UAE Adhesives Market Outlook to 2030

Region:Middle East

Author(s):Vijay Kumar

Product Code:KROD5178

December 2024

97

About the Report

UAE Adhesives Market Overview

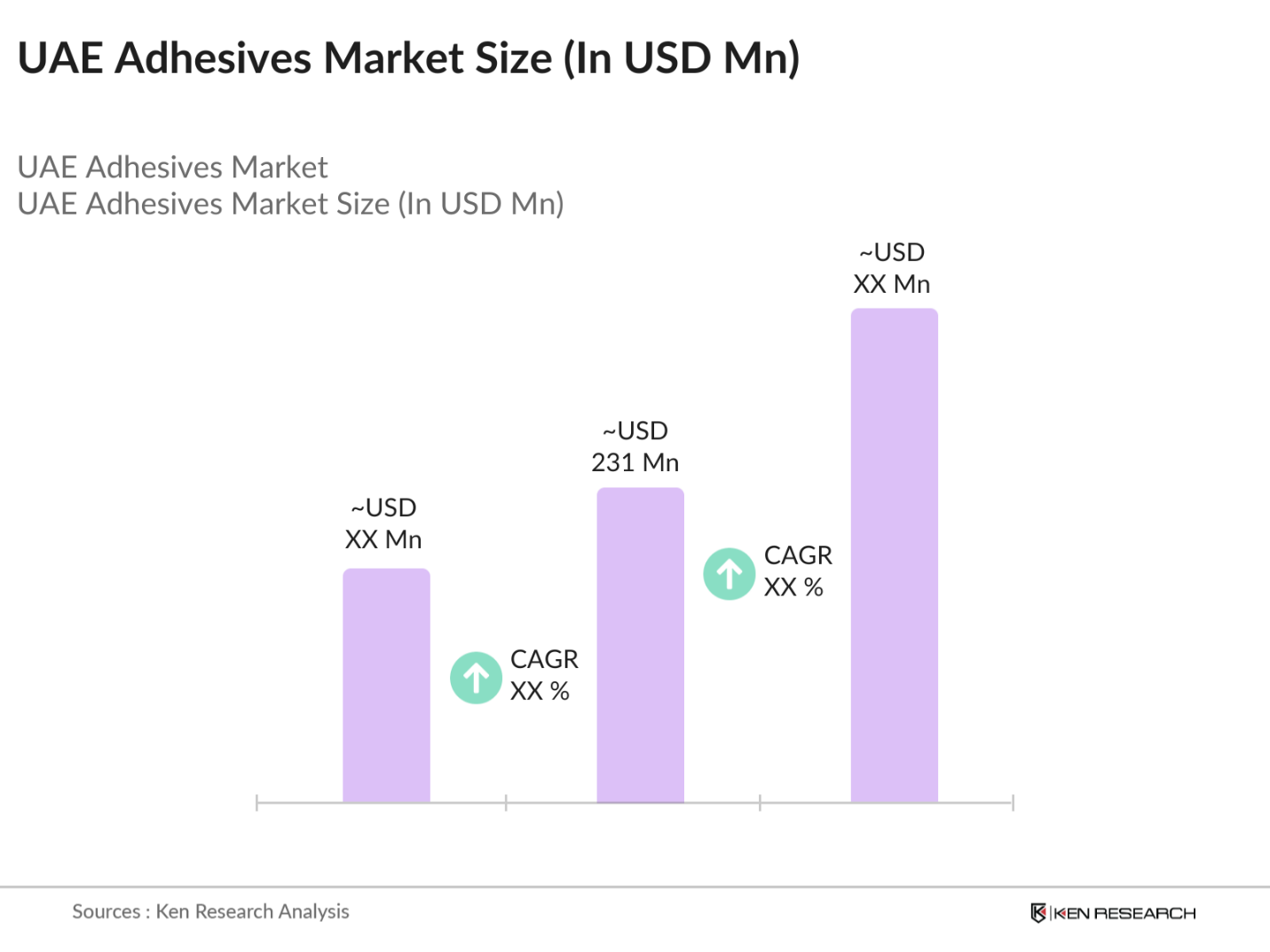

- The UAE Adhesives market is valued at USD 231 million, based on a five-year historical analysis. This market is primarily driven by the growing demand from the construction and automotive industries, fueled by large-scale infrastructure projects and the increasing use of adhesives in automotive manufacturing for lightweighting and durability. The rise of sustainable construction practices and the shift towards green building materials have also spurred the demand for advanced adhesive technologies, particularly in applications such as flooring, insulation, and structural bonding.

