Saudi Arabia Health & Medical Insurance Market Outlook 2030

Region:Middle East

Author(s):Shivani Mehra

Product Code:KROD11125

November 2024

83

About the Report

Saudi Arabia Health & Medical Insurance Market Overview

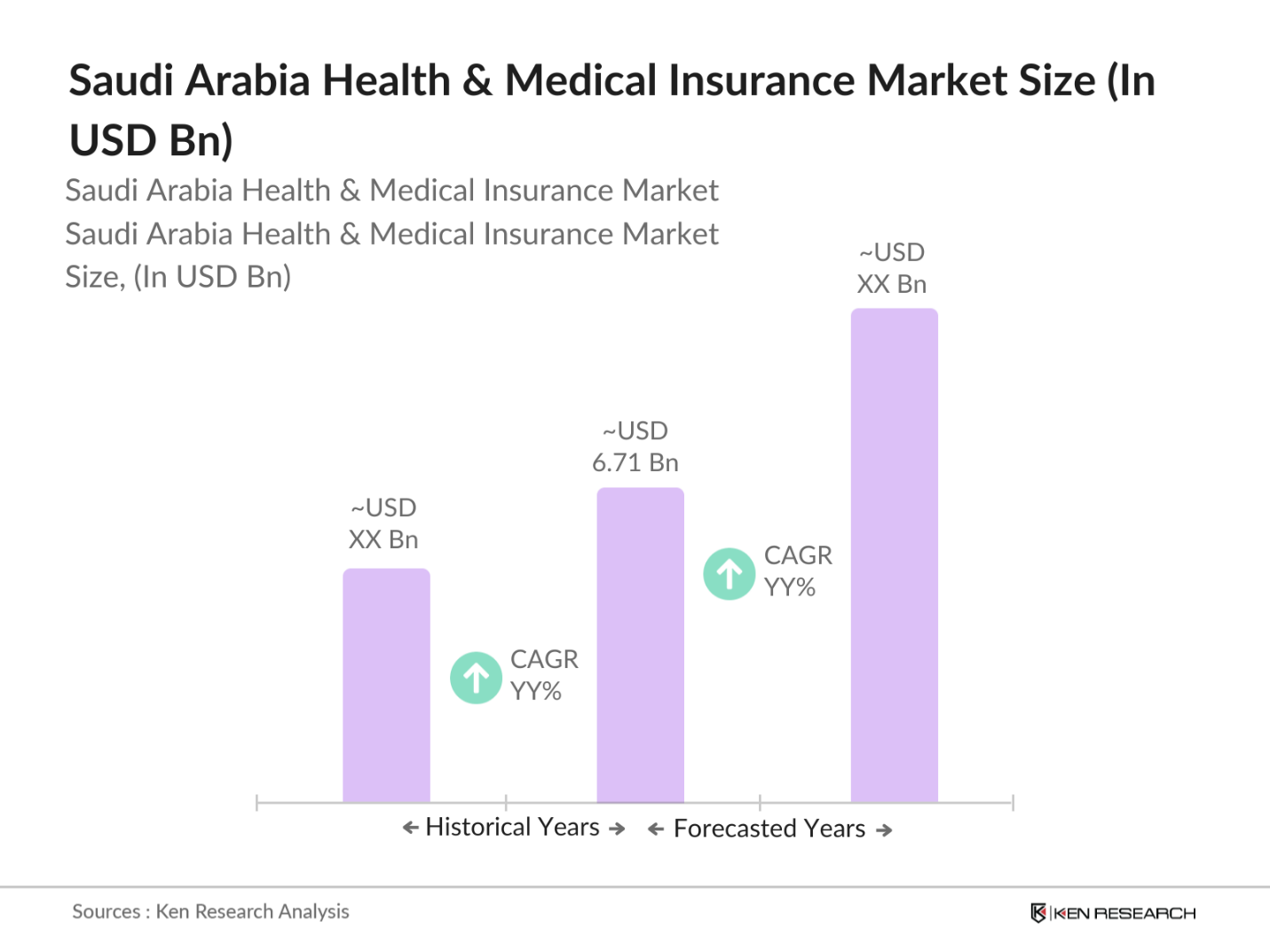

- The Saudi Arabia Health & Medical Insurance market is valued at USD 6.71 billion, based on a comprehensive analysis of historical and current data. The market is primarily driven by the increasing demand for healthcare services, propelled by a growing population and a rise in chronic diseases. Additionally, government initiatives aimed at enhancing healthcare infrastructure and insurance coverage have significantly contributed to market growth. The market is anticipated to supported by ongoing reforms and a focus on improving health service accessibility.

