U.S. Contraceptive Market Outlook to 2030

Region:North America

Author(s):Sanjeev

Product Code:KROD9930

December 2024

81

About the Report

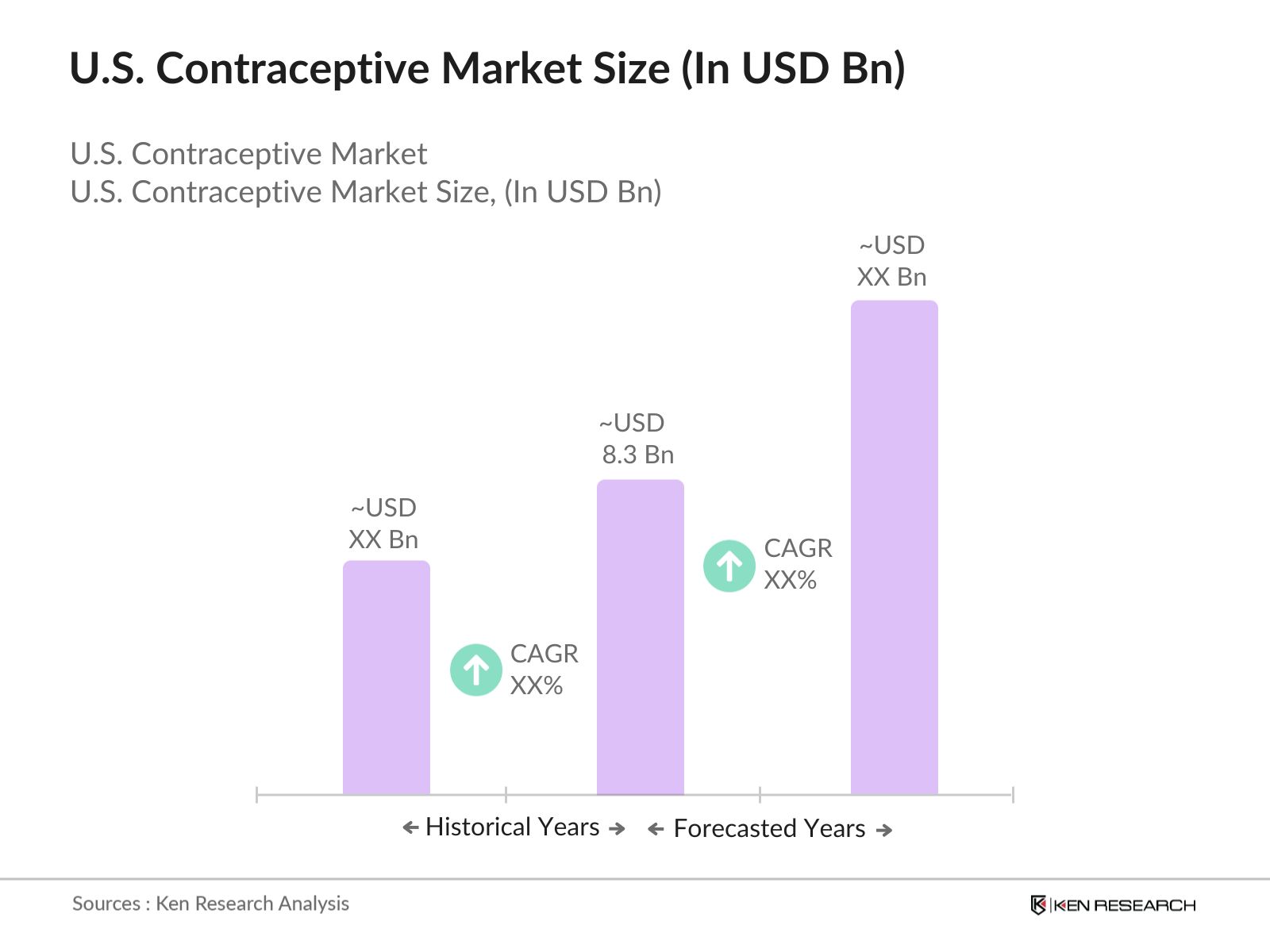

U.S. Contraceptive Market Overview

- The U.S. contraceptive market is valued at approximately USD 8.3 billion, based on a comprehensive five-year historical analysis. This market is driven by factors such as increasing awareness of family planning, the availability of a wide range of contraceptive products, and government support through programs like Medicaid and the Title X Family Planning Program. The accessibility of various contraceptive methods, both prescription and over-the-counter, has spurred demand, especially with rising consumer focus on sexual health and personal choice.

