Saudi Arabia Tobacco Market Outlook to 2030

Region:Middle East

Author(s):Sanjeev

Product Code:KROD8217

Region:Middle East

Author(s):Sanjeev

Product Code:KROD8217

November 2024

87

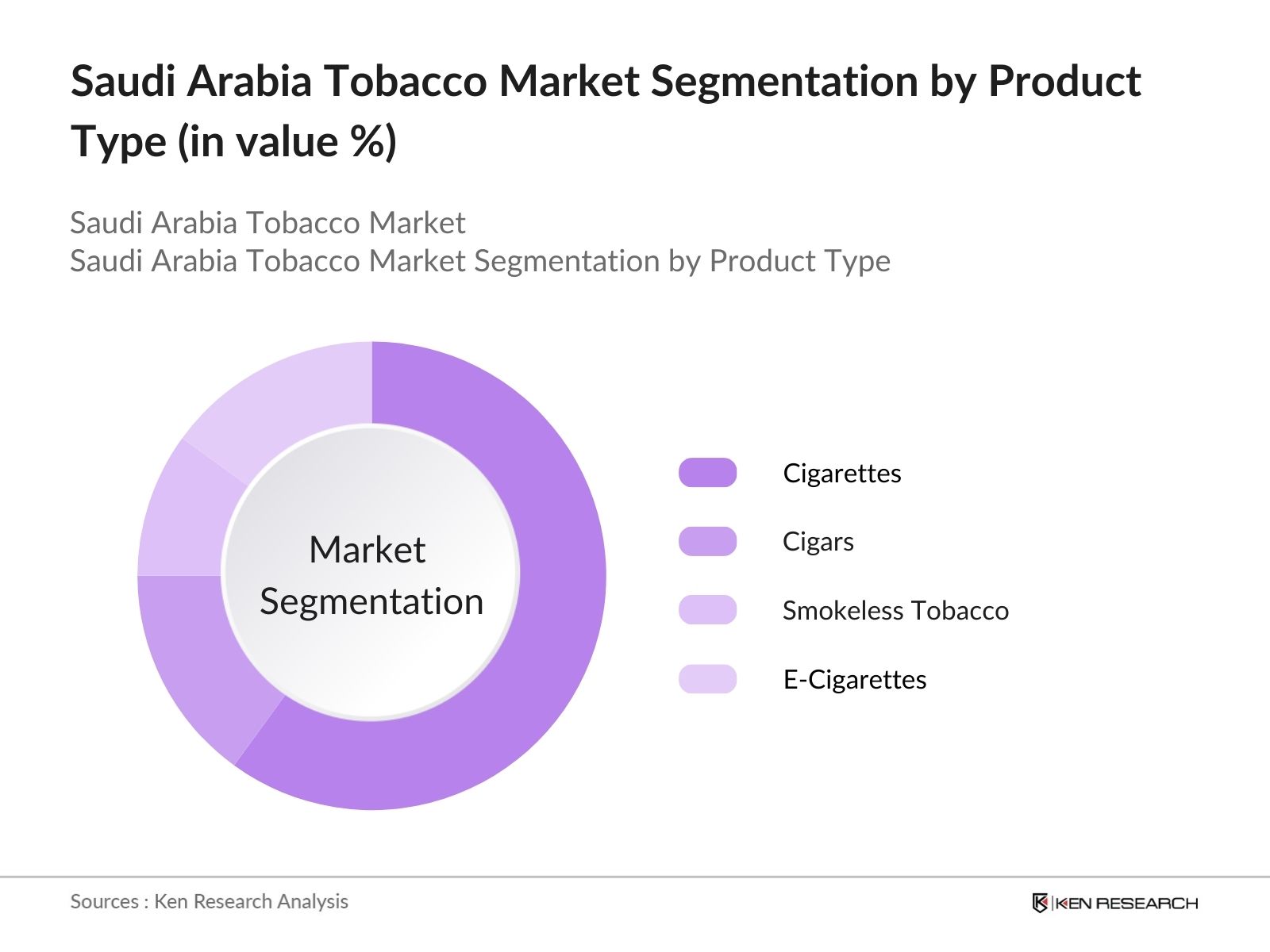

By Product Type: The market is segmented by product type into cigarettes, cigars, smokeless tobacco, and e-cigarettes. Cigarettes hold the dominant share under the product type segmentation, as they are deeply ingrained in the lifestyle of a significant portion of the population. The relatively low cost, ease of availability, and variety of flavors in both traditional and menthol cigarettes contribute to their continued popularity, despite growing awareness of health risks.

