U.S. Core Banking Software Market Outlook to 2030

Region:North America

Author(s):Sanjeev

Product Code:KROD9619

October 2024

89

About the Report

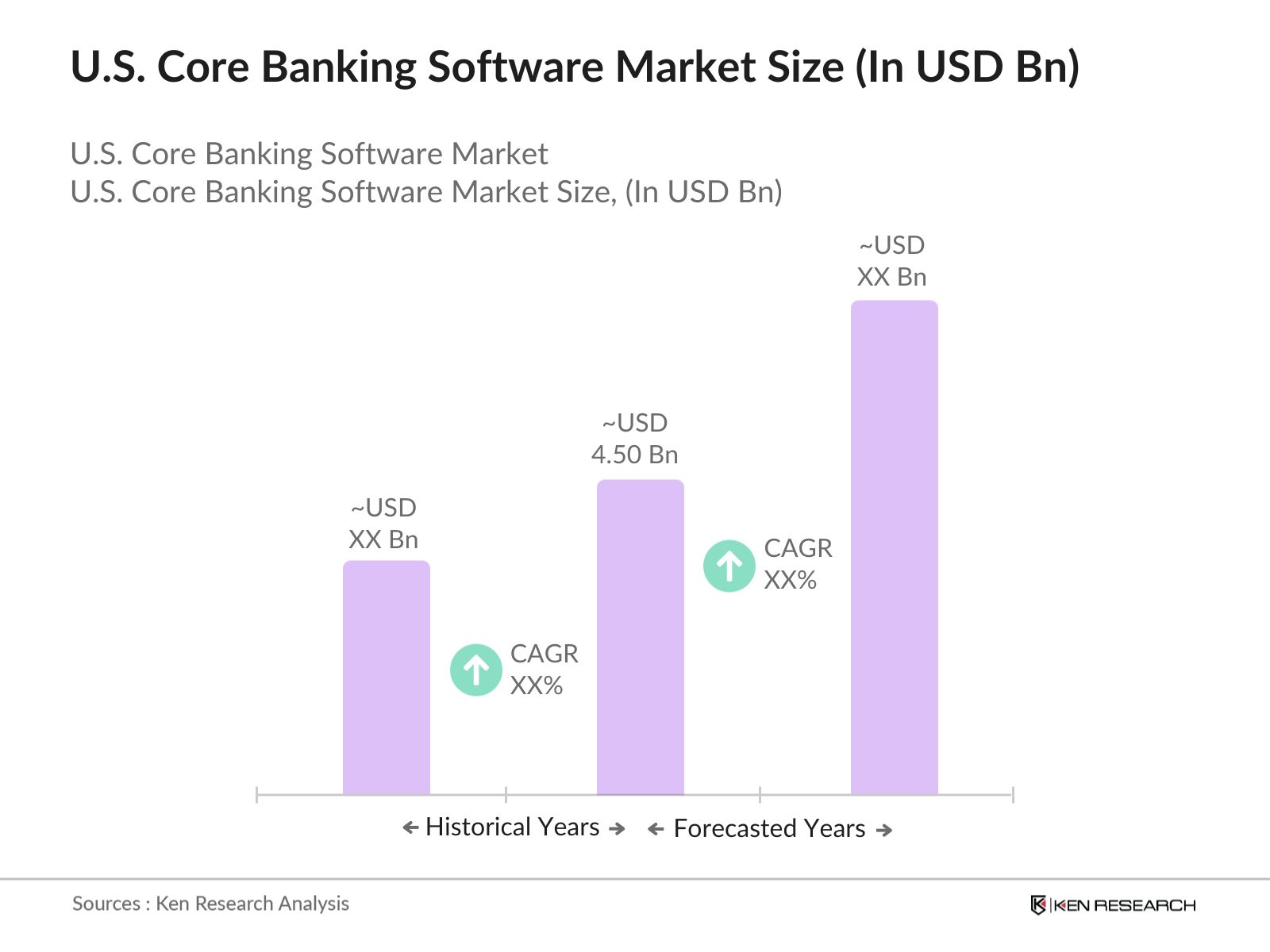

U.S. Core Banking Software Market Overview

- The U.S. Core Banking Software market is valued at USD 4.50 billion based on a comprehensive analysis of market dynamics and historical trends. This valuation is driven by the increasing digitalization of banking services, rising demand for cloud-based core banking solutions, and stringent regulatory requirements that compel financial institutions to upgrade their systems. With the banking sector rapidly adopting newer technologies, such as AI and machine learning, the need for advanced core banking platforms has gained momentum.

