Saudi Arabia Fruits and Vegetables Market Outlook to 2030

Region:Saudi Arabia

Author(s):Sanjeev

Product Code:KROD5656

Region:Saudi Arabia

Author(s):Sanjeev

Product Code:KROD5656

November 2024

99

The Saudi Arabia fruits and vegetables market is highly competitive, with both local and international players contributing to its growth. Large domestic companies have a presence due to their control over supply chains and close alignment with government initiatives. The market is dominated by local players such as Almarai and Al Watania Agriculture, alongside global firms like Del Monte and Dole. This consolidation highlights the importance of advanced farming technologies and cold chain logistics in maintaining market leadership. Companies with better access to cold storage and transportation are able to offer fresher produce, ensuring their competitiveness in a market where freshness is a key demand driver.

|

Company |

Established |

Headquarters |

Product Range |

Revenue (2023) |

No. of Employees |

Global Reach |

Local Market Share |

Distribution Network |

|

Almarai Company |

1977 |

Riyadh, Saudi Arabia |

||||||

|

Al Watania Agriculture |

1982 |

Al Jouf, Saudi Arabia |

||||||

|

Del Monte Saudi Arabia |

1886 |

Khobar, Saudi Arabia |

||||||

|

Pure Harvest Smart Farms |

2017 |

Abu Dhabi, UAE |

||||||

|

NADEC |

1981 |

Riyadh, Saudi Arabia |

Over the next five years, the Saudi Arabia fruits and vegetables market is expected to grow due to continued government support for agricultural innovation, improvements in farming technologies such as hydroponics, and efforts to reduce reliance on imports. The adoption of controlled-environment agriculture and increased investments in local farming infrastructure will also play pivotal roles in driving future growth. The rise in health-conscious consumers and the growing trend towards organic farming are anticipated to boost demand for fruits and vegetables. Moreover, the expansion of e-commerce and improved cold storage solutions will further solidify the market's growth trajectory, particularly in urban areas.

