UAE Food Market Outlook to 2030

Region:Middle East

Author(s):Paribhasha Tiwari

Product Code:KROD5138

December 2024

93

About the Report

UAE Food Market Overview

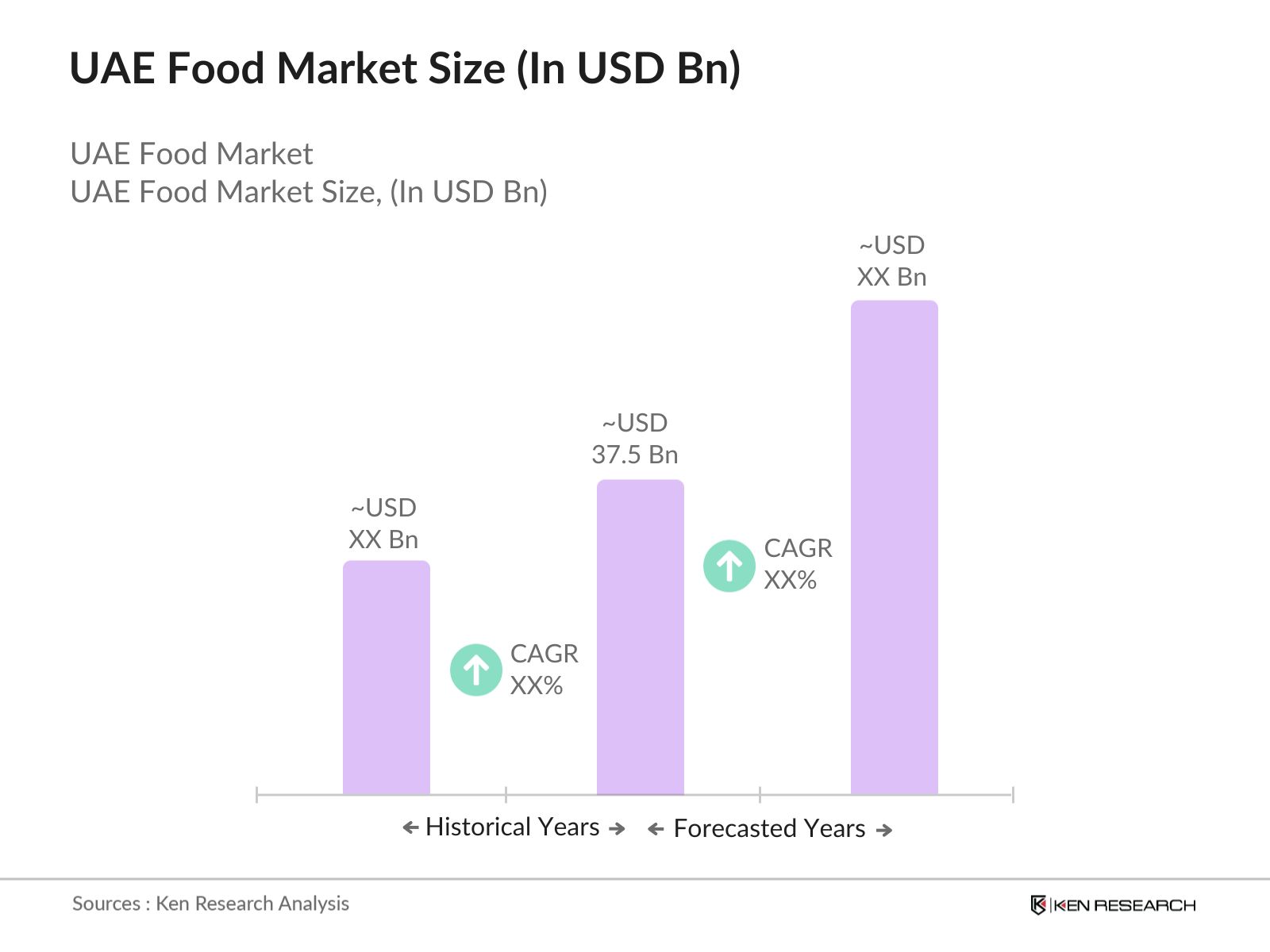

- The UAE food market, valued at USD 37.5 billion based on a five-year historical analysis, is experiencing robust growth driven by a rapidly growing population, high disposable income, and an influx of tourists. The demand for premium, organic, and health-conscious food products is on the rise, fueled by the nation's focus on adopting healthier eating habits. Additionally, the UAEs strategic position as a re-export hub further bolsters the food sector, making it an essential driver of the national economy.

