UAE Fintech Market Outlook to 2030

Region:United Arab Emirates

Author(s):Shreya

Product Code:KROD5183

Region:United Arab Emirates

Author(s):Shreya

Product Code:KROD5183

November 2024

89

The UAE fintech market is dominated by a blend of local startups and global companies. The sector has seen consolidation, with major players leading the charge in innovation and service provision. For instance, Dubai-based YAP has rapidly emerged as a leader in digital banking, offering a comprehensive suite of financial services to individuals and businesses alike. Similarly, foreign players like Payfort (now part of Amazon) have established a strong presence in the market, capitalizing on the rapid growth of e-commerce in the region. This consolidation highlights the influence of key players in shaping the UAE fintech market.

Competitive Landscape Table

|

Company Name |

Established |

Headquarters |

Technology Stack |

User Base |

Revenue s |

Key Partnerships |

VC Funding |

Product Focus |

|---|---|---|---|---|---|---|---|---|

|

Network International |

1994 |

Dubai |

||||||

|

Payfort (Amazon) |

2013 |

Dubai |

||||||

|

YAP |

2020 |

Dubai |

||||||

|

Mamo Pay |

2019 |

Dubai |

||||||

|

Beehive |

2014 |

Dubai |

Growth Drivers

Market Challenges

The UAE fintech market is expected to experience robust growth over the next five years, driven by increasing consumer demand for digital financial services and strong government support for innovation. The adoption of blockchain technology, AI, and digital payment solutions is anticipated to expand further, with government initiatives such as the National Artificial Intelligence Strategy and the Dubai Blockchain Strategy fostering innovation. Moreover, regulatory frameworks like the DIFC and ADGM's regulatory sandbox environments will continue to attract international fintech firms, facilitating the growth of cross-border payments and seamless integration of financial technologies.

