4.1.3 Retail Cakes and Pastries

4.1.4 Frozen Desserts

4.1.5 Frozen Pizza Crusts

4.2 By Distribution Channel (in Value %)

4.2.1 Supermarkets/Hypermarkets

4.2.2 Specialty Stores

4.2.3 Convenience Stores

4.2.4 Online Channels

4.2.5 Bakeries

4.3 By Customer Segment (in Value %)

4.3.1 Household Consumers

4.3.2 Food Service Industry

4.3.3 Institutional Buyers

4.4 By Category (in Value %)

4.4.1 Conventional Bakery Products

4.4.2 Premium and Artisanal Products

4.4.3 Health-Oriented Bakery Products

4.5 By Region (in Value %)

4.5.1 North

4.5.2 South

4.5.3 East

4.5.4 West

5.1 Detailed Profiles of Major Companies

5.1.1 Almarai Company

5.1.2 Al-Othaim Markets

5.1.3 Saudia Dairy and Foodstuff Company (SADAFCO)

5.1.4 Americana Group

5.1.5 Nestl Middle East

5.1.6 Sunbulah Group

5.1.7 United Food Industries Corporation (Deemah)

5.1.8 Al Kabeer Group ME

5.1.9 Aryzta AG

5.1.10 Dossary Farms

5.1.11 Fonterra Brands Arabia

5.1.12 International Foodstuffs Company (IFFCO)

5.1.13 Switz Group

5.1.14 Ulker Biskvi Sanayi AS

5.1.15 Olayan Group

5.2 Cross Comparison Parameters (Production Capacity, Employee Count, Regional Presence, Revenue, Market Share, Product Portfolio, R&D Investment, and Sustainability Initiatives)

5.3 Market Share Analysis

5.4 Strategic Initiatives (Product Development, Mergers and Acquisitions, and Expansion Plans)

5.5 Investment Analysis (Private Equity Funding and Government Grants)

5.6 Joint Ventures and Collaborations

5.7 Technological Partnerships

5.8 Market Entry Strategies

6.1 Food Safety and Quality Standards

6.2 Labeling and Packaging Regulations

6.3 Import and Export Regulations

6.4 Halal Certification Process

6.5 Environmental Compliance and Waste Management

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Product Type (in Value %)

8.2 By Distribution Channel (in Value %)

8.3 By Customer Segment (in Value %)

8.4 By Category (in Value %)

8.5 By Region (in Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Market Penetration Strategies

9.3 Product Innovation Recommendations

9.4 Market Expansion Opportunities

Disclaimer Contact Us

The initial stage involves mapping the frozen and retail bakery ecosystem in Saudi Arabia, including all prominent stakeholders. Secondary research sources, such as industry publications and government databases, were utilized to define the key factors influencing market growth.

Historical data on market dynamics, distribution channels, and consumer preferences were compiled and analyzed. This included evaluating the revenue contributions of various segments, allowing for an accurate projection of market trends.

Hypotheses regarding market drivers, challenges, and consumer behavior were developed and validated through expert interviews. These consultations provided insights into the operational and strategic focus areas for leading players.

This final stage involved synthesizing data collected from various sources and cross-verifying with leading bakery manufacturers in Saudi Arabia. The objective was to ensure a comprehensive and accurate analysis aligned with market realities.

