United States Cannabis Market Outlook to 2030

Region:North America

Author(s):Sanjeev

Product Code:KROD7167

October 2024

94

About the Report

United States Cannabis Market Overview

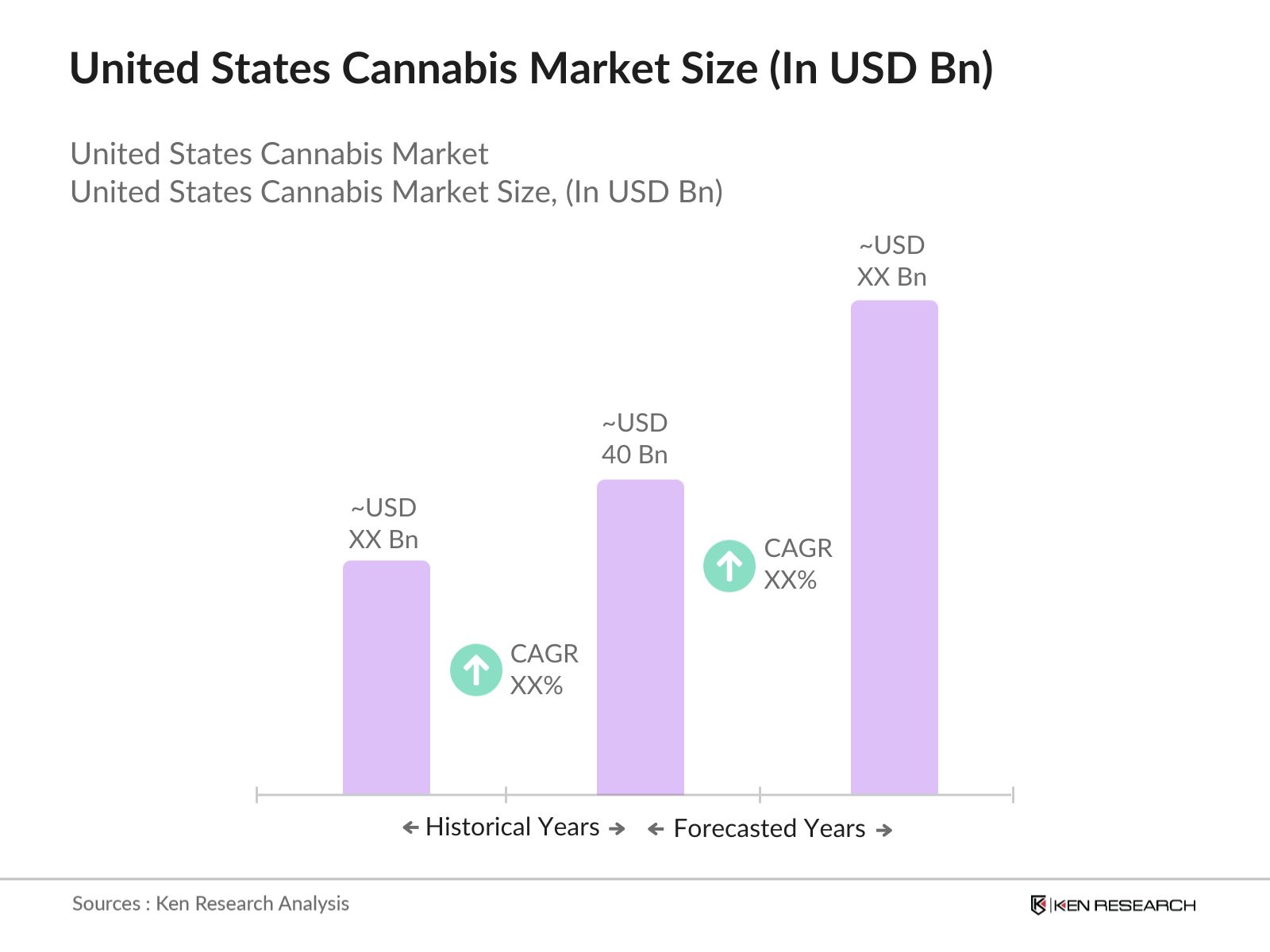

- The United States Cannabis Market is valued at USD 40 billion based on recent assessments, reflecting growth driven by the increased legalization for both medical and recreational purposes. This expansion is further fueled by heightened consumer awareness of the health benefits of cannabis products and the rising demand for CBD-infused items. Medical cannabis continues to drive a substantial portion of the market, supported by clinical research and the development of cannabis-derived pharmaceutical products.

