U.S. Insulin Delivery Devices Market Outlook to 2030

Region:United States

Author(s):Shreya Garg

Product Code:KROD3284

Region:United States

Author(s):Shreya Garg

Product Code:KROD3284

December 2024

83

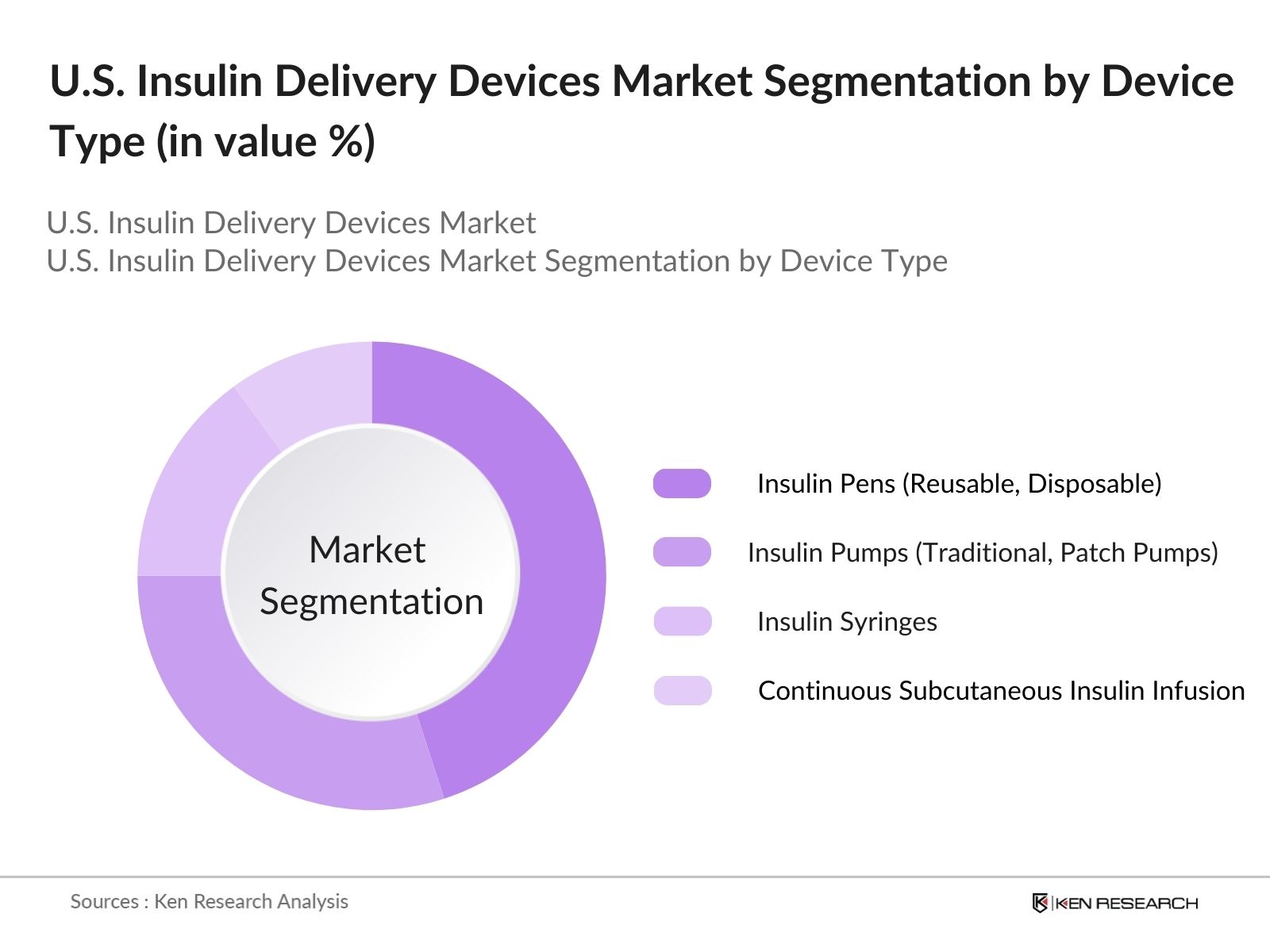

By Device Type: The U.S. insulin delivery devices market is segmented by device type into insulin pens, insulin pumps, insulin syringes, and continuous subcutaneous insulin infusion (CSII) devices. Among these, insulin pens hold the dominant market share. This is due to their user-friendly design, increasing patient preference for convenience, and wide availability across retail pharmacies. Insulin pens offer pre-measured doses, which helps reduce the chances of administering incorrect insulin amounts, making them particularly popular among elderly patients and those with visual impairments.

