UAE Fragrance Market Outlook to 2030

Region:Middle East

Author(s):Shubham Kashyap

Product Code:KROD2425

November 2024

85

About the Report

UAE Fragrance Market Overview

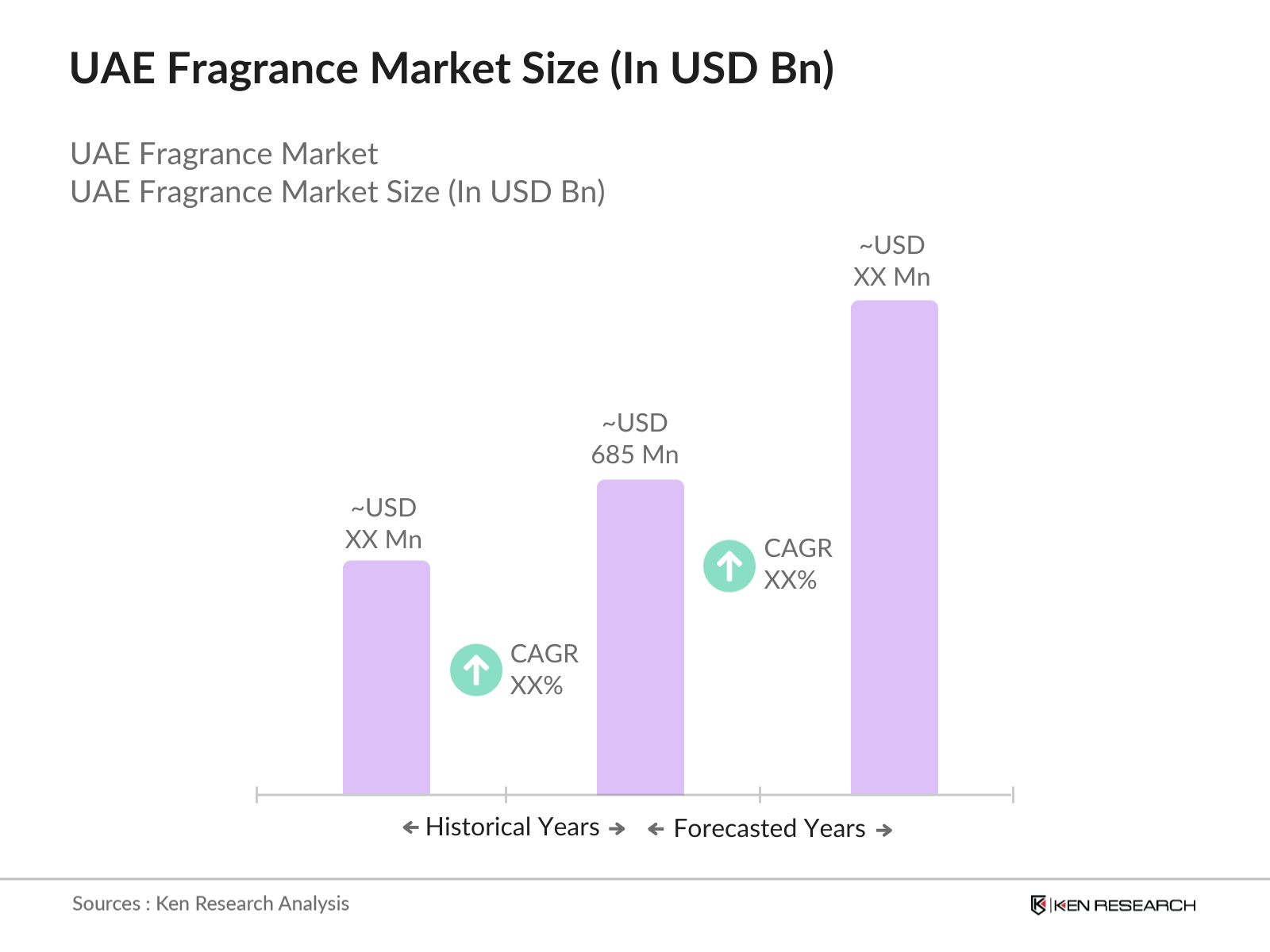

- The UAE Fragrance Market is valued at USD 685 million, driven by high consumer demand for premium fragrances and the country's unique positioning as a global luxury hub. The growing population of expatriates, coupled with increasing disposable income, continues to fuel the demand for fragrances, particularly in the luxury and niche segments.

