U.S. Dog Food Market Outlook to 2030

Region:North America

Author(s):Sanjeev

Product Code:KROD5135

Region:North America

Author(s):Sanjeev

Product Code:KROD5135

December 2024

95

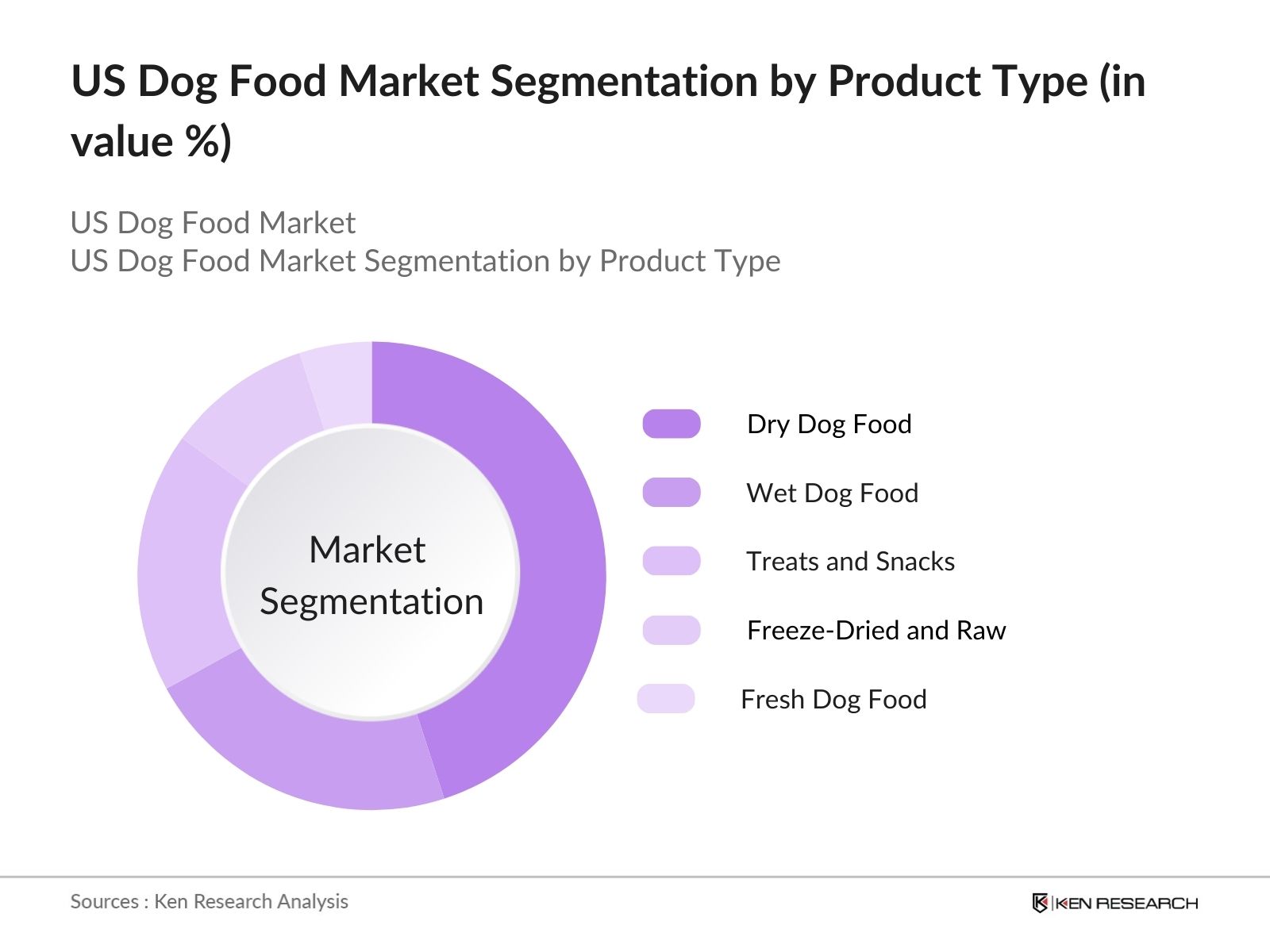

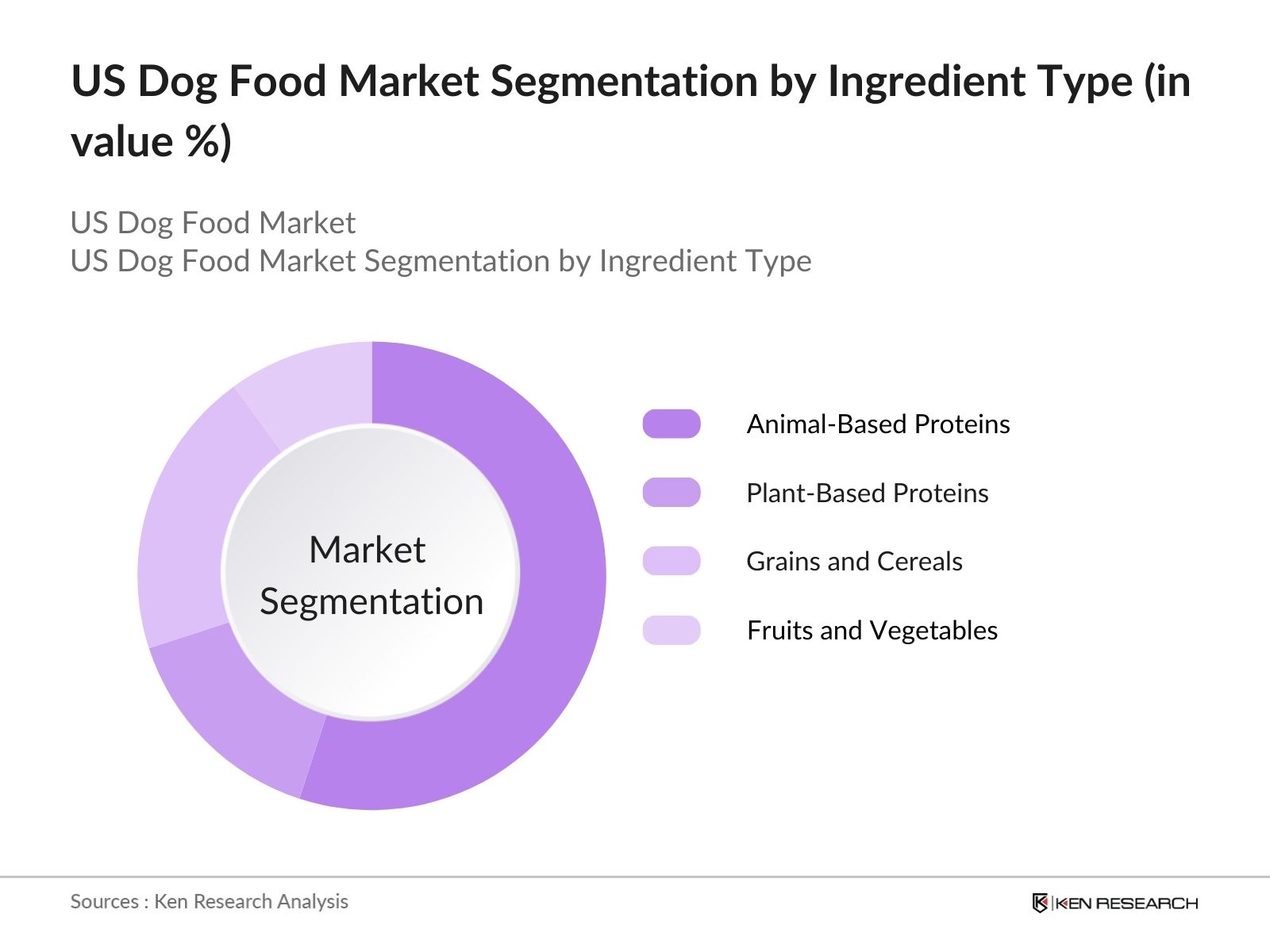

The U.S. dog food market is segmented by product type and by ingredient type.