Market Opportunities

|

Segments |

Sub-Segments |

|---|---|

|

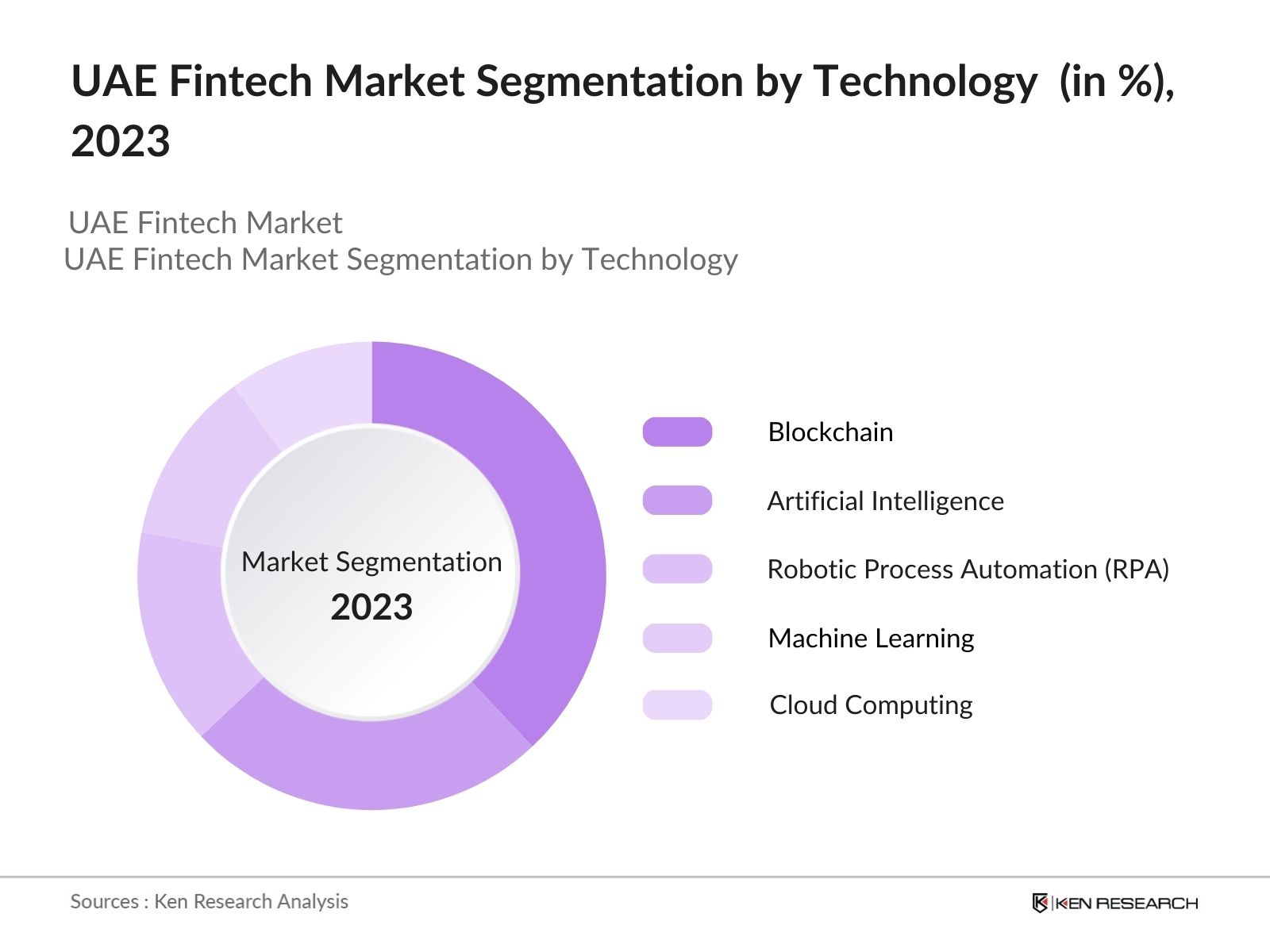

By Technology |

Blockchain Artificial Intelligence Robotic Process Automation Machine Learning Cloud Computing |

|

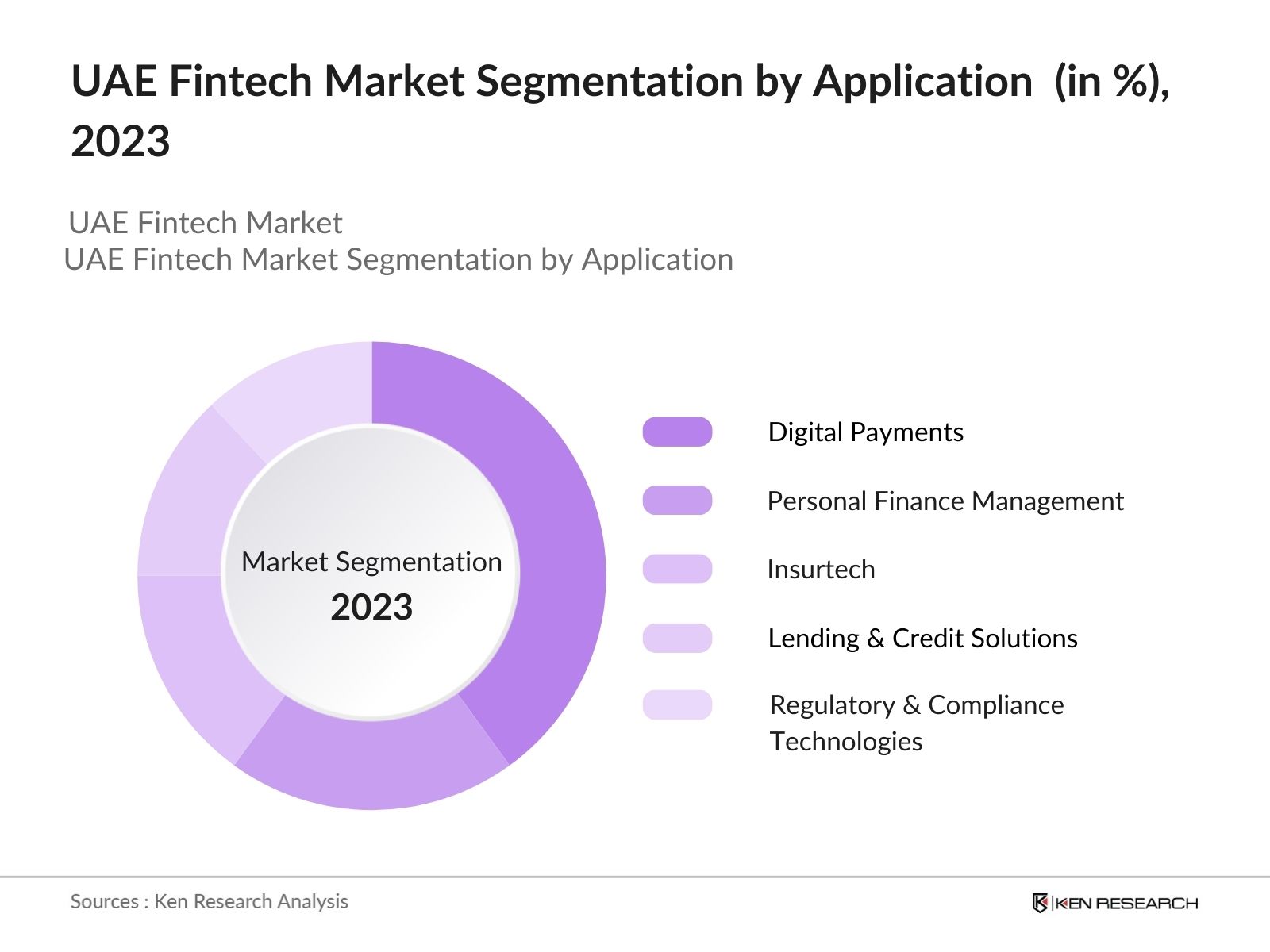

By Application |

Digital Payments Personal Finance Management Insurtech Lending & Credit Solutions Regulatory & Compliance Technologies |