- Dominant states in the U.S. cannabis market include California, Colorado, and Washington, which lead due to their well-established legal frameworks, large consumer bases, and advanced distribution networks. California, for example, benefits from early legalization and a strong cultural association with cannabis, contributing to its dominance. Similarly, Colorado and Washington have long histories of both recreational and medical cannabis legalization, which has fostered a thriving ecosystem of cultivators, dispensaries, and ancillary businesses.

- New states legalizing recreational cannabis present market expansion opportunities. In 2022, New Jersey became one of the latest states to legalize recreational use, generating over $200 million in tax revenue within the first 12 months of sales. Similarly, states like Connecticut and Maryland are expected to drive the next wave of market growth as they implement their own recreational cannabis frameworks. This trend reflects ongoing legislative momentum, which is likely to create new business opportunities for cannabis companies seeking to expand into these emerging markets.

United States Cannabis Market Segmentation

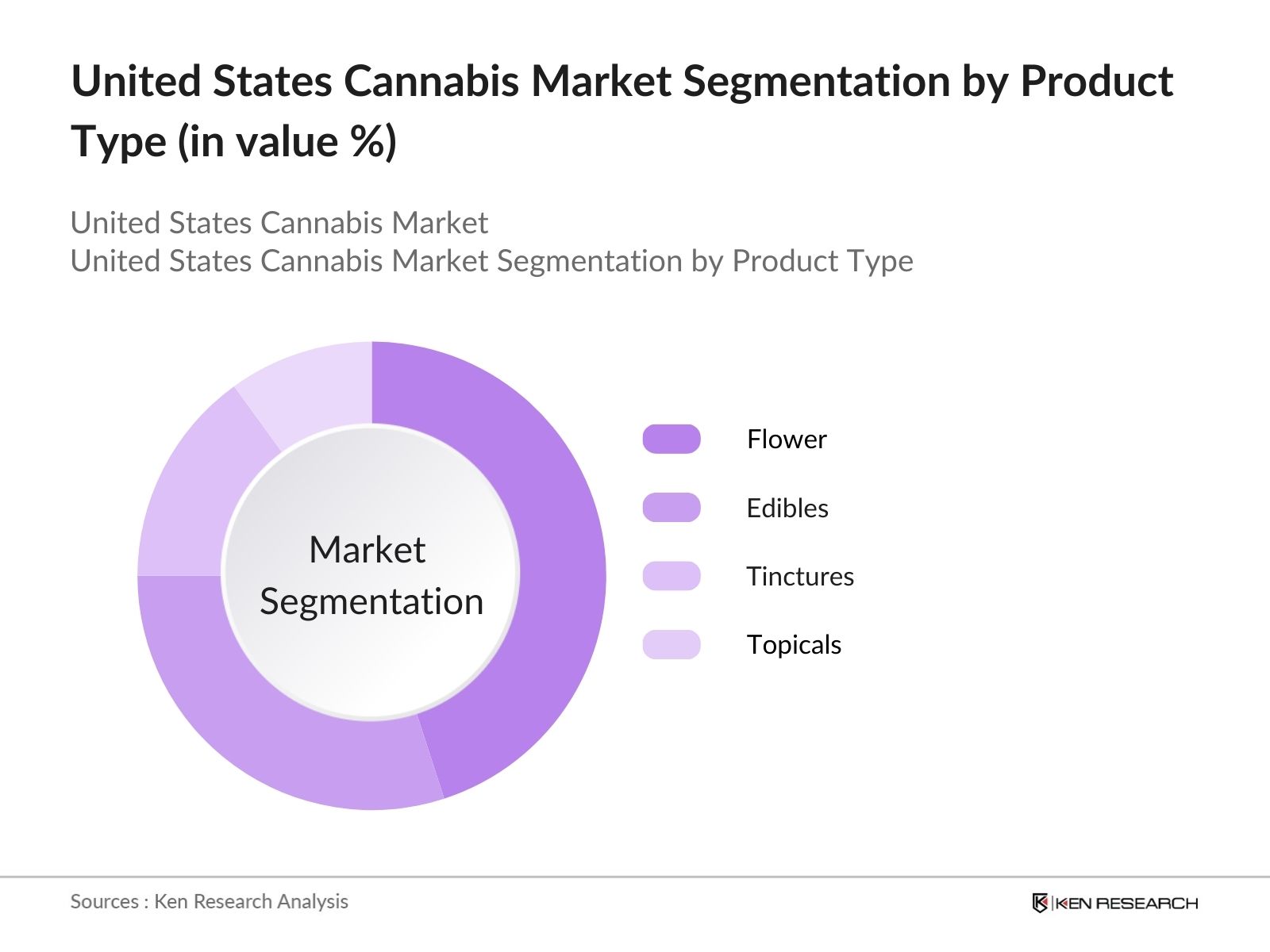

- By Product Type: The market is segmented by product type into flower, edibles, tinctures, and topicals. Among these, flower holds the largest share, with approximately 45% of the market in 2023. The preference for flower stems from its traditional association with cannabis consumption, as well as its versatility in use through smoking, vaporizing, or infusing. Consumers continue to favor it for its perceived natural form and ease of access through dispensaries. However, edibles are increasingly gaining traction, particularly among new users looking for discreet consumption options.