- Major players in the UAE Fragrance Market include global brands such as Chanel, Dior, and Este Lauder, alongside regional powerhouses like Ajmal Perfumes and Swiss Arabian. These brands leverage a combination of traditional Arabic fragrance notes, such as oud and musk, and modern perfume formulations to cater to the diverse preferences of UAE consumers.

- Key regions like Dubai and Abu Dhabi dominate the market due to their affluent customer base and vibrant tourism sector, which attracts international luxury shoppers. The demand for high-end, personalized, and exclusive fragrances is particularly strong in these cities, with consumers seeking bespoke perfumes tailored to individual tastes.

- In 2023, Ajmal Perfumes unveiled a captivating new fragrance collection called "Shadow Ice".This collection is inspired by the ethereal beauty and intrigue of the night, combining the darkness and mystique of the night with the refreshing coolness of ice.

UAE Fragrance Market Segmentation

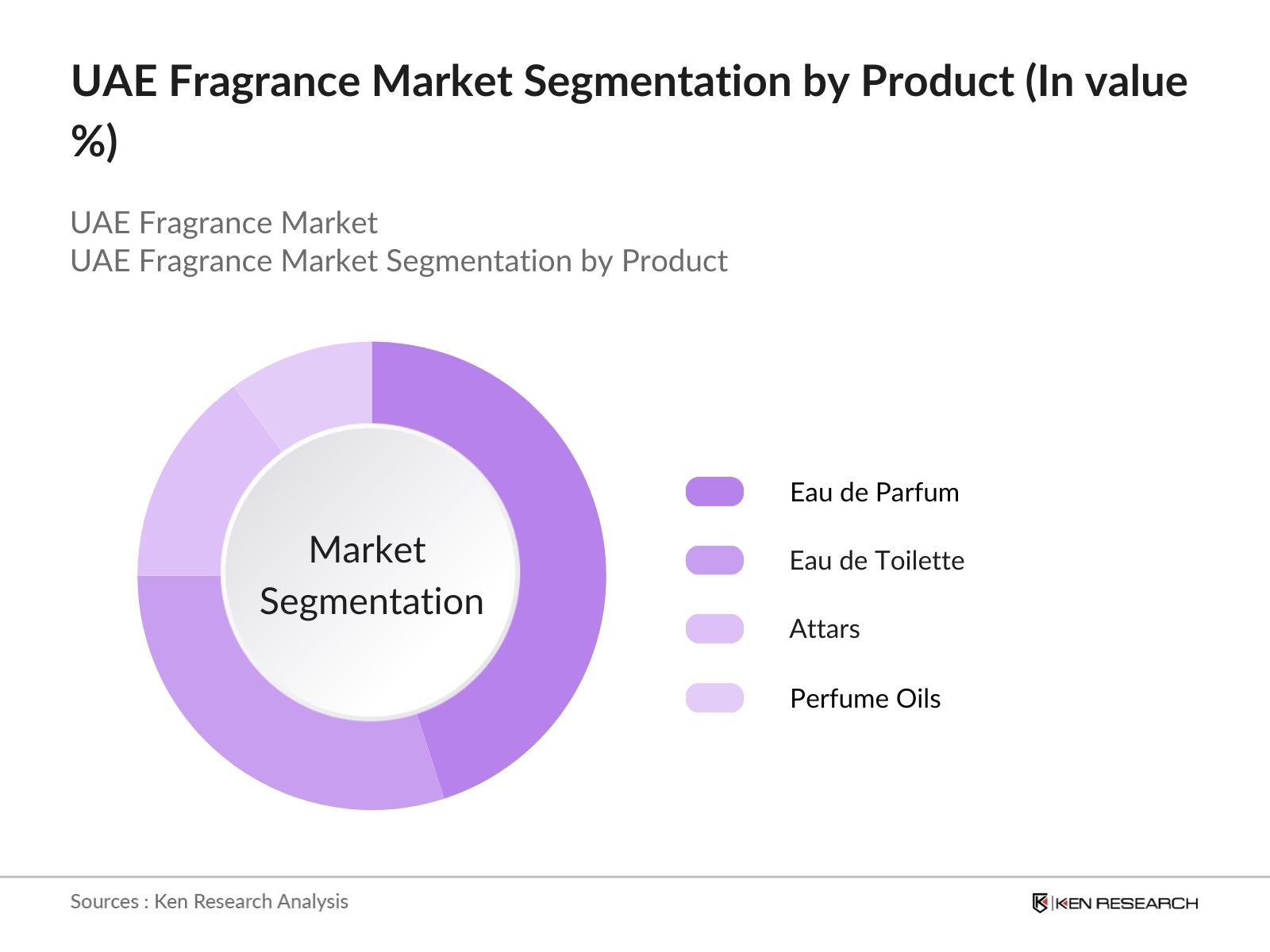

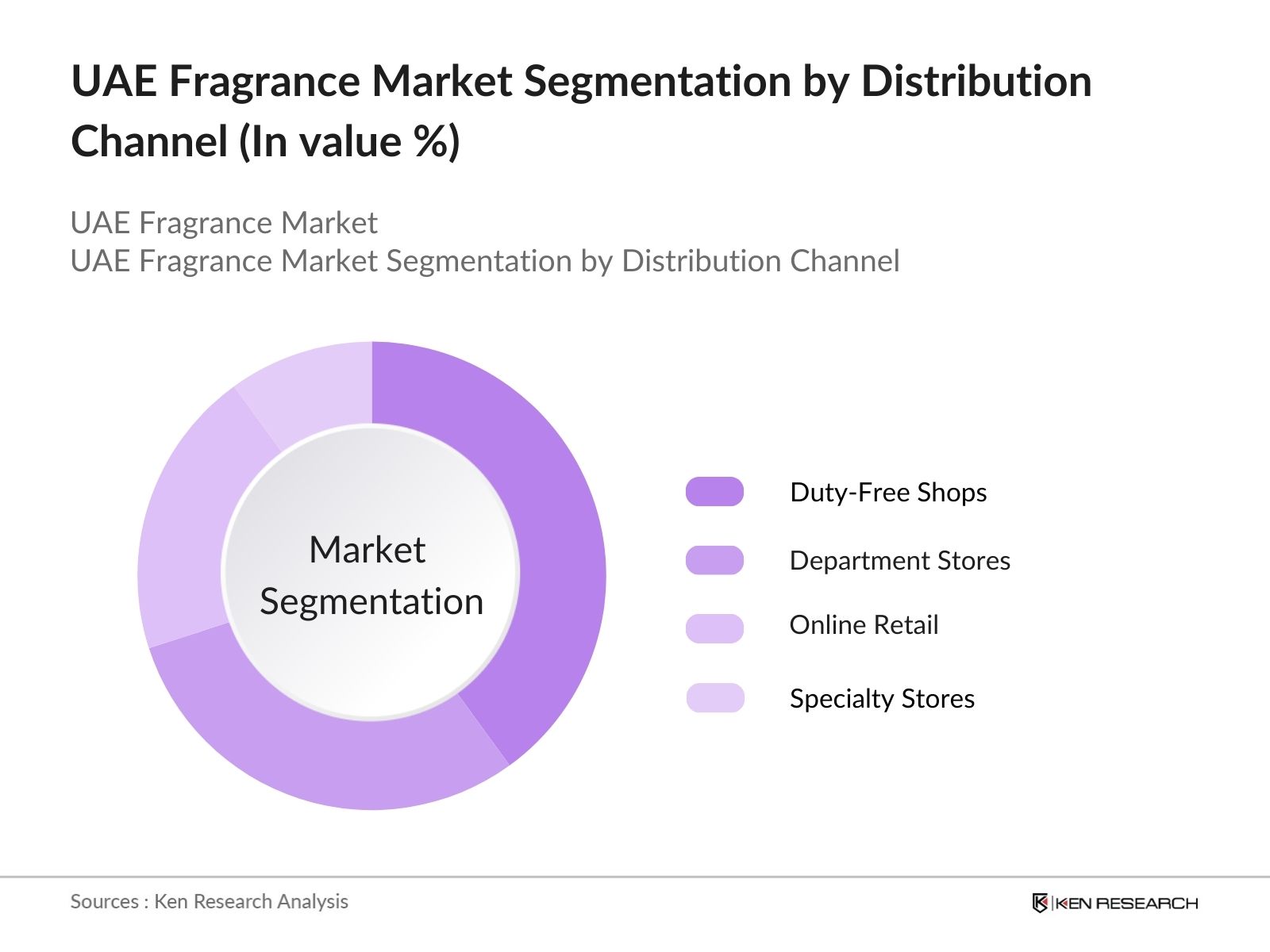

The UAE Fragrance Market is segmented by product type, distribution channel, and region.