- Dominant cities in this market include New York, Chicago, and San Francisco due to their roles as major financial hubs. These cities are home to some of the largest financial institutions that dominate the sector, including JPMorgan Chase, Citibank, and Bank of America. These financial institutions are market drivers because they lead digital transformation efforts, invest heavily in technology, and demand cutting-edge core banking solutions to maintain their competitive edge.

- Financial regulatory reforms, including updates to the Dodd-Frank Act and Basel III, have implications for the U.S. core banking software market. In 2024, U.S. banks have invested over $35 billion to comply with these updated regulations. These reforms require advanced reporting, risk management, and capital adequacy systems, driving demand for sophisticated core banking platforms. The U.S. Federal Reserve and OCC have mandated the use of technology to enhance compliance efforts, further boosting the adoption of core banking software.

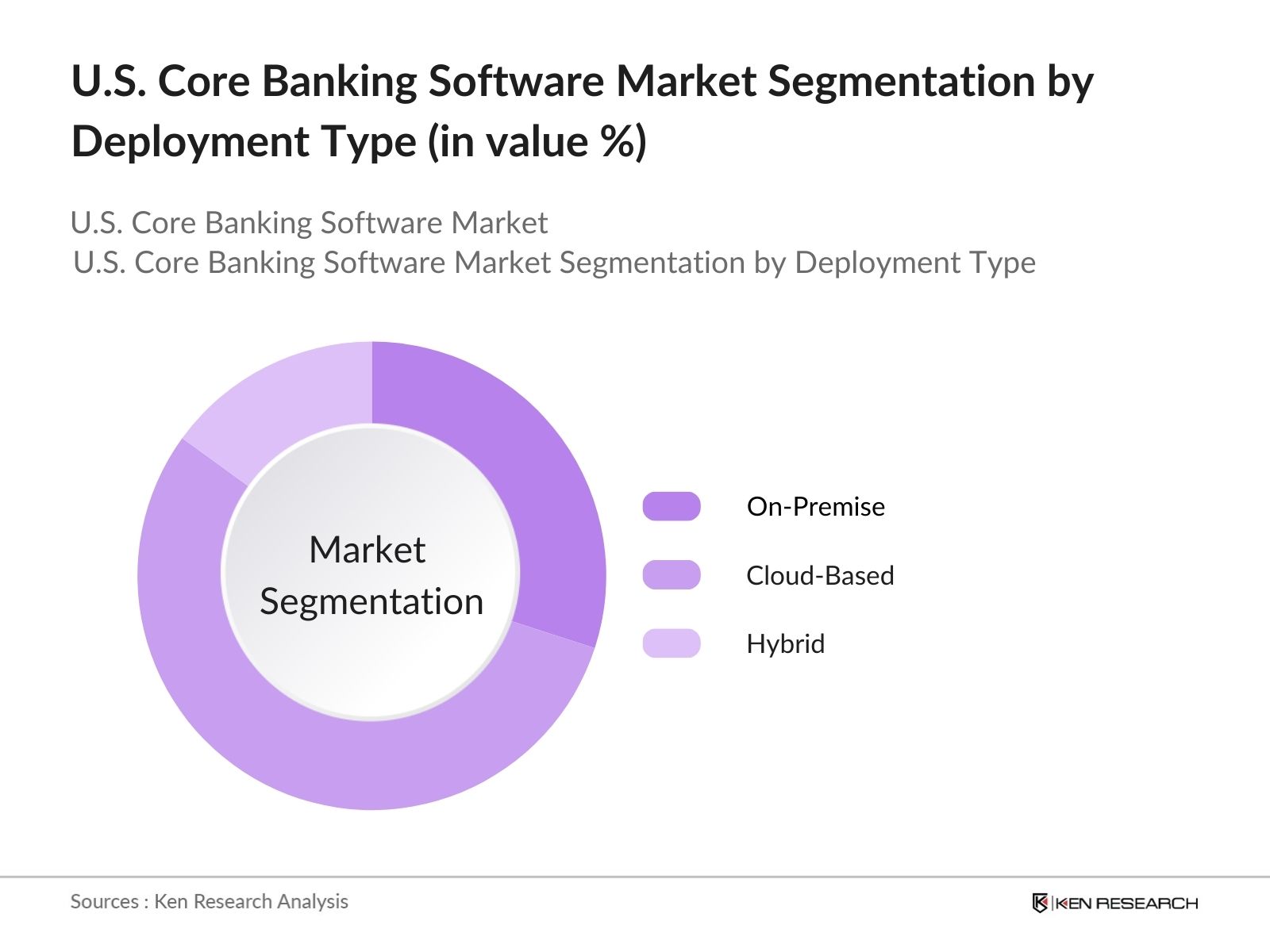

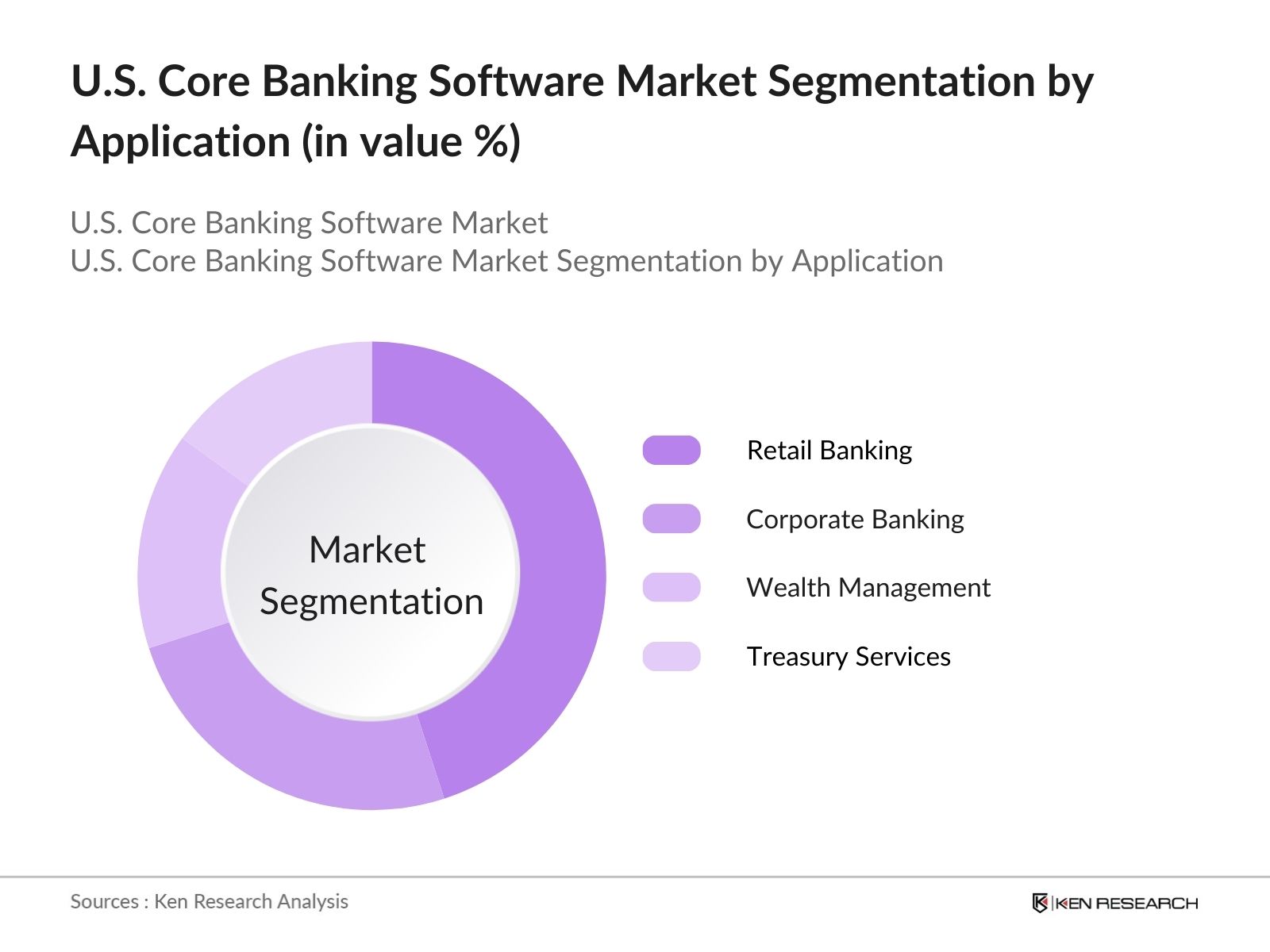

U.S. Core Banking Software Market Segmentation

- By Deployment Type: The market is segmented by deployment type into on-premises, cloud-based, and hybrid solutions. Recently, cloud-based deployments have captured a dominant market share due to their scalability, lower upfront costs, and ability to provide banks with seamless upgrades and improved customer experiences. Banks are increasingly adopting Software-as-a-Service (SaaS) models to streamline their operations, reduce operational costs, and focus on innovation. Cloud-based solutions also support the growing demand for digital banking services, making them highly favored by both large and small financial institutions.

