U.S. Aircraft Engines Market Outlook to 2030

Region:North America

Author(s):Sanjeev

Product Code:KROD7447

December 2024

81

About the Report

U.S. Aircraft Engines Market Overview

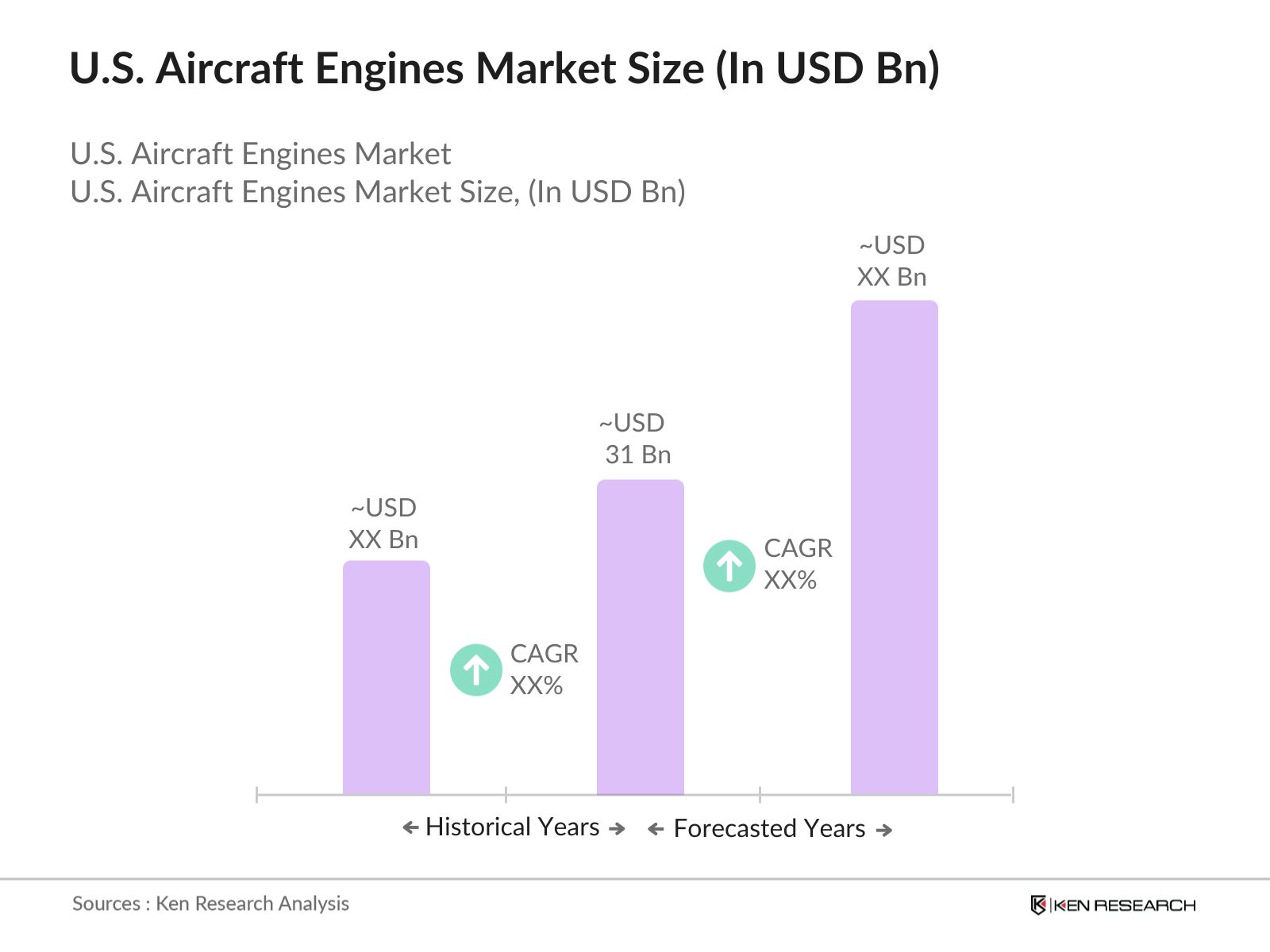

- The U.S. Aircraft Engines market is valued at USD 31 billion, driven by the rising demand for more fuel-efficient and technologically advanced engines. The market's growth is primarily fueled by the increasing number of air travelers and the rising defense budgets, which are aimed at modernizing aircraft fleets. Moreover, advancements in engine design focusing on reduced fuel consumption and lower emissions have further contributed to the expansion of this market. The growth is further bolstered by the emergence of hybrid-electric and hydrogen-powered engines, which are gaining attention as sustainable alternatives in both commercial and defense sectors.