|

Dates Citrus fruit Tropical fruits tomatoes |

|

|

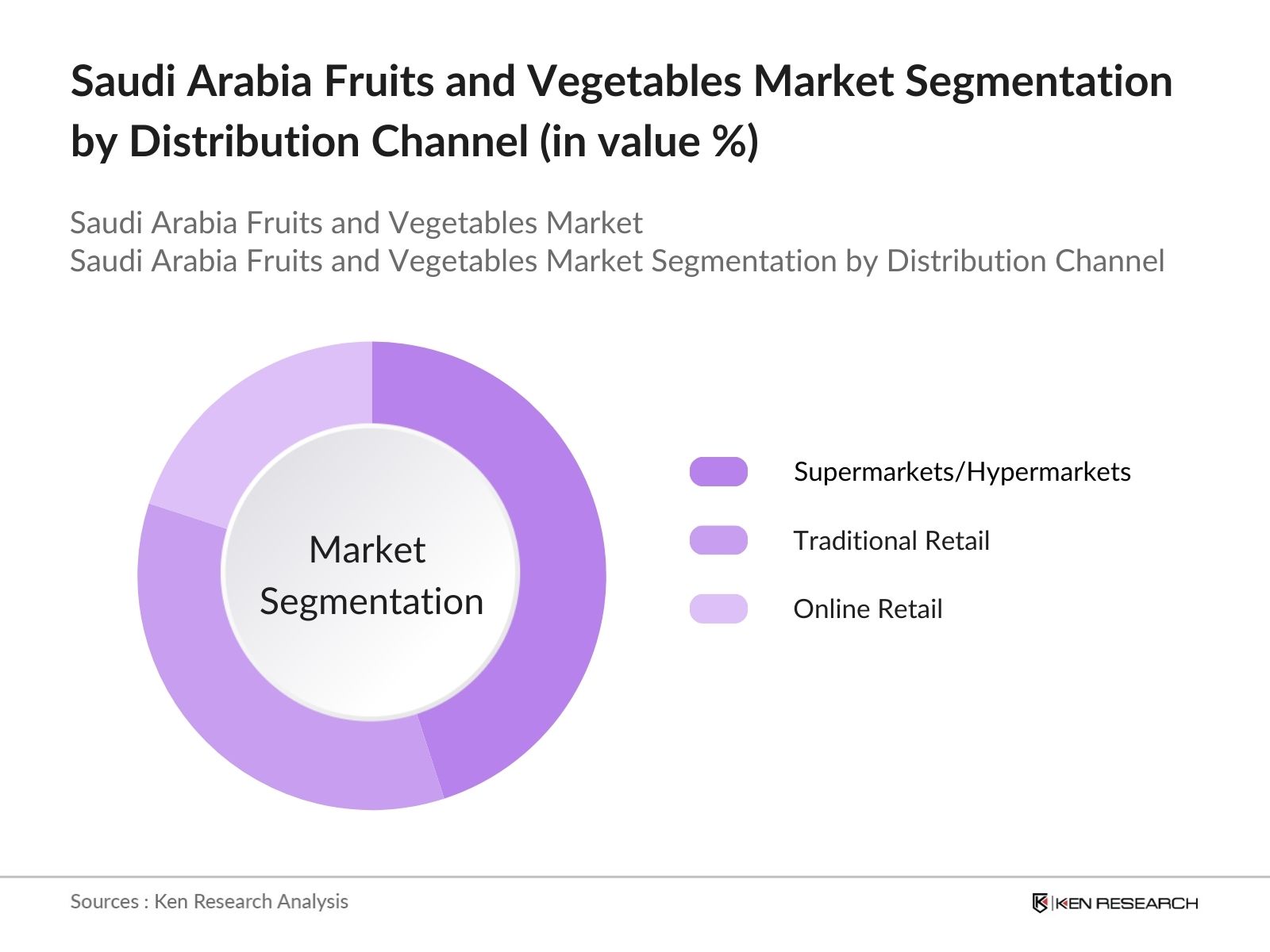

By Distribution Channel |

Supermarkets/Hypermarkets Traditional Retail Online Retail |

|

By Farming Technique |

Organic Farming Conventional Farming Hydroponic Farming |

|

By End-Use |

Retail Consumers HoReCa (Hotel/Restaurant/Catering) Food Processing Industry |

|

By Region |

North East West South |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Increased Consumption of Organic Produce

3.1.2 Government Initiatives (Saudi Vision 2030, National Agricultural Development Plan)

3.1.3 Advancements in Agriculture Technology (Hydroponics, Vertical Farming)

3.1.4 Rise in Health-Conscious Consumers

3.2 Market Challenges

3.2.1 Water Scarcity and Agricultural Sustainability

3.2.2 High Import Dependency for Fruits

3.2.3 Fluctuations in Climate Conditions

3.3 Opportunities

3.3.1 Growth in Organic Farming Initiatives

3.3.2 Expansion in Agri-Tech Investments

3.3.3 Improved Cold Storage Infrastructure

3.4 Trends

3.4.1 Adoption of Controlled-Environment Agriculture

3.4.2 Increased Use of Drip Irrigation

3.4.3 Growing Preference for Locally Grown Products

3.5 Government Regulation

3.5.1 Subsidies for Water-Saving Technologies

3.5.2 Import Tariff Changes

3.5.3 Support for Domestic Agriculture through Vision 2030

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces

3.9 Competitive Ecosystem

4.1 By Product Type (In Value %)

4.1.1 Fruits

4.1.1.1 Citrus Fruits

4.1.1.2 Dates

4.1.1.3 Tropical Fruits (Bananas, Mangoes)

4.1.1.4 Berries

4.1.2 Vegetables

4.1.2.1 Leafy Vegetables

4.1.2.2 Root Vegetables

4.1.2.3 Tomatoes

4.1.2.4 Cucumbers

4.2 By Distribution Channel (In Value %)

4.2.1 Supermarkets/Hypermarkets

4.2.2 Traditional Retail

4.2.3 Online Retail

4.3 By Farming Technique (In Value %)

4.3.1 Organic Farming

4.3.2 Conventional Farming

4.3.3 Hydroponic Farming

4.4 By End-Use (In Value %)

4.4.1 Retail Consumers

4.4.2 HoReCa (Hotel/Restaurant/Catering)

4.4.3 Food Processing Industry

4.5 By Region (In Value %)

4.5.1 Norht

4.5.2 West

4.5.3 East

4.5.4 South

5.1 Detailed Profiles of Major Companies

5.1.1 Almarai Company

5.1.2 Al Watania Agriculture

5.1.3 Del Monte Saudi Arabia

5.1.4 Dole Saudi Arabia

5.1.5 Desert Farms

5.1.6 Pure Harvest Smart Farms

5.1.7 NADEC (National Agricultural Development Company)

5.1.8 Saudi Vegetable Oil Company

5.1.9 Tamimi Markets

5.1.10 Lulu Hypermarket

5.1.11 Al Bakrawe Farm

5.1.12 Fresh Del Monte Produce Inc.

5.1.13 Almarai

5.1.14 Saudi Agricultural Development Company

5.1.15 Al Kabeer Group

5.2 Cross Comparison Parameters (Production Capacity, Farming Technique, Revenue, Number of Employees)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 Agricultural Certification Requirements

6.2 Water Use Regulations

6.3 Import and Export Compliance

6.4 Environmental Standards

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Product Type (In Value %)

8.2 By Distribution Channel (In Value %)

8.3 By Farming Technique (In Value %)

8.4 By End-Use (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

In this step, we mapped the major stakeholders of the Saudi Arabia fruits and vegetables market. We utilized secondary research tools, including industry databases and reports, to gather data on key market dynamics and stakeholders. The primary goal was to identify the variables driving market trends and influencing consumer demand.

We analyzed historical data on fruit and vegetable consumption, production rates, and import-export balances to build a detailed picture of the market. We also assessed supply chain infrastructure and advancements in agricultural technology.

Through interviews with leading agricultural experts and farmers, we validated key market assumptions regarding production costs, the impact of new technologies, and consumer preferences for locally grown produce.

The final phase involved engaging directly with local farming companies and Agri-Tech firms to validate sales data, production capabilities, and market expansion strategies. This synthesis ensured the accuracy of our market forecasts and segmentation.