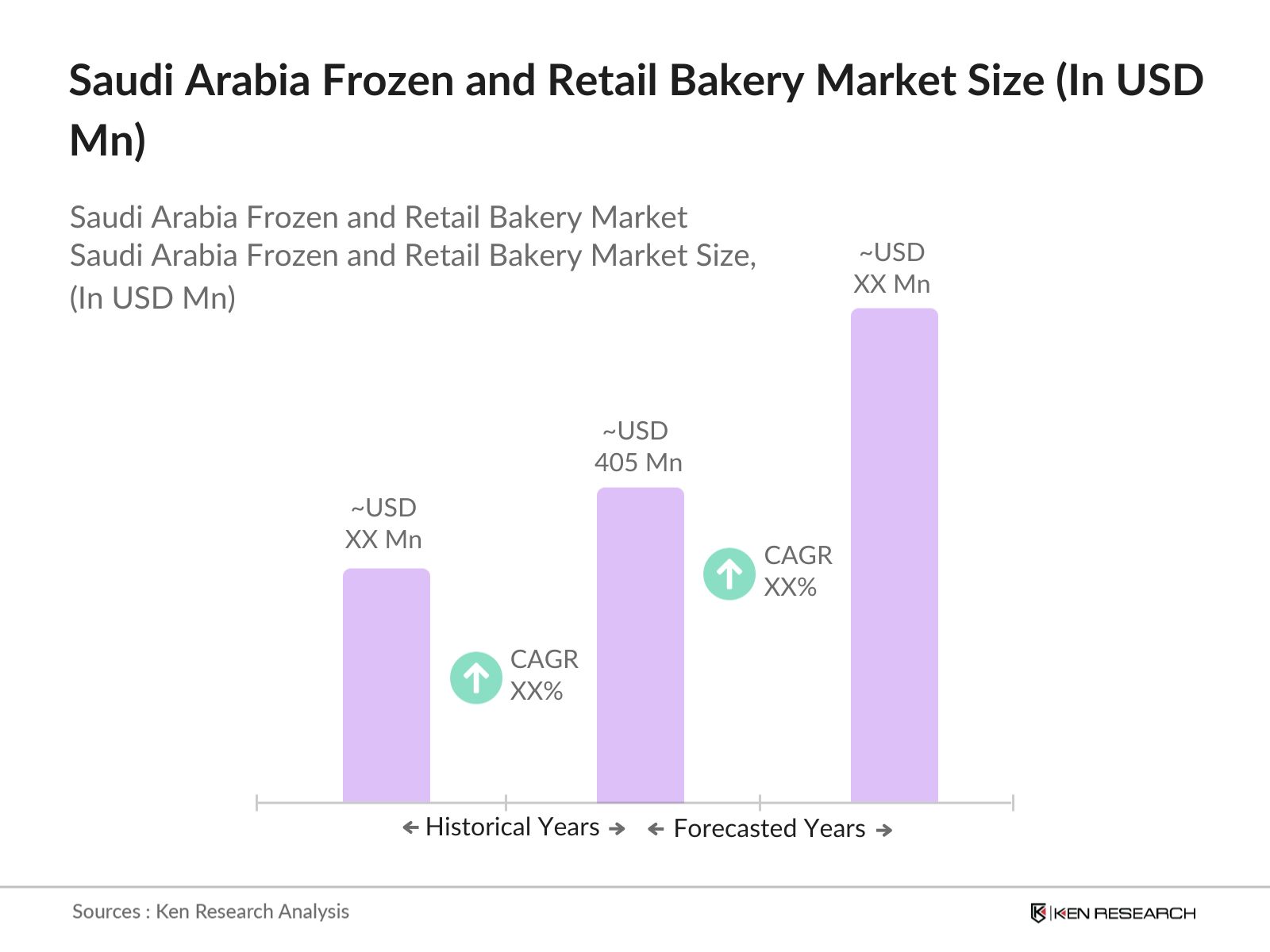

The Saudi Arabia frozen and retail bakery market was valued at USD 405 million, primarily driven by an increasing demand for convenient, ready-to-eat food options and a rising focus on health-conscious product offerings.

Key challenges include regulatory compliance with food safety standards, high production costs, and limited cold storage infrastructure, all of which affect operational efficiency and profitability.

Major players include Almarai Company, SADAFCO, Sunbulah Group, Nestl Middle East, and Americana Group, with strong brand recognition and extensive distribution networks.

Growth is driven by increased urbanization, rising disposable income, and the expanding tourism sector, which enhances the demand for convenient and high-quality bakery products across various consumer segments.

Frozen breads dominate the product type segment, benefiting from their convenience, extended shelf life, and appeal to both household and food service sectors.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.