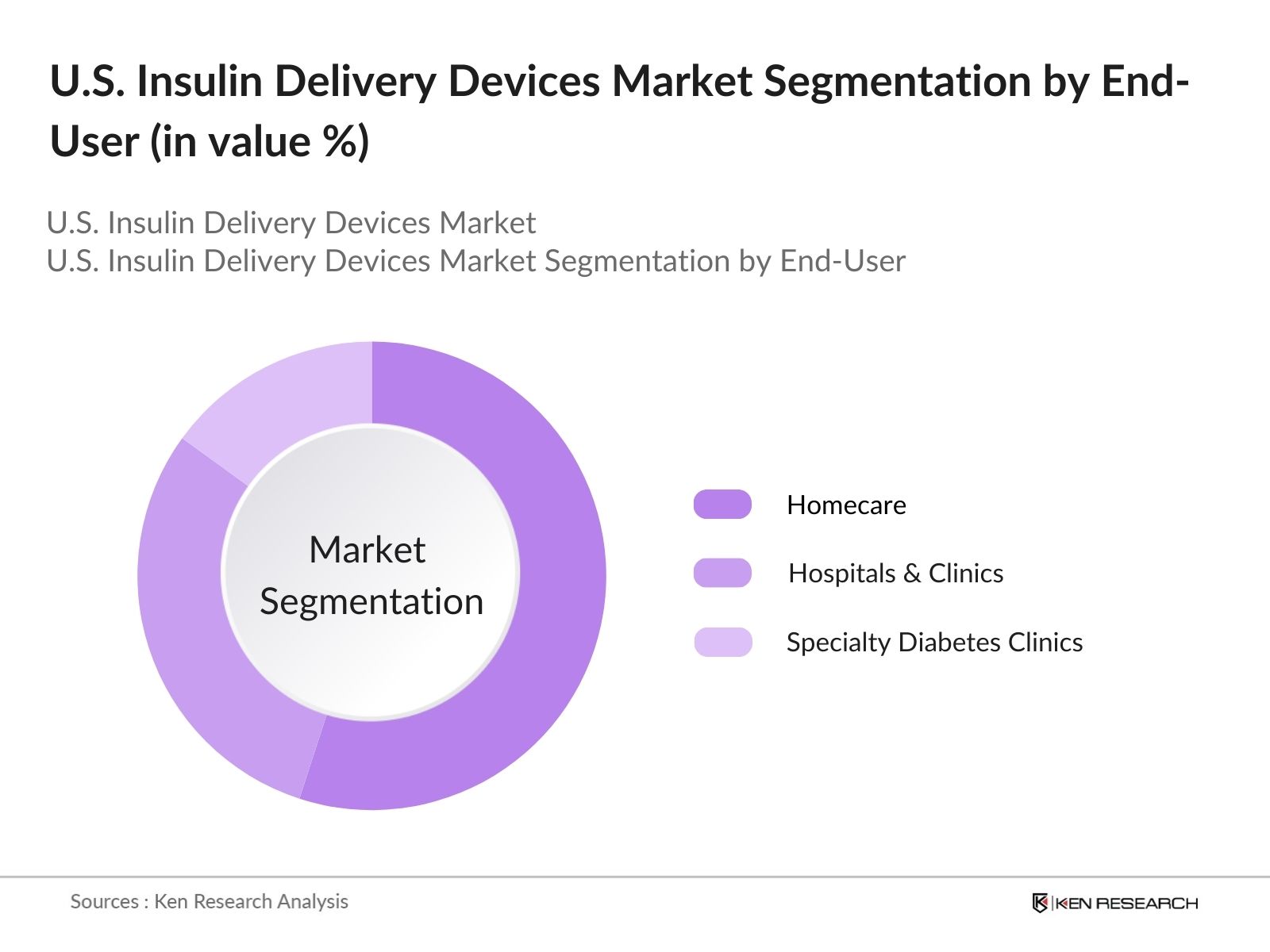

By End-User: The market is also segmented by end-user into homecare, hospitals & clinics, and specialty diabetes clinics. The homecare segment dominates the market as patients increasingly prefer self-administration of insulin using pens and pumps. The rise in telemedicine and remote monitoring services, along with increasing patient education on diabetes management, has significantly driven the demand for home-use devices.

The U.S. insulin delivery devices market is dominated by major players who lead through technological innovation, strategic partnerships, and extensive distribution networks. Companies such as Medtronic and Novo Nordisk hold significant influence in the market due to their advanced product lines and strong R&D capabilities.The U.S. insulin delivery devices market is dominated by several global and domestic manufacturers, such as Medtronic, Novo Nordisk, and Eli Lilly. These companies leverage their strong R&D focus and established distribution channels to maintain their market position.

|

Company Name |

Establishment Year |

Headquarters |

Revenue |

No. of Employees |

Key Product |

Patent Portfolio |

Recent Developments |

Strategic Partnerships |

|

Medtronic |

1949 |

Minneapolis, Minnesota |

||||||

|

Novo Nordisk |