- Major cities such as Riyadh, Jeddah, and Dammam dominate the Saudi Arabian Health & Medical Insurance market. Riyadh, being the capital, is a hub for healthcare services, housing numerous hospitals and insurance companies. Jeddah serves as a key coastal city with a significant expatriate population, increasing the demand for diverse insurance products. Dammam, a major industrial center, also drives demand due to its growing workforce and associated healthcare needs, contributing to the overall market expansion.

- The implementation of the National Health Insurance Framework aims to provide equitable healthcare access to all Saudi residents. In 2023, the Saudi government allocated SAR 10 billion to support the establishment of this framework, emphasizing its commitment to improving health services. This regulation is expected to standardize insurance coverage and enhance consumer protection, fostering a more robust health insurance market as it seeks to eliminate disparities in healthcare access across different regions.

Saudi Arabia Health & Medical Insurance Market Segmentation

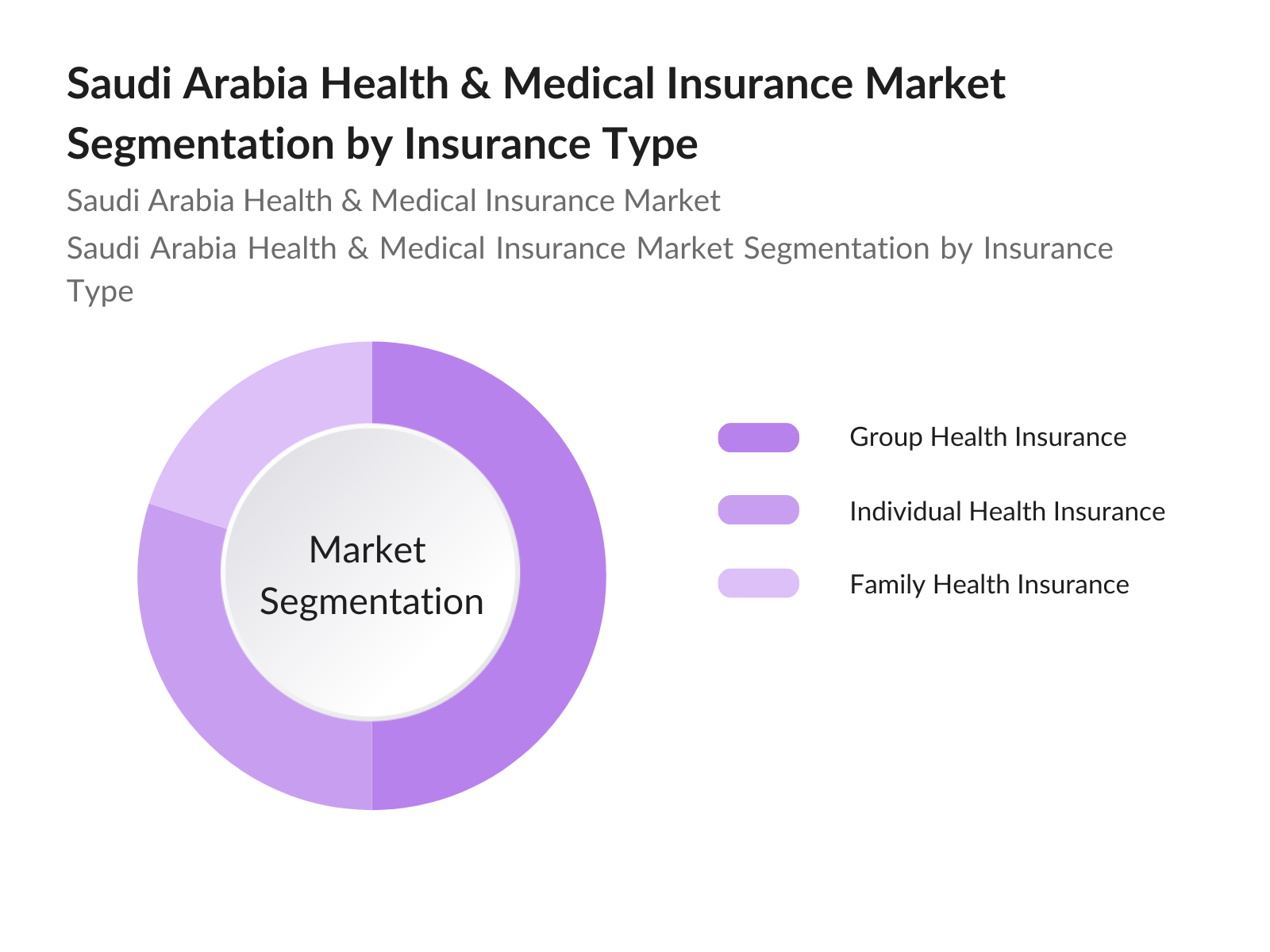

- By Insurance Type: The Saudi Arabia Health & Medical Insurance market is segmented by insurance type into individual health insurance, group health insurance, and family health insurance. Group health insurance holds a dominant market share, primarily due to its widespread adoption among employers seeking to provide healthcare benefits to employees. The corporate sector's emphasis on employee wellness and the growing trend of organizations offering comprehensive health plans have fueled the demand for group policies. Furthermore, the rise in small and medium enterprises (SMEs) in the region is driving the need for accessible group insurance options.