- By Application: The market is segmented by application into retail banking, corporate banking, wealth management, and treasury services. Retail banking has gained the dominant market share, driven by the shift in consumer behavior toward digital banking, mobile applications, and online transactions. Banks are prioritizing investment in core banking platforms that enhance their retail offerings, allowing them to serve customers with personalized products and services, driving operational efficiency. The focus on enhancing customer experience and optimizing internal processes has led to substantial investment in retail banking solutions.

U.S. Core Banking Software Market Competitive Landscape

The U.S. Core Banking Software market is dominated by a few major players that provide a comprehensive range of solutions to financial institutions. Key players are investing in technological advancements and strategic partnerships to maintain their competitive edge. The U.S. market includes both domestic companies and international software providers who play a critical role in shaping the competitive environment. Major players include Fiserv, FIS (Fidelity National Information Services), Oracle, and SAP, which offer innovative products, cloud-based solutions, and seamless integration capabilities.

|

U.S. Core Banking Software Industry Analysis

Growth Drivers

- Digital Transformation in Banking: The U.S. banking sector is witnessing rapid digital transformation driven by evolving customer expectations for seamless, technology-driven experiences. In 2024, over 80% of U.S. banks have integrated at least one form of digital banking, with $3.2 trillion in daily transactions handled through digital channels like mobile banking and online platforms. The U.S. Federal Reserve has reported that these digital services now account for over 75% of all financial activities, promoting a shift towards automated core banking software solutions. The push for modernization is supported by U.S. government initiatives encouraging the adoption of digital solutions in banking.

- Regulatory Compliance Mandates (e.g., Dodd-Frank, Basel III): Regulatory compliance remains a key driver for core banking software adoption, particularly with strict mandates like Dodd-Frank and Basel III. As of 2024, U.S. banks have spent an estimated $35 billion annually to ensure compliance with these regulations. These reforms require robust software platforms to manage risks, ensure transparency, and maintain the necessary capital buffers for financial stability. The U.S. Office of the Comptroller of the Currency (OCC) has mandated banks to adopt technologically advanced solutions to meet compliance reporting standards. This has led to a rise in demand for software that can streamline complex reporting processes and integrate risk management frameworks.

- Rising Adoption of Cloud Technology: Cloud technology adoption within U.S. banks surged in 2024, with over 60% of financial institutions transitioning core banking operations to cloud-based platforms. The shift to cloud solutions has been fueled by the demand for scalable, flexible infrastructure that reduces costs and improves operational efficiency. U.S. banks have reported savings of up to $12 billion in IT infrastructure expenses due to cloud adoption. Additionally, the U.S. government has supported this shift through policies that promote secure and compliant cloud implementations, especially in line with federal data privacy laws.

Market Challenges

- High Implementation and Maintenance Costs: The high costs associated with implementing and maintaining core banking software remain a challenge for U.S. banks. In 2024, large U.S. banks reported spending between $400 million and $800 million on core banking software upgrades and ongoing maintenance. Mid-sized and smaller banks face even more financial strain, with the U.S. Small Business Administration (SBA) reporting that nearly 45% of community banks have delayed digital transformation projects due to prohibitive costs. The need for continuous updates, driven by regulatory changes and cybersecurity concerns, adds to the financial burden.

- Data Security Concerns and Cybersecurity Threats: Cybersecurity remains a critical issue in the U.S. banking sector, with data breaches costing U.S. banks an estimated $18.3 billion in 2023 alone. Core banking systems, which store vast amounts of sensitive financial information, are prime targets for cyberattacks. The U.S. Department of Homeland Security has reported a 27% increase in cyberattacks targeting financial institutions in 2024. The challenge is exacerbated by the integration of new technologies such as cloud and open banking, which introduce new vulnerabilities, pushing banks to invest heavily in secure infrastructure and robust cybersecurity measures.