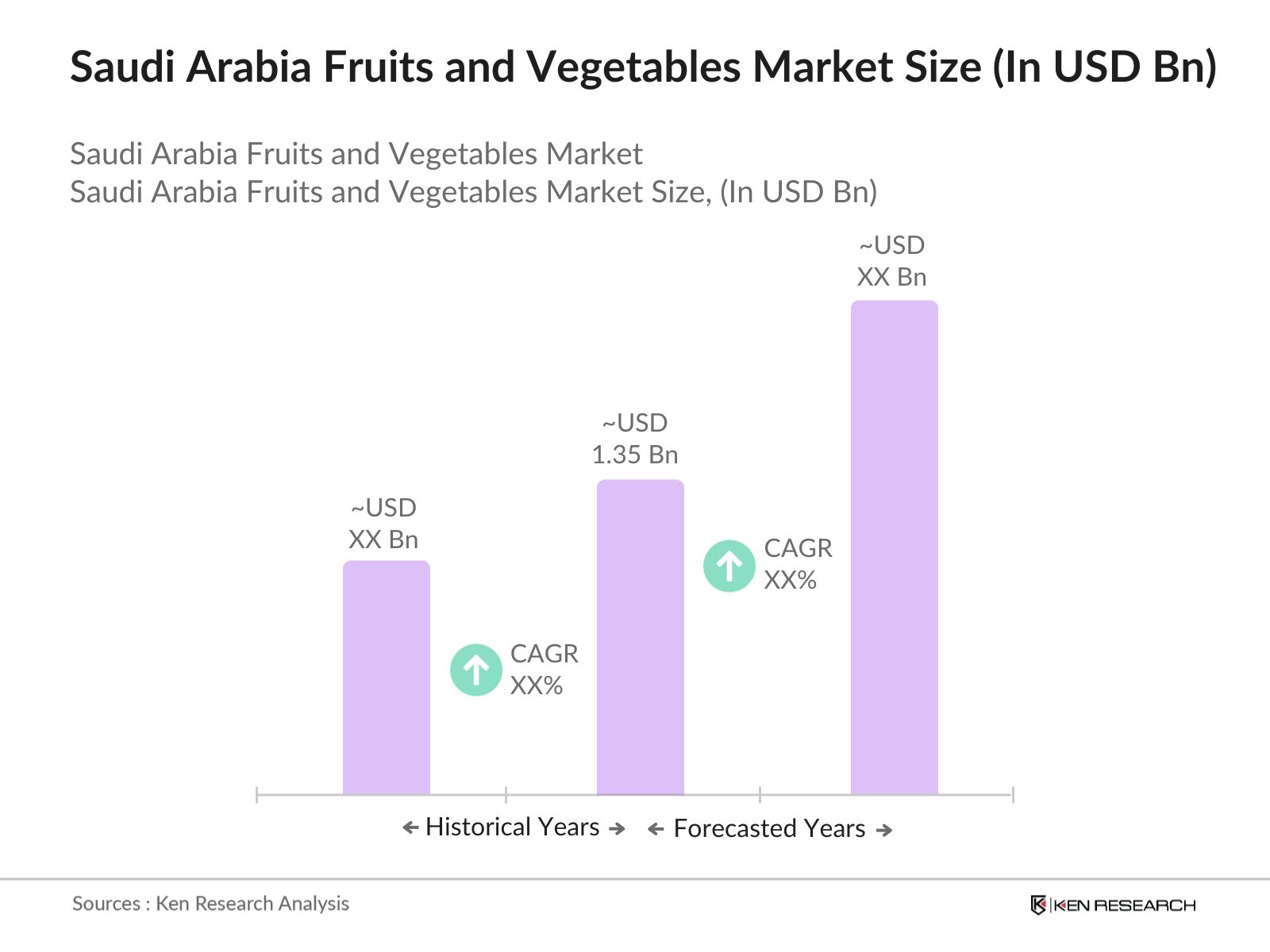

The Saudi Arabia fruits and vegetables market is valued at USD 1.35 billion, with steady growth driven by increasing domestic demand and government support for agricultural development.

Challenges in Saudi Arabia fruits and vegetables market include water scarcity, dependency on imported fruits, and climate change, all of which affect local production capacity. Additionally, supply chain inefficiencies and high production costs pose risks to market stability.

Key players in Saudi Arabia fruits and vegetables market include Almarai, Al Watania Agriculture, Del Monte Saudi Arabia, Pure Harvest Smart Farms, and NADEC, dominating through strong supply chains and government-backed agricultural programs.

Saudi Arabia fruits and vegetables market Growth is propelled by increased investment in agri-tech, government initiatives to reduce food import dependency, and growing consumer demand for fresh, organic produce.

Technologies like hydroponics, vertical farming, and drip irrigation systems are major technologies in Saudi Arabia fruits and vegetables market that are transforming local agriculture, improving efficiency, and reducing the environmental impact of farming.

This detailed report provides an in-depth analysis of the Saudi Arabia fruits and vegetables market, covering key market drivers, segmentation, competitive landscape, and future outlook.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.