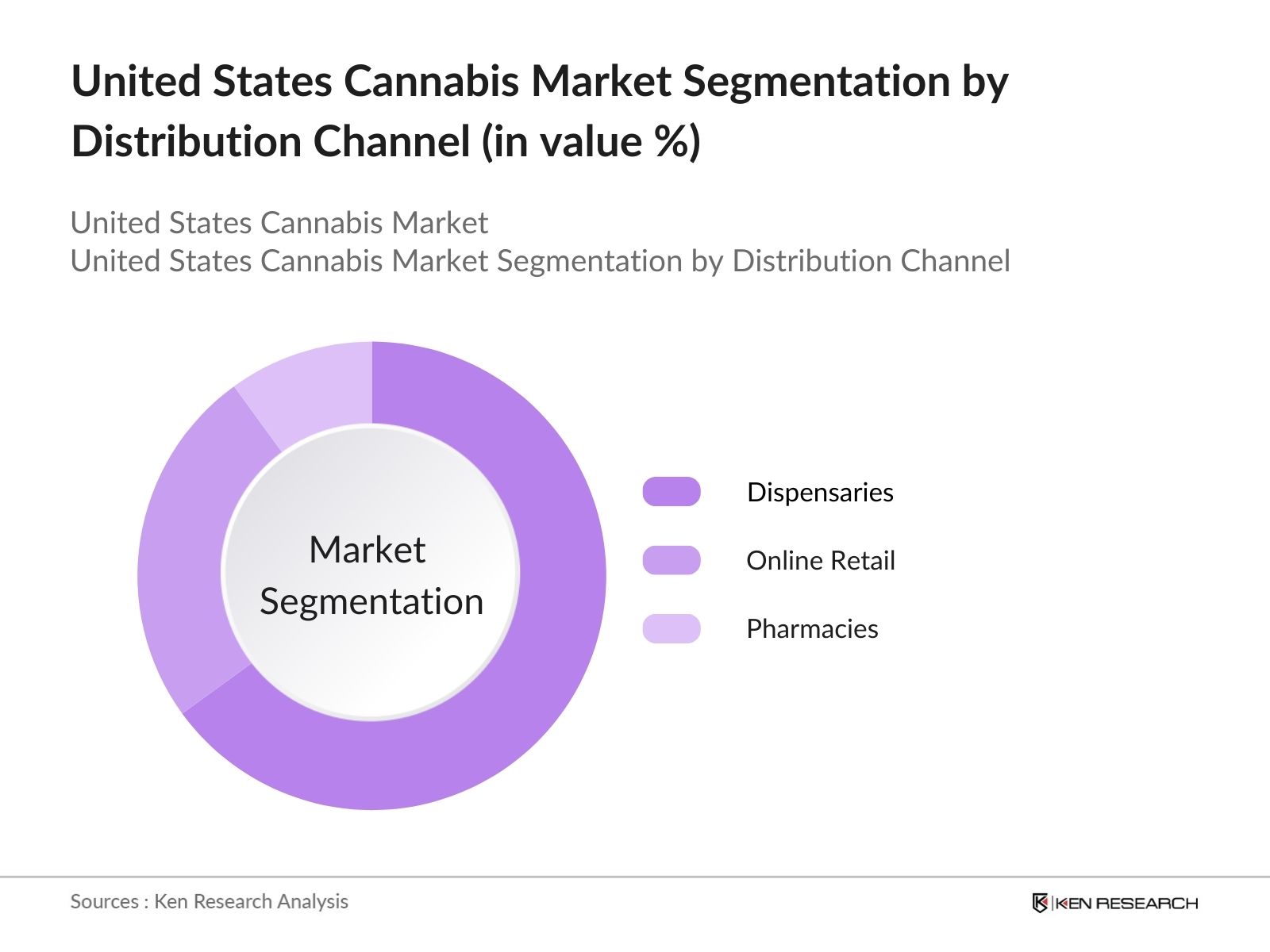

- By Distribution Channel: In terms of distribution, the cannabis market in the U.S. is primarily divided between dispensaries, pharmacies and online retail. Dispensaries dominate with a market share of 65% due to their wide presence, particularly in legal states where consumers prefer in-person purchasing experiences, aided by staff guidance. Dispensaries offer an environment where consumers can explore different strains and products, receive expert advice, and enjoy an instant purchase experience, contributing to their market share.

United States Cannabis Market Competitive Landscape

The U.S. cannabis market is dominated by several key players, each contributing to the rapid evolution of the industry. Leading companies have built strong brands, extensive cultivation facilities, and sophisticated distribution networks to maintain their edge in this competitive landscape. Companies such as Canopy Growth and Curaleaf have invested heavily in research and development, furthering product innovation and expanding into new territories.

The market is highly competitive, with both domestic companies and international brands vying for a larger share. Vertical integration, which allows companies to control the entire supply chain from cultivation to retail, has become a key competitive strategy, ensuring consistent product quality and supply reliability.

|

Company |

Establishment Year |

Headquarters |

No. of Dispensaries |

Cultivation Facilities |

Revenue (2023) |

Product Lines |

Geographical Reach |

Market Strategy |

R&D Investments |

|

Canopy Growth |

2013 |

Smiths Falls, ON |

|||||||

|

Curaleaf Holdings |

2010 |

Wakefield, MA |

|||||||

|

Green Thumb |

2014 |

Chicago, IL |

|||||||

|

Trulieve Cannabis |

2015 |

Quincy, FL |

|||||||

|

Charlottes Web |

2014 |

Boulder, CO |

United States Cannabis Industry Analysis

Market Growth Drivers

- Rising Medical Cannabis Approvals: Medical cannabis has gained widespread acceptance in the U.S., with over 3 million registered patients by 2024. States like Florida saw a 30% increase in medical cannabis patient registration, and Oklahoma reported over 400,000 registered medical cannabis patients in 2023. This surge in approvals reflects growing recognition of cannabiss potential therapeutic benefits for chronic pain, anxiety, and PTSD. As research advances, states like Virginia and New Mexico are enhancing accessibility to medical cannabis products, boosting the market.