- The market is predominantly concentrated in cities with strong aerospace and defense manufacturing ecosystems, such as Seattle, home to Boeing, and Connecticut, where Pratt & Whitney operates. These regions dominate due to their historical significance, R&D capabilities, and proximity to major aerospace hubs. Additionally, states such as Georgia and Ohio play critical roles in engine manufacturing due to government investments and a skilled workforce in aerospace technology.

- The FAAs new emission standards, targeting a 10% reduction in NOx emissions for new aircraft engines, apply strict criteria to engine manufacturers, demanding advanced design innovations. Compliance with these standards is mandatory for market entry and impacts production processes significantly. Engine manufacturers must implement costly upgrades to meet FAA compliance, adding to the production investment for engines.

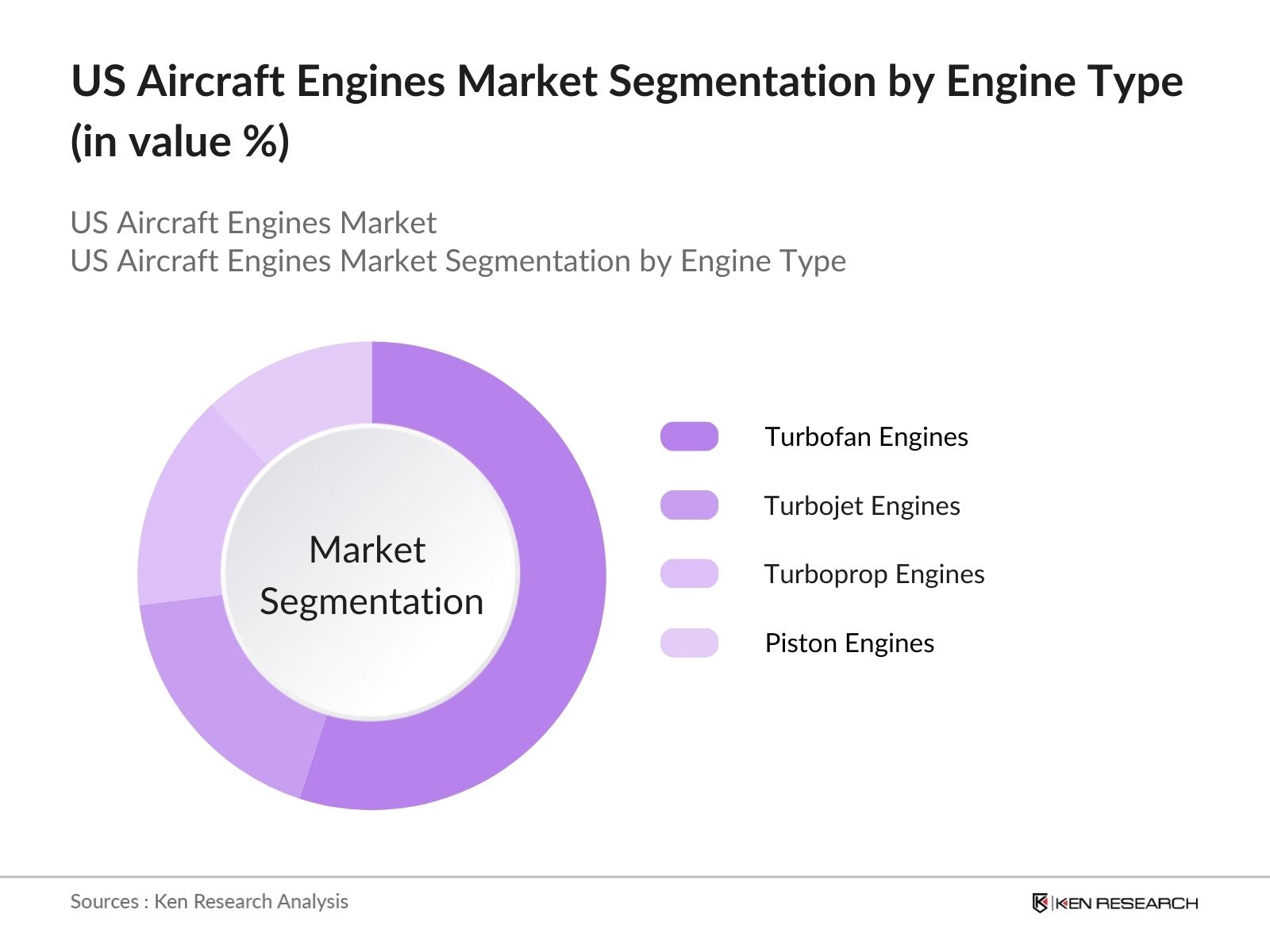

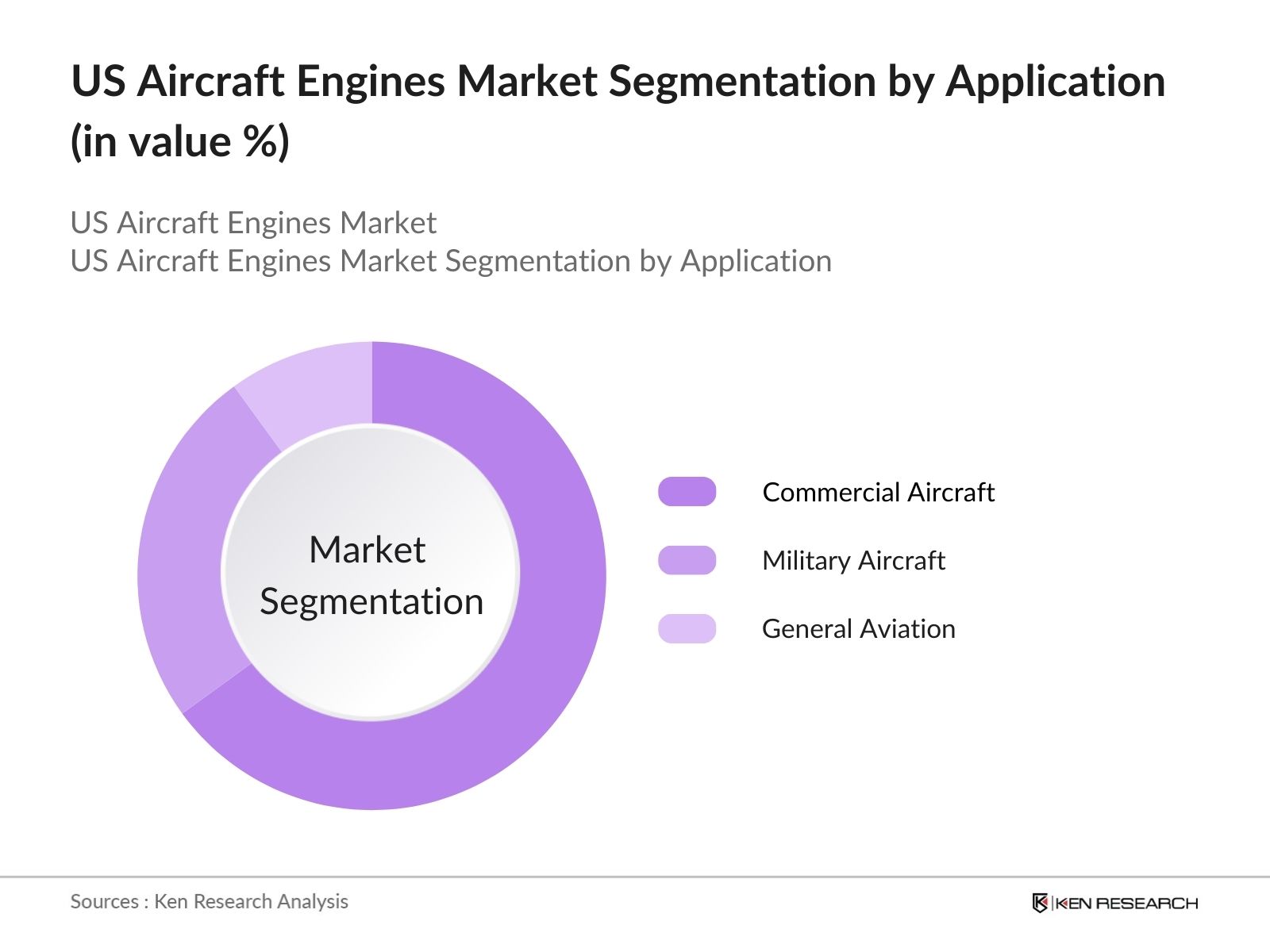

U.S. Aircraft Engines Market Segmentation

The U.S. Aircraft Engines market is segmented by engine type and by application.