U.S. Dog Food Market Competitive Landscape

U.S. Dog Food Market Competitive LandscapeThe U.S. dog food market is highly competitive, dominated by both global conglomerates and emerging brands. Established players like Mars Petcare and Nestl Purina control a significant share of the market, offering a diverse range of products across all price segments. These companies benefit from their broad distribution networks and strong brand loyalty. Smaller brands like Freshpet and The Honest Kitchen are making strides in niche segments such as raw, organic, and fresh food categories, appealing to consumers seeking more natural options for their pets.

|

Company Name |

Establishment Year |

Headquarters |

Market Segmentation |

Product Range |

Sustainability Initiatives |

|

Mars Petcare |

1930 |

McLean, Virginia |

|||

|

Nestl Purina PetCare |

1894 |

St. Louis, Missouri |

|||

|

Hills Pet Nutrition |

1907 |

Topeka, Kansas |

|||

Blue Buffalo |

2002 |

Wilton, Connecticut |

|||

|

The Honest Kitchen |

2002 |

San Diego, California |

Over the next five years, the U.S. dog food market is expected to experience steady growth driven by continued trends in premiumization, rising pet ownership, and increasing awareness about pet nutrition. The market will see significant innovation in terms of personalized nutrition, functional food products, and sustainable packaging options. Moreover, the shift toward e-commerce will continue to reshape the industry, making niche products more accessible to a broader consumer base.

|

Dry Dog Food Wet Dog Food Treats and Snacks Freeze-Dried and Raws Fresh Dog Food |

|

|

By Distribution Channel |

Supermarkets and Hypermarkets Pet Specialty Stores Veterinary Clinics E-Commerce |

|

By Ingredient Type |

Animal-Based Proteins Plant-Based Proteins Grains and Cereals Fruits and Vegetables |

|

By Pricing Tier |

Supermarkets and Hypermarkets Pet Specialty Stores Veterinary Clinics E-Commerce |

|

By Region |

North East West South |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Growth, Saturation, and CAGR)

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rising Pet Ownership (Pet Adoption Rate, Multi-pet Household Growth)