- By Product Type: The market is segmented into Eau de Parfum, Eau de Toilette, Attars, and Perfume Oils. In 2023, Eau de Parfum held the dominant market share due to its long-lasting nature and strong scent, preferred by both male and female consumers. Attars and perfume oils are popular among traditional customers who prefer alcohol-free and concentrated fragrances.

- By Distribution Channel: The market is segmented into Online Retail, Department Stores, Specialty Stores, and Duty-Free Shops. Department stores and duty-free shops account for a noteworthy share of fragrance sales, with duty-free outlets in Dubai and Abu Dhabi airports catering to the luxury segment. However, online retail is rapidly gaining traction, with e-commerce platforms offering exclusive collections and personalized fragrance experiences.

- By Region: The market is segmented by region into Dubai, Abu Dhabi, Sharjah, and Northern Emirates. Dubai and Abu Dhabi lead the market due to their high population density, affluence, and status as international shopping destinations. Sharjah and Northern Emirates are witnessing growing demand, especially for mid-range and budget fragrances, driven by an expanding middle-class population.

UAE Fragrance Market Competitive Landscape

|

Company |

Establishment Year |

Headquarters |

|

Chanel |

1910 |

Paris, France |

|

Dior |

1946 |

Paris, France |

|

Ajmal Perfumes |

1951 |

Dubai, UAE |

|

Swiss Arabian |

1974 |

Sharjah, UAE |

|

Este Lauder |

1946 |

New York, USA |

- Dior: In 2023, Dior launched the Miss Dior Rose N'Roses fragrance in the UAE, featuring fresh and tender rose notes.This joins their existing Miss Dior line which includes the Eau de Parfum with floral and fresh notes and the Blooming Bouquet Eau de Toilette with delicate floral scents.

- Este Lauder: On June 3, 2024, the Este Lauder finalized its acquisition of the Canadian-based DECIEM Beauty Group for a total investment of USD 1.7 billion. This acquisition includes the well-known brand The Ordinary, which has gained popularity for its straightforward and effective skincare products.

UAE Fragrance Market Analysis

Growth Drivers

- Increased Demand for Personalized Fragrances: In 2023, the UAE saw a substantial increase in demand for personalized fragrances, with more consumers seeking unique, customized scent experiences. Brands like Ajmal Perfumes and Swiss Arabian have capitalized on this trend by offering bespoke fragrance creation services. According to the UAE Ministry of Economy, the personal luxury goods sector, which includes fragrances, witnessed substantial growth, driven in part by these personalized offerings. The demand for niche and exclusive products in the fragrance market is expected to continue growing as UAE residents and tourists look for luxury products that reflect their individual identities.

- Booming Tourism Sector: The UAEs fragrance market growth is strongly tied to the tourism boom, with Dubai and Abu Dhabi serving as key hubs for luxury shopping. In 2023 Dubai hosted 17.2 million overnight international visitors, a 19% increase over 2022, with many international tourists purchasing fragrances as souvenirs or luxury gifts. Dubai Duty-Free, which accounts for a noteworthy portion of total fragrance sales, plays a vital role in this surge. The strategic positioning of the UAE as a global shopping destination continues to attract high-spending tourists, particularly from Europe and Asia, contributing to increased fragrance consumption.

- Cultural Importance of Fragrance in the UAE: Fragrances, particularly oud and attar, hold significant cultural and traditional value in the UAE. According to a 2023 survey by the UAE Federal Competitiveness and Statistics Authority, more than half of UAE residents prefer oud-based fragrances, which are deeply embedded in local traditions. The use of fragrances in everyday life, weddings, and religious ceremonies creates a consistent and stable demand in the market. This cultural affinity for perfumes, particularly traditional Arabic fragrances, continues to be a key growth driver, ensuring strong demand for oud and other region-specific fragrance ingredients.

Challenges

- Counterfeit Perfume Market: The proliferation of counterfeit perfumes has become a major challenge for the UAE fragrance market. This ongoing issue affects brand integrity and consumer trust, as fake products are often sold at lower prices, leading to revenue losses for established brands. Counterfeit products also pose health risks, further complicating the regulatory framework for perfume sales in the country.

- High Import Duties and Regulatory Barriers: The UAE imposes substantial import duties on luxury goods, including fragrances, which raises retail prices and limits market accessibility for some consumers. These duties impact the affordability of foreign brands, making it harder for consumers to access international luxury fragrances. Furthermore, stringent regulations by the UAE General Civil Aviation Authority (GCAA) limit the transportation of flammable perfume ingredients.