- Recreational Use Trends: Recreational cannabis consumption is growing rapidly, especially in states that recently legalized it, such as New York and New Jersey. Data from the New York State Department of Taxation shows that adult-use cannabis sales exceeded $600 million in the first half of 2023. Moreover, Colorado reported that over 600 metric tons of cannabis flower were sold in 2022, reflecting sustained demand for recreational use. Increasing social acceptance and evolving regulations are anticipated to drive further expansion in states considering legalization measures.

- Increased Cannabis Tourism: Cannabis tourism is becoming a economic driver in states where recreational use is legal. For instance, Nevadas cannabis tourism industry contributed over $250 million to the local economy in 2022, driven by visitors flocking to legal dispensaries in Las Vegas. States like Colorado, California, and Oregon are also seeing similar trends, where cannabis tourism has fueled hotel occupancy rates and local tax revenues. This has prompted several other states, such as Michigan, to explore cannabis tourism initiatives as a revenue generator.

Market Challenges

- Federal Banking Restrictions: The inability of cannabis businesses to access traditional banking services due to federal restrictions creates operational and financial challenges. With cannabis still classified under federal law as illegal, businesses are forced to rely heavily on cash transactions, increasing security risks and financial inefficiencies. According to the U.S. Treasury Department, over $12 billion in cannabis-related funds are held outside of regulated banking systems. The SAFE Banking Act has been introduced to alleviate this issue, but legislative progress remains slow, posing a challenge to market growth.

Source: U.S. Treasury Department. - Black Market Competition: The illicit cannabis market continues to pose competition to the legal cannabis industry. In California, it is estimated that black market cannabis sales outpace legal sales by a factor of 2:1, with over $8 billion in annual illicit transactions. This persistent issue undermines the legal market by offering cheaper, untaxed products. In states like Massachusetts, efforts to combat illegal sales through regulatory crackdowns have been slow, allowing illicit operators to capitalize on the high costs associated with legal cannabis compliance.

