UK Aerospace and Defense Market Outlook to 2030

Region:United Kingdom

Author(s):Sanjeev

Product Code:KROD1591

Region:United Kingdom

Author(s):Sanjeev

Product Code:KROD1591

November 2024

94

UK Aerospace and Defense Market Overview

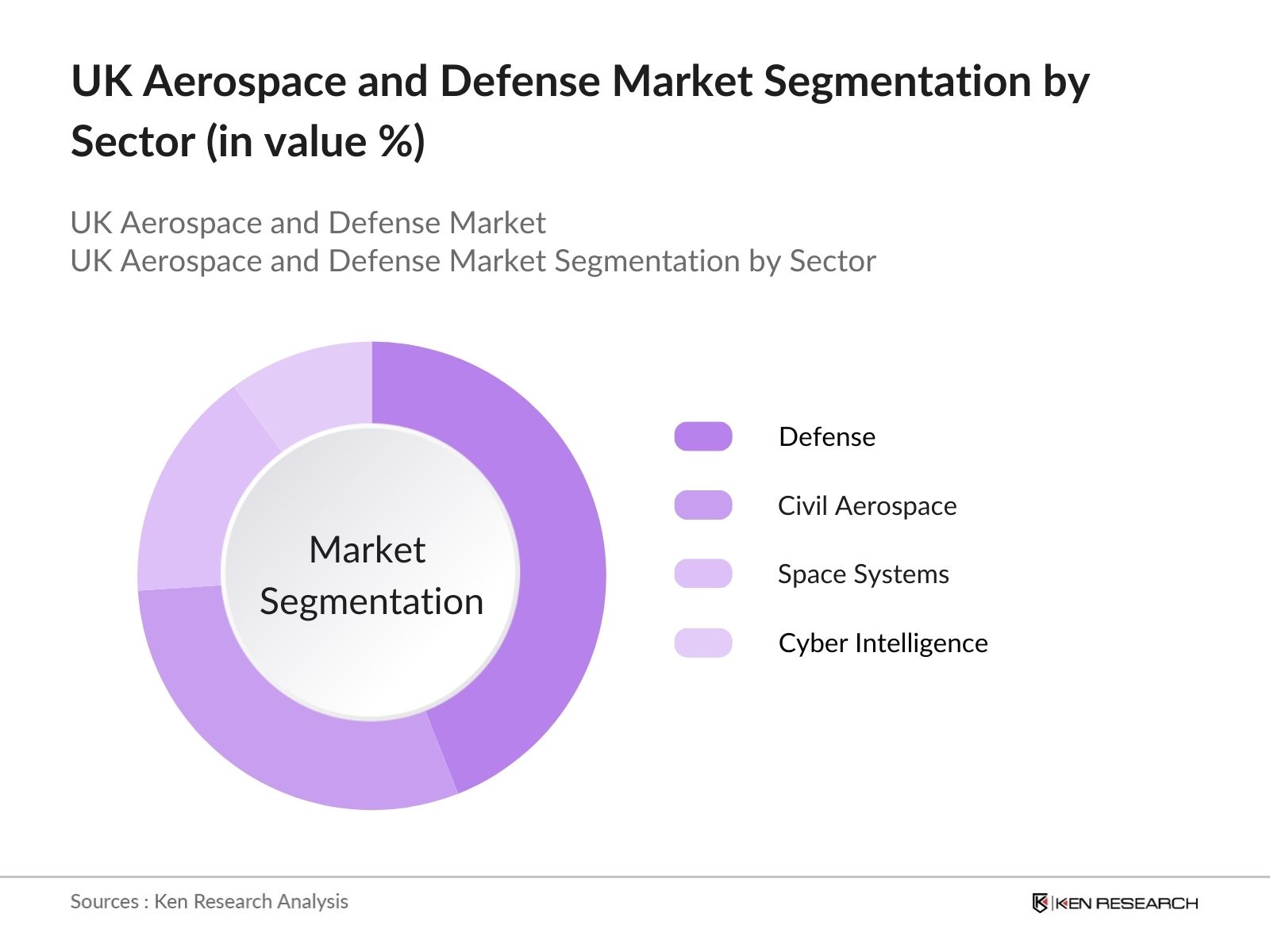

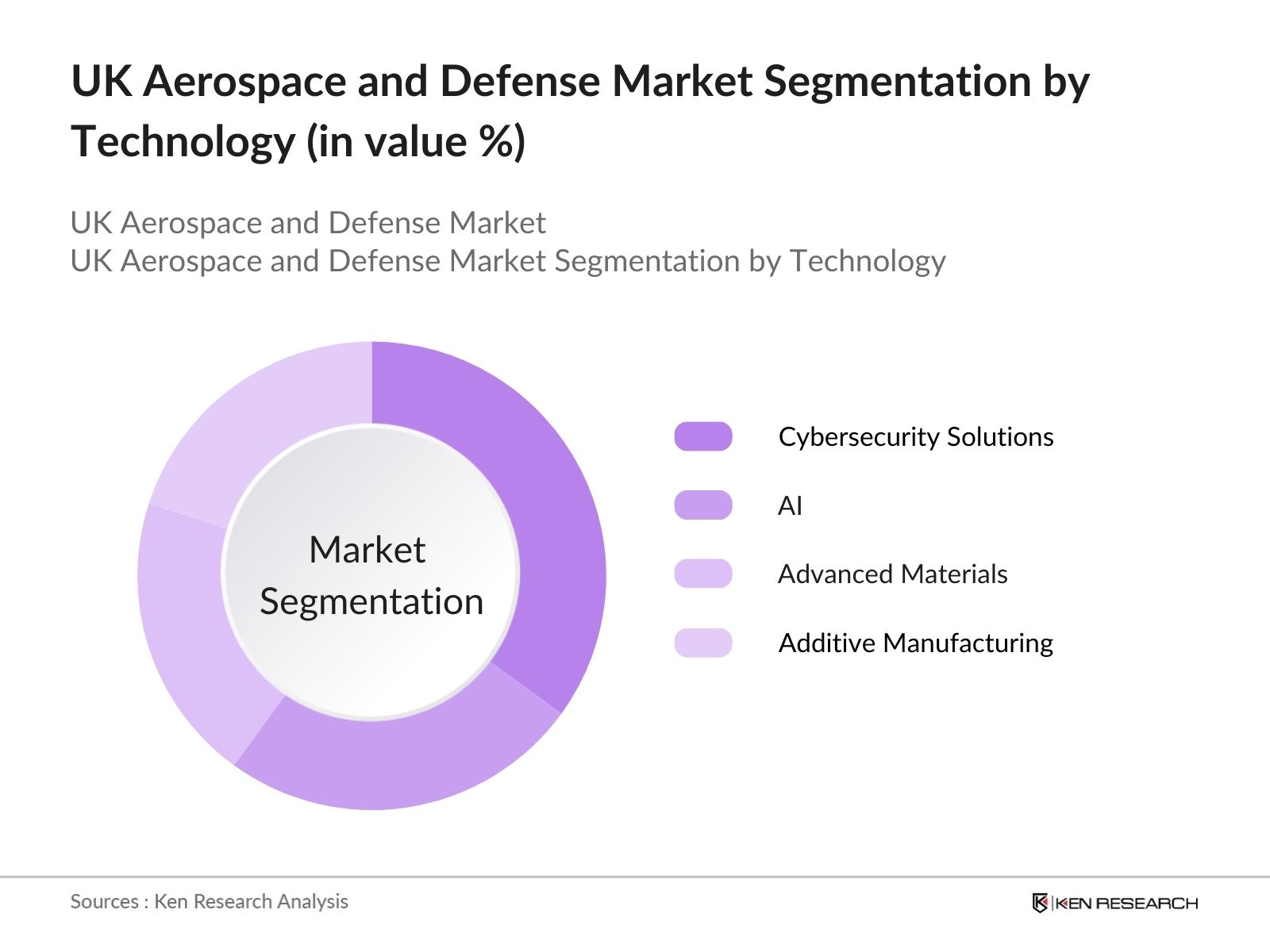

The UK Aerospace and Defense Market is segmented by sector and by technology.