1923 |

Bagsvrd, Denmark |

||||||

|

Eli Lilly and Company |

1876 |

Indianapolis, Indiana |

||||||

|

Insulet Corporation |

2000 |

Acton, Massachusetts |

||||||

|

Tandem Diabetes Care |

2006 |

San Diego, California |

Over the next five years, the U.S. insulin delivery devices market is expected to grow significantly, driven by technological advancements in diabetes management devices, rising healthcare spending, and the increasing prevalence of diabetes. With the rise of smart insulin delivery systems that integrate AI and IoT, the market is poised for expansion. The growth of homecare solutions and telemedicine, alongside favorable government policies and increased focus on patient education, will further bolster the market.

|

Device Type |

Insulin Pens (Reusable, Disposable) Insulin Pumps (Traditional, Patch Pumps) Insulin Syringes Continuous Subcutaneous Insulin Infusion (CSII) Devices |

|

End-User |

Homecare Hospitals & Clinics Specialty Diabetes Clinics |

|

Technology Type |

Smart Insulin Delivery Systems Traditional Devices |

|

Distribution Channel |

Hospital Pharmacies Retail Pharmacies Online Channels |

|

Region |

Northeast Midwest South West |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Prevalence of Diabetes (Diabetes Prevalence Rate, Public Health Data)