- Dominant cities like Dubai and Abu Dhabi lead the UAE adhesives market due to their advanced infrastructure and massive construction projects. These cities are major hubs for real estate development, with ongoing projects like Expo 2020 and urban transformation initiatives. Additionally, their established automotive, aerospace, and packaging industries further cement their dominance in the market, making them key contributors to overall adhesive consumption in the UAE.

- The UAE government enforces strict environmental protection regulations, particularly regarding the use of hazardous materials in adhesives. In 2023, the Ministry of Climate Change and Environment set new limits on the permissible levels of VOCs in adhesive products to align with the country's sustainability goals. These regulations mandate that adhesive manufacturers reduce emissions, with a significant push toward water-based and bio-based alternatives.

UAE Adhesives Market Segmentation

By Resin Type: The market is segmented by resin type into acrylic adhesives, polyurethane adhesives, epoxy adhesives, rubber-based adhesives, and silicone adhesives. Recently, polyurethane adhesives have shown a dominant market share within this segmentation. The rise in demand for these adhesives is largely due to their excellent durability, flexibility, and heat resistance, making them ideal for use in construction and automotive applications.

By End-Use Industry: The market is also segmented by end-use industry into construction, packaging, automotive and aerospace, healthcare, and electronics. The construction industry holds the largest share in this segmentation. The rapid urbanization and massive investments in infrastructure development across Dubai, Abu Dhabi, and other emirates drive the demand for adhesives in flooring, roofing, insulation, and other structural applications.

UAE Adhesives Market Competitive Landscape

The UAE adhesives market is characterized by the presence of both global and regional players, including multinational giants like Henkel and 3M, as well as local manufacturers such as RAK Ceramics. The industry is highly competitive, with companies vying for market dominance through innovations in adhesive technology, expanding product lines, and offering sustainable solutions. Companies such as Sika AG and H.B. Fuller have invested heavily in research and development to offer high-performance, eco-friendly adhesives tailored to the construction and automotive sectors.

UAE Adhesives Industry Analysis

Growth Drivers

- Rapid Urbanization and Infrastructure Development: The UAE's urbanization is accelerating, with over 88% of the population living in urban areas by 2024, driven by the construction of large-scale projects like the Dubai South project and Abu Dhabi's urban expansion. This growth in infrastructure directly impacts the adhesives market, as adhesives play a critical role in construction activities, including flooring, tiling, and insulation. According to the UAE Federal Competitiveness and Statistics Authority, the construction sector contributed over $110 billion to the economy in 2023, necessitating a surge in adhesive applications.

- Increased Demand in the Automotive and Aerospace Sectors: The UAE's automotive sector produced over 300,000 vehicles in 2023, with increasing demand for lightweight materials that require high-performance adhesives. Additionally, the aerospace industry is expanding with Emirates Airlines and Etihad Airways driving demand for adhesive technologies for aircraft assembly and maintenance. Adhesives are essential in reducing vehicle and aircraft weight, thereby improving fuel efficiency. In 2023, the UAE aerospace sector alone attracted investments of approximately $6.5 billion, driving adhesive demand.

- Rise in Packaging and Construction Activities: With a sharp increase in e-commerce, the UAE's packaging industry saw a rise in adhesive use, especially in sustainable packaging solutions. The UAE Ministry of Economy noted that over 250 million parcels were processed in 2023, further driving adhesive consumption. Furthermore, the ongoing construction projects, including residential, commercial, and industrial buildings, increased demand for construction adhesives in tiling, plumbing, and installation.

Market Challenges

- Volatile Raw Material Prices (Petrochemical-Derived Inputs): The UAE heavily relies on petrochemical-based raw materials for adhesive production, which are subject to volatile global oil prices. In 2023, the price of crude oil fluctuated between $70 and $90 per barrel, leading to unpredictable costs in the adhesive production chain. This volatility affects manufacturers' profit margins and leads to price uncertainty in adhesive products. Additionally, disruptions in the global supply chain due to geopolitical tensions have further strained raw material availability.

- Environmental Regulations (VOC Content in Adhesives): The UAEs Ministry of Climate Change and Environment has implemented stringent regulations to limit volatile organic compounds (VOCs) in adhesive products, requiring manufacturers to innovate and produce eco-friendly alternatives. In 2023, the UAE set a maximum limit of 5% VOC content in adhesives to minimize environmental impact, aligning with the country's Net Zero by 2050 initiative.