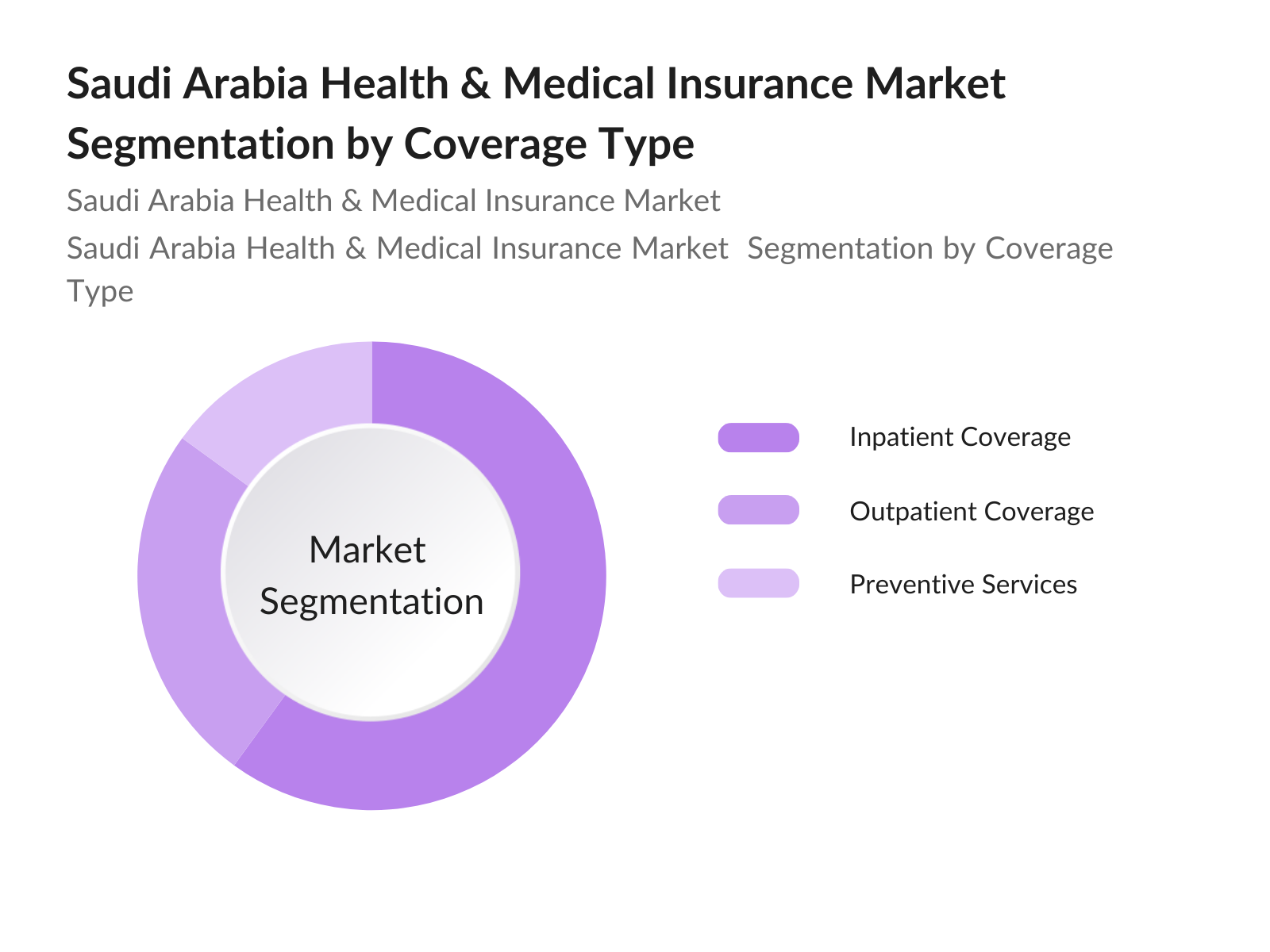

- By Coverage Type: The market is also segmented by coverage type into inpatient coverage, outpatient coverage, and preventive services. Inpatient coverage is the leading segment, driven by the rising costs of hospitalization and the increasing incidence of surgeries and severe illnesses. As healthcare expenses rise, patients are more inclined to opt for comprehensive insurance plans that offer extensive inpatient coverage. This segment is crucial for mitigating financial risks associated with high medical bills, thus making it the preferred choice among policyholders.

Saudi Arabia Health & Medical Insurance Market Competitive Landscape

The Saudi Arabia Health & Medical Insurance market is dominated by several key players, including Tawuniya, Bupa Arabia, and Al Rajhi Takaful. This consolidation reflects the significant influence of these companies, which have established robust networks and strong brand recognition. The competitive landscape is characterized by innovative product offerings and aggressive marketing strategies aimed at expanding customer bases.

Saudi Arabia Health & Medical Insurance Market Analysis

Market Growth Drivers

- Increasing Population and Aging Demographics: Saudi Arabias population reached approximately 35 million in 2023, with projections indicating an increase to over 37 million by 2025, according to the World Bank. The number of individuals aged 65 and older is expected to rise significantly, reflecting the increasing demand for health insurance as older adults typically require more medical services. Additionally, the government's initiative aims to enhance healthcare accessibility for all age groups, which includes improved health insurance coverage. This demographic shift, combined with government efforts, is driving the growth of the health insurance market in Saudi Arabia.

- Rising Incidence of Chronic Diseases: The prevalence of chronic diseases such as diabetes and cardiovascular disorders is escalating in Saudi Arabia, with the Ministry of Health reporting that around 7.4 million people were diagnosed with diabetes in 2022. This number is projected to increase to approximately 8.2 million by 2025. Chronic diseases require long-term medical attention, driving demand for comprehensive health insurance coverage. In addition, healthcare expenditure on chronic diseases was estimated at over SAR 30 billion in 2023, accounting for a substantial portion of the total healthcare budget.

- Government Initiatives and Regulatory Framework: The Saudi government has initiated several reforms to enhance the healthcare sector, including the implementation of the National Health Insurance System, which aims to provide universal healthcare coverage by 2025. In 2023, the government allocated SAR 192 billion to health services, up from SAR 175 billion in 2022, indicating a strong commitment to improving healthcare infrastructure and access. These initiatives are expected to boost the insurance market significantly by creating a more favorable regulatory environment for insurers and ensuring broader coverage for the population.

