United States Drone Market Outlook to 2030

Region:North America

Author(s):Sanjeev

Product Code:KROD6874

December 2024

86

About the Report

United States Drone Market Overview

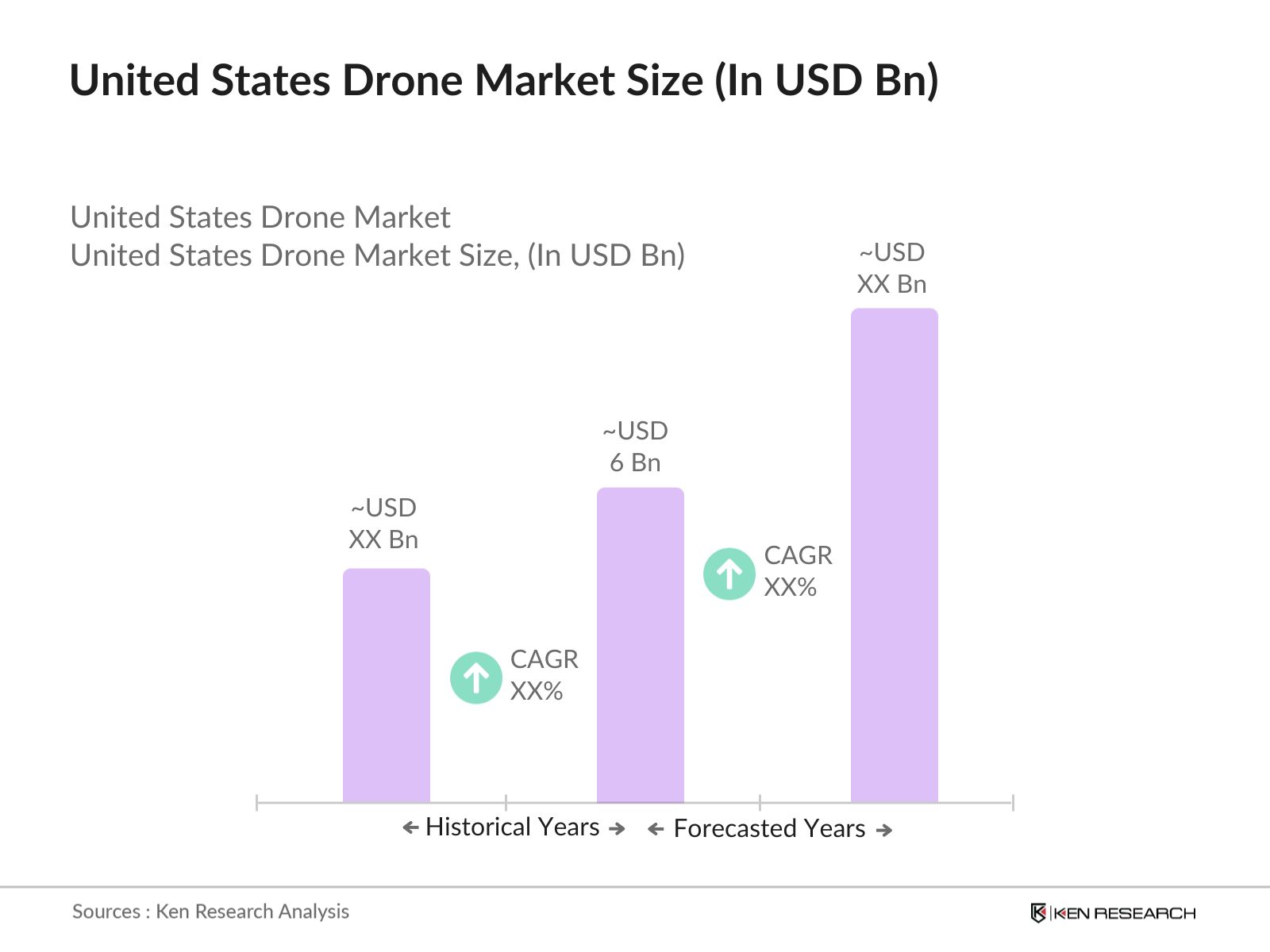

- The U.S. drone market is valued at USD 6 billion, based on a five-year historical analysis. This growth has been largely driven by increasing adoption in both commercial and defense sectors, especially in applications such as agriculture, industrial inspection, surveillance, and e-commerce deliveries. The surge in demand for unmanned aerial vehicles (UAVs) is also linked to technological advancements like AI integration, enhanced battery life, and improved communication systems. Additionally, federal government policies, including FAA regulations, have further encouraged the growth of drone usage, facilitating a controlled yet dynamic environment for innovation in the industry.

- Cities like Los Angeles, New York, and San Francisco are major hubs for drone-related activities in the United States, while states like California and Texas are at the forefront of the industry. These regions dominate due to a combination of factors such as a high concentration of technology firms, the presence of established drone manufacturers, and significant investments in research and development. The strategic presence of tech giants and defense contractors also plays a key role in the dominance of these regions in the U.S. drone market.

- The FAA Part 107 regulation governs the use of small, unmanned aircraft systems (sUAS) for commercial purposes in the U.S. As of 2023, more than 265,000 drone pilots had obtained the FAA Part 107 certification, which permits them to operate drones weighing under 55 pounds for commercial use. This certification mandates operators to adhere to strict guidelines, such as flying only during daylight hours, maintaining visual line of sight (VLOS), and flying below 400 feet in controlled airspace. The FAAs constant updates, including the Remote ID rule, aim to improve safety and accountability in commercial drone operations.

