Saudi Arabia Red Meat Market Outlook to 2030

Region:Saudi Arabia

Author(s):Sanjeev

Product Code:KROD10042

Region:Saudi Arabia

Author(s):Sanjeev

Product Code:KROD10042

December 2024

91

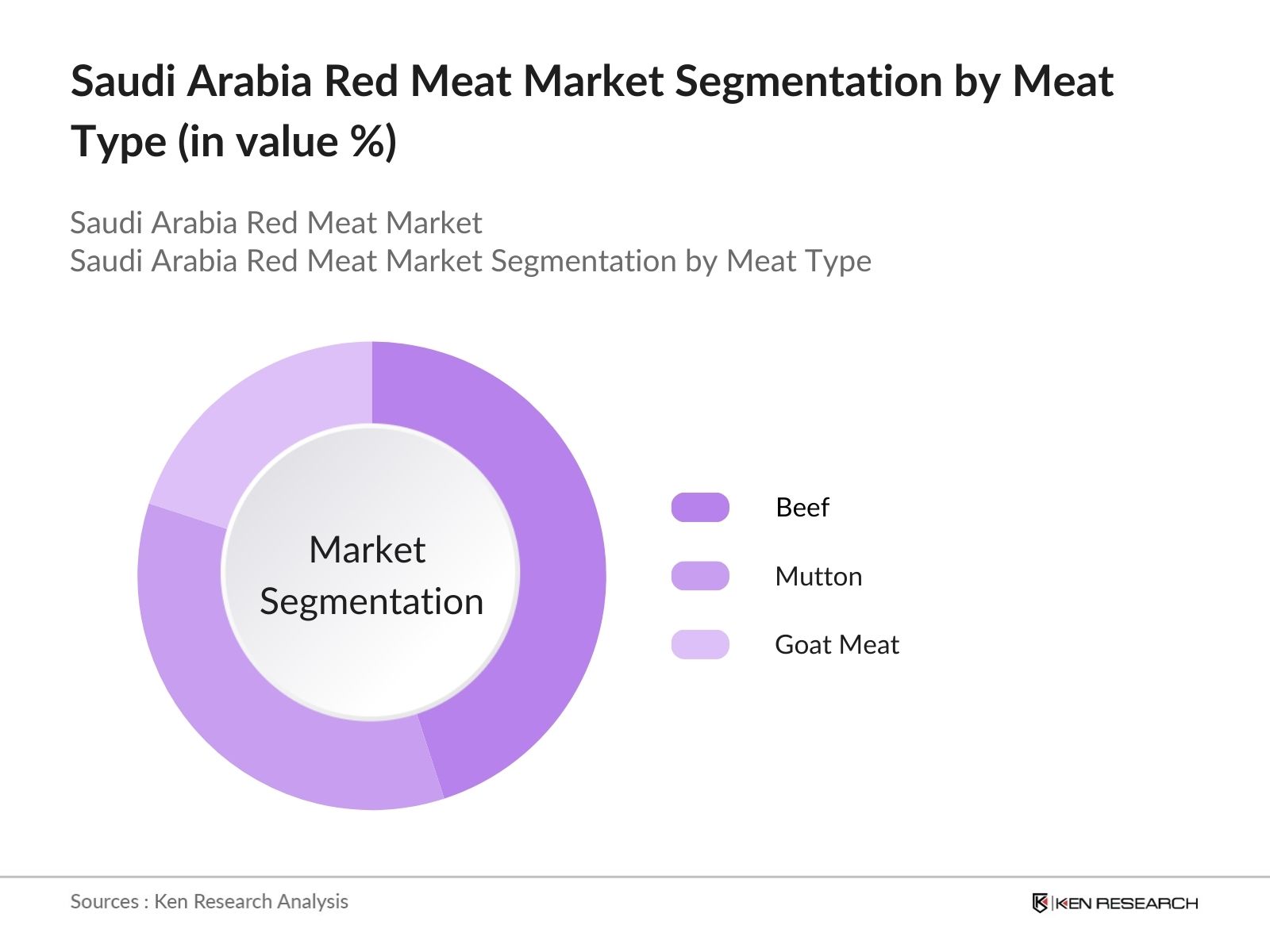

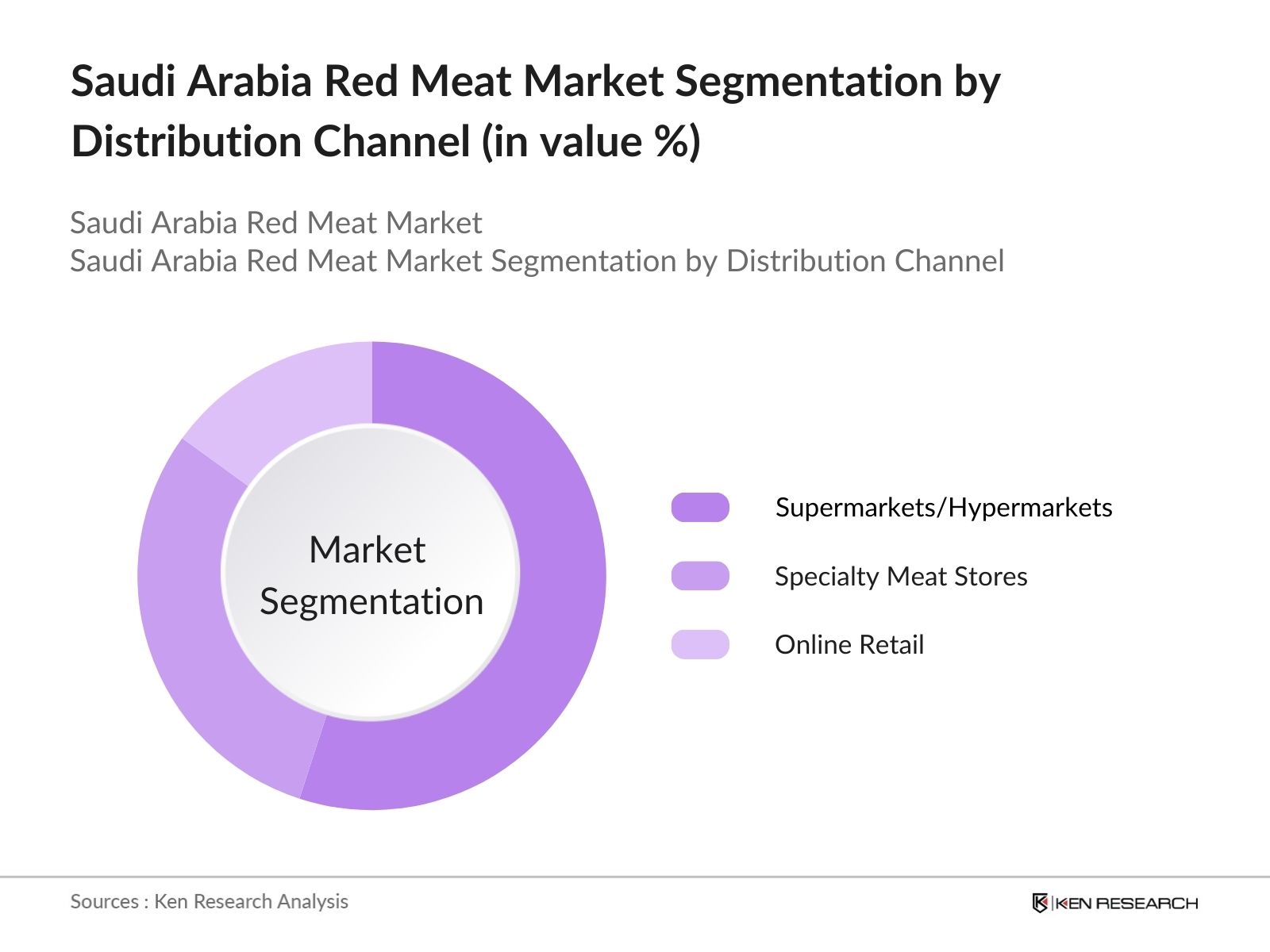

The Saudi Arabia red meat market is segmented by meat type and by distribution channel.

The Saudi Arabia red meat market is characterized by a combination of local and international players. The market is dominated by key domestic players like Almarai and Tanmiah, as well as international firms like BRF Sadia and Hormel Foods. These companies maintain a competitive edge through their extensive distribution networks, investments in advanced farming and processing technologies, and the ability to meet the growing demand for premium and halal-certified products. The competitive landscape is also influenced by strong government support for local meat producers as part of the Saudi Vision 2030, which aims to reduce import dependency.

|

Company Name |

Establishment Year |

Headquarters |

Product Range |

Processing Capacity |

Distribution Network |

|

Almarai |

1977 |

Riyadh, Saudi Arabia |

|||

|

Tanmiah |

1962 |

Jeddah, Saudi Arabia |

|||

|

Al Kabeer Group |

1972 |

Dubai, UAE |

|||

|

BRF Sadia |

1934 |

So Paulo, Brazil |

|||

|

Hormel Foods International |

1891 |

Minnesota, USA |

Over the next five years, the Saudi Arabia red meat market is expected to experience steady growth driven by the increasing consumer preference for premium meat products and the expansion of foodservice industries. The government's emphasis on enhancing local food security through investments in agriculture and livestock farming will further contribute to the growth of the domestic meat sector. Furthermore, the rising demand for organic and halal-certified red meat, as well as the development of more efficient supply chains, will open new opportunities for both local and international market players.

