U.S. Chemical Distribution Market Outlook to 2030

Region:United States

Author(s):Sanjeev

Product Code:KROD527

Region:United States

Author(s):Sanjeev

Product Code:KROD527

November 2024

87

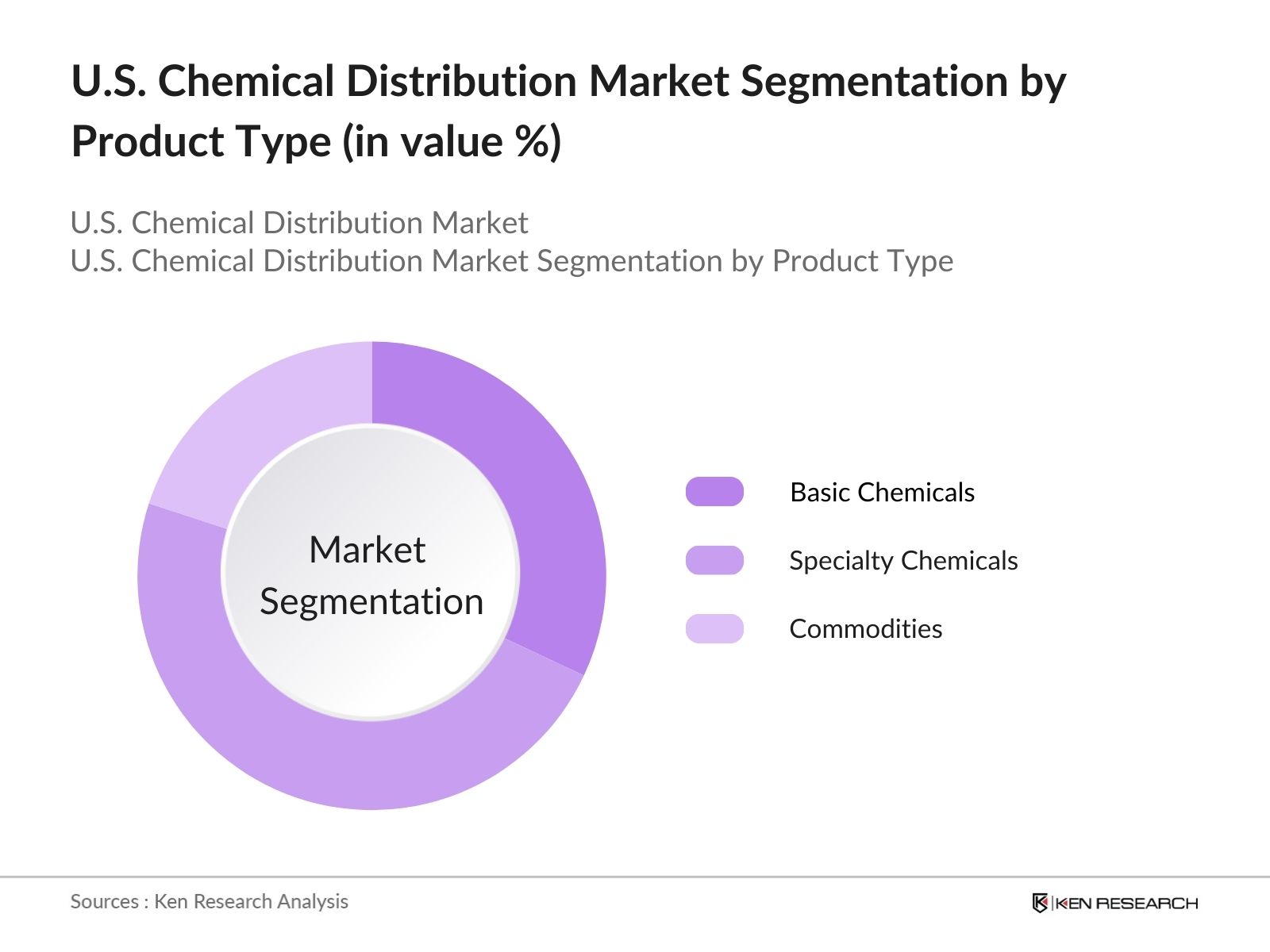

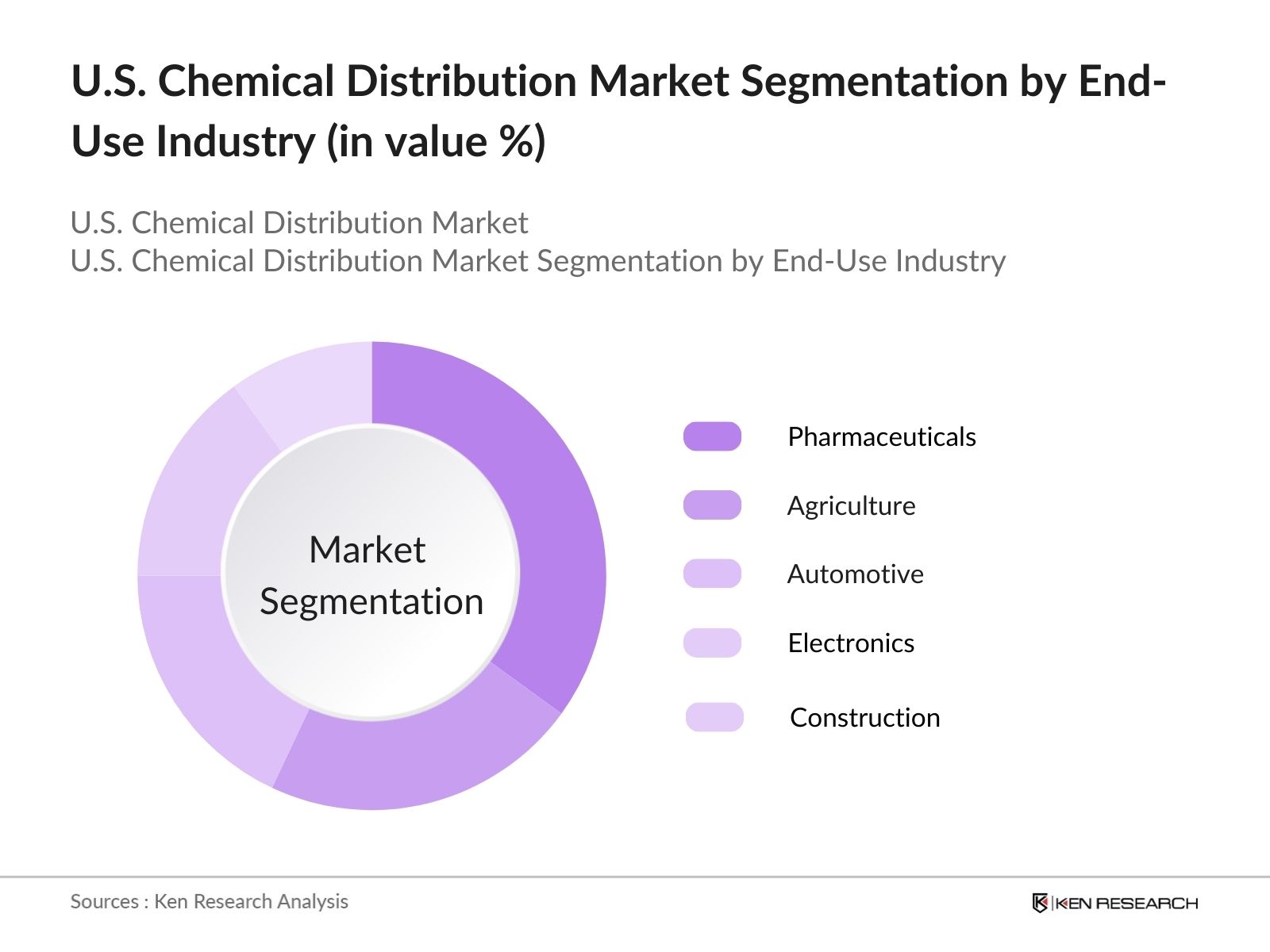

The U.S. chemical distribution market is segmented by product type and by end-use industry.

The U.S. chemical distribution market is dominated by a few key players, including global and domestic distributors. Companies like Brenntag, Univar Solutions, and IMCD have established strong market positions through their vast distribution networks, comprehensive product portfolios, and deep industry relationships. The competitive landscape is characterized by ongoing consolidation, with several mergers and acquisitions shaping the industry. These key players are leveraging their scale to offer innovative solutions and meet the growing demand for specialty chemicals.

|

Company Name |

Establishment Year |

Headquarters |

Revenue |

No. of Employees |

Industry Focus |

|

Brenntag North America |

1874 |

Essen, Germany |

|||

|

Univar Solutions |

1924 |

Downers Grove, IL, USA |

|||

|

IMCD US |

1995 |

Rotterdam, Netherlands |

|||

|

Helm U.S. Corporation |

1900 |

Hamburg, Germany |

|||

|

Barentz North America |

1953 |

Hoofddorp, Netherlands |

Over the next five years, the U.S. chemical distribution market is expected to witness growth, driven by advances in digital supply chains, the growing demand for specialty chemicals, and evolving environmental regulations. The ongoing digital transformation is expected to improve operational efficiencies for distributors, while sustainability trends will push for greener chemical solutions, which will further boost market demand.