United States Drone Market Segmentation

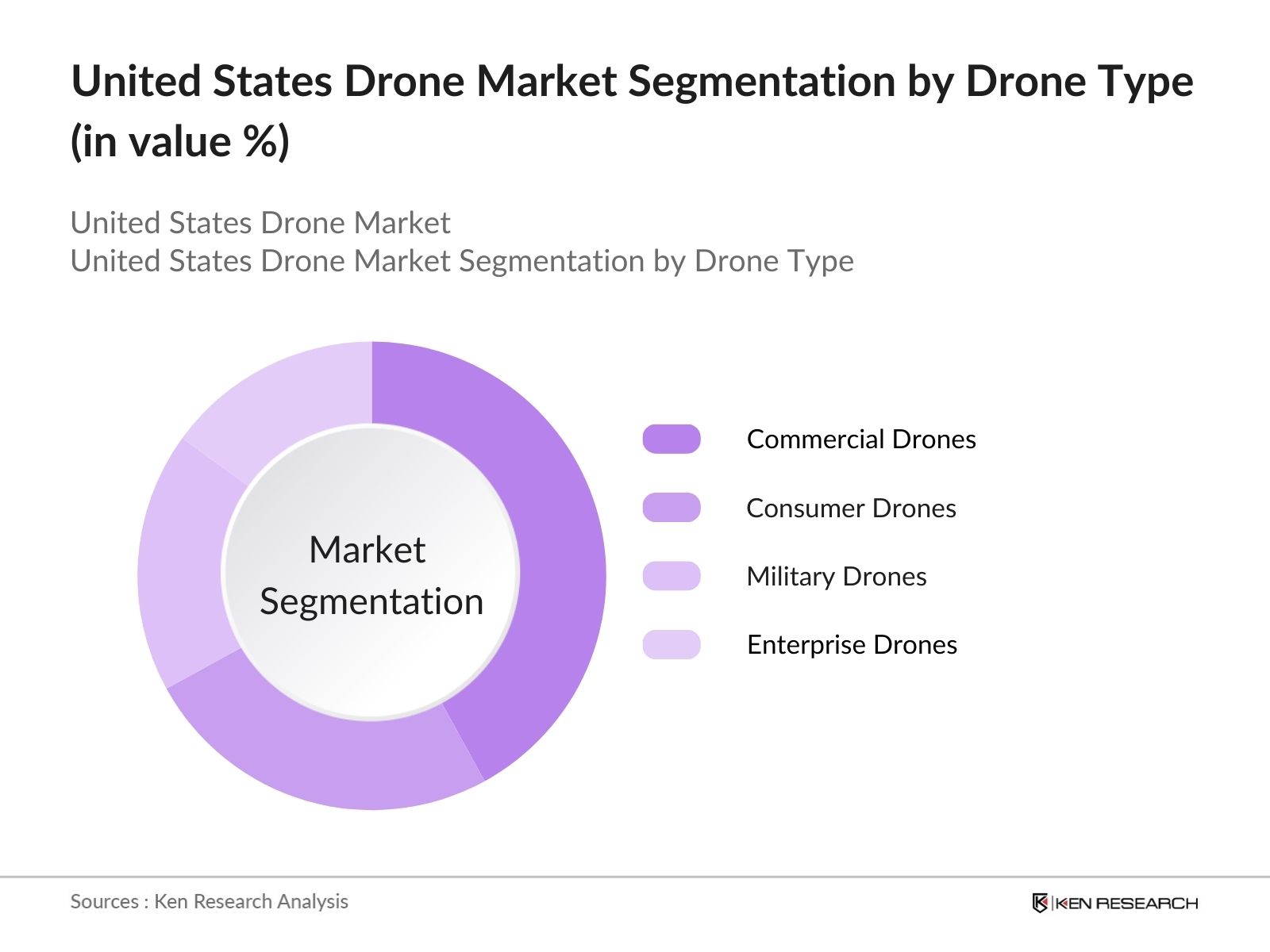

- By Drone Type: The market is segmented by drone type into commercial drones, consumer drones, military drones, and enterprise drones. Recently, commercial drones have dominated the market share due to their growing adoption in sectors such as logistics, construction, and agriculture. The rise of delivery drones in e-commerce and advancements in drone-enabled data collection for precision agriculture have further contributed to their leading position in the market. Meanwhile, enterprise drones are gaining traction due to their ability to handle more complex tasks with greater precision, such as infrastructure inspection and survey mapping, supported by AI-powered systems.