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rising Disposable Income (per capita income growth)

3.1.2. Cultural Preference for Meat-Based Diet (food habits)

3.1.3. Population Growth and Urbanization (demographics)

3.1.4. Government Policies Supporting Local Meat Production (local production initiatives)

3.2. Market Challenges

3.2.1. High Production Costs (input costs like feed and water)

3.2.2. Supply Chain Inefficiencies (cold chain logistics)

3.2.3. Increasing Competition from Imported Meat (import dependency)

3.3. Opportunities

3.3.1. Investment in Modern Farming Techniques (agritech investments)

3.3.2. Growth of Organic and Halal Meat Segments (premium segments)

3.3.3. Expansion into Export Markets (regional trade opportunities)

3.4. Trends

3.4.1. Rise in Meat Alternatives and Processed Red Meat (consumer preferences)

3.4.2. Increase in Animal Welfare Concerns (sustainable practices)

3.4.3. Adoption of Automation in Meat Processing (industry 4.0 in slaughterhouses)

3.5. Government Regulation

3.5.1. Saudi Vision 2030 Agriculture Policies (sector-specific regulations)

3.5.2. Food Safety and Quality Standards (SFDA regulations)

3.5.3. Import Quotas and Tariffs (import duty structures)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.8.1. Threat of New Entrants

3.8.2. Bargaining Power of Suppliers

3.8.3. Bargaining Power of Buyers

3.8.4. Threat of Substitutes

3.8.5. Industry Rivalry

3.9. Competitive Landscape

4.1. By Type (In Value %)

4.1.1. Beef

4.1.2. Mutton

4.1.3. Goat Meat

4.2. By Distribution Channel (In Value %)

4.2.1. Supermarkets/Hypermarkets

4.2.2. Specialty Meat Stores

4.2.3. Online Retail

4.3. By Product Type (In Value %)

4.3.1. Fresh Meat

4.3.2. Frozen Meat

4.3.3. Processed Meat

4.4. By End-User (In Value %)

4.4.1. Households

4.4.2. Foodservice (Hotels, Restaurants, Catering)

4.5. By Region (In Value %)

4.5.1. Riyadh

4.5.2. Jeddah

4.5.3. Dammam

4.5.4. Makkah

4.5.5. Madinah

5.1 Detailed Profiles of Major Competitors

5.1.1. Almarai

5.1.2. Tanmiah

5.1.3. Al Ain Farms

5.1.4. Al-Rabie

5.1.5. Gulf International Meat Factory

5.1.6. Al Kabeer Group

5.1.7. National Food Industries Company

5.1.8. Savola Group

5.1.9. Sidco Foods

5.1.10. Halwani Brothers

5.1.11. Arabian Farms

5.1.12. BRF Sadia

5.1.13. Al Watania Agriculture

5.1.14. Al Islami Foods

5.1.15. Hormel Foods International

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Product Portfolio, Processing Capacity, Distribution Network, Brand Recognition)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Agricultural Subsidies and Incentives

6.2. Compliance with SFDA Regulations

6.3. Halal Certification Processes

6.4. Import Quotas and Tariff Structures

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Type (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By Product Type (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The first phase involved mapping the ecosystem of the Saudi Arabia red meat market by analyzing the roles of various stakeholders, including producers, distributors, and consumers. A combination of secondary and proprietary databases was used to gather relevant market information. Critical variables such as meat production capacity, import volumes, and consumer preferences were identified.

In this step, historical data related to the Saudi Arabia red meat market was compiled and analyzed. The analysis focused on understanding consumption trends, the growth of distribution channels, and market penetration of different meat types. Market segmentation and distribution data were analyzed to ensure an accurate understanding of market dynamics.

Market hypotheses were developed and validated through consultations with industry experts. These consultations provided insights into consumer behavior, regulatory challenges, and competitive strategies. Interviews were conducted with meat processors, retailers, and distributors to cross-validate the data.

The final step involved synthesizing the data collected from various sources and presenting a detailed analysis of the market. The output included forecasts, recommendations, and an understanding of consumer preferences, which was verified by engaging with multiple meat producers and distributors.

