Saudi Arabia Ultrasound Devices Market Outlook to 2030

Region:Saudi Arabia

Author(s):Sanjeev

Product Code:KROD7503

Region:Saudi Arabia

Author(s):Sanjeev

Product Code:KROD7503

November 2024

95

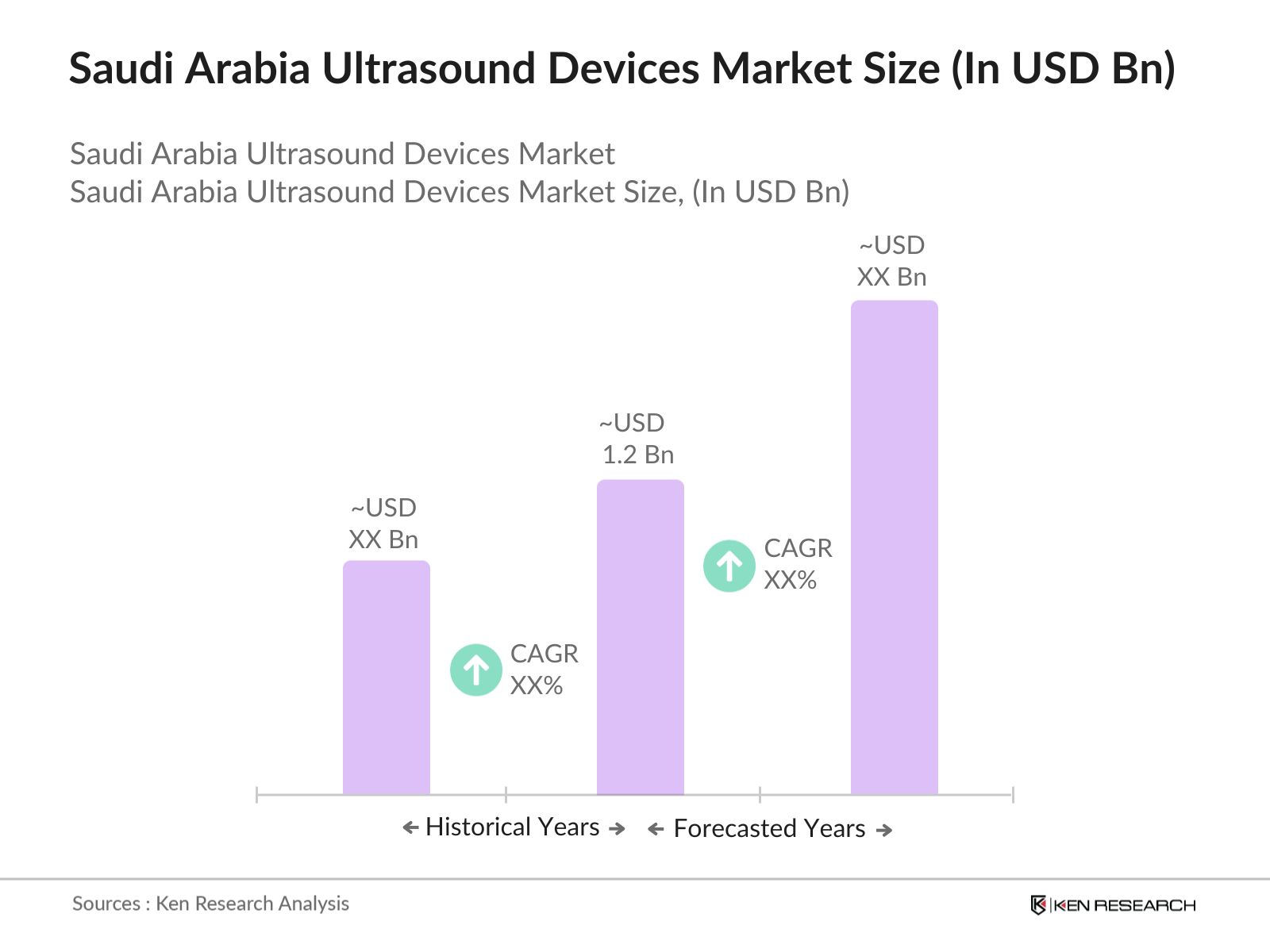

The Saudi Arabia Ultrasound Devices market is segmented by product type and by end-user.