United States Cannabis Market Future Outlook

Over the next five years, the U.S. cannabis market is expected to see expansion, driven by increasing state-level legalization and federal policy shifts that could pave the way for broader decriminalization. The market will likely witness continued growth in product innovation, particularly in edibles and wellness products like CBD, catering to an increasingly health-conscious consumer base. Additionally, advancements in cultivation technologies, including sustainable farming practices and automation, will reduce production costs and enhance scalability.

The expected entry of large consumer goods companies into the market will also shape future trends, with partnerships between cannabis brands and mainstream retailers becoming more common.

Market Opportunities

- New Recreational States: New states legalizing recreational cannabis present market expansion opportunities. In 2022, New Jersey became one of the latest states to legalize recreational use, generating over $200 million in tax revenue within the first 12 months of sales. Similarly, states like Connecticut and Maryland are expected to drive the next wave of market growth as they implement their own recreational cannabis frameworks. This trend reflects ongoing legislative momentum, which is likely to create new business opportunities for cannabis companies seeking to expand into these emerging markets.

- Rise in Cannabis-Infused Products: The growing demand for cannabis-infused products, including edibles, beverages, and topicals, represents a lucrative opportunity for market players. According to the Nevada Cannabis Compliance Board, sales of cannabis edibles increased by 20% in 2022, reaching over $500 million. States like California and Massachusetts are seeing increased consumer interest in non-smokable cannabis formats, driven by health-conscious individuals seeking alternatives to traditional smoking. This shift in consumer preferences is prompting companies to innovate and diversify their product offerings to capture a broader market.

Scope of the Report

|

Cigarettes Cigars Smokeless Tobacco Roll-Your-Own (RYO) Tobacco E-cigarettes and Vaping Products

|

|

|

By Distribution Channel |

Online Retail Supermarkets/Hypermarkets Tobacco Specialty Stores Convenience Stores Duty-Free Retail |

|

By Consumer Age Group |

18-24 Years 25-34 Years 35-44 Years 45+ Years |

|

By Nicotine Content |

Low Nicotine Medium Nicotine High Nicotine |

|

By Region |

North East West South |

Products

Key Target Audience

Cannabis Cultivators

Licensed Dispensaries

Health and Wellness Companies

Pharmaceutical Manufacturers

Retail Chains

Banks and Financial Institutes

Investments and Venture Capital Firms

Government and Regulatory Bodies (FDA, DEA, State Cannabis Regulatory Agencies)

Consumer Packaged Goods (CPG) Companies

Companies

Players Mention in the Report:

- Canopy Growth

- Curaleaf Holdings

- Green Thumb Industries

- Trulieve Cannabis Corp

- Cresco Labs

- Charlotte’s Web

- Tilray Inc.

- MedMen Enterprises

- Aurora Cannabis

- Aphria Inc.

- Harvest Health & Recreation

- Acreage Holdings

- Columbia Care

- TerrAscend Corp

- Ayr Wellness

Table of Contents

United States Cannabis Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

United States Cannabis Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

United States Cannabis Market Analysis

3.1. Growth Drivers (Legislation, Market Demand, Medical Use, Recreational Use, Tax Revenue)

3.1.1. Federal and State Legalization

3.1.2. Rising Medical Cannabis Approvals

3.1.3. Recreational Use Trends

3.1.4. Increased Cannabis Tourism

3.2. Market Challenges (Federal Restrictions, Banking Limitations, High Taxation, Regulatory Compliance)

3.2.1. Federal Banking Restrictions

3.2.2. Black Market Competition

3.2.3. Regulatory Fragmentation

3.2.4. Marketing and Advertising Restrictions

3.3. Opportunities (Expansion into New States, Product Innovation, Edibles and Beverages, Health and Wellness)

3.3.1. New Recreational States

3.3.2. Rise in Cannabis-Infused Products

3.3.3. Partnerships with Health and Wellness Brands

3.3.4. Growth in CBD-Related Products

3.4. Trends (Mergers & Acquisitions, Vertical Integration, Sustainability Practices, Digital Transformation)

3.4.1. Increase in Vertical Integration Strategies

3.4.2. Adoption of Sustainable Cultivation Practices

3.4.3. Digital and Online Sales Growth

3.4.4. Strategic Mergers & Acquisitions in Cannabis Industry

3.5. Government Regulation (Federal Law, State Laws, Licensing, Interstate Trade, Compliance Costs)

3.5.1. Federal vs. State Discrepancies

3.5.2. License Types and Regulatory Overviews

3.5.3. Taxation Frameworks by State

3.5.4. Compliance and Monitoring Costs

3.6. SWOT Analysis

3.7. Stake Ecosystem (Growers, Dispensaries, Regulatory Agencies, Consumers)

3.8. Porter’s Five Forces (Market Dynamics)

3.9. Competition Ecosystem

United States Cannabis Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Flower