By Distribution Channel: The market is also segmented by distribution channels into online retail, supermarkets/hypermarkets, tobacco specialty stores, and convenience stores. Tobacco specialty stores dominate this segment, with a 40% share of the market. These stores offer a wide variety of products, including premium and niche tobacco items, catering to the preferences of consumers who seek personalized experiences and product variety. Additionally, these specialty stores often serve as social hubs, which helps maintain their relevance in the market.

The Saudi Arabia tobacco market is dominated by a mix of international and local players, all competing to maintain market share through product differentiation, distribution reach, and innovation. The competitive landscape is marked by brand loyalty, with leading companies focusing on expanding their premium product lines to cater to evolving consumer preferences.

|

Company Name |

Establishment Year |

Headquarters |

Market Presence |

Product Range |

Sales Channels |

No. of Employees |

Global Reach |

R&D Investments |

|

British American Tobacco |

1902 |

London, UK |

||||||

|

Philip Morris International |

1847 |

Lausanne, CH |

||||||

|

Japan Tobacco International |

1985 |

Tokyo, JP |

||||||

|

Al Nakhla Tobacco Co. |

1913 |

Cairo, EG |

||||||

|

Imperial Brands |

1901 |

Bristol, UK |

Market Growth Drivers

Market Challenges

Over the next five years, the Saudi Arabia tobacco market is expected to experience steady growth driven by product diversification and the increasing demand for reduced-risk tobacco products such as e-cigarettes and smokeless tobacco. Government regulations may continue to challenge traditional cigarette consumption; however, companies are likely to invest heavily in alternative products and marketing strategies to align with the changing regulatory landscape. This dynamic will lead to a more innovative market with new opportunities for local and international players.

Market Opportunities

|

||

|

By Distribution Channel |

Online Retail Supermarkets/Hypermarkets Tobacco Specialty Stores Convenience Stores Duty-Free Retail |

|

|

By Consumer Age Group |

18-24 Years 25-34 Years 35-44 Years 45+ Years |

|

|

By Nicotine Content |

Low Nicotine Medium Nicotine High Nicotine |

|

|

By Region |

North East West South |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers (Tobacco Consumption Trends, Economic Factors, Cultural Preferences) 3.1.1. High Consumer Demand

3.1.2. Increased Disposable Income

3.1.3. Influence of Cultural and Social Norms

3.1.4. Economic Diversification Efforts

3.2. Market Challenges (Government Regulations, Health Awareness, Illicit Trade) 3.2.1. Stringent Government Regulations

3.2.2. Public Health Campaigns and Awareness

3.2.3. Illicit Trade and Counterfeiting

3.2.4. Shifting Consumer Preferences to Alternatives (e.g., E-cigarettes, Nicotine Pouches)

3.3. Opportunities (Product Diversification, Innovation, New Market Entrants) 3.3.1. Innovation in Flavored Tobacco Products

3.3.2. Expansion of Reduced-Risk Products

3.3.3. Market Penetration in Underdeveloped Regions

3.3.4. Partnerships with Global Tobacco Companies

3.4. Trends (Digitalization, Retail Growth, Shift Toward Reduced-Risk Products) 3.4.1. Increased Digital Marketing and Online Sales Channels

3.4.2. Growth of Premium and Luxury Tobacco Brands

3.4.3. Rise in Demand for Organic and Sustainable Tobacco Products

3.4.4. Retail Expansion in Rural Areas

3.5. Government Regulation (Health Policies, Import Tariffs, Advertising Restrictions) 3.5.1. National Tobacco Control Program