|

Basic Chemicals Specialty Chemicals Commodities |

|

|

By End-Use Industry |

Pharmaceuticals Agriculture Automotive Electronics |

|

By Distribution Channel |

Direct Distribution Third-Party Distribution |

|

By Company Size |

Large Enterprises Small and Medium Enterprises (SMEs) |

|

By Region |

North East West South |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers (Supply Chain Efficiencies, Increasing Demand in Downstream Sectors)

3.1.1. Rising Demand in End-Use Industries (Pharmaceuticals, Agriculture, Automotive)

3.1.2. Expansion of Specialty Chemicals

3.1.3. Strategic Partnerships and M&A

3.2. Market Challenges (Pricing Volatility, Regulatory Pressure)

3.2.1. Rising Transportation Costs

3.2.2. Stringent Environmental Regulations

3.2.3. Supply Chain Disruptions

3.3. Opportunities (Growth in E-Commerce, Technological Integration in Distribution)

3.3.1. Digital Transformation of Supply Chains

3.3.2. Development of Sustainable Chemical Solutions

3.3.3. Green Chemistry and Circular Economy Initiatives

3.4. Trends (Automation, Consolidation in the Industry)

3.4.1. Adoption of AI and Machine Learning in Distribution Networks

3.4.2. Consolidation of Major Distributors

3.4.3. Shifting Focus to Specialty Chemicals

3.5. Government Regulations (Hazardous Material Handling, Trade Tariffs)

3.5.1. Chemical Safety Regulations (OSHA, EPA)

3.5.2. Import/Export Compliance and Tariffs

3.5.3. Industry-Specific Regulations (FDA, FIFRA)

3.6. SWOT Analysis

3.7. Value Chain and Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competitive Landscape and Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Basic Chemicals

4.1.2. Specialty Chemicals

4.1.3. Commodities

4.2. By End-Use Industry (In Value %)

4.2.1. Pharmaceuticals

4.2.2. Agriculture

4.2.3. Automotive

4.2.4. Electronics

4.2.5. Construction

4.3. By Distribution Channel (In Value %)

4.3.1. Direct Distribution

4.3.2. Third-Party Distribution

4.4. By Region (In Value %)

4.4.1. North

4.4.2. West

4.4.3. South

4.4.4. East

4.5. By Company Size (In Value %)

4.5.1. Large Enterprises

4.5.2. Small and Medium Enterprises (SMEs)

5.1. Detailed Profiles of Major Companies

5.1.1. Univar Solutions

5.1.2. Brenntag North America

5.1.3. Helm U.S. Corporation

5.1.4. Barentz North America

5.1.5. Nexeo Solutions

5.1.6. IMCD US

5.1.7. ChemGroup

5.1.8. Caldic

5.1.9. Maroon Group

5.1.10. Chemisphere

5.1.11. Azelis Americas

5.1.12. Hawkins Inc.

5.1.13. Tarr LLC

5.1.14. PVS Chemicals

5.1.15. Cornelius Group

5.2. Cross Comparison Parameters (Headquarters, Product Offerings, Revenue, No. of Employees, Distribution Networks, Industry Focus, Sustainability Initiatives, M&A Activities)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, Expansions, M&A)

5.5. Mergers and Acquisitions Overview

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Chemical Safety Standards and Compliance (OSHA, EPA)

6.2. Licensing and Certification Requirements

6.3. Trade Compliance and Tariff Structures

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By End-Use Industry (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By Region (In Value %)

8.5. By Company Size (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. White Space Opportunities

9.4. Strategic Marketing Initiatives

The first step involves mapping the U.S. chemical distribution ecosystem, identifying key stakeholders including manufacturers, distributors, and end-users. Secondary research was conducted using proprietary databases and industry reports to define the primary variables that influence market dynamics.

We compiled historical data related to chemical distribution trends in the U.S. and assessed market penetration, distribution networks, and revenue generation. Service quality and logistics efficiency were evaluated to verify revenue estimates.

Industry hypotheses were validated through in-depth interviews with industry leaders and experts from top chemical distribution firms. These discussions provided critical operational insights, further refining our market forecasts.

Finally, detailed insights were gathered through engagements with key players in the U.S. chemical distribution market, helping to validate our bottom-up approach. This synthesis ensured a thorough and reliable market analysis.