- Cities and regions such as New York, California, and Texas dominate the U.S. contraceptive market due to their large, diverse populations, progressive healthcare policies, and robust healthcare infrastructures. In these areas, access to contraceptives is more widespread due to supportive state policies and higher levels of consumer awareness. Additionally, metropolitan areas often see stronger penetration of innovative contraceptive technologies and services, such as telemedicine, further solidifying their leadership in the market.

- The U.S. Food and Drug Administration (FDA) oversees the approval and regulation of contraceptive products. In 2023, the FDA introduced updated guidelines for over-the-counter oral contraceptives, ensuring they meet the highest standards for safety and efficacy. The FDA continues to regulate contraceptive products to guarantee public health, with 12 new contraceptive products approved between 2022 and 2023.

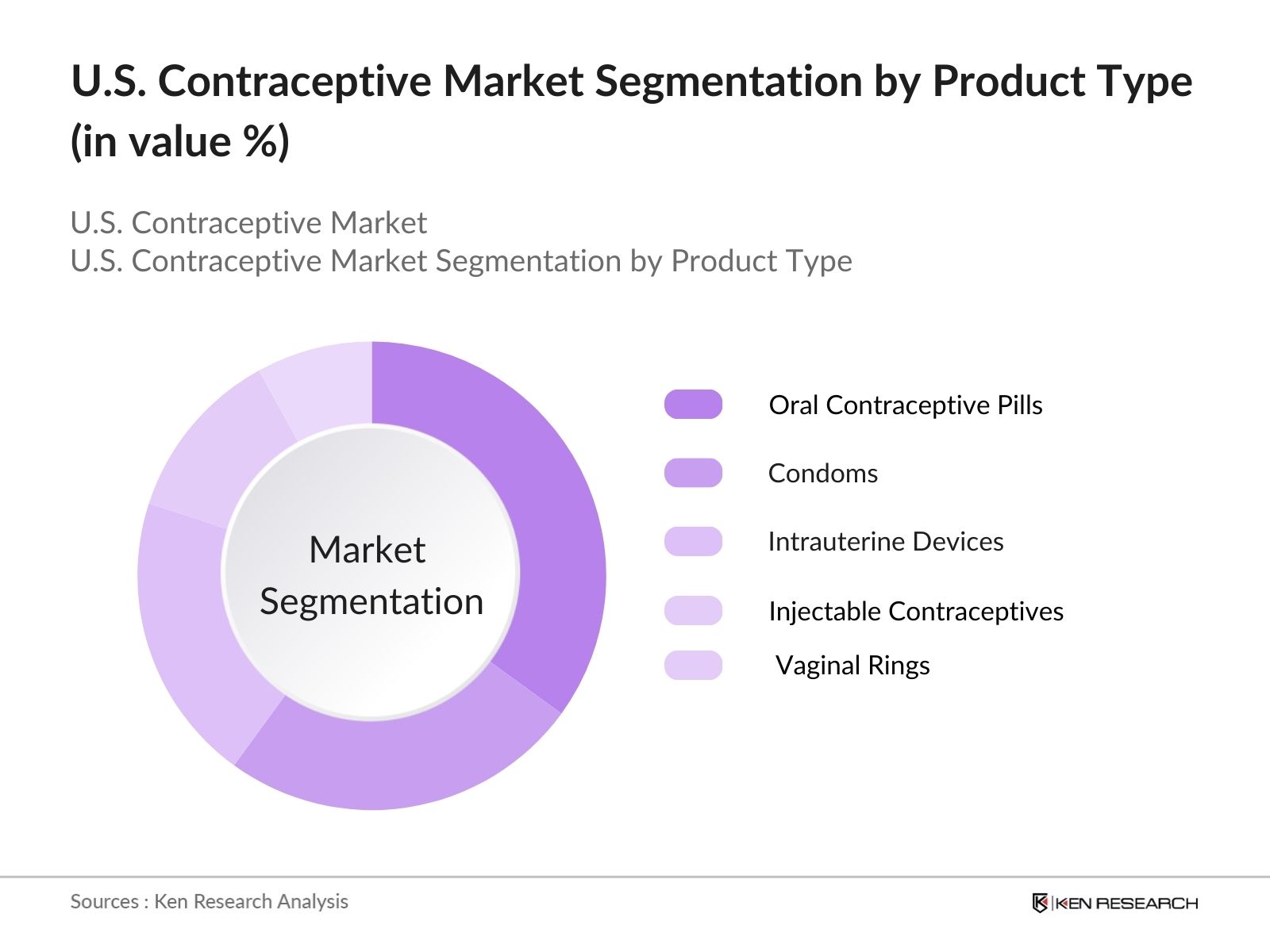

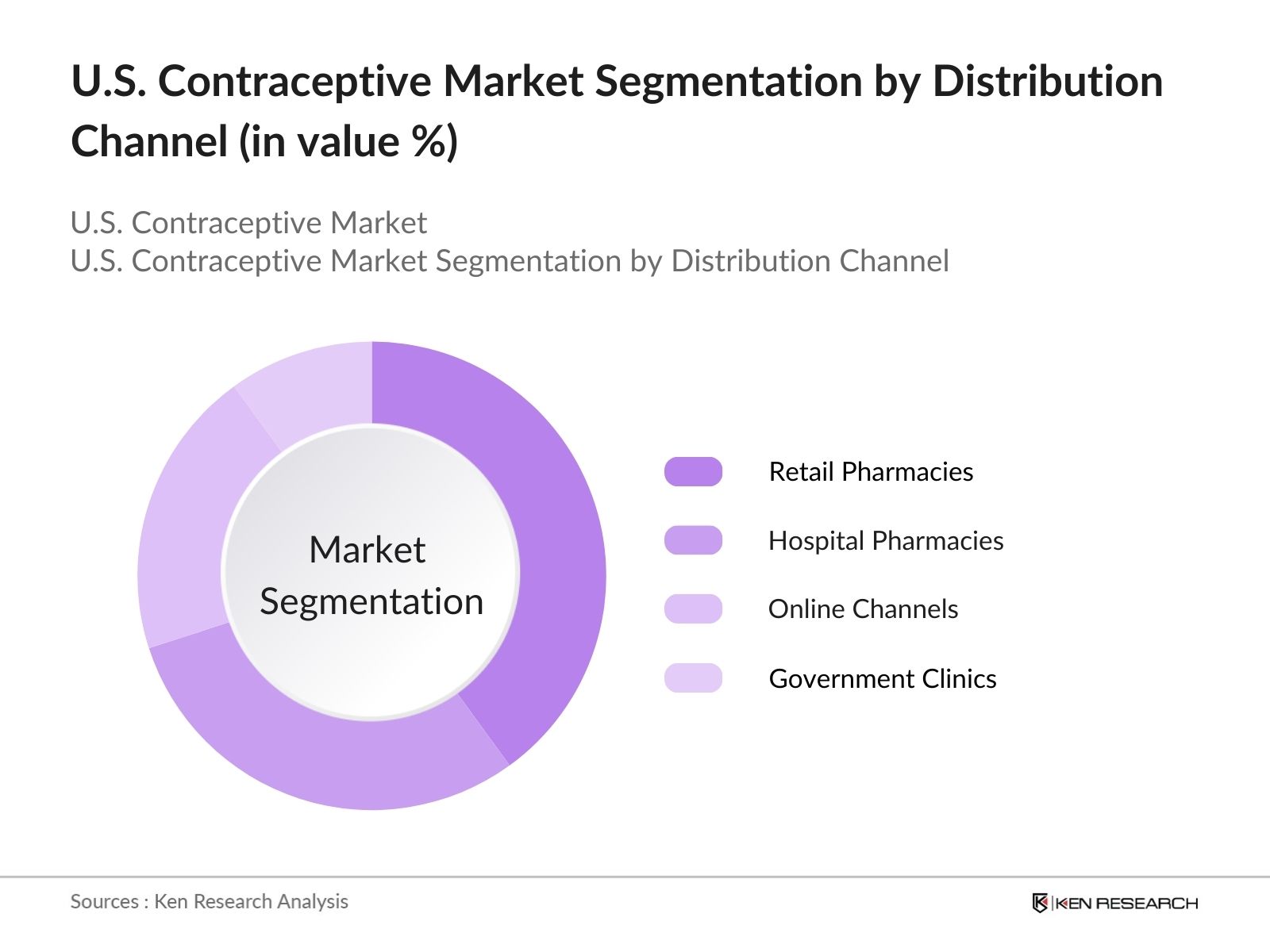

U.S. Contraceptive Market Segmentation

The U.S. contraceptive market is segmented by product type and by distribution channels.