UAE Adhesives Market Future Outlook

Over the next five years, the UAE adhesives market is expected to experience significant growth, driven by ongoing advancements in adhesive technologies, increased demand from the construction and automotive industries, and the introduction of eco-friendly and sustainable adhesive solutions. As Dubai and Abu Dhabi continue to witness massive infrastructural development projects, demand for high-performance adhesives in structural applications is likely to surge. Moreover, the government's push toward sustainable construction practices and local manufacturing will foster a conducive environment for growth in this market.

Market Opportunities

- Growth of Eco-Friendly Adhesives: In 2023, the UAE saw a 20% increase in demand for eco-friendly adhesives, particularly in construction and packaging industries. The UAE governments focus on sustainable development, underlined by the Net Zero by 2050 initiative, has driven manufacturers to innovate in bio-based and water-based adhesive products. Adhesive manufacturers are responding by increasing their production capacity of eco-friendly alternatives, bolstered by government support, which has provided over $1 billion in sustainability funding in 2023.

- Adoption of Advanced Adhesive Technologies (Reactive and Hot Melt): The demand for reactive and hot melt adhesives has been growing rapidly, particularly in automotive and aerospace sectors. In 2023, over 50,000 tons of hot melt adhesives were consumed in these sectors in the UAE, due to their superior performance in extreme conditions. With the UAE's strong push for innovation, manufacturers are increasingly adopting these advanced adhesive technologies to meet high-performance requirements.

Scope of the Report

|

Resin Type |

Acrylic Adhesives Polyurethane Adhesives Epoxy Adhesives Rubber-Based Adhesives Silicone Adhesives |

|

Technology |

Solvent-Based Water-Based Hot Melt Reactive |

|

End-Use Industry |

Construction Packaging Automotive and Aerospace Healthcare and Medical Devices Electronics and Appliances |

|

Application |

Structural Adhesives Non-Structural Adhesives Pressure-Sensitive Adhesives Flooring and Tiling Adhesives |

|

Region |

Dubai Abu Dhabi Sharjah Northern Emirates |

Products

Key Target Audience

Adhesive Manufacturers

Construction and Infrastructure Companies

Automotive and Aerospace Manufacturers

Healthcare and Medical Device Manufacturers

Electronics Manufacturers

Packaging Companies

Government and Regulatory Bodies (e.g., UAE Ministry of Climate Change and Environment, Emirates Authority for Standardization and Metrology)

Investment and Venture Capital Firms

Companies

Players Mentioned in the Report

Henkel AG & Co. KGaA

H.B. Fuller

Sika AG

Dow Chemical Company

3M Company

Huntsman Corporation

Bostik (Arkema Group)

Avery Dennison Corporation

Wacker Chemie AG

Ashland Global Holdings Inc.

Table of Contents

1. UAE Adhesives Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. UAE Adhesives Market Size (In AED Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. UAE Adhesives Market Analysis

3.1. Growth Drivers

3.1.1. Rapid Urbanization and Infrastructure Development

3.1.2. Increased Demand in the Automotive and Aerospace Sectors

3.1.3. Rise in Packaging and Construction Activities

3.1.4. Government Initiatives Supporting Local Manufacturing

3.2. Market Challenges

3.2.1. Volatile Raw Material Prices (Petrochemical-Derived Inputs)

3.2.2. Environmental Regulations (VOC Content in Adhesives)

3.2.3. Technological Gaps in Adhesive Application Processes

3.3. Opportunities

3.3.1. Growth of Eco-Friendly Adhesives

3.3.2. Adoption of Advanced Adhesive Technologies (Reactive and Hot Melt)

3.3.3. Partnerships with Sustainable Packaging Manufacturers

3.3.4. Expansion of the Healthcare Adhesive Segment

3.4. Trends

3.4.1. Increasing Use of Bio-Based Adhesives

3.4.2. Shift Towards Lightweight Adhesive Solutions in Automotives

3.4.3. Demand for High-Performance Adhesives in Electronics

3.4.4. Rising Adoption of Smart Adhesive Technologies

3.5. Government Regulations

3.5.1. UAE Environmental Protection Regulations

3.5.2. Emirates Quality Mark Certification for Adhesive Products

3.5.3. Restrictions on Hazardous Chemicals in Adhesive Manufacturing

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Manufacturers, Distributors, End-Users)