Government Initiatives

- Made in UAE Campaign: The "Made in UAE" campaign is a key initiative by the UAE government to boost local manufacturing and support homegrown industries. It is part of the broader "Make it in the Emirates" strategy and "Operation 300Bn" plan to transform the UAE into a global industrial hub by 2031. The initiative encourages local production of perfumes by offering incentives such as reduced taxes and subsidies for manufacturers who source raw materials domestically.

- UAE Green Agenda 2030: The UAE Green Agenda 2030, launched in 2023, emphasizes sustainability across all industries, including the fragrance sector. The Ministry of Climate Change and Environment has outlined new regulations requiring fragrance manufacturers to reduce their carbon footprint and adopt eco-friendly practices. This policy shift is expected to influence product development, with major players in the market adopting more sustainable practices in sourcing and packaging.

UAE Fragrance Market Future Outlook

The UAE Fragrance Market is projected to grow remarkably in the forecasted period, driven by increasing demand for luxury fragrances, rising online sales, and the continued popularity of oud-based perfumes.

Future Market Trends

- Sustainable and Natural Fragrances: The market will see an increasing shift towards sustainable and eco-friendly fragrances by 2028, driven by government regulations and consumer demand. The UAE Green Agenda 2030 will play a significant role in shaping market trends, with brands expected to adopt biodegradable packaging and ethically sourced ingredients.

- Technological Integration in Fragrance Manufacturing: By 2028, advancements in technology will revolutionize the fragrance manufacturing process, particularly with the use of AI and data analytics in perfume creation. Major brands in the UAE are expected to leverage these technologies to develop personalized fragrances based on consumer preferences and scent profiles.

Scope of the Report

|

By Product |

Eau de Parfum Eau de Toilette Attars Perfume Oils |

|

By Distribution |

Online Retail Department Stores Specialty Stores Duty-Free Shops |

|

By Gender |

Male Female Unisex |

|

By End-Users |

Individual Consumers Hospitality Corporate Buyers |

|

By Region |

Dubai Abu Dhabi Sharjah Northern Emirates |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing to This Report

Luxury Retailers and Boutiques

Hotel and Hospitality Chains

Department Stores

Airport Duty-Free Operators

E-commerce Platforms

Fragrance Manufacturers and Suppliers

Distributors and Wholesalers

Government and Regulatory Bodies (Dubai Department of Economic Development)