- Dominant cities such as Dubai and Abu Dhabi lead the UAE food market due to their high population density, cosmopolitan consumer base, and tourism influx. These cities also benefit from well-developed infrastructure and government investments in food security initiatives, such as large-scale food storage facilities and the promotion of agribusiness investments. Additionally, Dubai's role as a global trade hub and Abu Dhabis significant government investments in food security have positioned these cities as the central nodes of the country's food market.

- The UAEs National Food Security Strategy aims to make the country one of the top 10 most food-secure nations by 2051. As of 2024, the government has allocated over $1 billion towards food security projects, including investments in local agriculture, food technology, and alternative farming methods such as hydroponics and aquaculture. The strategy also promotes partnerships with international companies to improve food production and processing capabilities within the UAE. The governments commitment to reducing its dependence on food imports is driving innovation and investments in the food sector.

UAE Food Market Segmentation

By Product Type: The UAE food market is segmented by product type into packaged foods, fresh foods, frozen foods, organic foods, and beverages. Recently, packaged foods have maintained a dominant market share, driven by the high demand for convenience among working professionals and expatriates. Urbanization and an increase in dual-income households are significant factors contributing to the consumption of packaged foods. This segment is also favored due to the wide availability of international brands and innovative product offerings catering to local preferences.

By Distribution Channel: The UAE food market is also segmented by distribution channels, including supermarkets/hypermarkets, convenience stores, online retail, specialty stores, and direct sales. Supermarkets and hypermarkets dominate the distribution channels due to their large product variety, competitive pricing, and wide availability across urban centers. The UAEs preference for modern retail formats and the growing penetration of international retail chains like Carrefour and Lulu Hypermarket further strengthens this segment. Consumers also favor supermarkets for their reliability in sourcing fresh and high-quality products.

UAE Food Market Competitive Landscape

The UAE food market is dominated by both domestic and international players, which compete based on factors such as product quality, pricing strategies, and distribution networks. The market is highly consolidated, with major players maintaining strong brand loyalty and extensive distribution channels.

|

Company |

Establishment Year |

Headquarters |

Revenue (USD Mn) |

Product Lines |

Global Presence |

Halal Certification |

Sustainability Initiatives |

Local Production Facilities |

Distribution Networks |

|

Al Rawabi Dairy Company |

1989 |

Dubai |

320 |

- | - | - | - | - | - |

|

Agthia Group PJSC |

2004 |

Abu Dhabi |

540 |

- | - | - | - | - | - |

|

Al Islami Foods |

1970 |

Dubai |

150 |

- | - | - | - | - | - |

|

Al Khaleej Sugar |

1992 |

Dubai |

600 |

- | - | - | - | - | - |

|

Al Ain Farms |

1981 |

Abu Dhabi |

400 |

- | - | - | - | - | - |

UAE Food Market Analysis

Growth Drivers

- Increase in Tourism: The UAE's robust tourism sector is a significant growth driver for its food market. As of 2024, the country expects over 22 million international visitors, according to the Dubai Department of Economy and Tourism. The influx of tourists, especially to cities like Dubai and Abu Dhabi, leads to increased demand for diverse and premium food offerings. The UAEs status as a global travel hub, coupled with world-class dining experiences, is driving the growth of its food industry. Tourists from countries like India, China, and Europe are also contributing to the demand for culturally diverse cuisines.

- Growing Expatriate Population: In 2024, the UAE's expatriate population exceeds 9 million, forming a substantial portion of the countrys total population of 12.50 million. This diverse expatriate base, consisting of people from over 200 nationalities, drives demand for a wide variety of international foods. Major retail chains, such as Carrefour and Lulu Hypermarket, are expanding their product offerings to cater to this diverse consumer base, which includes European, South Asian, and Southeast Asian cuisines. The expat-driven demand for both premium and affordable food products has significantly shaped the UAE's food market.

- Increased Government Investment in Food Security: The UAE government continues to invest heavily in food security initiatives. In 2024, the country allocated over $1 billion towards projects aimed at reducing dependency on food imports and enhancing domestic food production. Key initiatives include investments in vertical farming, hydroponics, and aquaculture projects. These investments are driven by the National Food Security Strategy, which aims to ensure a sustainable supply of essential food items. The UAE's focus on improving food security is also attracting international investments and partnerships in agriculture and food processing.