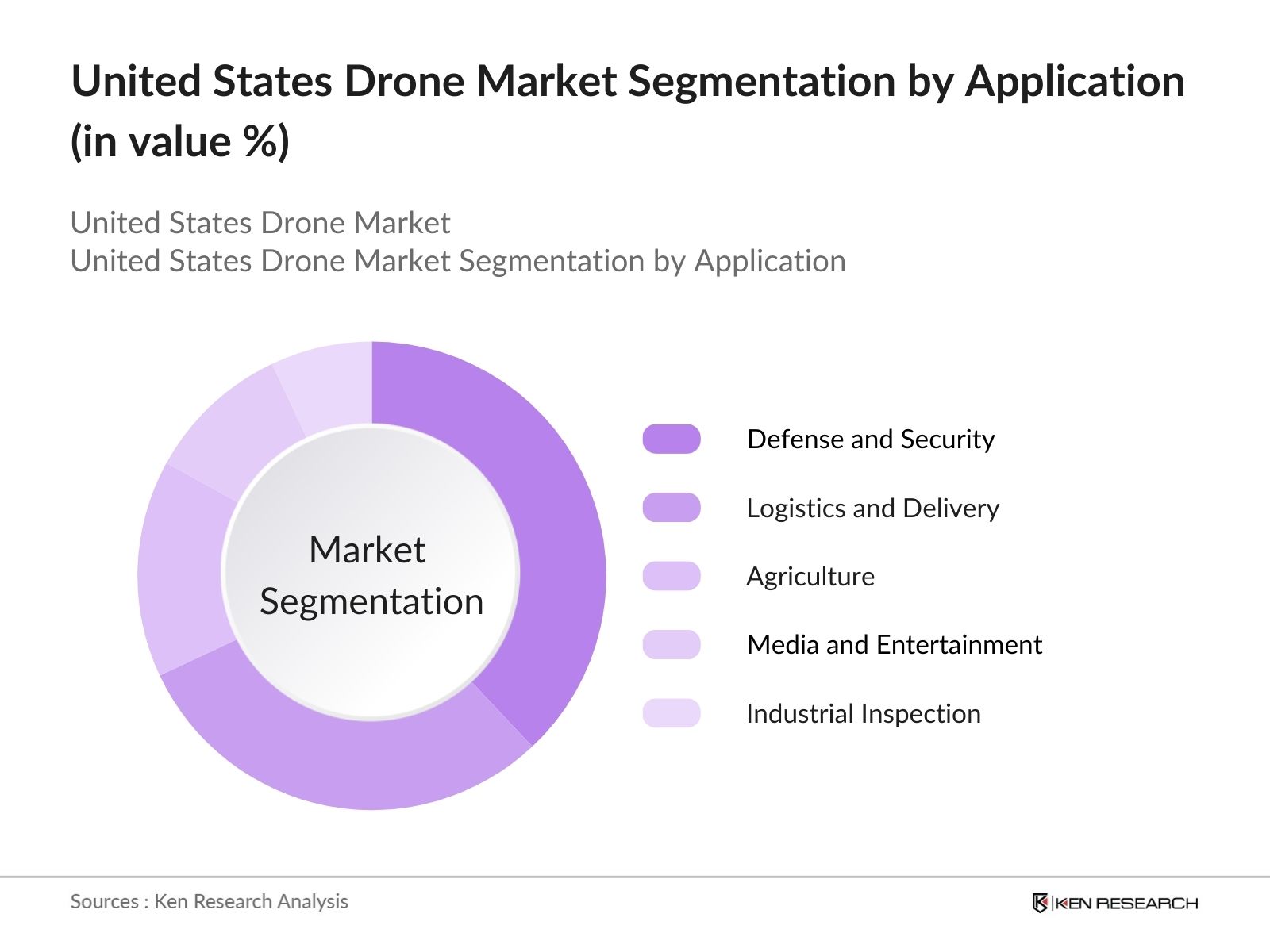

- By Application: The market is further segmented by application into agriculture, logistics and delivery, media and entertainment, defense and security, and industrial inspection. Defense and security dominate the application segment due to the extensive use of military drones in surveillance, reconnaissance, and combat missions. The U.S. government and defense departments have significantly increased investments in military drones to enhance national security and monitor border activities. Additionally, commercial drone applications in logistics are expanding rapidly, driven by the growing need for efficient delivery solutions by e-commerce giants such as Amazon and UPS.

United States Drone Market Competitive Landscape

The U.S. drone market is characterized by the presence of several dominant players, including global giants and emerging local firms. Companies like DJI, Boeing Insitu, and Northrop Grumman have established themselves as leaders in both consumer and defense drone segments. These firms benefit from technological superiority, significant R&D investments, and strategic partnerships. In addition to hardware, the integration of AI, IoT, and cloud-based drone management platforms by software providers is reshaping the competitive landscape, enabling enhanced flight capabilities and operational efficiency.

|

Company |

Establishment Year |

Headquarters |

No. of Employees |

Product Portfolio |

|

DJI |

2006 |

Shenzhen, China |

||

|

Northrop Grumman |

1939 |

Falls Church, USA |

||

|

Boeing Insitu |

1994 |

Bingen, USA |

||

|

Parrot Drones |

1994 |

Paris, France |

||

|

AeroVironment |

1971 |

Simi Valley, USA |

United States Drone Industry Analysis

Market Growth Drivers

- FAA Regulations for Commercial Drones: The Federal Aviation Administration (FAA) has established Part 107, which governs the commercial use of drones in the United States. As of 2023, over 300,000 commercial drones have been registered with the FAA, with expectations for this number to grow as industries like agriculture and logistics increasingly integrate drones into their operations. The FAAs continual revision of rulessuch as the introduction of Remote ID and Beyond Visual Line of Sight (BVLOS) waiversaims to create a structured regulatory environment, promoting the safe expansion of commercial drone use across industries.