Investors and Venture Capital Firms

Banks and Financial Institutes

Time Period Captured in the Report

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report

Chanel

Dior

Ajmal Perfumes

Swiss Arabian

Este Lauder

Gucci

Yves Saint Laurent

Arabian Oud

Rasasi Perfumes

Gucci

Burberry

Prada

Tom Ford

Lancme

Jo Malone

Table of Contents

01 UAE Fragrance Market Overview

1.1. Definition and Scope

1.2. Market Structure and Taxonomy

1.3. Market Growth Rate Analysis (Financial and Operational Metrics)

1.4. Key Market Developments and Milestones

02 UAE Fragrance Market Size (USD Billion)

2.1. Historical Market Size (Value and Volume)

2.2. Year-on-Year Growth Analysis (Operational Parameters)

2.3. Contribution of Key Regions (Dubai, Abu Dhabi, Sharjah, Northern Emirates)

2.4. Industry Revenue Analysis (Top-to-Bottom Approach)

2.5. Breakdown of Market Value by Fragrance Type (Eau de Parfum, Eau de Toilette, Attars, Perfume Oils)

03 UAE Fragrance Market Dynamics

3.1. Growth Drivers

3.1.1. Rising Demand for Oud-Based Fragrances

3.1.2. Increase in Luxury and Niche Fragrance Purchases

3.1.3. Expanding E-commerce and Digital Sales Channels

3.2. Market Challenges

3.2.1. Proliferation of Counterfeit Perfumes

3.2.2. High Import Duties on Luxury Fragrances

3.2.3. Regulatory Issues Related to Ingredients and Sustainability

3.3. Market Opportunities

3.3.1. Growing Trend of Personalized and Bespoke Fragrances

3.3.2. Sustainability and Eco-Friendly Packaging Solutions

3.3.3. Increased Interest in Gender-Neutral Fragrances

04 UAE Fragrance Market Segmentation

4.1. By Fragrance Type (In Value %)

4.1.1. Eau de Parfum

4.1.2. Eau de Toilette

4.1.3. Attars

4.1.4. Perfume Oils

4.2. By Distribution Channel (In Value %)

4.2.1. Online Retail

4.2.2. Department Stores

4.2.3. Specialty Stores

4.2.4. Duty-Free Shops

4.3. By Region (In Value %)

4.3.1. Dubai

4.3.2. Abu Dhabi

4.3.3. Sharjah

4.3.4. Northern Emirates

05 UAE Fragrance Market Competitive Landscape

5.1. Competitive Market Share Analysis (Market Share %, Financial and Operational Metrics)

5.2. Strategic Initiatives and Partnerships (Investments, JVs, and Alliances)

5.3. Key Market Players Analysis

5.3.1. Chanel

5.3.2. Dior

5.3.3. Ajmal Perfumes

5.3.4. Swiss Arabian

5.3.5. Este Lauder

5.4. Cross-Comparison (Company Profiles Establishment Year, Headquarters, Revenue, No. of Employees)

5.4.1. Gucci

5.4.2. Tom Ford

5.4.3. Jo Malone

5.4.4. Burberry

5.4.5. Prada

06 UAE Fragrance Market Financial Analysis

6.1. Financial Performance of Key Players

6.1.1. Revenue Analysis by Key Companies

6.1.2. Operational Efficiency Metrics (Production Volume, Cost Efficiency)

6.2. Investment and Venture Capital Analysis

6.2.1. Recent Investments and Fundings (Venture Capital, Government Grants)

6.2.2. Mergers and Acquisitions

6.3. Profitability and Revenue Forecasts

07 UAE Fragrance Market Regulatory Framework

7.1. Government Policies Supporting Local Fragrance Brands

7.2. Compliance and Certification Requirements for Fragrance Manufacturers

7.3. Regulations on Ingredients and Health & Safety Standards

7.4. Environmental Standards for Sustainable Packaging and Sourcing

08 Future Outlook for UAE Fragrance Market

8.1. Market Growth Projections

8.2. Key Trends Shaping Future Demand (Luxury, Bespoke, and Eco-Friendly Fragrances)

8.3. Expansion of Local Production and Export Opportunities

8.4. Integration of AI and Technology in Fragrance Customization

09 UAE Fragrance Market Future Segmentation, 2028

9.1. By Fragrance Type (In Value %)

9.2. By Distribution Channel (In Value %)

9.3. By Region (In Value %)

10 Analyst Recommendations

10.1. TAM/SAM/SOM Analysis for Fragrance Market

10.2. Key Strategic Recommendations for Fragrance Brands

10.3. Emerging Markets and White-Space Opportunities (Gender-Neutral, Sustainable Fragrances)

10.4. Customer-Centric Approach for Enhanced Fragrance Offerings

Research Methodology

Step 1 Identifying Key Variables

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry-level information.

Step 2 Market Building

Collating statistics on the UAE fragrance market over the years, penetration of marketplaces, and service providers ratio to compute revenue generated for the UAE fragrance market. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Step 3 Validating and Finalizing

Building market hypotheses and conducting CATIs with industry experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Step 4 Research Output

Our team will approach multiple essential fragrance companies and understand the nature of product segments and sales, consumer preference, and other parameters, which will support us to validate statistics derived through a bottom-to-top approach from fragrance companies.

Frequently Asked Questions

01

How big is the UAE Fragrance Market?

The UAE fragrance market was valued at USD 685 million, driven by high consumer demand for luxury and oud-based perfumes, a rising expatriate population, and the countrys status as a global luxury shopping destination.

02

What are the challenges in the UAE Fragrance Market?

Challenges in the UAE fragrance market include the proliferation of counterfeit perfumes, high import duties on luxury fragrances, and regulatory barriers related to the transportation of perfume ingredients. These issues impact brand reputation and market accessibility, especially for niche and international brands.

03

Who are the major players in the UAE Fragrance Market?

Key players in the UAE fragrance market include Chanel, Dior, Ajmal Perfumes, Swiss Arabian, and Este Lauder. These brands dominate the market through strong product portfolios, extensive retail presence, and a blend of traditional and modern fragrance offerings.

04

What are the growth drivers of the UAE Fragrance Market?

The UAE fragrance market is propelled by the growing demand for oud-based fragrances, the rise in personalized and bespoke perfume experiences, and the expanding e-commerce sector, which offers greater accessibility and convenience for consumers.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.