The Saudi Arabia Ultrasound Devices market is characterized by the dominance of both international and regional players. Leading companies drive innovation while capitalizing on distribution networks and customer trust. The market exhibits significant consolidation, with top firms leveraging their technological advancements and local partnerships.

Over the next five years, the Saudi Arabia Ultrasound Devices market is anticipated to witness robust growth driven by continued government investments in healthcare infrastructure, increased adoption of AI-powered imaging, and a growing focus on telemedicine and point-of-care diagnostics. Rising demand for advanced portable ultrasound devices and emerging applications in cardiology and emergency medicine will further propel market expansion.

|

Diagnostic Ultrasound Systems |

|||

|

By Portability |

Trolley/Cart-Based Ultrasound Devices |

||

|

By Display Type |

Colored Ultrasound Devices |

||

|

By Application |

Radiology |

||

|

By Region |

North East West South |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rising Prevalence of Chronic Diseases

3.1.2. Technological Advancements in Ultrasound Imaging

3.1.3. Government Initiatives and Healthcare Infrastructure Development

3.1.4. Increasing Demand for Point-of-Care Diagnostics

3.2. Market Challenges

3.2.1. High Cost of Advanced Ultrasound Devices

3.2.2. Limited Skilled Workforce

3.2.3. Regulatory and Compliance Issues

3.3. Opportunities

3.3.1. Expansion into Rural and Underserved Areas

3.3.2. Integration of Artificial Intelligence in Ultrasound Imaging

