United States Packaging Materials Market Outlook to 2030

Region:United States

Author(s):Sanjna

Product Code:KROD11084

Region:United States

Author(s):Sanjna

Product Code:KROD11084

November 2024

83

By Material Type: The United States packaging materials market is segmented by material type into plastic, paper and paperboard, metal, glass, and others. Plastic packaging materials hold a dominant market share due to their versatility, lightweight nature, and cost-effectiveness, making them suitable for a wide range of applications across various industries.

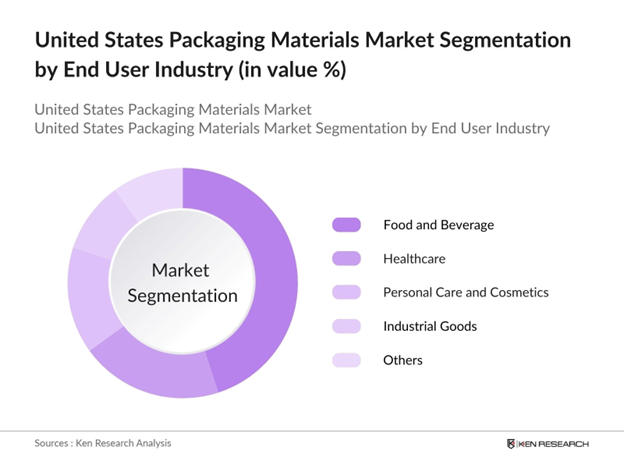

By End-Use Industry: The market is also segmented by end-use industry into food and beverage, healthcare, personal care and cosmetics, industrial goods, and others. The food and beverage industry commands the largest market share, driven by the continuous demand for packaged foods, beverages, and ready-to-eat meals, necessitating diverse packaging solutions to ensure product safety and shelf life.

The U.S. packaging materials market is characterized by the presence of several key players who contribute significantly to market dynamics.

Growth Drivers

Challenges

Over the next five years, the United States packaging materials market is expected to experience steady growth, driven by advancements in sustainable packaging solutions, increasing consumer awareness regarding environmental impact, and the expansion of e-commerce, which necessitates innovative packaging designs to ensure product safety and customer satisfaction.

Market Opportunities

|

Segment |

Sub-Segments |

|

Material Type |

Plastic |

|

Packaging Type |

Rigid Packaging |

|

End-Use Industry |

Food and Beverage |

|

Function |

Primary Packaging |

|

Region |

Northeast |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 E-commerce Expansion

3.1.2 Sustainability Initiatives

3.1.3 Technological Advancements

3.1.4 Consumer Preference Shifts

3.2 Market Challenges

3.2.1 Regulatory Compliance

3.2.2 Raw Material Price Volatility

3.2.3 Environmental Concerns

3.3 Opportunities

3.3.1 Biodegradable Materials Adoption

3.3.2 Smart Packaging Solutions

3.3.3 Emerging Markets Expansion

3.4 Trends

3.4.1 Lightweight Packaging

3.4.2 Recyclable Materials Usage

3.4.3 Digital Printing Integration

3.5 Government Regulations

3.5.1 Environmental Protection Agency (EPA) Guidelines

3.5.2 Food and Drug Administration (FDA) Packaging Standards

3.5.3 State-Level Packaging Waste Regulations

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porter’s Five Forces Analysis

3.9 Competitive Landscape

4.1 By Material Type (In Value %)

4.1.1 Plastic

4.1.2 Paper and Paperboard

4.1.3 Metal

4.1.4 Glass

4.1.5 Others

4.2 By Packaging Type (In Value %)

4.2.1 Rigid Packaging

4.2.2 Flexible Packaging

4.2.3 Semi-Rigid Packaging

4.3 By End-Use Industry (In Value %)

4.3.1 Food and Beverage

4.3.2 Healthcare

4.3.3 Personal Care and Cosmetics

4.3.4 Industrial Goods

4.3.5 Others

4.4 By Function (In Value %)

4.4.1 Primary Packaging

4.4.2 Secondary Packaging

4.4.3 Tertiary Packaging

4.5 By Region (In Value %)

4.5.1 Northeast

4.5.2 Midwest

4.5.3 South

4.5.4 West

5.1 Detailed Profiles of Major Companies

5.1.1 Amcor PLC

5.1.2 International Paper Company

5.1.3 Berry Global Inc.

5.1.4 Sealed Air Corporation

5.1.5 Crown Holdings Inc.

5.1.6 Smurfit Kappa Group PLC

5.1.7 WestRock Company

5.1.8 Ball Corporation

5.1.9 Mondi PLC

5.1.10 Huhtamaki OYJ

5.2 Cross Comparison Parameters

- Revenue

- Market Share

- Product Portfolio

- Regional Presence

- Sustainability Initiatives

- Technological Innovations

- Mergers and Acquisitions

- R&D Investments

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 Environmental Standards

6.2 Compliance Requirements

6.3 Certification Processes

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Material Type (In Value %)

8.2 By Packaging Type (In Value %)

8.3 By End-Use Industry (In Value %)

8.4 By Function (In Value %)

8.5 By Region (In Value %)

9.1 Total Addressable Market (TAM) / Serviceable Available Market (SAM) / Serviceable Obtainable Market (SOM) Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the United States Packaging Materials Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

In this phase, we compile and analyze historical data pertaining to the United States Packaging Materials Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics is conducted to ensure the reliability and accuracy of the revenue estimates.

Market hypotheses are developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

The final phase involves direct engagement with multiple packaging materials manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction serves to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the United States Packaging Materials Market.

The United States packaging materials market is valued at USD 267 billion, driven by the expansion of the food and beverage sector and the growing demand for secure and convenient packaging solutions.

Challenges in United States packaging materials market include regulatory compliance, raw material price volatility, and environmental concerns related to waste management and sustainability, which necessitate continuous innovation and adaptation by industry players.

Key players in United States packaging materials market include Amcor PLC, International Paper Company, Berry Global Inc., Sealed Air Corporation, and Crown Holdings Inc., among others, each contributing significantly to market dynamics.

United States packaging materials market is propelled by factors such as the expansion of e-commerce, sustainability initiatives, technological advancements, and shifts in consumer preferences towards eco-friendly and convenient packaging solutions.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.