- By Engine Type: The market is segmented by engine type into Turbofan Engines, Turbojet Engines, Turboprop Engines, and Piston Engines. Recently, Turbofan Engines have maintained a dominant market share due to their widespread use in commercial and military aircraft. Their high fuel efficiency, reduced noise levels, and ability to power large commercial jets like the Boeing 787 and Airbus A350 have made them the preferred choice for airlines and defense contractors. Additionally, Turbofan engines are critical for long-haul flights, making them integral to the growth of global air travel.

- By Application: The U.S. Aircraft Engines market is also segmented by application into Commercial Aircraft, Military Aircraft, and General Aviation. Commercial Aircraft holds the largest share in this category, driven by the increase in passenger air traffic and the demand for more fuel-efficient engines. Major airlines are prioritizing the acquisition of fuel-efficient aircraft engines to reduce operational costs and meet stringent environmental regulations. Additionally, advancements in hybrid-electric propulsion systems are expected to further enhance the market dominance of the commercial segment.

U.S. Aircraft Engines Market Competitive Landscape

The U.S. Aircraft Engines market is dominated by several key players with significant market influence. These companies have established themselves through innovation, strategic partnerships, and government contracts in the aerospace and defense sectors. The market consolidation highlights the competitiveness and barriers to entry for new players.

U.S. Aircraft Engines Market Analysis

Growth Drivers

- Increasing Passenger Air Traffic: The growth in U.S. passenger air traffic has been evident as airports saw an average of over 2.5 million passengers per day in 2024, marking increased demand for efficient and reliable aircraft engines. Data from the Bureau of Transportation Statistics indicates over 850 million U.S. air travelers annually, reinforcing the demand for high-performance engines. This surge in air travel pushes engine manufacturers to enhance engine reliability and efficiency to meet operational demands. The current fleet maintenance and upgrade requirements have accelerated engine manufacturing orders.

- Rising Demand for Fuel-Efficient Engines: In 2024, the U.S. saw increased fuel consumption in the aviation sector, accounting for 10 billion gallons annually, highlighting a need for fuel-efficient engine technology. The U.S. Department of Energy has incentivized R&D on advanced engine technology with a focus on reducing fuel use per passenger mile, further bolstering demand for fuel-efficient aircraft engines. With operational fuel costs accounting for nearly 30% of airline expenses, airlines have turned to fuel-efficient engines to improve cost-effectiveness.

- Defense Budget Expansions (Military Aircraft Engine Orders): The U.S. defense budget allocated $84 billion to the Air Force in 2024, with $7 billion earmarked specifically for aircraft upgrades and engine procurement. The Department of Defense has invested in next-generation fighter jets, requiring advanced engine technology with increased power and durability. Rising defense allocations underline the ongoing government commitment to superior engine capabilities, aligning with increased production demands in the military segment.

Market Challenges

- High Production Costs: Aircraft engine production involves significant costs due to precision manufacturing and high-grade materials. Data shows that material expenses for jet engines constitute 35% of total production costs, with alloy prices seeing a 20% hike since 2022. The U.S. Bureau of Labor Statistics highlights that these costs are compounded by skilled labor shortages, making production cost-intensive and presenting challenges in scaling engine production.

- Stringent Environmental Regulations: With the aviation industry accounting for 2.4% of global CO emissions, the U.S. Environmental Protection Agency (EPA) has enforced strict emissions standards for aircraft engines. New regulatory thresholds require advanced designs to minimize NOx and particulate matter emissions, making compliance costly for manufacturers. Companies must invest heavily in R&D to meet these stringent standards, adding to development expenses and extending production timelines.