- By Product Type: The U.S. contraceptive market is segmented by product type into oral contraceptive pills, condoms, intrauterine devices (IUDs), injectable contraceptives, and vaginal rings. Oral contraceptive pills have a dominant market share due to their long-standing presence, ease of use, and widespread acceptance among women. Prescription pills are covered under health insurance plans, and they are a preferred method due to their high efficacy and established reputation in the market. The availability of various brands and formulations also caters to different user needs, further reinforcing their dominance.

- By Distribution Channel: In terms of distribution channels, the U.S. contraceptive market is segmented into hospital pharmacies, retail pharmacies, online channels, and government clinics. Retail pharmacies hold the largest share due to their extensive reach and convenience for consumers. Major pharmacy chains like CVS and Walgreens offer a wide range of contraceptive products, making them the most accessible option. Additionally, many retail pharmacies have adopted flexible pricing policies and work with insurance companies to make contraceptives affordable for a broad demographic.

U.S. Contraceptive Market Competitive Landscape

The U.S. contraceptive market is dominated by a mix of global pharmaceutical companies and smaller, innovative startups. These companies offer a variety of products, including oral pills, IUDs, and condoms, and focus on R&D to develop newer contraceptive methods. The presence of established brands ensures market consolidation, but newer entrants are gaining traction with hormone-free and eco-friendly options.

U.S. Contraceptive Industry Analysis

Growth Drivers

- Increasing Awareness of Family Planning: The U.S. government has heavily invested in family planning programs. For instance, the Office of Population Affairs allocates over $280 million annually for family planning services through Title X programs. According to the U.S. Department of Health & Human Services (HHS), the number of women of reproductive age (15-44 years) accessing these services has reached 20 million in 2023, a rise from 18 million in 2022. This increase is supported by rising educational campaigns promoting contraceptive use, directly contributing to heightened awareness and usage of birth control options.

- Government Support Programs (Medicaid, Title X funding): Medicaid provides family planning services to low-income individuals, funding nearly 75% of all public contraceptive services in the U.S. The federal governments funding for contraceptives through Title X amounted to $286 million in 2022, offering access to over 3,000 service sites. In 2023, Medicaid paid for more than 12 million prescriptions of contraceptives. The expansion of these programs ensures contraceptive access across diverse socioeconomic backgrounds, driving market growth.

- Rise in Sexually Transmitted Infections (STI) Prevention Campaigns: The Centers for Disease Control and Prevention (CDC) reported that over 2.5 million cases of sexually transmitted infections were diagnosed in 2023, prompting large-scale national campaigns to prevent STIs through contraceptive use. Such campaigns include condom distribution and education, helping drive demand for contraceptive products. In particular, condoms are a key tool, with nearly 500 million units being supplied through federally funded programs in 2023.

U.S. Contraceptive Market Future Outlook

Over the next few years, the U.S. contraceptive market is expected to experience significant growth due to continuous government support for reproductive health, advancements in contraceptive technologies, and increasing consumer demand for a broader range of options. The rise of telehealth platforms providing access to prescriptions and consultations will further boost market expansion. Additionally, the growing interest in hormone-free alternatives and sustainable contraceptive methods will shape the market landscape in the years to come.

Market Challenges

- Religious and Cultural Barriers: In 2023, nearly 20% of the U.S. population identifies with religious affiliations that discourage contraceptive use, such as Catholicism and certain Evangelical Protestant groups. According to the Pew Research Center, these groups have slowed contraceptive adoption, particularly in rural and conservative regions. In states like Alabama and Utah, these cultural and religious beliefs pose significant barriers to accessing and utilizing contraceptive products.