Market Challenges:

- High Healthcare Costs: Healthcare spending in Saudi Arabia was estimated at SAR 187 billion in 2022, with expectations to reach SAR 200 billion by 2025. Despite efforts to increase insurance coverage, high out-of-pocket expenses remain a significant barrier for many citizens, with an average expenditure of SAR 5,000 per individual per year. This financial burden can deter potential policyholders from enrolling in health insurance plans, thereby stifling market growth. The government is working to address these costs through various subsidies and reforms aimed at making healthcare more affordable.

- Market Fragmentation: The health insurance market in Saudi Arabia is characterized by fragmentation, with over 30 companies operating in the space. This competitive landscape can lead to inconsistencies in service quality and product offerings, making it challenging for consumers to navigate their options. Additionally, small insurers often struggle to provide comprehensive coverage compared to larger, more established players. The Saudi government has recognized this issue and is encouraging consolidation within the industry to improve efficiency and service delivery.

Saudi Arabia Health & Medical Insurance Market Future Outlook

Over the next five years, the Saudi Arabia Health & Medical Insurance market is expected to show substantial growth driven by continuous government reforms, increased healthcare awareness, and technological advancements in health insurance services. The government's push towards universal healthcare coverage and the expansion of private sector participation in the healthcare system are anticipated to enhance the market's appeal. Furthermore, the growing prevalence of lifestyle-related diseases will lead to a higher demand for comprehensive insurance products, positioning the market for robust expansion.

Market Opportunities:

- Expansion of Insurance Products: There is a growing demand for diverse insurance products tailored to meet the specific needs of various demographic groups. In 2023, many insurance policyholders expressed interest in specialized plans covering preventive care and wellness services. This trend indicates an opportunity for insurers to expand their product offerings, such as mental health coverage and family health plans. Additionally, the rise of health savings accounts (HSAs) is encouraging more individuals to seek insurance, thereby contributing to market growth as consumers look for plans that cater to their unique healthcare needs.

- Growth in Medical Tourism: Saudi Arabia's initiative to promote medical tourism is expected to bolster the health insurance market. In 2022, the country attracted over 400,000 medical tourists, with projections indicating this number could reach 1 million by 2025. This influx is driven by the availability of high-quality medical services and the government's commitment to developing the healthcare infrastructure. Insurance providers can capitalize on this trend by offering tailored packages that include coverage for international patients, thus tapping into a lucrative market segment and expanding their reach.

Scope of the Report

|

By Product Type |

Individual Health Insurance Group Health Insurance Family Health Insurance |

|

By Coverage Type |

Inpatient Coverage Outpatient Coverage Preventive Services |

|

By Provider Type |

Public Sector Insurance Private Sector Insurance |

|

By Distribution Channel |

Direct Sales Brokers and Agents Online Platforms |

|

By Region |

North-East Midwest West Coast Southern States |

Products

Key Target Audience

Insurance Companies

Healthcare Providers

Corporate Employers

Government Agencies (Saudi Ministry of Health, Saudi Arabian Monetary Authority)

Regulatory Bodies (Council of Cooperative Health Insurance)

Investments and Venture Capitalist Firms

International Insurance Firms

Health Technology Companies

Companies

Players Mentioned in the market

Tawuniya

Bupa Arabia

Al Rajhi Takaful

United Cooperative Assurance

Arabian Shield Cooperative

AXA Cooperative Insurance

Al Ahlia Insurance Company

Gulf Insurance Group

Saudi Enaya Cooperative Insurance

MetLife Alico

SABB Takaful

Zurich Insurance Group

Allianz Saudi Fransi

Alahli Takaful

Medgulf

Table of Contents

1. Saudi Arabia Health & Medical Insurance Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.Saudi Arabia Health & Medical Insurance Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Saudi Arabia Health & Medical Insurance Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Population and Aging Demographics