3.5.2. Import Regulations and Excise Duties

3.5.3. Advertising Bans and Labeling Requirements

3.5.4. Public Smoking Bans

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Cigarettes

4.1.2. Cigars

4.1.3. Smokeless Tobacco (Chewing Tobacco, Snuff)

4.1.4. Roll-Your-Own (RYO) Tobacco

4.1.5. E-Cigarettes and Vaping Products

4.2. By Distribution Channel (In Value %)

4.2.1. Online Retail

4.2.2. Supermarkets/Hypermarkets

4.2.3. Tobacco Specialty Stores

4.2.4. Convenience Stores

4.2.5. Duty-Free Retail

4.3. By Consumer Age Group (In Value %)

4.3.1. 18-24 Years

4.3.2. 25-34 Years

4.3.3. 35-44 Years

4.3.4. 45+ Years

4.4. By Region (In Value %)

4.4.1. North

4.4.2. South

4.4.3. East

4.4.4. West

4.5. By Nicotine Content (In Value %)

4.5.1. Low Nicotine

4.5.2. Medium Nicotine

4.5.3. High Nicotine

5.1. Detailed Profiles of Major Companies

5.1.1. British American Tobacco

5.1.2. Philip Morris International

5.1.3. Japan Tobacco International

5.1.4. Imperial Brands

5.1.5. Al Nakhla Tobacco Co.

5.1.6. Al Fakher Tobacco

5.1.7. Eastern Tobacco Company

5.1.8. Altadis

5.1.9. Scandinavian Tobacco Group

5.1.10. Altria Group Inc.

5.1.11. Reynolds American Inc.

5.1.12. KT&G Corporation

5.1.13. ITC Limited

5.1.14. Godfrey Phillips India

5.1.15. Vype (BATs Subsidiary)

5.2. Cross Comparison Parameters (Revenue, Market Share, Nicotine Alternatives Portfolio, Global Reach, Market Penetration Rate, Distribution Network, Number of Employees, Inception Year)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Health and Safety Standards

6.2. Compliance and Certification Requirements

6.3. Advertising and Marketing Restrictions

6.4. Environmental Regulations

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By Consumer Age Group (In Value %)

8.4. By Region (In Value %)

8.5. By Nicotine Content (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Behavior and Cohort Analysis

9.3. Marketing and Branding Initiatives

9.4. White Space Opportunity Analysis

The initial stage includes mapping out the major stakeholders within the Saudi Arabia tobacco market. Desk research forms the foundation, utilizing secondary and proprietary data sources to identify critical variables such as consumption trends, retail channels, and market regulations.

This step involves analyzing historical data, including the penetration of various tobacco products, sales performance by region, and consumer demographics. We compile and evaluate service quality metrics to provide an accurate estimate of revenue generation in the market.

Market assumptions are validated through interviews with industry experts and professionals. This allows us to refine the data and ensure that our analysis reflects the actual market environment and competitive dynamics.

The final step involves synthesizing the data collected and validated to generate a comprehensive analysis. This includes integrating insights from local tobacco companies and international brands to verify key statistics and trends shaping the market.