U.S. Core Banking Software Market Future Outlook

Over the next few years, the U.S. Core Banking Software market is expected to experience continued growth, driven by rapid advancements in cloud technology, artificial intelligence, and machine learning. The increasing demand for digital banking and customer-centric platforms will continue to fuel investments by banks and financial institutions in core banking systems. Furthermore, the regulatory landscape will likely push smaller banks to upgrade their legacy systems to meet compliance standards, thereby increasing market opportunities for SaaS and cloud-based core banking solutions.

Market Opportunities

- Advancements in AI and Machine Learning for Banking Operations: Artificial Intelligence (AI) and Machine Learning (ML) are opening new opportunities for U.S. banks, particularly in enhancing operational efficiency and customer service. By 2024, over 65% of U.S. banks are utilizing AI-powered chatbots and virtual assistants to manage customer queries. AI applications in fraud detection, risk management, and predictive analytics are also gaining traction, with U.S. banks reporting a 30% reduction in fraud incidents through AI-based solutions. The integration of AI in core banking systems allows for real-time data analysis, improving decision-making and operational efficiency.

- Increasing Demand for SaaS-Based Core Banking Solutions: Software-as-a-Service (SaaS) is rapidly becoming the preferred model for core banking solutions in the U.S. As of 2024, more than 55% of U.S. banks have adopted SaaS-based platforms, driven by the flexibility, scalability, and lower upfront costs they offer compared to traditional on-premises solutions. The U.S. government has also supported SaaS adoption through policies that encourage cloud computing and digital banking infrastructure. This trend presents a opportunity for vendors offering secure, compliant, and cost-effective SaaS solutions tailored to the needs of U.S. banks.

Scope of the Report

| By Deployment Type |

On-Premise Cloud-Based Hybrid |

| By Application |

Retail Banking Corporate Banking Wealth Management Treasury Services |

| By Solution Type |

Core Banking Platform Loan Management Customer Relationship Management (CRM) Risk Management |

| By Institution Size |

Large Banks Medium-Sized Banks Small Community Banks and Credit Unions |

| By Region |

North East West South |

Products

Key Target Audience

- Banks and Financial Institutions

- IT Departments of Major Banks

- Investors and Venture Capitalist Firms

- Government and Regulatory Bodies (e.g., FDIC, OCC)

- Technology Service Providers

- Fintech Startups

- Core Banking Solution Providers

- Cloud Service Providers

Companies

Major Players in the U.S. Core Banking Software Market

- Fiserv

- FIS (Fidelity National Information Services)

- Oracle Corporation

- SAP

- Jack Henry & Associates

- Temenos

- Infosys Finacle

- Tata Consultancy Services (TCS)

- Microsoft

- Avaloq

- IBM Corporation

- EdgeVerve Systems

- Finastra

- CGI Group

- Temenos AG

Table of Contents

U.S. Core Banking Software Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Key Growth Metrics

1.4. Market Segmentation Overview

U.S. Core Banking Software Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

U.S. Core Banking Software Market Analysis

3.1. Growth Drivers

3.1.1. Digital Transformation in Banking

3.1.2. Regulatory Compliance Mandates (e.g., Dodd-Frank, Basel III)

3.1.3. Rising Adoption of Cloud Technology

3.1.4. Expansion of Open Banking Initiatives

3.2. Market Challenges

3.2.1. High Implementation and Maintenance Costs

3.2.2. Data Security Concerns and Cybersecurity Threats

3.2.3. Legacy System Integration Issues

3.3. Opportunities

3.3.1. Advancements in AI and Machine Learning for Banking Operations

3.3.2. Increasing Demand for SaaS-Based Core Banking Solutions

3.3.3. Opportunities in Neo-banks and Digital-Only Banks

3.4. Trends

3.4.1. Adoption of Blockchain Technology in Banking

3.4.2. Focus on Customer Experience Enhancements (e.g., personalization, omnichannel integration)

3.4.3. Collaboration with Fintech Companies

3.5. Government Regulations

3.5.1. Financial Regulatory Reforms in the U.S.

3.5.2. Data Privacy Regulations (e.g., GDPR, CCPA)

3.5.3. Anti-Money Laundering (AML) Compliance

3.5.4. Federal and State-Level Guidelines for Digital Banking

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porter’s Five Forces Analysis