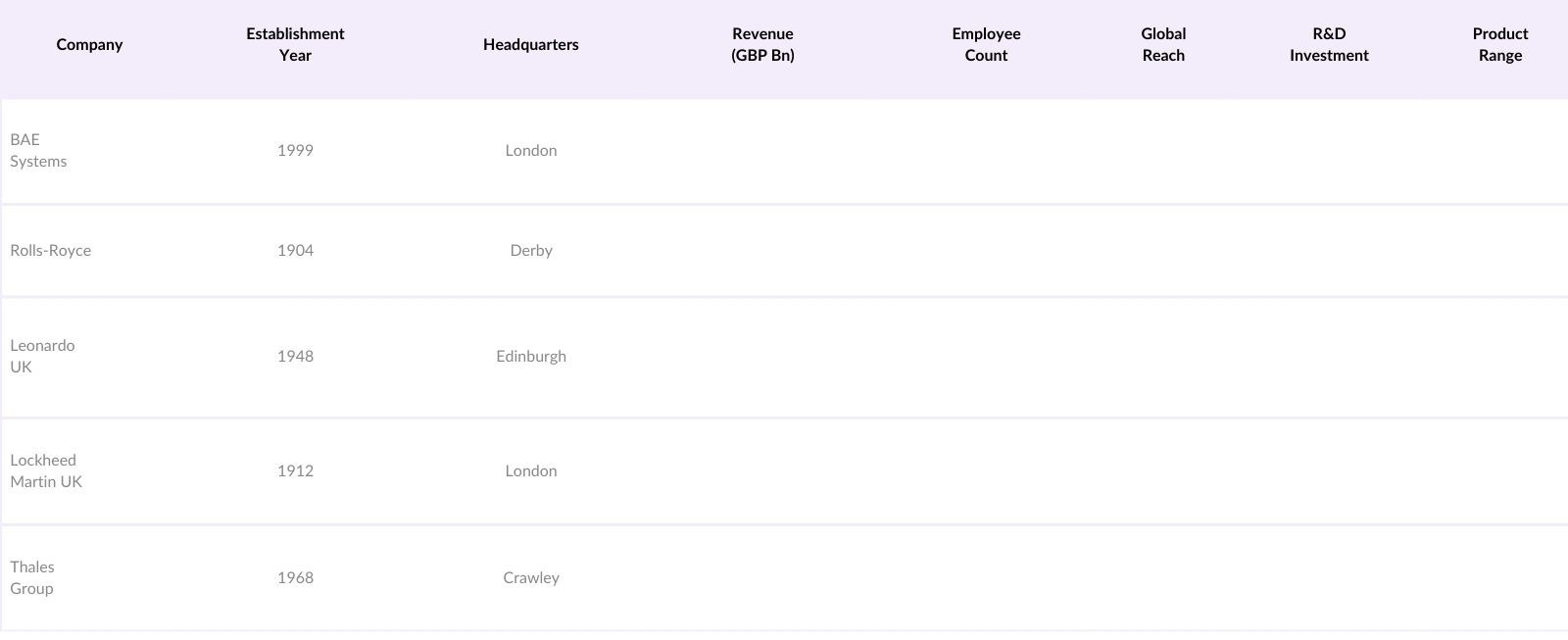

The UK Aerospace and Defense Market is led by key players who leverage long-standing industry experience and technological prowess. The major players in this market include local giants like BAE Systems and Rolls-Royce and global aerospace and defense firms with UK-based operations, ensuring strong competitive dynamics.

Growth Drivers

Market Challenges

UK Aerospace and Defense Market Future Outlook

Over the next five years, the UK Aerospace and Defense Market is expected to expand significantly. This growth is anticipated to be fueled by advancements in aerospace technology, increased government budgets, and the rising global demand for cybersecurity solutions within defense systems. Expanding the UKs presence in civil aerospace and space exploration initiatives will further contribute to market growth, alongside the focus on sustainable aerospace solutions.

|

||

|

By Component Type |

Aircraft |

|

|

By Technology |

AI and Machine Learning |

|

|

By Platform |

Air-based |

|

|

By Region |

North East West South |

Key Target Audience

Players Mention in the Report:

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers (Emerging Demand for Advanced Defense Systems, Increased Defense Budgets)