3.1.2. Humanization of Pets (Premiumization, Ingredient Preferences)

3.1.3. Innovation in Dog Food Formulations (Organic, Grain-Free, Allergen-Free, Raw)

3.1.4. Increased Disposable Income (Consumer Spending on Pet Care)

3.2. Market Challenges

3.2.1. Regulatory Restrictions (FDA Approvals, Labeling Compliance)

3.2.2. Fluctuating Raw Material Prices (Cost of Meat, Grain, and Plant-based Ingredients)

3.2.3. Competition from Homemade Dog Food (Consumer Shift to DIY Food)

3.3. Opportunities

3.3.1. Growth in E-Commerce (Subscription-Based Models, Direct-to-Consumer Platforms)

3.3.2. Expansion of Sustainable Packaging Solutions (Biodegradable, Recyclable Packaging)

3.3.3. Emerging Markets for Functional Dog Foods (Probiotics, Supplements, Weight Management)

3.4. Trends

3.4.1. Rise in Personalized Nutrition (Breed-Specific, Age-Specific, Health-Condition-Specific Food)

3.4.2. Growth in Freeze-Dried and Fresh Dog Food Categories

3.4.3. Increased Focus on Transparency and Traceability (Sourcing of Ingredients, Ethical Practices)

3.5. Government Regulation

3.5.1. FDA and AAFCO Guidelines

3.5.2. Nutritional Labeling Standards

3.5.3. Pet Food Safety Standards (Recalls, Contaminants Testing)

3.6. SWOT Analysis (Market Strengths, Weaknesses, Opportunities, and Threats)

3.7. Stake Ecosystem (Manufacturers, Retailers, E-Commerce Platforms, Regulatory Bodies)

3.8. Porters Five Forces (Competitive Rivalry, Threat of New Entrants, Bargaining Power of Suppliers and Buyers)

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Dry Dog Food

4.1.2. Wet Dog Food

4.1.3. Treats and Snacks

4.1.4. Freeze-Dried and Raw

4.1.5. Fresh Dog Food

4.2. By Ingredient Type (In Value %)

4.2.1. Animal-Based Proteins

4.2.2. Plant-Based Proteins

4.2.3. Grains and Cereals

4.2.4. Fruits and Vegetables

4.3. By Pricing Tier (In Value %)

4.3.1. Economy

4.3.2. Premium

4.3.3. Super Premium

4.4. By Distribution Channel (In Value %)

4.4.1. Supermarkets and Hypermarkets

4.4.2. Pet Specialty Stores

4.4.3. Veterinary Clinics

4.4.4. E-Commerce

4.5. By Region (In Value %)

4.5.1. North

4.5.2. East

4.5.3. West

4.5.4. South

5.1. Detailed Profiles of Major Companies

5.1.1. Mars Petcare

5.1.2. Nestl Purina PetCare

5.1.3. Hills Pet Nutrition

5.1.4. Blue Buffalo

5.1.5. J.M. Smucker (Big Heart Pet Brands)

5.1.6. Nutro

5.1.7. Wellness Pet Food

5.1.8. Freshpet

5.1.9. The Honest Kitchen

5.1.10. Stella & Chewy's

5.1.11. Canidae

5.1.12. Diamond Pet Foods

5.1.13. Natures Logic

5.1.14. Solid Gold Pet

5.1.15. Merrick Pet Care

5.2. Cross Comparison Parameters (Revenue, Product Offerings, Ingredient Transparency, Innovation Index, Market Share, R&D Spend, Distribution Network, Sustainability Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, Licensing Agreements, Innovations)

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. AAFCO Pet Food Labeling Requirements

6.2. FDA Pet Food Regulations

6.3. Certification Processes (Organic, Non-GMO, USDA-Certified)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Ingredient Type (In Value %)

8.3. By Pricing Tier (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Dog Size and Breed (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The research began by mapping out the U.S. dog food market's key stakeholders, which included manufacturers, distributors, e-commerce platforms, and regulatory bodies. Primary and secondary databases were utilized to collect detailed data on product offerings, market penetration, and consumer preferences, helping to define key variables that drive market dynamics.

In this step, historical data from the U.S. dog food market was compiled and analyzed to identify market trends and revenue generation patterns. This included an evaluation of market share across different product segments, distribution channels, and regions. Data from authoritative sources such as industry reports and government publications was used to ensure accuracy.

Market hypotheses were formulated based on the analysis of historical data and were validated through consultations with key industry experts. These consultations provided qualitative insights into market trends, helping to refine revenue estimates and product segment growth forecasts.

The final phase involved synthesizing all collected data into a comprehensive report. The insights from industry experts were cross-referenced with market statistics to ensure the accuracy and reliability of the final output, providing a well-rounded understanding of the U.S. dog food market.