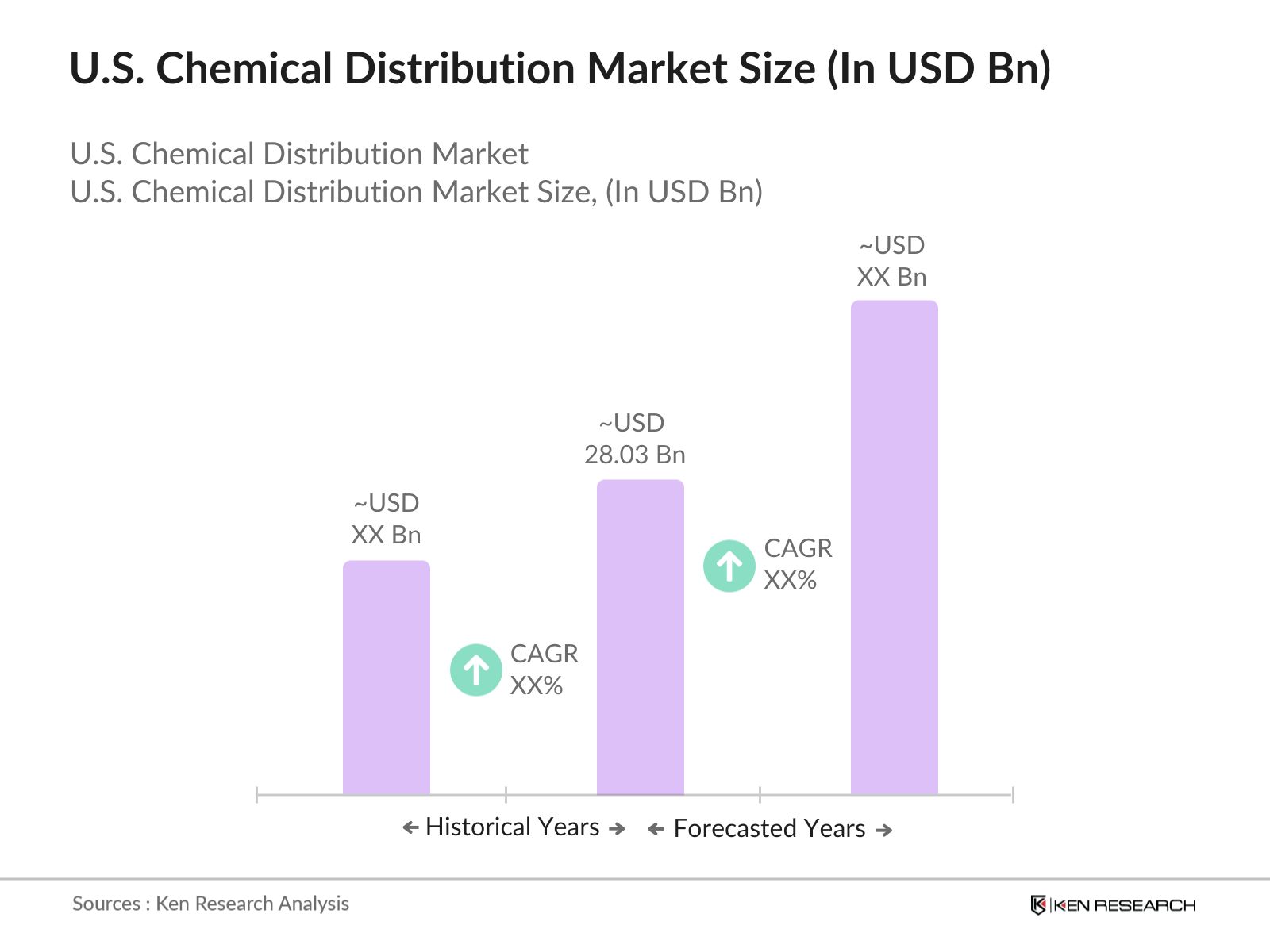

The U.S. chemical distribution market is valued at USD 28.03 billion, driven by increasing demand from various end-use sectors such as pharmaceuticals, agriculture, and automotive.

The U.S. chemical distribution market faces challenges such as pricing volatility due to fluctuating raw material costs, stringent environmental regulations, and rising transportation costs, which put pressure on profitability.

Key players in U.S. chemical distribution market include Brenntag North America, Univar Solutions, IMCD US, Helm U.S. Corporation, and Barentz North America. These companies dominate due to their extensive distribution networks and focus on specialty chemicals.

Growth drivers in U.S. chemical distribution market include the increasing demand for specialty chemicals, advancements in digital supply chains, and the rise of sustainable chemical solutions driven by environmental regulations.

Opportunities in U.S. chemical distribution market lie in the expansion of e-commerce platforms for chemical distribution, increasing demand for sustainable and green chemical solutions, and growth in end-use industries such as pharmaceuticals and electronics.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.