3.8. Porters Five Forces Analysis

3.9. Competitive Ecosystem

4. UAE Adhesives Market Segmentation

4.1. By Resin Type (In Value %)

4.1.1. Acrylic Adhesives

4.1.2. Polyurethane Adhesives

4.1.3. Epoxy Adhesives

4.1.4. Rubber-Based Adhesives

4.1.5. Silicone Adhesives

4.2. By Technology (In Value %)

4.2.1. Solvent-Based

4.2.2. Water-Based

4.2.3. Hot Melt

4.2.4. Reactive

4.3. By End-Use Industry (In Value %)

4.3.1. Construction

4.3.2. Packaging

4.3.3. Automotive and Aerospace

4.3.4. Healthcare and Medical Devices

4.3.5. Electronics and Appliances

4.4. By Application (In Value %)

4.4.1. Structural Adhesives

4.4.2. Non-Structural Adhesives

4.4.3. Pressure-Sensitive Adhesives

4.4.4. Flooring and Tiling Adhesives

4.5. By Region (In Value %)

4.5.1. Dubai

4.5.2. Abu Dhabi

4.5.3. Sharjah

4.5.4. Northern Emirates

5. UAE Adhesives Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. H.B. Fuller

5.1.2. Henkel AG & Co. KGaA

5.1.3. Sika AG

5.1.4. 3M Company

5.1.5. Huntsman Corporation

5.1.6. Bostik (Arkema Group)

5.1.7. Avery Dennison Corporation

5.1.8. Ashland Global Holdings Inc.

5.1.9. Dow Chemical Company

5.1.10. Wacker Chemie AG

5.1.11. ITW Performance Polymers

5.1.12. BASF SE

5.1.13. Pidilite Industries

5.1.14. Lord Corporation

5.1.15. Eastman Chemical Company

5.2 Cross Comparison Parameters (No. of Employees, Revenue, R&D Investments, Adhesive Technology Portfolio, Production Facilities, Sustainability Initiatives, Global Presence, Certifications)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Incentives and Support

6. UAE Adhesives Market Regulatory Framework

6.1. Compliance with Environmental and Safety Standards

6.2. Certification Processes for Industrial and Consumer Adhesives

6.3. Local Content Requirements for Adhesive Manufacturing

7. UAE Adhesives Future Market Size (In AED Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. UAE Adhesives Future Market Segmentation

8.1. By Resin Type (In Value %)

8.2. By Technology (In Value %)

8.3. By End-Use Industry (In Value %)

8.4. By Application (In Value %)

8.5. By Region (In Value %)

9. UAE Adhesives Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Emerging Market Trends and Technologies

9.3. Marketing and Distribution Strategies

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The research process began with identifying the primary stakeholders in the UAE adhesives market, such as adhesive manufacturers, end-users in various industries, and regulatory authorities. Extensive secondary research was conducted to map the ecosystem and pinpoint the major factors driving market dynamics, including technological innovations and regulatory requirements.

Step 2: Market Analysis and Construction

In this phase, we gathered and analyzed historical data from proprietary databases and public sources to evaluate the market size, revenue generation, and industry trends. Particular attention was paid to the distribution channels and key end-use industries, ensuring that the final output reflected a comprehensive understanding of the market landscape.

Step 3: Hypothesis Validation and Expert Consultation

To validate our hypotheses, interviews were conducted with industry experts, including adhesive manufacturers and distributors, who provided insights into the latest market developments and future trends. Their feedback helped refine our projections and added depth to the qualitative data collected during the research process.

Step 4: Research Synthesis and Final Output

The final phase involved compiling all the data into a cohesive report that accurately represented the state of the UAE adhesives market. Insights from both the bottom-up and top-down approaches were integrated to ensure the findings were both detailed and accurate. Additionally, primary data gathered through expert consultations was cross-referenced to validate market trends and growth drivers.

Frequently Asked Questions

01. How big is the UAE Adhesives Market?

The UAE Adhesives market is valued at USD 231 million, based on a five-year historical analysis. This market is primarily driven by the growing demand from the construction and automotive industries, fueled by large-scale infrastructure projects and the increasing use of adhesives in automotive manufacturing for lightweighting and durability.

02. What are the challenges in the UAE Adhesives Market?

Challenges in the UAE adhesives market include volatile raw material prices, environmental regulations related to VOC emissions, and technological gaps in advanced adhesive applications. These factors impact production costs and compliance requirements for manufacturers.

03. Who are the major players in the UAE Adhesives Market?

Key players in the UAE adhesives market include Henkel AG & Co. KGaA, H.B. Fuller, Sika AG, Dow Chemical Company, and 3M. These companies dominate due to their extensive product portfolios, R&D investments, and global reach.

04. What are the growth drivers of the UAE Adhesives Market?

The market is driven by the rapid development of the construction sector, increasing demand for lightweight materials in automotive and aerospace industries, and advancements in eco-friendly adhesive technologies.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.