U.S. Aircraft Engines Market Future Outlook

Over the next five years, the U.S. Aircraft Engines market is expected to continue its steady growth. Key factors contributing to this growth include the continuous development of sustainable and fuel-efficient technologies, the rise in air traffic, and increased defense spending on military aircraft modernization. Additionally, hybrid-electric propulsion systems and hydrogen-powered engines are expected to play a pivotal role in reshaping the aircraft engine industry. Government regulations on carbon emissions will likely accelerate investments in green technologies, further driving innovation in the sector.

Market Opportunities

- Growing Adoption of Hybrid-Electric and Hydrogen Technologies: The adoption of hybrid-electric and hydrogen-based engines is gaining traction, with the U.S. Department of Energy funding over $400 million for clean aviation technology in 2024. Research shows that hybrid engines can cut fuel consumption by up to 30% compared to traditional engines, aligning with sustainability goals. With hybrid and hydrogen engines reducing emissions, engine manufacturers are set to benefit from technological advancements in low-emission solutions.

- Investment in Green Technologies: With global aviation emissions under scrutiny, investments in green aviation technology have escalated. The U.S. Federal Aviation Administration (FAA) has allocated $1 billion toward sustainable aviation technologies, encouraging engine manufacturers to pursue innovations in green engines. This support aids manufacturers in lowering emissions and fuel consumption, enhancing market prospects for eco-friendly engine solutions.

Scope of the Report

|

Turbofan Engines Turbojet Engines Turboprop Engines Piston Engines |

|

|

By Application |

Commercial Aircraft Military Aircraft General Aviation |

|

By Technology |

Conventional Jet Engines Hybrid-Electric Engines Hydrogen-Powered Engines SAF-Compatible Engines |

|

By Component Type |

Fan Blades Combustors Turbines Compressors |

|

By Region |

North East West South |

Products

Key Target Audience

Aircraft Manufacturers

Airlines and Commercial Aviation Companies

Military and Defense Contractors

Government and Regulatory Bodies (e.g., FAA, EPA)

Investors and Venture Capitalist Firms

Aerospace R&D Organizations

Aircraft Maintenance, Repair, and Overhaul (MRO) Companies

Suppliers of Aircraft Engine Components

Companies

Major Players in the U.S. Aircraft Engines Market

General Electric (GE)

Pratt & Whitney (Raytheon Technologies)

Rolls-Royce Holdings PLC

Safran Aircraft Engines

Honeywell Aerospace

MTU Aero Engines AG

IAE International Aero Engines AG

Engine Alliance

Williams International

CFM International

UEC-Aviadvigatel (Russia)

Klimov

HondaJet

Lycoming Engines

AECC Commercial Aircraft Engine Co., Ltd.

Table of Contents

1. U.S. Aircraft Engines Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics

1.3.1. Growth Drivers (increased air travel demand, technological advancements, defense sector investment)

1.3.2. Market Restraints (environmental regulations, supply chain disruptions)

1.3.3. Market Opportunities (hybrid-electric propulsion, sustainable aviation fuels)

1.3.4. Key Challenges (cost of innovation, regulatory compliance)

1.4. Market Segmentation Overview

2. U.S. Aircraft Engines Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Major Market Developments and Milestones (fuel-efficient engines, R&D investment, new product launches)