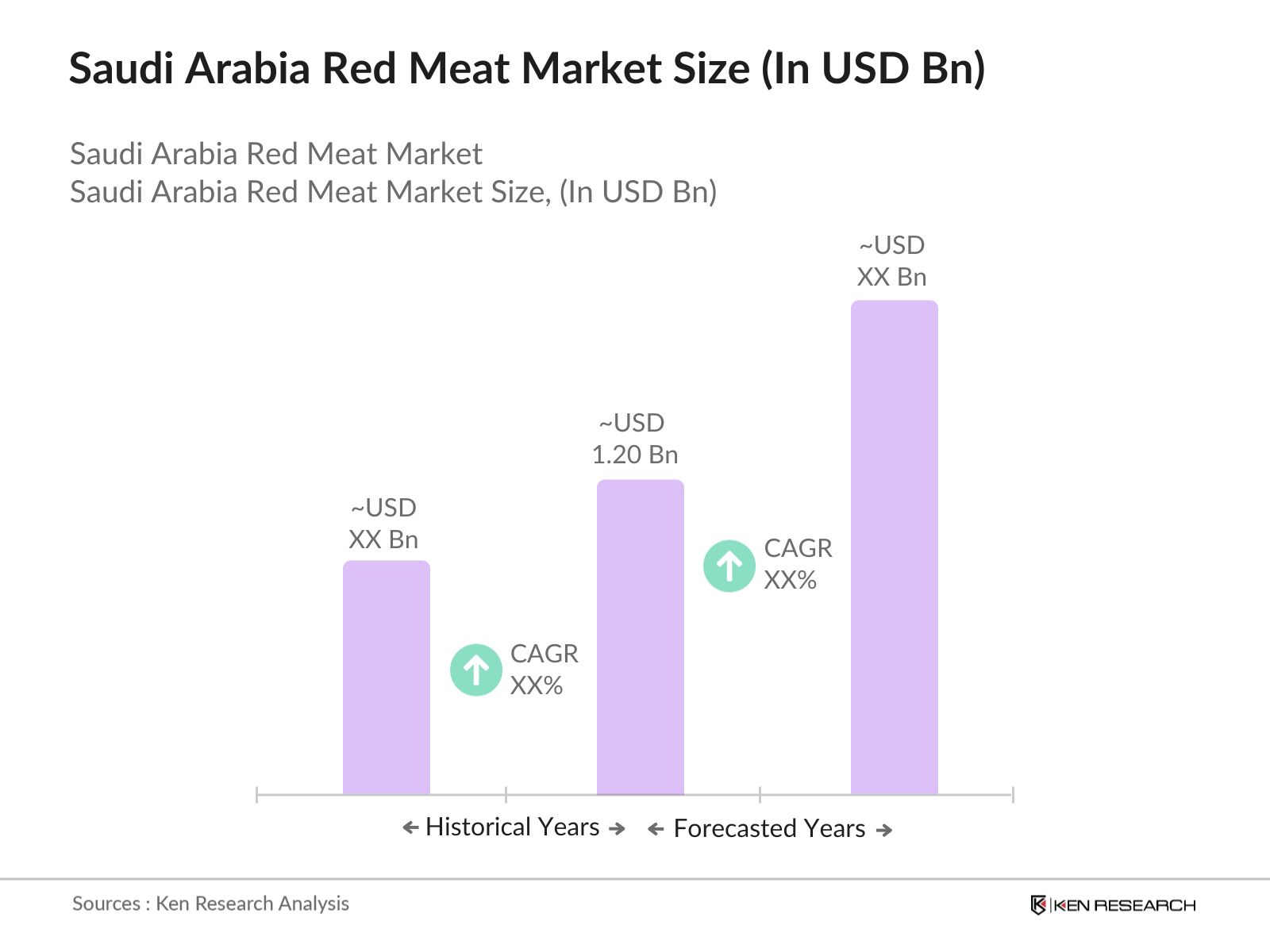

The Saudi Arabia red meat market is valued at 1.20 billion, driven by a combination of local production and imports. Increasing consumer demand for premium meat products is a key factor fueling the market's growth.

Saudi Arabia red meat market Challenges include high production costs due to the arid climate, which makes animal farming expensive, and reliance on imports to meet growing demand. Additionally, supply chain inefficiencies, particularly in cold chain logistics, pose hurdles to the market.

Key players in Saudi Arabia red meat market include Almarai, Tanmiah, BRF Sadia, Hormel Foods International, and Al Kabeer Group. These companies dominate the market through their established distribution networks, brand recognition, and investments in processing technologies.

The Saudi Arabia red meat market is propelled by factors such as rising disposable incomes, urbanization, and government initiatives like Vision 2030, which encourages local food production. The expansion of the foodservice industry also plays a crucial role in driving demand for red meat.

Supermarkets and hypermarkets dominate the distribution channels due to their wide reach and consumer trust in the quality and freshness of the products. Specialty meat stores also have a significant share, particularly for premium meat products.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.