3.3.3. Growth in Medical Tourism

3.4. Trends

3.4.1. Adoption of Portable and Handheld Ultrasound Devices

3.4.2. Increasing Use in Pre-hospital and Emergency Care

3.4.3. Development of 3D and 4D Imaging Technologies

3.5. Government Regulations

3.5.1. Saudi Food and Drug Authority (SFDA) Guidelines

3.5.2. National Health Transformation Program

3.5.3. Vision 2030 Healthcare Objectives

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape

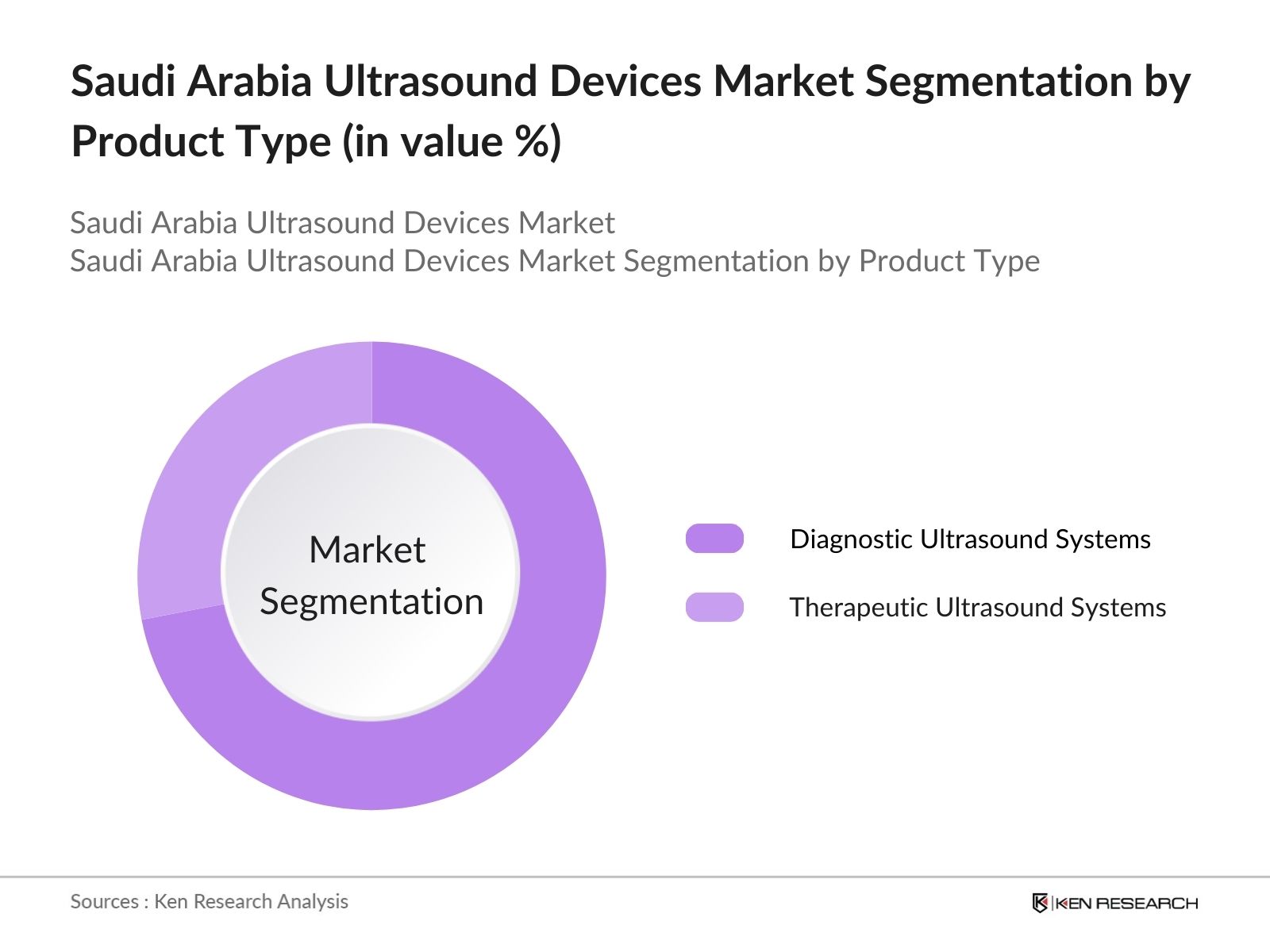

4.1. By Product Type (Value %)

4.1.1. Diagnostic Ultrasound Systems

4.1.2. Therapeutic Ultrasound Systems

4.2. By Portability (Value %)

4.2.1. Trolley/Cart-Based Ultrasound Devices

4.2.2. Compact/Handheld Ultrasound Devices

4.3. By Display Type (Value %)

4.3.1. Colored Ultrasound Devices

4.3.2. Black & White Ultrasound Devices

4.4. By Application (Value %)

4.4.1. Radiology

4.4.2. Cardiology

4.4.3. Obstetrics & Gynecology

4.4.4. Gastroenterology

4.4.5. Urology

4.4.6. Others

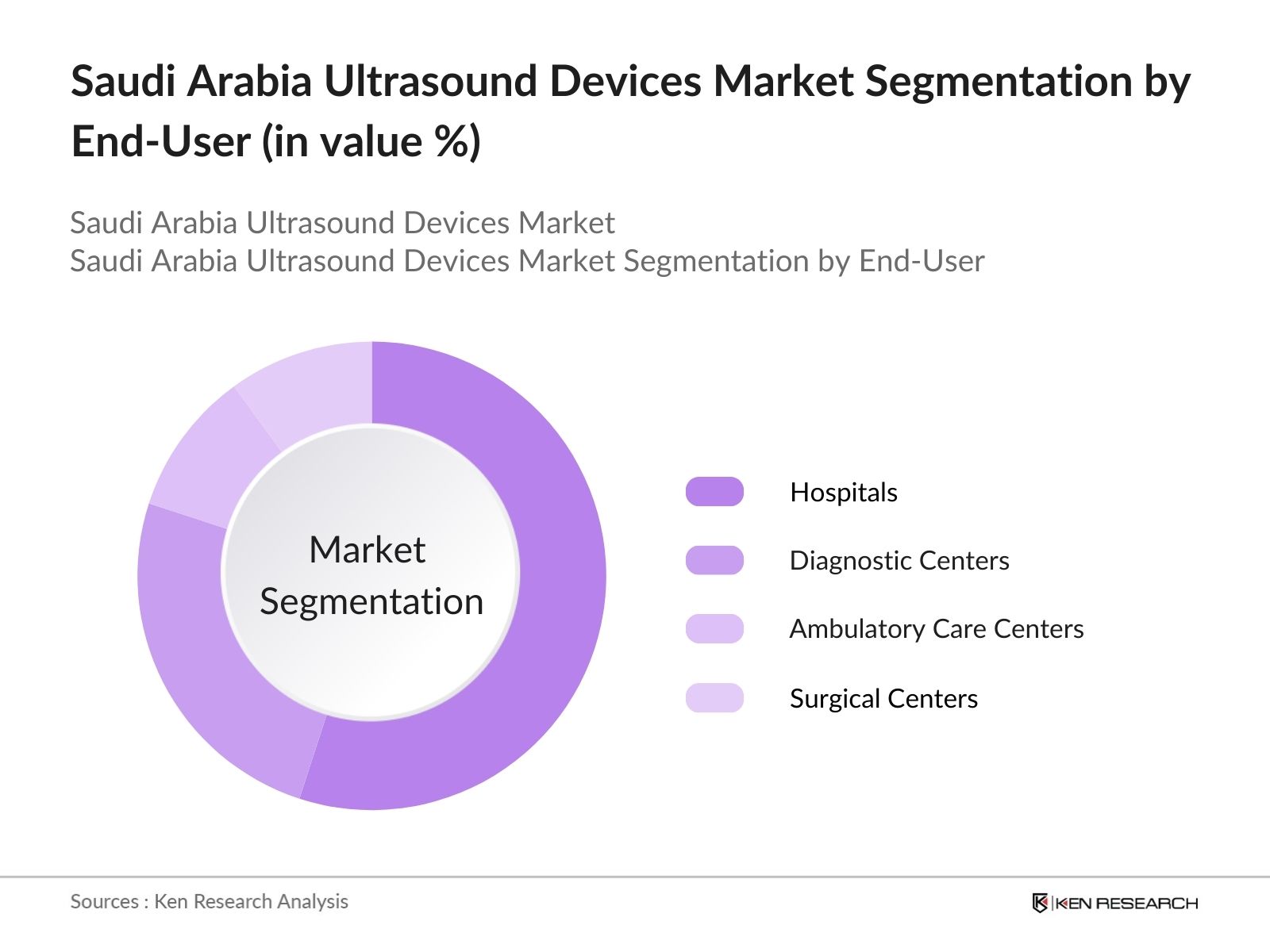

4.5. By End-User (Value %)

4.5.1. Hospitals

4.5.2. Diagnostic Centers

4.5.3. Ambulatory Care Centers

4.5.4. Surgical Centers

4.5.5. Others

4.6. By Distribution Channel (Value %)

4.6.1. Online

4.6.2. Offline

4.7. By Region (Value %)

4.7.1. South

4.7.2. West

4.7.3. North

4.7.4. East

5.1. Detailed Profiles of Major Companies

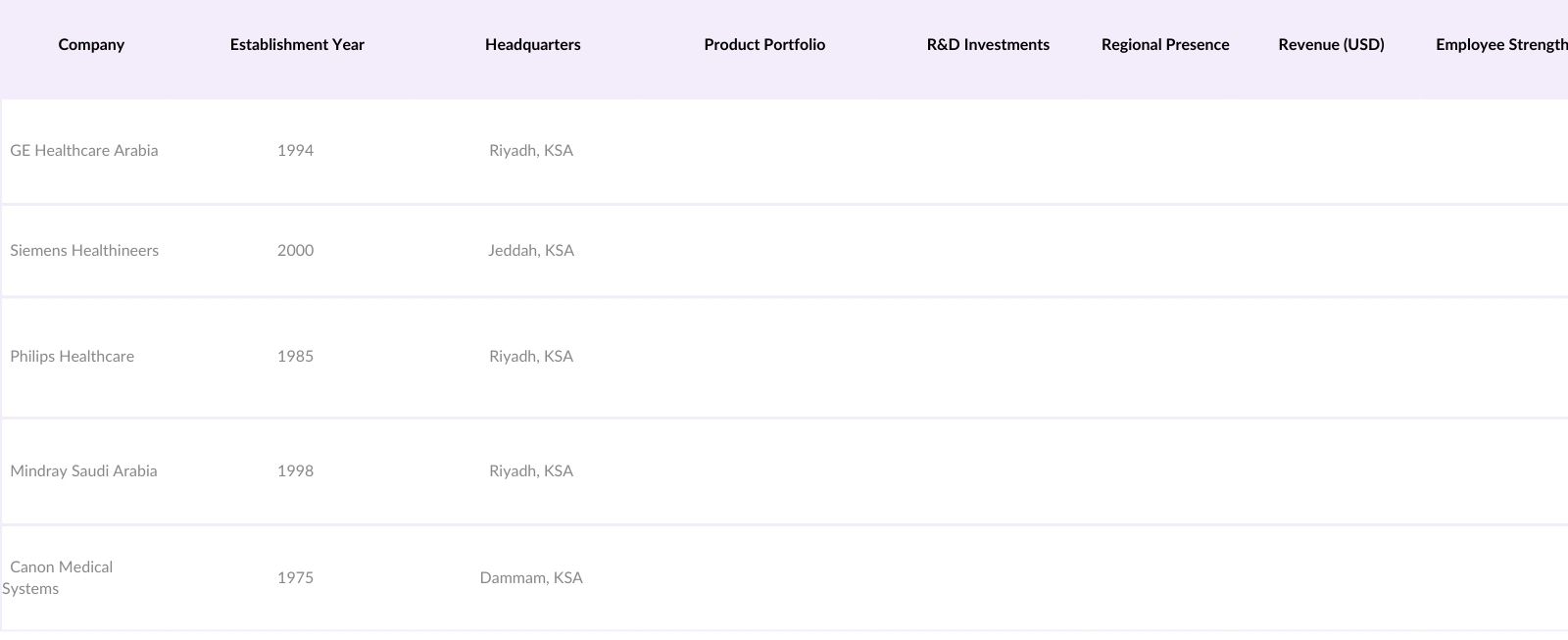

5.1.1. GE Healthcare Arabia Ltd.

5.1.2. Siemens Ltd Saudi Arabia

5.1.3. Philips Healthcare Saudi Arabia Ltd.

5.1.4. Hitachi Medical Systems Saudi Arabia

5.1.5. Mindray Saudi Arabia