- Technological Integration (AI, Machine Learning, Cloud): Technological advancements, particularly in AI and machine learning, have enabled drones to perform complex tasks autonomously, driving higher adoption across various sectors. In 2022, AI-powered drones with machine learning capabilities were used to optimize precision agriculture, analyzing vast amounts of data to improve crop yields. The integration of cloud computing in drone operations has also enabled real-time data processing and remote piloting. The U.S. government has invested $2.3 billion in AI and cloud technologies that are projected to enhance the functionality of drones in both public and private sectors.

- Adoption Across Industries: Drone adoption across multiple industries has surged, with agriculture, defense, logistics, and media being the top adopters. In agriculture, drones equipped with sensors and imaging technology were deployed across over 2 million acres of farmland in 2023, enabling real-time crop monitoring. In defense, the Pentagon allocated $900 million in 2023 to enhance unmanned aerial vehicle (UAV) operations for surveillance. The logistics sector also used drones for last-mile deliveries, with leading retailers like Walmart expanding pilot programs in 2024 to increase delivery efficiency.

Market Challenges

- Regulatory Constraints (Airspace Restrictions, Privacy Laws): Drones in the U.S. face stringent airspace restrictions enforced by the FAA, limiting their deployment in key areas like airports, government buildings, and military zones. By 2023, over 60% of U.S. airspace was subject to some form of drone regulation, hampering commercial expansion in these regions. Privacy concerns have also led to state-specific laws, with over 25 states implementing drone-related privacy legislation as of 2024. These legal constraints pose a challenge for companies seeking to integrate drones into everyday operations, particularly in the logistics and surveillance sectors.

- High Initial Capital Expenditure: One of the significant challenges faced by industries adopting drones is the high initial capital investment required for the technology. By 2023, the average cost of a commercial drone capable of industrial applications ranged between $20,000 and $50,000, excluding additional costs for software integration and maintenance. These costs are prohibitive for small and medium-sized enterprises (SMEs), restricting their ability to capitalize on drone benefits. Despite the availability of government grants and subsidies, the high cost remains a barrier to wider market adoption.

United States Drone Market Future Outlook

Over the next five years, the U.S. drone market is expected to show significant growth, driven by continued federal support, advancements in drone technology, and the expanding applications of drones across sectors such as e-commerce, agriculture, and defense. The development of autonomous drone systems and the integration of AI and 5G technologies are projected to be key catalysts in transforming the market landscape. Additionally, with the FAA actively updating drone regulations, the commercial drone market is set to experience accelerated growth, supported by innovative business models and increasing use cases.

Market Opportunities

- Integration in E-commerce Delivery Systems: E-commerce giants like Amazon and Walmart have increasingly integrated drones into their delivery systems, aiming to enhance last-mile delivery. In 2023, drones were used in over 1 million deliveries in the U.S., with the average delivery time reduced by 40%. As e-commerce expands, particularly in rural areas where traditional delivery methods are inefficient, drones offer a significant opportunity for faster and more cost-effective deliveries. The FAAs approval of BVLOS operations further enhances the capability of drones to cover wider distances, unlocking growth potential in the logistics sector.

- Growth in Defense and Surveillance Applications: The U.S. defense sector has rapidly expanded its use of drones for surveillance and security operations. In 2023, over $1.5 billion was allocated for the procurement of military-grade UAVs, which were deployed for intelligence gathering, border surveillance, and reconnaissance missions. The growing focus on enhancing national security has positioned the defense sector as one of the largest adopters of drone technology. UAVs are also being utilized for disaster management, offering real-time data collection and monitoring during emergencies like wildfires and hurricanes.