3. U.S. Aircraft Engines Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Passenger Air Traffic

3.1.2. Rising Demand for Fuel-Efficient Engines

3.1.3. Defense Budget Expansions (military aircraft engine orders)

3.2. Market Challenges

3.2.1. High Production Costs

3.2.2. Stringent Environmental Regulations

3.2.3. Supply Chain Volatility

3.3. Opportunities

3.3.1. Growing Adoption of Hybrid-Electric and Hydrogen Technologies

3.3.2. Investment in Green Technologies

3.3.3. Partnerships Between OEMs and Airlines for Sustainable Aviation Fuel (SAF) Initiatives

3.4. Trends

3.4.1. Increasing Demand for Lightweight and Composite Materials

3.4.2. Integration of Digital Twin Technology for Predictive Maintenance

3.4.3. Shift Toward Zero-Emission Aircraft Engines

3.5. Government Regulation

3.5.1. FAA Emission Standards

3.5.2. Defense Contracts and Regulations

3.5.3. U.S. Environmental Protection Agency (EPA) Air Quality Standards

3.6. SWOT Analysis

3.7. Porters Five Forces (Bargaining power of suppliers, threat of substitutes, etc.)

3.8. Competitive Landscape Overview

4. U.S. Aircraft Engines Market Segmentation

4.1. By Engine Type (In Value %)

4.1.1. Turbofan Engines

4.1.2. Turbojet Engines

4.1.3. Turboprop Engines

4.1.4. Piston Engines

4.2. By Application (In Value %)

4.2.1. Commercial Aircraft

4.2.2. Military Aircraft

4.2.3. General Aviation

4.3. By Technology (In Value %)

4.3.1. Conventional Jet Engines

4.3.2. Hybrid-Electric Engines

4.3.3. Hydrogen-Powered Engines

4.3.4. Sustainable Aviation Fuel-Compatible Engines

4.4. By Component Type (In Value %)

4.4.1. Fan Blades

4.4.2. Combustors

4.4.3. Turbines

4.4.4. Compressors

4.5. By Region (In Value %)

4.5.1. North-East

4.5.2. Mid-West

4.5.3. South-East

4.5.4. West

U.S. Aircraft Engines Market Competitive Analysis

5.1. Detailed Profiles of Major Competitors

5.1.1. General Electric Aviation

5.1.2. Rolls-Royce Holdings PLC

5.1.3. Pratt & Whitney (Raytheon Technologies)

5.1.4. Safran Aircraft Engines

5.1.5. Honeywell Aerospace

5.1.6. MTU Aero Engines AG

5.1.7. IAE International Aero Engines AG

5.1.8. Engine Alliance

5.1.9. Williams International

5.1.10. CFM International

5.1.11. UEC-Aviadvigatel (Russia)

5.1.12. Klimov

5.1.13. HondaJet

5.1.14. Lycoming Engines

5.1.15. AECC Commercial Aircraft Engine Co., Ltd.

5.2. Cross Comparison Parameters (Revenue, Number of Employees, R&D Spending, Inception Year, Headquarters, Annual Production Units, Market Share, Key Clients)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Joint Ventures, Partnerships, New Product Development)

5.5. Mergers and Acquisitions

5.6. Investment Analysis (Capital Expenditure, Expansion into Emerging Markets)

5.7. Venture Capital Funding

5.8. Government Grants

6. U.S. Aircraft Engines Market Regulatory Framework

6.1. Federal Aviation Administration (FAA) Guidelines

6.2. Emission and Environmental Standards

6.3. Safety and Certification Requirements

6.4. Export Control and Trade Regulations

7. U.S. Aircraft Engines Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (fuel-efficient engine demand, fleet modernization)

8. U.S. Aircraft Engines Future Market Segmentation

8.1. By Engine Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By Component Type (In Value %)

8.5. By Region (In Value %)

9. U.S. Aircraft Engines Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Competitive Positioning

9.3. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the U.S. Aircraft Engines Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the U.S. Aircraft Engines Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics is conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple aircraft engine manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction serves to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the U.S. Aircraft Engines Market.

Frequently Asked Questions

01. How big is the U.S. Aircraft Engines Market?

The U.S. Aircraft Engines Market, valued at USD 31 billion, is driven by the growing demand for fuel-efficient and low-emission aircraft engines across commercial and defense sectors.

02. What are the challenges in the U.S. Aircraft Engines Market?

Challenges in the U.S. Aircraft Engines market include high production costs, stringent environmental regulations, and supply chain disruptions, particularly in the procurement of critical raw materials.

03. Who are the major players in the U.S. Aircraft Engines Market?

Key players in the U.S. Aircraft Engines Market include General Electric, Pratt & Whitney, Rolls-Royce, Safran Aircraft Engines, and Honeywell Aerospace, known for their extensive R&D investments and global reach.

04. What are the growth drivers of the U.S. Aircraft Engines Market?

The U.S. Aircraft Engines Market is propelled by factors such as increased air travel demand, rising defense budgets, and the push for sustainable aviation solutions through hybrid-electric and hydrogen-powered engines.

05. Which engine type dominates the U.S. Aircraft Engines Market?

Turbofan engines dominate the U.S. Aircraft Engines Market due to their fuel efficiency, lower emissions, and widespread application in both commercial and military aircraft.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.