|

By Deployment Mode |

On-Premise Solutions Cloud-Based Solutions |

|

By End-User |

Retail Banking Corporate Banking Wealth Management Insurance Companies SMEs & Startups |

|

By Region |

Abu Dhabi Dubai Sharjah Ras Al Khaimah Fujairah |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Increased Adoption of Digital Payments (Mobile Wallet Transactions, E-commerce Transactions)

3.1.2 Government Initiatives (Smart Dubai, Fintech Regulatory Sandbox)

3.1.3 Technological Advancements (AI in Banking, Blockchain-based Solutions)

3.1.4 Rise of Financial Inclusion (Unbanked and Underbanked Populations, Digital Banking)

3.2 Market Challenges

3.2.1 Regulatory Hurdles (Licensing, Compliance Requirements)

3.2.2 Cybersecurity Threats (Data Breaches, Fraud Risks)

3.2.3 Limited Consumer Trust in Digital-Only Platforms

3.3 Opportunities

3.3.1 Growing Venture Capital Investments

3.3.2 Strategic International Collaborations (Cross-Border Payment Solutions)

3.3.3 Emergence of Islamic Fintech (Sharia-Compliant Digital Services)

3.4 Trends

3.4.1 Growth of Digital-Only Banks (Neo Banks)

3.4.2 Integration of AI and Machine Learning in Risk Management

3.4.3 Expansion of Buy-Now-Pay-Later (BNPL) Services

3.5 Government Regulation

3.5.1 Central Bank of UAE Digital Payment Regulations

3.5.2 DIFC Regulatory Framework for Fintech Startups

3.5.3 Data Privacy Laws (UAE Personal Data Protection Law)

3.6 SWOT Analysis

3.7 Stake Ecosystem

3.8 Porters Five Forces

3.9 Competition Ecosystem

4.1 By Technology (In Value %)

4.1.1 Blockchain

4.1.2 Artificial Intelligence

4.1.3 Robotic Process Automation

4.1.4 Machine Learning

4.1.5 Cloud Computing

4.2 By Application (In Value %)

4.2.1 Digital Payments

4.2.2 Personal Finance Management

4.2.3 Insurtech

4.2.4 Lending & Credit Solutions

4.2.5 Regulatory & Compliance Technologies

4.3 By Deployment Mode (In Value %)

4.3.1 On-Premise Solutions

4.3.2 Cloud-Based Solutions

4.4 By End-User (In Value %)

4.4.1 Retail Banking

4.4.2 Corporate Banking

4.4.3 Wealth Management

4.4.4 Insurance Companies

4.4.5 SMEs & Startups

4.5 By Region (In Value %)

4.5.1 Abu Dhabi

4.5.2 Dubai

4.5.3 Sharjah

4.5.4 Ras Al Khaimah

4.5.5 Fujairah

5.1 Detailed Profiles of Major Companies

5.1.1 Network International

5.1.2 Payfort (Amazon Payments)

5.1.3 Tabby

5.1.4 YAP

5.1.5 NOW Money

5.1.6 eDirham

5.1.7 Mamo Pay

5.1.8 Sarwa

5.1.9 Ajar

5.1.10 Finablr

5.1.11 Beehive

5.1.12 Liquidity Club

5.1.13 Lendo

5.1.14 Zbooni

5.1.15 Trriple

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Market Valuation, Technology Stack, Target Audience, User Base, Revenue s)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers And Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 Fintech Licensing Requirements

6.2 Digital Payment Regulatory Guidelines

6.3 Compliance with International Banking Standards (Basel III)

6.4 Regulatory Sandbox Programs

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Technology (In Value %)

8.2 By Application (In Value %)

8.3 By Deployment Mode (In Value %)

8.4 By End-User (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

The initial phase involves mapping the ecosystem of the UAE Fintech Market. This includes key players, regulatory bodies, and fintech service providers. Desk research is used to identify the critical market drivers such as the rise of digital payments and blockchain technology.

This step involves the compilation of historical data from both primary and secondary s. Key factors such as the number of fintech companies, consumer behavior trends, and financial transactions are analyzed. A bottom-up approach is used to estimate market revenue.

Key market hypotheses are validated through interviews with fintech industry experts and stakeholders. These consultations help fine-tune our market assumptions and provide industry-specific insights into fintech adoption and growth trends.

The final phase synthesizes all the data gathered to ensure accuracy and reliability. Insights are further corroborated through direct consultations with fintech firms operating in the UAE, ensuring the final report presents an accurate and comprehensive view of the market landscape.