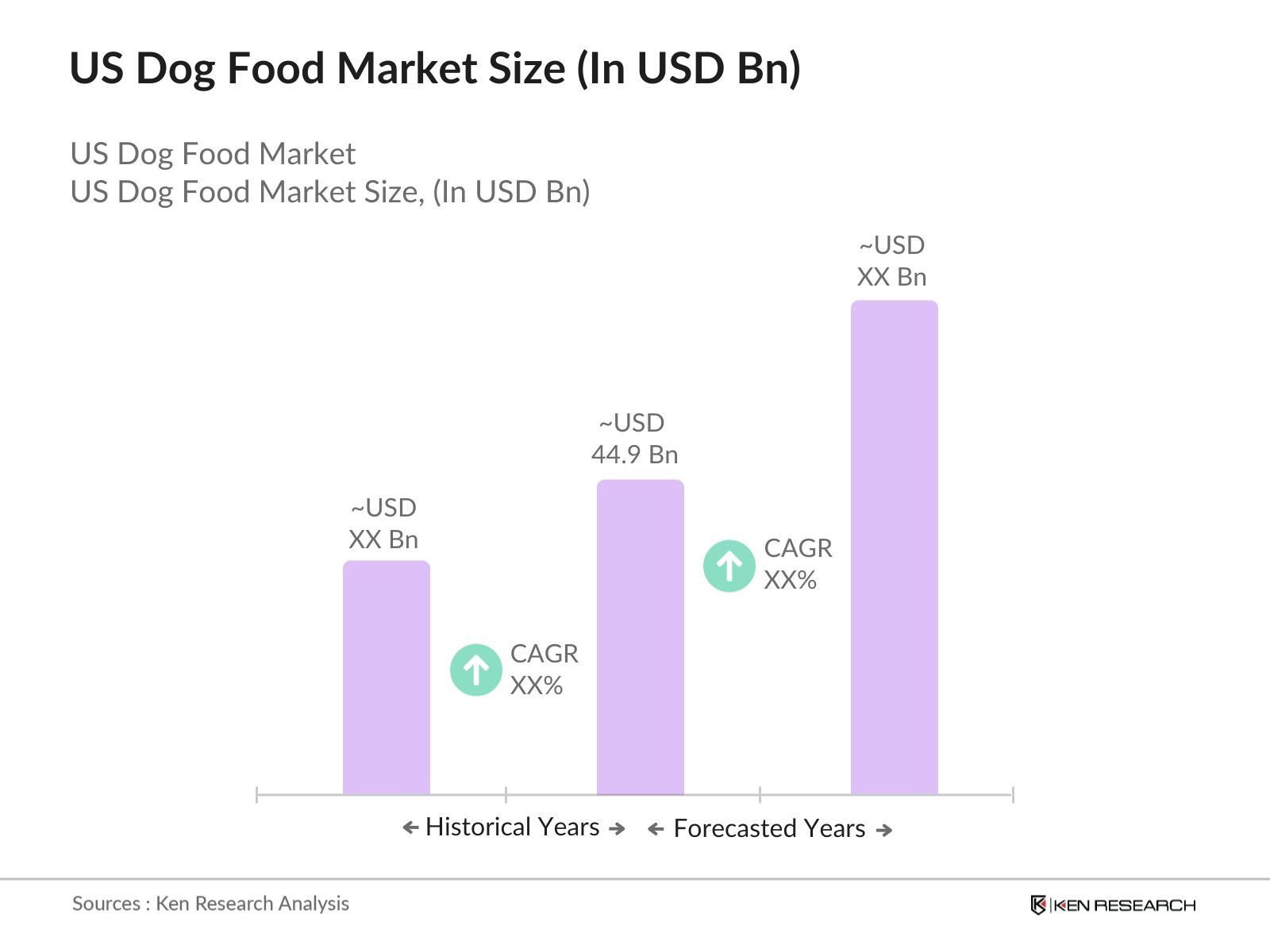

The U.S. dog food market was valued at USD 44.9 billion, driven by increasing pet ownership, the trend toward premiumization, and the rise of e-commerce as a major distribution channel.

The U.S. dog food market faces challenges such as regulatory hurdles, particularly in ingredient sourcing and labeling requirements. Fluctuating raw material prices also impact profitability, especially for premium and organic products.

Key players in the U.S. dog food market include Mars Petcare, Nestl Purina PetCare, Hills Pet Nutrition, Blue Buffalo, and J.M. Smucker, all of whom maintain dominance due to strong brand loyalty and expansive distribution networks.

The U.S. dog food market is driven by the humanization of pets, increasing consumer awareness of pet nutrition, and the growing popularity of premium, organic, and raw food products. The rise of e-commerce platforms has also significantly contributed to market expansion.

Key trends in U.S. dog food market include the shift toward personalized nutrition, functional food products, and sustainable packaging. Consumers are increasingly seeking transparency in ingredient sourcing and are gravitating toward environmentally friendly and ethically sourced dog food options.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.