5.1.6. Fujifilm-Middle East

5.1.7. Shimadzu Middle East & Africa FZE

5.1.8. Gulf Medical Co Ltd.

5.1.9. Hologic, Inc.

5.1.10. Canon Medical Systems Saudi Arabia

5.1.11. Esaote SpA

5.1.12. Samsung Medison Co., Ltd.

5.1.13. Al Faisaliah Medical Systems

5.1.14. Al Zahrawi Medical Supplies

5.1.15. Al Maarefa Medical Supplies

5.2. Cross Comparison Parameters

5.2.1. Number of Employees

5.2.2. Headquarters Location

5.2.3. Year of Establishment

5.2.4. Revenue

5.2.5. Product Portfolio

5.2.6. Market Share

5.2.7. Regional Presence

5.2.8. Strategic Initiatives

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.6.1. Venture Capital Funding

5.6.2. Government Grants

5.6.3. Private Equity Investments

6.1. Saudi Food and Drug Authority (SFDA) Regulations

6.2. Compliance Requirements for Medical Devices

6.3. Certification Processes and Standards

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (Value %)

8.2. By Portability (Value %)

8.3. By Display Type (Value %)

8.4. By Application (Value %)

8.5. By End-User (Value %)

8.6. By Distribution Channel (Value %)

8.7. By Region (Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Market Penetration Strategies

9.4. White Space Opportunity Analysis

9.5. Go-to-Market Strategies

9.6. Product Differentiation Insights

9.7. Regional Market Entry Strategies

Disclaimer Contact UsWe constructed an ecosystem map incorporating stakeholders, including healthcare providers, device manufacturers, and regulatory authorities, in the Saudi Arabia Ultrasound Devices Market. This step utilized proprietary databases and secondary research to determine critical market variables.

Comprehensive analysis of historical data was conducted to understand market penetration, device adoption rates, and revenue trends. This included evaluating service quality metrics to ensure precise revenue estimates.

Market hypotheses were validated through in-depth interviews with industry experts and practitioners, providing operational and financial insights. These insights were instrumental in refining market data.

Detailed insights from device manufacturers and healthcare providers were incorporated to verify and complement the analysis. This ensured an accurate and validated understanding of market dynamics.

The Saudi Arabia Ultrasound Devices market is valued at USD 1.2 billion, supported by increasing demand for diagnostic and therapeutic imaging solutions and extensive healthcare investments.

Challenges include high costs of advanced imaging systems, lack of skilled professionals, and regulatory compliance hurdles.

Key players include GE Healthcare Arabia, Siemens Healthineers, Philips Healthcare, Mindray Saudi Arabia, and Canon Medical Systems, known for their innovative technologies and strong market presence.

The market is propelled by government initiatives, increased prevalence of chronic diseases, advancements in imaging technology, and growing demand for portable and point-of-care devices.

Central and Western regions, including Riyadh and Jeddah, dominate due to advanced healthcare facilities, high population density, and substantial public and private investments.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.