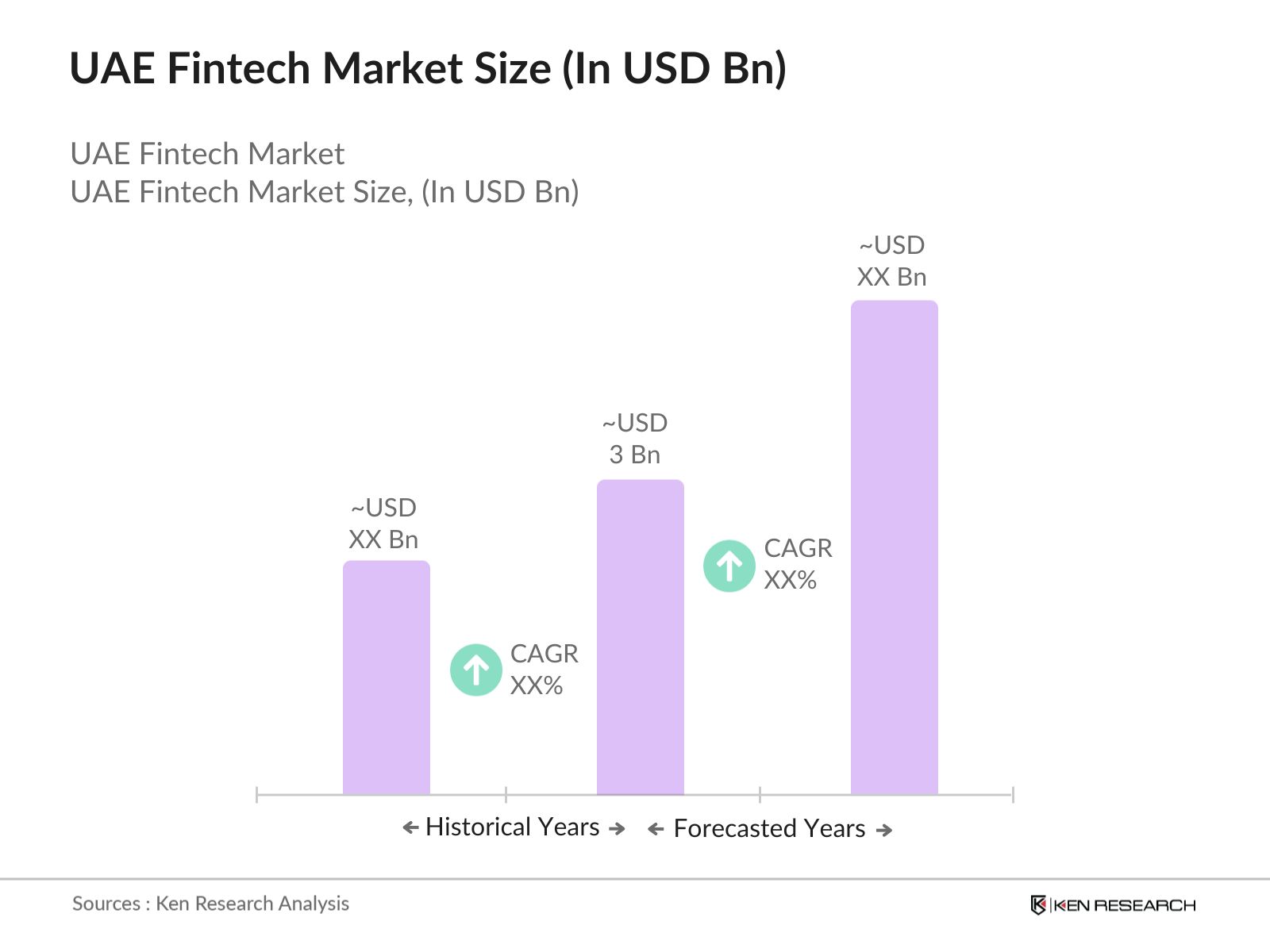

The UAE fintech market is valued at USD 3 billion in 2023, primarily driven by the adoption of digital payment solutions, government support, and advances in AI and blockchain technologies.

Key challenges include regulatory complexities, cybersecurity threats, and limited consumer trust in digital-only platforms. Additionally, the fast pace of technological change makes it difficult for smaller fintechs to keep up.

Major players include Network International, Payfort (Amazon), YAP, Mamo Pay, and Beehive, which have established strong market presence through innovation, strategic partnerships, and regulatory support.

Growth is propelled by factors such as the rise of mobile banking, blockchain adoption, government-backed fintech strategies like Smart Dubai, and the increasing demand for contactless and secure financial transactions.

Key applications include digital payments, personal finance management, insurtech, lending solutions, and regulatory compliance technologies, all of which are gaining traction due to their convenience and efficiency.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.