3.1.2. Increasing Geriatric Population (Age Demographics, Elderly Population Stats)

3.1.3. Rising Awareness of Diabetes Management (Public Health Campaigns, Awareness Programs)

3.1.4. Favorable Reimbursement Policies (Insurance Coverage, Government Aid Programs)

3.2. Market Challenges

3.2.1. High Cost of Devices (Average Device Pricing, Affordability Issues)

3.2.2. Limited Access in Rural Areas (Healthcare Accessibility, Infrastructure Challenges)

3.2.3. Patient Adherence Issues (Non-Compliance Rates, Usage Statistics)

3.3. Opportunities

3.3.1. Technological Innovations (Advances in Smart Insulin Pens, Continuous Glucose Monitoring Integration)

3.3.2. Expanding Home Healthcare (Growth in Home-Based Treatment, Market Demand for Self-Administered Devices)

3.3.3. New Entrants in Digital Health Space (Emerging Digital Platforms, AI-Driven Insulin Devices)

3.4. Trends

3.4.1. Integration of Wearable Technology (Adoption Rate of Smart Devices, IoT-Connected Insulin Pumps)

3.4.2. Shift Toward Prefilled Insulin Pens (Market Share of Disposable Devices)

3.4.3. Increasing Usage of Automated Insulin Delivery (Growth of Closed-Loop Systems)

3.5. Government Regulation

3.5.1. U.S. FDA Approval Pathways (Pre-Market Approval Processes, Regulatory Timelines)

3.5.2. Medicare Coverage and Policies (Medicare Reimbursement, Coverage for Insulin Pumps and CGMs)

3.5.3. Affordable Care Act Impact on Insulin Delivery (Healthcare Reform Influence, Impact on Insurance Coverage)

3.5.4. Public-Private Partnerships (Collaborations Between Healthcare Providers, Device Manufacturers, and Government)

3.6. SWOT Analysis

3.7. Stake Ecosystem (Healthcare Providers, Distributors, Manufacturers, Insurers)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Device Type (In Value %)

4.1.1. Insulin Pens (Reusable, Disposable)

4.1.2. Insulin Pumps (Traditional, Patch Pumps)

4.1.3. Insulin Syringes

4.1.4. Continuous Subcutaneous Insulin Infusion (CSII) Devices

4.2. By Distribution Channel (In Value %)

4.2.1. Hospital Pharmacies

4.2.2. Retail Pharmacies

4.2.3. Online Channels

4.3. By End-User (In Value %)

4.3.1. Homecare

4.3.2. Hospitals & Clinics

4.3.3. Specialty Diabetes Clinics

4.4. By Technology Type (In Value %)

4.4.1. Smart Insulin Delivery Systems

4.4.2. Traditional Devices

4.5. By Region (In Value %)

4.5.1. Northeast

4.5.2. Midwest

4.5.3. South

4.5.4. West

5.1. Detailed Profiles of Major Companies

5.1.1. Medtronic

5.1.2. Novo Nordisk

5.1.3. Eli Lilly and Company

5.1.4. Sanofi

5.1.5. Tandem Diabetes Care

5.1.6. Insulet Corporation

5.1.7. Becton, Dickinson and Company

5.1.8. Ypsomed Holding AG

5.1.9. Roche Diabetes Care

5.1.10. Abbott Laboratories

5.1.11. Dexcom, Inc.

5.1.12. Bigfoot Biomedical

5.1.13. Companion Medical

5.1.14. Senseonics

5.1.15. Biocon

5.2. Cross Comparison Parameters (Revenue, Headquarters, No. of Employees, Product Portfolio, Market Share, Key Patents, Strategic Partnerships, Research and Development Focus)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants and Subsidies

6.1. U.S. FDA Device Classifications and Approvals

6.2. Regulatory Compliance Standards

6.3. Insurance Reimbursement Policies

6.4. Certification Processes

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Device Type (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By End-User (In Value %)

8.4. By Technology Type (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Cohort Analysis

9.3. Pricing Strategy Recommendations

9.4. White Space Opportunity Analysis

The initial phase involves identifying key variables that impact the U.S. insulin delivery devices market. Extensive desk research, incorporating secondary sources such as company filings, government data, and healthcare reports, helps construct an ecosystem map of major stakeholders.

In this phase, we analyze historical data on device adoption rates, reimbursement policies, and market growth drivers. This step includes compiling data from proprietary databases and validated reports to provide insights into market penetration and revenue generation.

Our market hypotheses are validated through expert consultations, including interviews with industry insiders, healthcare professionals, and device manufacturers. These insights help refine data accuracy and validate market estimates.

The final phase involves synthesizing the data collected into actionable insights. Engagements with insulin device manufacturers further validate the findings, ensuring a robust and accurate market analysis.

The U.S. insulin delivery devices market was valued at USD 4 billion in 2023, driven by increasing diabetes prevalence and demand for advanced insulin delivery systems.

Challenges in the U.S. insulin delivery devices market include the high cost of advanced devices, limited access to diabetes care in rural areas, and patient adherence issues.

Key players in the U.S. insulin delivery devices market include Medtronic, Novo Nordisk, Eli Lilly and Company, Tandem Diabetes Care, and Insulet Corporation. These companies dominate due to their strong R&D focus and established distribution networks.

The U.S. insulin delivery devices market is driven by the rising prevalence of diabetes, increasing awareness of diabetes management, technological advancements in insulin delivery systems, and favorable reimbursement policies.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.