Scope of the Report

|

Commercial Drones Consumer Drones Military Drones Enterprise Drones |

|

|

By Application |

Agriculture Logistics and Delivery Media and Entertainment Defense and Security Industrial Inspection |

|

By Payload |

Less than 2kg 2-10kg 10-20kg Above 20kg |

|

By Technology |

AI-Powered Drones Autonomous Drones Hybrid Drones GPS-Controlled Drones |

|

By Region |

North East West South |

Products

Key Target Audience

Defense Contractors (U.S. Department of Defense)

Aerospace Manufacturers

E-commerce Companies (Amazon, UPS)

Agriculture and Farming Solutions Providers

Logistics Companies

Drone Technology Developers

Investors and Venture Capital Firms

Banks and Financial Institutes

Government and Regulatory Bodies (FAA)

Companies

Major Players in the United States Drone Market

DJI

Northrop Grumman

Boeing Insitu

AeroVironment

Parrot Drones

Textron Systems

General Atomics Aeronautical Systems

3D Robotics

Lockheed Martin

PrecisionHawk

Kratos Defense & Security Solutions

FLIR Systems

Yuneec

EHang

Zipline

Table of Contents

1. United States Drone Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. United States Drone Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. United States Drone Market Analysis

3.1. Growth Drivers (Market Regulations, Technological Advancements, Consumer Adoption)

3.1.1. FAA Regulations for Commercial Drones

3.1.2. Technological Integration (AI, Machine Learning, Cloud)

3.1.3. Adoption Across Industries (Agriculture, Defense, Logistics, Media)

3.1.4. Rise of Autonomous Drones

3.2. Market Challenges (Infrastructure, Legal Concerns, Technological Constraints)

3.2.1. Regulatory Constraints (Airspace Restrictions, Privacy Laws)

3.2.2. High Initial Capital Expenditure

3.2.3. Lack of Standardization

3.2.4. Battery Life and Payload Challenges

3.3. Opportunities (Sector Expansion, New Applications, Collaborations)

3.3.1. Integration in E-commerce Delivery Systems

3.3.2. Growth in Defense and Surveillance Applications

3.3.3. Collaborations Between Drone Manufacturers and Software Providers

3.3.4. Use in Disaster Management and Humanitarian Aid

3.4. Trends (Advanced Technologies, New Use Cases)

3.4.1. Growth of UAV Swarms

3.4.2. Advancements in Drone Communication Systems (5G, Satellite Communication)

3.4.3. Commercialization of VTOL Drones

3.4.4. Increasing Role of AI and Automation in Flight Operations

3.5. Government Regulation (FAA Guidelines, State-level Laws, Compliance)

3.5.1. FAA Part 107 Certification

3.5.2. Anti-Drone Technologies and Policies

3.5.3. State-Specific Drone Legislation (Privacy, Surveillance, and Usage)

3.5.4. Public-Private Partnerships in Regulatory Frameworks

3.6. SWOT Analysis

3.7. Stake Ecosystem (Manufacturers, Software Developers, Service Providers)

3.8. Porters Five Forces

3.9. Competition Ecosystem (Competitive Landscape by Market Share, Pricing Strategies, and Innovations)

4. United States Drone Market Segmentation

4.1. By Drone Type (In Value %)

4.1.1. Commercial Drones

4.1.2. Consumer Drones

4.1.3. Military Drones

4.1.4. Enterprise Drones

4.2. By Application (In Value %)

4.2.1. Agriculture

4.2.2. Logistics and Delivery

4.2.3. Media and Entertainment

4.2.4. Defense and Security

4.2.5. Industrial Inspection

4.3. By Payload (In Value %)

4.3.1. Less than 2kg

4.3.2. 2-10kg

4.3.3. 10-20kg

4.3.4. Above 20kg

4.4. By Technology (In Value %)

4.4.1. AI-Powered Drones

4.4.2. Autonomous Drones

4.4.3. Hybrid Drones

4.4.4. GPS-Controlled Drones

4.5. By Region (In Value %)

4.5.1. North

4.5.2. West

4.5.3. South

4.5.4. East

5. United States Drone Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. DJI

5.1.2. Lockheed Martin

5.1.3. Parrot Drones

5.1.4. Northrop Grumman

5.1.5. AeroVironment

5.1.6. Boeing Insitu

5.1.7. General Atomics Aeronautical Systems

5.1.8. PrecisionHawk

5.1.9. 3D Robotics

5.1.10. Yuneec

5.1.11. Textron

5.1.12. Kratos Defense & Security Solutions

5.1.13. Zipline

5.1.14. EHang

5.1.15. FLIR Systems

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Market Share, Inception Year, Revenue, Product Portfolio, R&D Expenditure, Partnerships)