Market Challenges

- Dependence on Food Imports: The UAE imports approximately 90% of its food requirements, a challenge exacerbated by global supply chain disruptions in 2024. The high dependence on imported food products exposes the country to fluctuations in international prices and transportation costs. The governments efforts to diversify supply chains have helped mitigate some challenges, but the lack of domestic agricultural resources continues to be a constraint. Geopolitical tensions and climate-related disruptions in exporting countries further compound the issue, making food imports costly and less reliable.

- Limited Domestic Production: As of 2024, only 2.5% of the UAEs land is arable, severely limiting domestic food production capabilities. The harsh desert climate and water scarcity hinder the expansion of traditional agriculture. Despite government investments in technologies such as hydroponics and vertical farming, local production accounts for a small fraction of the food supply. The high costs associated with these technologies also limit their scalability. This makes it difficult for the UAE to achieve significant progress in domestic food production in the short term, contributing to continued reliance on imports.

UAE Food Market Future Outlook

Over the next five years, the UAE food market is expected to witness significant growth driven by a combination of factors such as population growth, rising demand for premium and organic food products, and technological advancements in food production and distribution. The government's commitment to enhancing food security through strategic investments in agribusiness, urban farming, and the National Food Security Strategy will further fuel market expansion. Additionally, the continuous expansion of e-commerce platforms and the increasing consumer preference for convenience will drive innovation in distribution models.

Market Opportunities

- Growing Demand for Organic and Health Foods: The UAE food market is witnessing a strong shift towards organic and health foods, driven by growing health consciousness among consumers. In 2024, it is estimated that over 60% of UAE residents are actively incorporating organic and healthy food choices into their diets. Organic food sales have surged in major urban centers like Dubai, with supermarkets expanding their product ranges to include more organic and plant-based items. Government initiatives supporting sustainable agriculture are likely to further promote the growth of this sector in the coming years.

- Technological Advancements in Food Processing: The adoption of new food processing technologies, such as automation, precision agriculture, and AI-driven food safety measures, is reshaping the UAE food industry. In 2023, the UAE invested heavily in food technology parks and innovation hubs, aiming to reduce its dependency on imported processed foods. These advancements are helping improve efficiency, reduce food waste, and enhance the quality and safety of food products. Technology is also enabling the local production of high-value food items such as dairy alternatives, gluten-free products, and fortified foods.

Scope of the Report

|

By Product Type |

Packaged Foods Fresh Foods Frozen Foods Organic Foods Beverages |

|

By Distribution Channel |

Supermarkets/Hypermarkets Convenience Stores Online Retail Specialty Stores Direct Sales |

|

By Consumer Group |

Individual Consumers Institutional Buyers Retailers |

|

By Cuisine Preference |

Middle Eastern Western Asian Fusion |

|

By Region |

Abu Dhabi Dubai Sharjah Northern Emirates |

Products

Key Target Audience

Food and Beverage Manufacturers

Retail Chains and Supermarket Operators

Food Importers and Exporters

Hospitality and Catering Services

Investments and Venture Capital Firms

Government and Regulatory Bodies (Dubai Municipality, Abu Dhabi Agriculture and Food Safety Authority)

E-commerce Platforms

Agribusiness Investors

Companies

Players Mentioned in the Report:

Al Rawabi Dairy Company

Agthia Group PJSC

Al Ain Farms

Emirates Modern Poultry Co.

Gulf Food Industries

Al Islami Foods

Al Foah Company

Barakat Quality Plus

National Food Products Company

Emirates Snack Foods

Table of Contents

1. UAE Food Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (CAGR, Market Drivers, Economic Influence)

1.4. Market Segmentation Overview

2. UAE Food Market Size (In AED Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. UAE Food Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Urbanization

3.1.2. Changing Dietary Preferences

3.1.3. Rise in Disposable Income

3.1.4. Expansion of E-commerce Platforms

3.2. Market Challenges

3.2.1. Price Volatility of Raw Materials (Food Commodities, Oil, Grains)

3.2.2. Regulatory Compliance (UAE Food Safety Regulations, Halal Certification)

3.2.3. Limited Agricultural Resources

3.3. Opportunities

3.3.1. Growing Demand for Organic and Health Foods

3.3.2. Technological Advancements in Food Processing

3.3.3. Increased Focus on Food Security (National Food Security Strategy)

3.4. Trends

3.4.1. Shift Toward Plant-based Foods

3.4.2. Rising Demand for Sustainable Packaging

3.4.3. Emergence of Food Delivery Platforms

3.5. Government Regulations

3.5.1. Food Import and Export Regulations

3.5.2. Emiratization in Food Industry

3.5.3. National Food Security Strategy

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Suppliers, Distributors, Retailers)