3.1.1. Demand for Cutting-edge Technology

3.1.2. Government Investment Initiatives

3.1.3. International Defense Collaborations

3.2. Market Challenges (Regulatory Complexities, Cost Management)

3.2.1. Stringent Regulations

3.2.2. High Manufacturing Costs

3.2.3. Dependency on Global Supply Chains

3.3. Opportunities (Expansion of Civil Aerospace, Space Industry Potential)

3.3.1. Emerging Space Exploration Market

3.3.2. Civil Aerospace Growth

3.3.3. Potential in UAV and Drone Technologies

3.4. Trends (Adoption of AI, Increased Focus on Cybersecurity)

3.4.1. Artificial Intelligence in Defense Applications

3.4.2. Cybersecurity for Defense Systems

3.4.3. Emphasis on Sustainable Manufacturing

3.5. Government Regulations

3.5.1. Defense Equipment and Support (DE&S) Standards

3.5.2. Export Control Requirements

3.5.3. UK Space Agency Regulations

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape Overview

4.1. By Sector (in Value %)

4.1.1. Defense

4.1.2. Civil Aerospace

4.1.3. Space Systems

4.1.4. Intelligence and Cyber

4.2. By Component Type (in Value %)

4.2.1. Aircraft

4.2.2. Naval Systems

4.2.3. Land Systems

4.2.4. Satellite and Space Systems

4.3. By Technology (in Value %)

4.3.1. AI and Machine Learning

4.3.2. Cybersecurity Solutions

4.3.3. Additive Manufacturing

4.3.4. Advanced Materials

4.4. By Platform (in Value %)

4.4.1. Air-based

4.4.2. Land-based

4.4.3. Sea-based

4.4.4. Space-based

4.5. By Region (in Value %)

4.5.1. North

4.5.2. East

4.5.3. West

4.5.4. South

5.1. Detailed Profiles of Major Companies

5.1.1. BAE Systems

5.1.2. Rolls-Royce Holdings

5.1.3. Leonardo UK

5.1.4. Lockheed Martin UK

5.1.5. Airbus Group UK

5.1.6. Thales Group UK

5.1.7. Northrop Grumman UK

5.1.8. Raytheon UK

5.1.9. Boeing UK

5.1.10. MBDA UK

5.1.11. QinetiQ Group

5.1.12. General Dynamics UK

5.1.13. Cobham Ltd

5.1.14. Ultra Electronics Holdings

5.1.15. Serco Group

5.2. Cross Comparison Parameters (Revenue, No. of Employees, Inception Year, Headquarters, Market Reach, Product Range, Technological Capabilities, ESG Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives and Alliances

5.5. Mergers and Acquisitions

5.6. Investment and Funding Analysis

5.7. Government Grants and Incentives

5.8. Private Equity and Venture Capital Investments

6.1. Compliance and Certification Standards

6.2. Export and Import Controls

6.3. Environmental Impact Regulations

6.4. Cybersecurity Compliance Requirements

7.1. Future Market Size Projections

7.2. Key Factors for Future Market Growth

8.1. By Sector (in Value %)

8.2. By Component Type (in Value %)

8.3. By Technology (in Value %)

8.4. By Platform (in Value %)

8.5. By Region (in Value %)

9.1. Market Entry Strategy Analysis

9.2. Customer Demographics Analysis

9.3. Strategic Marketing Initiatives

9.4. Competitive White Space Opportunities

Disclaimer Contact Us

This initial phase involves constructing a detailed map of stakeholders in the UK Aerospace and Defense Market. Extensive desk research and proprietary databases provide in-depth information, allowing identification and definition of critical market dynamics.

Historical data collection for the UK market includes market penetration rates, ratio analysis of key sectors, and revenue estimations. Service quality metrics ensure reliable revenue calculations, forming a solid basis for market size analysis.

Market hypotheses are developed and validated through interviews with industry experts across various segments. These insights directly from the market participants provide accurate financial and operational data for a more refined analysis.

Engagements with key aerospace and defense manufacturers and stakeholders contribute detailed insights into product segments, sales, and preferences. These interactions substantiate data and validate the bottom-up approach for final market analysis.