- High Cost of Prescription Contraceptives: Despite insurance coverage mandates, out-of-pocket costs for certain contraceptives remain high for many women. In 2023, the average retail price for long-acting reversible contraceptives (LARCs) such as intrauterine devices (IUDs) were between $800 and $1,300. For women without insurance coverage or those facing coverage limitations, such costs can pose a significant challenge, reducing the affordability and accessibility of effective contraceptive methods.

Market Opportunities

- Technological Innovations (Smart Contraceptive Devices, Hormonal Advancements): Technological advancements in the U.S. contraceptive market, such as smart contraceptive devices, are presenting new opportunities. In 2023, smart fertility tracking apps had over 6 million users, facilitating better planning for contraceptive use. Additionally, hormonal advancements, such as non-pill methods like hormone patches and implants, have gained popularity, with over 3 million users of hormone patches recorded by the CDC in 2022.

- Increased Role of Telehealth in Birth Control Access: Telehealth has transformed contraceptive access, especially post-pandemic. In 2023, more than 10 million women accessed birth control prescriptions through telehealth services, an increase from 6 million in 2022, according to the U.S. Department of Health & Human Services. This has allowed easier access for women in rural areas where healthcare providers may be scarce, reducing barriers associated with geographic location.

Scope of the Report

|

Oral Contraceptive Pills Condoms Intrauterine Devices (IUDs) Injectable Contraceptives Vaginal Rings |

|

|

By Gender |

Female Contraceptives Male Contraceptives |

|

By Distribution Channel |

Hospital Pharmacies Retail Pharmacies Online Channels Government Clinics |

|

By Age Group |

Teenagers Adults (18-35) Middle-Aged (35-50) |

|

By Region |

North East West South |

Products

Key Target Audience

Pharmaceutical Manufacturers

Retail Pharmacy Chains

Government and Regulatory Bodies (FDA, CDC)

Telemedicine Providers

Health Insurance Companies

Non-Governmental Organizations (NGOs) Focused on Reproductive Health

Investment and Venture Capitalist Firms

Healthcare Service Providers

Companies

Players Mention in the Report:

Pfizer Inc.

Merck & Co.

Bayer AG

CooperSurgical

Teva Pharmaceuticals

Church & Dwight Co., Inc.

Agile Therapeutics

Reckitt Benckiser

Mylan N.V.

Mayer Laboratories, Inc.

Karex Berhad

Cipla Inc.

Ansell Limited

Afaxys, Inc.

Lupin Pharmaceuticals

Table of Contents

1. U.S. Contraceptive Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics (Demand for contraceptive products, regulatory landscape, consumer preferences)

1.4. Market Segmentation Overview (By product type, by distribution channel, by region)

2. U.S. Contraceptive Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis (Adoption rate by product type, government spending, insurance coverage)

2.3. Key Market Developments and Milestones (FDA approvals, major product launches, mergers)

3. U.S. Contraceptive Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Awareness of Family Planning

3.1.2. Government Support Programs (Medicaid, Title X funding)

3.1.3. Rise in Sexually Transmitted Infections (STI) Prevention Campaigns

3.1.4. Expanding Access to Over-the-Counter Products

3.2. Market Challenges

3.2.1. Religious and Cultural Barriers

3.2.2. High Cost of Prescription Contraceptives

3.2.3. Supply Chain Issues Post-COVID

3.3. Opportunities

3.3.1. Technological Innovations (smart contraceptive devices, hormonal advancements)

3.3.2. Increased Role of Telehealth in Birth Control Access

3.3.3. Growing Market for Male Contraceptives

3.4. Trends

3.4.1. Rising Popularity of Long-Acting Reversible Contraceptives (LARCs)

3.4.2. Focus on Hormone-Free Contraceptives

3.4.3. Subscription-Based Contraceptive Delivery Services

3.5. Government Regulations

3.5.1. FDA Guidelines on Contraceptive Products

3.5.2. Contraceptive Coverage Mandates under the Affordable Care Act (ACA)

3.5.3. Title X Family Planning Program

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Manufacturers, regulatory agencies, advocacy groups)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. U.S. Contraceptive Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Oral Contraceptive Pills