3.8. Porters Five Forces (Supplier Power, Buyer Power, Competitive Rivalry, etc.)

3.9. Competitive Ecosystem

4. UAE Food Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Packaged Foods

4.1.2. Fresh Foods

4.1.3. Frozen Foods

4.1.4. Organic Foods

4.1.5. Beverages

4.2. By Distribution Channel (In Value %)

4.2.1. Supermarkets/Hypermarkets

4.2.2. Convenience Stores

4.2.3. Online Retail

4.2.4. Specialty Stores

4.2.5. Direct Sales

4.3. By Consumer Group (In Value %)

4.3.1. Individual Consumers

4.3.2. Institutional Buyers (Hotels, Restaurants, Catering)

4.3.3. Retailers

4.4. By Cuisine Preference (In Value %)

4.4.1. Middle Eastern

4.4.2. Western

4.4.3. Asian

4.4.4. Fusion

4.5. By Region (In Value %)

4.5.1. Abu Dhabi

4.5.2. Dubai

4.5.3. Sharjah

4.5.4. Northern Emirates

5. UAE Food Market Competitive Analysis

5.1. Detailed Profiles of Major Competitors

5.1.1. Al Rawabi Dairy Company

5.1.2. Agthia Group PJSC

5.1.3. Al Ain Farms

5.1.4. Emirates Modern Poultry Co.

5.1.5. Gulf Food Industries

5.1.6. Al Islami Foods

5.1.7. Al Foah Company

5.1.8. Barakat Quality Plus

5.1.9. National Food Products Company

5.1.10. Emirates Snack Foods

5.1.11. Al Khaleej Sugar

5.1.12. Al Ghurair Foods

5.1.13. Jebel Ali Flour Mills

5.1.14. Fresh Fruits Company

5.1.15. Emirates Macaroni Factory

5.2. Cross Comparison Parameters (Headquarters, Revenue, No. of Employees, Product Lines, Market Share, Global Presence, Halal Certification, Sustainability Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Subsidies

5.8. Venture Capital Investments

6. UAE Food Market Regulatory Framework

6.1. Food Safety and Standards Authority Regulations

6.2. Halal Certification Processes

6.3. Labeling and Packaging Standards

6.4. Import and Export Compliance

6.5. Taxation Policies (VAT on Food Products)

7. UAE Food Future Market Size (In AED Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. UAE Food Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By Consumer Group (In Value %)

8.4. By Cuisine Preference (In Value %)

8.5. By Region (In Value %)

9. UAE Food Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Preference Trends Analysis

9.3. Marketing Strategy Insights

9.4. Untapped Market Opportunities

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map that includes major stakeholders across the UAE Food Market. Extensive desk research is conducted using proprietary and secondary databases to gather in-depth industry-level information. The key objective is to define the essential variables influencing the market, such as consumer preferences and the supply chain dynamics.

Step 2: Market Analysis and Construction

In this phase, historical data related to the UAE food market is compiled and analyzed. This includes assessing market penetration, distribution networks, and revenue generation in different product categories. Moreover, the quality of food imports and local production facilities is analyzed to determine supply chain efficiencies.

Step 3: Hypothesis Validation and Expert Consultation

Developed hypotheses will be validated through computer-assisted telephone interviews (CATIs) with market experts, including key players from the food and beverage sector. These expert consultations provide valuable insights into consumer preferences, market competition, and operational strategies that influence the market landscape.

Step 4: Research Synthesis and Final Output

The final stage involves synthesizing data from expert consultations and proprietary databases. Detailed insights are gathered from food producers, importers, and retailers to refine and validate the market data. The final output ensures that the analysis is comprehensive, accurate, and actionable for business professionals.

Frequently Asked Questions

01. How big is the UAE Food Market?

The UAE food market was valued at USD 37.5 billion, driven by increasing urbanization, high disposable incomes, and a growing expatriate population.

02. What are the challenges in the UAE Food Market?

The UAE food market faces challenges such as price volatility in global food commodities, limited local agricultural resources, and stringent food safety regulations.

03. Who are the major players in the UAE Food Market?

Key players in the UAE food market include Al Rawabi Dairy Company, Agthia Group PJSC, Al Islami Foods, and Al Ain Farms. These companies lead the market due to their strong distribution networks and diverse product offerings.

04. What are the growth drivers of the UAE Food Market?

Key growth drivers in UAE food market include a rising demand for premium and organic food products, the expansion of e-commerce platforms, and government initiatives promoting food security.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.