4.1.2. Edibles

4.1.3. Oils & Tinctures

4.1.4. Topicals

4.2. By Application (In Value %)

4.2.1. Recreational

4.2.2. Medical

4.2.3. Industrial Hemp

4.3. By Distribution Channel (In Value %)

4.3.1. Dispensaries

4.3.2. Online Retail

4.3.3. Pharmacies (For Medical Use)

4.4. By Consumer Group (In Value %)

4.4.1. Adult Consumers

4.4.2. Medical Patients

4.4.3. Seniors

4.5. By Region (In Value %)

4.5.1. North

4.5.2. South

4.5.3. West

4.5.4. East

United States Cannabis Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Canopy Growth

5.1.2. Curaleaf Holdings

5.1.3. Green Thumb Industries

5.1.4. Trulieve Cannabis Corp

5.1.5. Cresco Labs

5.1.6. Charlotte’s Web

5.1.7. Tilray Inc.

5.1.8. MedMen Enterprises

5.1.9. Aurora Cannabis

5.1.10. Aphria Inc.

5.1.11. Harvest Health & Recreation

5.1.12. Acreage Holdings

5.1.13. Columbia Care

5.1.14. TerrAscend Corp

5.1.15. Ayr Wellness

5.2. Cross Comparison Parameters (Revenue, Product Portfolio, Retail Footprint, Legal Presence, Licenses, No. of Employees, Headquarters, Profit Margins)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7 Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

United States Cannabis Market Regulatory Framework

6.1. Federal and State Regulations

6.2. Licensing Process

6.3. Compliance Requirements

6.4. Environmental Regulations

United States Cannabis Market Future Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

United States Cannabis Market Future Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By Consumer Group (In Value %)

8.5. By Region (In Value %)

United States Cannabis Market Analysts’ Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase of research involves mapping the entire ecosystem of the U.S. cannabis market, identifying major stakeholders such as cultivators, dispensaries, regulatory bodies, and consumers. Extensive desk research, supported by proprietary databases, is employed to gather detailed industry insights. Key variables, including legal frameworks, consumer demographics, and product segments, are identified as crucial market influencers.

Step 2: Market Analysis and Construction

Historical data on the cannabis market is analyzed to assess penetration rates, consumer behavior, and product demand across different states. Market analysis includes evaluating revenue generation from product segments such as flower, edibles, and CBD products. Data collected ensures accurate projections for future market development.

Step 3: Hypothesis Validation and Expert Consultation

In this phase, hypotheses are formed around market drivers, challenges, and growth opportunities, and validated through consultations with industry experts. These interviews provide firsthand insights into operational strategies, consumer trends, and regulatory impacts.

Step 4: Research Synthesis and Final Output

The final stage synthesizes data from manufacturers, retailers, and other market players, providing a comprehensive overview of the U.S. cannabis market. This analysis, combining top-down and bottom-up approaches, ensures a validated and well-rounded market report.

Frequently Asked Questions

01. How big is the United States Cannabis Market?

The U.S. cannabis market is valued at USD 40 billion, driven by increasing legalization, consumer demand for cannabis-based products, and advancements in medical research supporting cannabis use.

02. What are the challenges in the United States Cannabis Market?

Challenges in the U.S. cannabis market include regulatory fragmentation between states, federal banking restrictions, and high taxation, which complicates market operations and creates barriers for smaller businesses.

03. Who are the major players in the United States Cannabis Market?

Key players in the U.S. cannabis market include Canopy Growth, Curaleaf Holdings, Green Thumb Industries, Trulieve Cannabis Corp, and Charlottes Web, dominating through vertical integration and large-scale cultivation facilities.

04. What are the growth drivers of the United States Cannabis Market?

Growth drivers in U.S. cannabis market include increasing legalization for medical and recreational use, rising consumer interest in CBD-infused products, and growing acceptance of cannabis for therapeutic purposes.

05. What is the future of the United States Cannabis Market?

The U.S. cannabis market is expected to expand , with potential federal legalization on the horizon, increased product innovation, and greater market penetration through online sales and partnerships with mainstream retailers.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.