3.9. Competition Landscape and Ecosystem

U.S. Core Banking Software Market Segmentation

4.1. By Deployment Type (In Value %)

4.1.1. On-Premise

4.1.2. Cloud-Based

4.1.3. Hybrid

4.2. By Application (In Value %)

4.2.1. Retail Banking

4.2.2. Corporate Banking

4.2.3. Wealth Management

4.2.4. Treasury Services

4.3. By Solution Type (In Value %)

4.3.1. Core Banking Platform

4.3.2. Loan Management

4.3.3. Customer Relationship Management (CRM)

4.3.4. Risk Management

4.4. By Institution Size (In Value %)

4.4.1. Large Banks

4.4.2. Medium-Sized Banks

4.4.3. Small Community Banks and Credit Unions

4.5. By Region (In Value %)

4.5.1. North

4.5.2. West

4.5.3. South

4.5.4. East

U.S. Core Banking Software Market Competitive Analysis

5.1. Detailed Profiles of Major Competitors

5.1.1. Fiserv

5.1.2. FIS (Fidelity National Information Services)

5.1.3. Temenos

5.1.4. Oracle Corporation

5.1.5. SAP

5.1.6. Jack Henry & Associates

5.1.7. Infosys Finacle

5.1.8. Tata Consultancy Services (TCS)

5.1.9. Microsoft

5.1.10. Avaloq

5.1.11. IBM Corporation

5.1.12. EdgeVerve Systems

5.1.13. Finastra

5.1.14. CGI Group

5.1.15. Temenos AG

5.2. Cross-Comparison Parameters (Revenue, Cloud Adoption Rate, Digital Transformation Initiatives, Technology Partnerships, Market Share, Customer Base, Employee Strength, Global Reach)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital and Private Equity Funding

5.8. Government Grants and Incentives

U.S. Core Banking Software Market Regulatory Framework

6.1. Financial Compliance Requirements

6.2. Cloud Computing and Data Localization Laws

6.3. Certification and Compliance Standards

6.4. State and Federal-Level Financial Regulatory Bodies

U.S. Core Banking Software Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

U.S. Core Banking Software Future Market Segmentation

8.1. By Deployment Type (In Value %)

8.2. By Application (In Value %)

8.3. By Solution Type (In Value %)

8.4. By Institution Size (In Value %)

8.5. By Region (In Value %)

U.S. Core Banking Software Market Analysts’ Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The first step in researching the U.S. Core Banking Software Market involves building a comprehensive framework that includes key stakeholders, such as software providers, banks, and regulatory bodies. We begin with extensive secondary research, including industry reports and proprietary databases, to define the critical variables influencing market dynamics.

Step 2: Market Analysis and Construction

We then compile historical data related to the U.S. Core Banking Software market, such as the rate of digital transformation, cloud adoption, and overall market growth. This analysis includes the assessment of the number of financial institutions using different deployment models and the corresponding revenue streams, which help validate our market projections.

Step 3: Hypothesis Validation and Expert Consultation

Through primary research methods, such as interviews with industry experts, including CIOs and IT decision-makers from leading financial institutions, we validate our market assumptions. These consultations provide direct insights into the operational and financial drivers of core banking system adoption.

Step 4: Research Synthesis and Final Output

The final step involves synthesizing data from both primary and secondary sources, ensuring that the final report provides a holistic, data-driven analysis of the U.S. Core Banking Software market. This process includes direct collaboration with core banking software providers to ensure the report accurately reflects the market’s competitive dynamics and future opportunities.

Frequently Asked Questions

01. How big is the U.S. Core Banking Software Market?

The U.S. Core Banking Software market was valued at USD 4.50 billion, driven by increasing digitalization in the financial sector and the growing demand for cloud-based solutions.

02. What are the challenges in the U.S. Core Banking Software Market?

Challenges in the U.S. Core Banking Software market include the high cost of implementation and maintenance, data security concerns, and difficulties in integrating with legacy systems.

03. Who are the major players in the U.S. Core Banking Software Market?

Major players in the U.S. Core Banking Software market include Fiserv, FIS, Oracle, SAP, and Jack Henry & Associates, which dominate due to their comprehensive solutions and strong market presence.

04. What are the growth drivers of the U.S. Core Banking Software Market?

The U.S. Core Banking Software market is driven by factors such as the increasing adoption of cloud technology, regulatory compliance mandates, and a shift toward customer-centric banking models.

05. What trends are shaping the U.S. Core Banking Software Market?

Key trends in U.S. Core Banking Software market include the adoption of AI and machine learning in core banking platforms, the rise of open banking initiatives, and collaboration between traditional banks and fintech companies.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.