3.1.2. Rising Incidence of Chronic Diseases

3.1.3. Government Initiatives and Regulatory Framework

3.1.4. Increasing Health Awareness among Citizens

3.2. Market Challenges

3.2.1. High Healthcare Costs

3.2.2. Limited Insurance Coverage

3.2.3. Market Fragmentation

3.3. Opportunities

3.3.1. Technological Innovations in Healthcare

3.3.2. Expansion of Insurance Products

3.3.3. Growth in Medical Tourism

3.4. Trends

3.4.1. Digital Health Solutions

3.4.2. Shift Towards Value-Based Care

3.4.3. Integration of Telemedicine

3.5. Government Regulation

3.5.1. National Health Insurance Framework

3.5.2. Quality Assurance Standards

3.5.3. Compliance and Reporting Requirements

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. Saudi Arabia Health & Medical Insurance Market Segmentation

4.1. By Insurance Type (In Value %)

4.1.1. Individual Health Insurance

4.1.2. Group Health Insurance

4.1.3. Family Health Insurance

4.2. By Coverage Type (In Value %)

4.2.1. Inpatient Coverage

4.2.2. Outpatient Coverage

4.2.3. Preventive Services

4.3. By Provider Type (In Value %)

4.3.1. Public Sector Insurance

4.3.2. Private Sector Insurance

4.4. By Distribution Channel (In Value %)

4.4.1. Direct Sales

4.4.2. Brokers and Agents

4.4.3. Online Platforms

4.5. By Region (In Value %)

4.5.1. Riyadh

4.5.2. Jeddah

4.5.3. Dammam

4.5.4. Other Regions

5. Saudi Arabia Health & Medical Insurance Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Tawuniya

5.1.2. Bupa Arabia

5.1.3. Al Rajhi Takaful

5.1.4. United Cooperative Assurance

5.1.5. Arabian Shield Cooperative Insurance

5.1.6. AXA Cooperative Insurance

5.1.7. Al Ahlia Insurance Company

5.1.8. Gulf Insurance Group

5.1.9. Saudi Enaya Cooperative Insurance

5.1.10. MetLife Alico

5.1.11. SABB Takaful

5.1.12. Zurich Insurance Group

5.1.13. Allianz Saudi Fransi

5.1.14. Alahli Takaful

5.1.15. Medgulf

5.2 Cross Comparison Parameters (Market Share, Number of Policies, Revenue, Customer Satisfaction, Claim Settlement Ratio, Digital Presence, Provider Network, Compliance Rate)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Saudi Arabia Health & Medical Insurance Market Regulatory Framework

6.1. Insurance Sector Regulations

6.2. Compliance Requirements

6.3. Licensing Processes

7. Saudi Arabia Health & Medical Insurance Market Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Saudi Arabia Health & Medical Insurance Market Future Segmentation

8.1. By Insurance Type (In Value %)

8.2. By Coverage Type (In Value %)

8.3. By Provider Type (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9. Saudi Arabia Health & Medical Insurance Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing a detailed ecosystem map encompassing all major stakeholders within the Saudi Arabia Health & Medical Insurance Market. This step is supported by extensive desk research, utilizing both secondary and proprietary databases to gather comprehensive industry-level information. The primary goal is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, historical data related to the Saudi Arabia Health & Medical Insurance Market will be compiled and analyzed. This includes assessing market penetration, the ratio of insured individuals to the population, and the resultant revenue generation. Additionally, an evaluation of service quality statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple insurance providers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, ensuring a comprehensive, accurate, and validated analysis of the Saudi Arabia Health & Medical Insurance Market.

Frequently Asked Questions

01. How big is the Saudi Arabia Health & Medical Insurance market?

The Saudi Arabia Health & Medical Insurance market is valued at USD 6.71 billion, driven by rising healthcare demands and government initiatives aimed at expanding insurance coverage.

02. What are the challenges in the Saudi Arabia Health & Medical Insurance market?

Challenges include high healthcare costs, limited insurance penetration among the population, and the need for enhanced regulatory frameworks to ensure compliance and service quality.

03. Who are the major players in the Saudi Arabia Health & Medical Insurance market?

Key players include Tawuniya, Bupa Arabia, Al Rajhi Takaful, and United Cooperative Assurance, which dominate due to their strong brand presence and extensive service offerings.

04. What are the growth drivers of the Saudi Arabia Health & Medical Insurance market?

The market is propelled by factors such as increasing healthcare costs, growing awareness of health issues, and ongoing government reforms to improve healthcare access and affordability.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.