4.1.2. Condoms

4.1.3. Intrauterine Devices (IUDs)

4.1.4. Injectable Contraceptives

4.1.5. Vaginal Rings

4.2. By Gender (In Value %)

4.2.1. Female Contraceptives

4.2.2. Male Contraceptives

4.3. By Distribution Channel (In Value %)

4.3.1. Hospital Pharmacies

4.3.2. Retail Pharmacies

4.3.3. Online Channels

4.3.4. Government Clinics

4.4. By Age Group (In Value %)

4.4.1. Teenagers

4.4.2. Adults (18-35)

4.4.3. Middle-Aged (35-50)

4.5. By Region (In Value %)

4.5.1. Northeast

4.5.2. Midwest

4.5.3. South

4.5.4. West

5. U.S. Contraceptive Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Pfizer Inc.

5.1.2. Merck & Co.

5.1.3. Bayer AG

5.1.4. CooperSurgical

5.1.5. Teva Pharmaceutical

5.1.6. Church & Dwight Co., Inc.

5.1.7. Agile Therapeutics

5.1.8. Reckitt Benckiser

5.1.9. Mylan N.V.

5.1.10. Mayer Laboratories, Inc.

5.1.11. Karex Berhad

5.1.12. Cipla Inc.

5.1.13. Ansell Limited

5.1.14. Afaxys, Inc.

5.1.15. Lupin Pharmaceuticals

5.2 Cross Comparison Parameters (No. of Employees, Product Portfolio, Revenue, Market Presence, Innovation Rate, R&D Investments, Global Footprint, Strategic Collaborations)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. U.S. Contraceptive Market Regulatory Framework

6.1 FDA Approval Process

6.2 ACA Contraceptive Coverage Mandate

6.3 Title X Compliance Requirements

7. U.S. Contraceptive Future Market Size (In USD Mn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. U.S. Contraceptive Future Market Segmentation

8.1 By Product Type (In Value %)

8.2 By Gender (In Value %)

8.3 By Distribution Channel (In Value %)

8.4 By Age Group (In Value %)

8.5 By Region (In Value %)

9. U.S. Contraceptive Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Consumer Behavior Insights

9.3 Marketing Strategies

9.4 White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The first step involves the identification of critical market variables that affect the dynamics of the U.S. contraceptive market. This process is supported by extensive desk research and analysis of historical data from reputable sources. The goal is to map the key stakeholders, including manufacturers, distributors, and healthcare providers.

Step 2: Market Analysis and Construction

Historical data from multiple sources is collected and analyzed to understand market trends and consumer behavior. This step includes analyzing the penetration rates of different contraceptive methods and the distribution channels that influence revenue generation.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through expert consultations, involving key industry stakeholders such as healthcare professionals and product developers. These insights provide a clear understanding of product adoption rates, market challenges, and growth opportunities.

Step 4: Research Synthesis and Final Output

The final step involves synthesizing research findings and validating them through engagement with contraceptive manufacturers. This stage ensures the accuracy and reliability of market data, leading to a comprehensive report that includes both quantitative and qualitative insights.

Frequently Asked Questions

01. How big is the U.S. Contraceptive Market?

The U.S. contraceptive market is valued at USD 8.3 billion, driven by the high demand for various contraceptive methods, government support, and increased awareness of family planning and sexual health.

02. What are the challenges in the U.S. Contraceptive Market?

Challenges in U.S. contraceptive market include cultural and religious opposition to contraceptive use in certain regions, high costs for prescription contraceptives, and supply chain issues that affect the availability of certain products, particularly in rural areas.

03. Who are the major players in the U.S. Contraceptive Market?

Key players in U.S. contraceptive market include Pfizer Inc., Merck & Co., Bayer AG, CooperSurgical, and Teva Pharmaceuticals. These companies lead due to their extensive product portfolios, robust R&D investments, and strong distribution networks.

04. What are the growth drivers of the U.S. Contraceptive Market?

Growth drivers in U.S. contraceptive market include increasing government support for family planning initiatives, rising consumer demand for accessible and affordable contraceptive options, and advancements in telemedicine that make it easier for individuals to access prescriptions and consultations.

05. What are the trends in the U.S. Contraceptive Market?

Key trends in U.S. contraceptive market include a growing preference for hormone-free and eco-friendly contraceptives, the expansion of telehealth services for contraceptive prescriptions, and increased demand for long-acting reversible contraceptives (LARCs) such as IUDs and injectables.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.