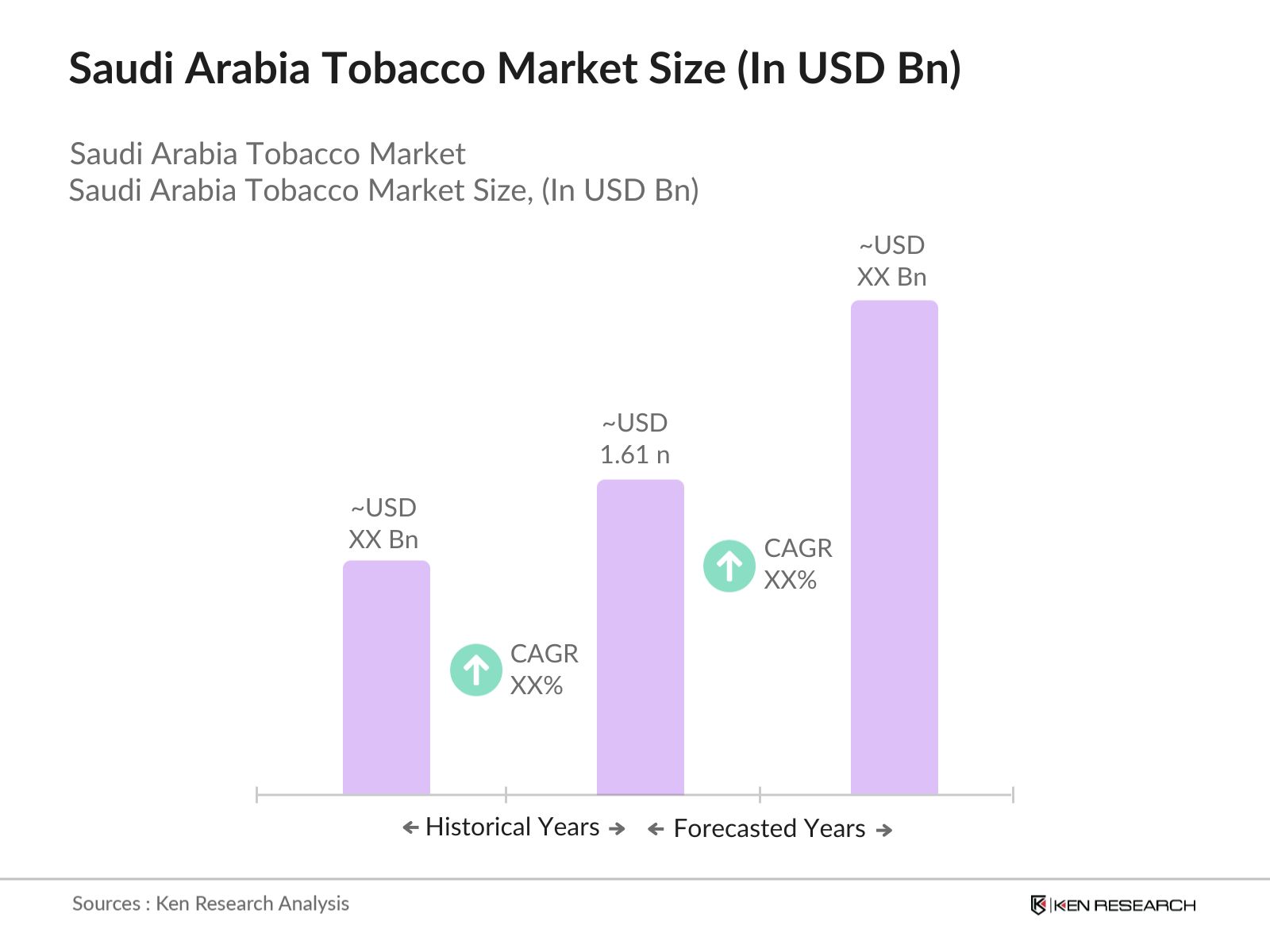

The Saudi Arabia tobacco market is valued at USD 1.61 billion, driven by the widespread use of cigarettes, shisha, and the increasing popularity of reduced-risk products such as e-cigarettes.

Challenges in Saudi Arabia tobacco market include stringent government regulations, increasing public awareness of health risks, and the growing influence of anti-smoking campaigns which could reduce cigarette consumption in the long term.

Key players in Saudi Arabia tobacco market include British American Tobacco, Philip Morris International, Japan Tobacco International, Al Nakhla Tobacco Co., and Imperial Brands, all of which maintain a strong presence in the market through product innovation and extensive distribution networks.

Saudi Arabia tobacco market Growth is driven by high consumer demand for cigarettes and shisha, increased disposable income, and the introduction of reduced-risk products like e-cigarettes, which are gaining popularity due to their perceived lower health risks.

Riyadh, Jeddah, and the Eastern Province dominate the Saudi Arabia tobacco market due to their large populations, strong consumer spending, and well-established retail and distribution networks, especially for premium tobacco products.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.