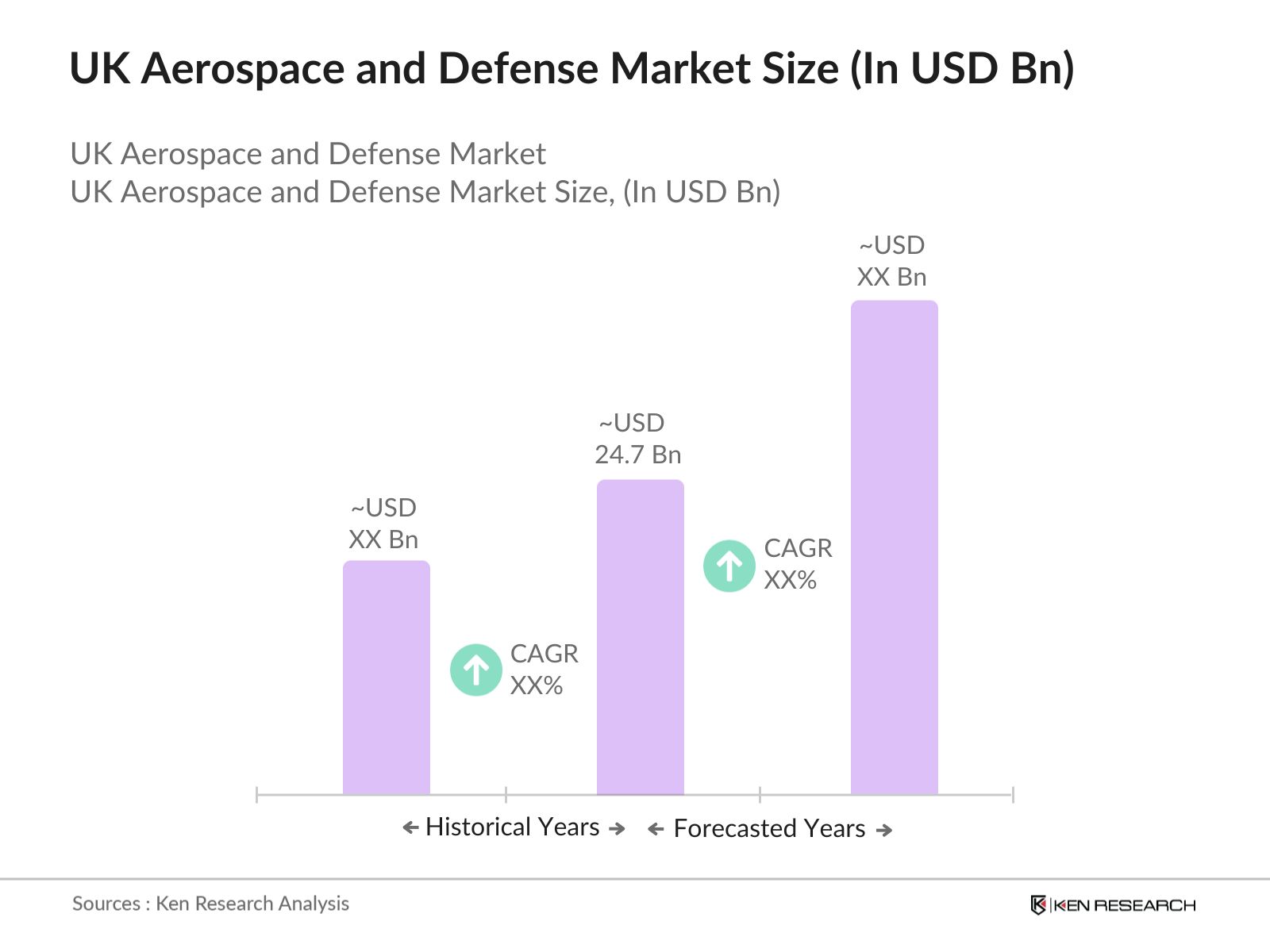

The UK Aerospace and Defense Market was valued at USD 24.7 billion, driven by significant investments in defense technology and expanding civil aerospace demands.

Challenges in UK Aerospace and Defense Market include regulatory complexity, high production costs, and dependency on international supply chains, impacting manufacturing and development.

The UK Aerospace and Defense Market includes key players like BAE Systems, Rolls-Royce, Leonardo UK, and Lockheed Martin UK, who dominate through technological prowess and government partnerships.

UK Aerospace and Defense Market Growth is primarily driven by increased government budgets, technological advancements, and the UK's focus on civil aerospace and cybersecurity in defense systems.

Dominant technologies include cybersecurity, AI, and additive manufacturing, each addressing specific sector demands and enhancing market competitiveness.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.