5.3. Market Share Analysis (Market Leaders, Tier-1, Tier-2 Competitors)

5.4. Strategic Initiatives (Partnerships, New Product Launches, R&D Focus)

5.5. Mergers And Acquisitions (Notable Deals in the Last 3 Years)

5.6. Investment Analysis (Major Funding Rounds, Venture Capital)

5.7. Government Grants (FAA Research Grants, State-specific Subsidies)

5.8. Private Equity Investments (Private Investments into Drone Startups)

6. United States Drone Market Regulatory Framework

6.1. Federal Aviation Administration (FAA) Guidelines

6.2. Compliance Requirements (Airspace, Pilot Certifications, Drone Insurance)

6.3. Certification Processes (Remote ID Certification, Airworthiness Certifications)

7. United States Drone Market Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. United States Drone Market Future Market Segmentation

8.1. By Drone Type (In Value %)

8.2. By Application (In Value %)

8.3. By Payload (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

9. United States Drone Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase of research focuses on mapping the ecosystem of the U.S. Drone Market, involving key stakeholders such as manufacturers, service providers, and regulatory bodies. Secondary data sources and proprietary databases are used to gather detailed information on market trends, revenue models, and technological advancements. This step aims to define and quantify the major variables that shape the market.

Step 2: Market Analysis and Construction

In this stage, we compile historical data on the U.S. Drone Market, focusing on market penetration across commercial, consumer, and defense segments. Analyzing drone adoption rates, revenue growth, and key operational factors, we validate market estimates and trends. This ensures a holistic understanding of market dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Our research team develops market hypotheses, which are then validated through interviews with industry experts, including senior executives at drone manufacturing companies and government officials from the FAA. These consultations provide critical insights into the operational challenges and opportunities in the market.

Step 4: Research Synthesis and Final Output

The final phase of the research involves direct engagement with drone manufacturers, service providers, and end-users to collect in-depth insights on product innovation, consumer preferences, and regulatory challenges. This interaction ensures the accuracy of the data derived from both top-down and bottom-up approaches.

Frequently Asked Questions

01. How big is the U.S. Drone Market?

The U.S. drone market is valued at USD 6 billion, driven by growing demand for drones across commercial, consumer, and defense sectors, along with advancements in UAV technology and government regulations.

02. What are the challenges in the U.S. Drone Market?

Challenges in the U.S. drone market include stringent FAA regulations, high capital expenditure for commercial applications, and concerns over airspace management and drone security. These factors restrict rapid market expansion.

03. Who are the major players in the U.S. Drone Market?

Key players in U.S. drone market include DJI, Northrop Grumman, Boeing Insitu, AeroVironment, and Parrot Drones. These companies lead the market due to their technological capabilities, extensive R&D investments, and strong global presence.

04. What are the growth drivers of the U.S. Drone Market?

Growth in the U.S. drone market is driven by factors such as advancements in drone technology (AI, 5G), rising adoption in sectors like agriculture and logistics, and increasing defense budgets for UAVs.

05. How is the U.S. government supporting the drone market?

The U.S. government supports the U.S. drone market through the FAAs regulatory framework, which enables controlled commercial drone operations, research grants for autonomous systems, and partnerships with private firms for military UAV development.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.