US Video Surveillance Market Outlook 2030

Region:North America

Author(s):Shivani Mehra

Product Code:KROD11480

December 2024

81

About the Report

US Video Surveillance Market Overview

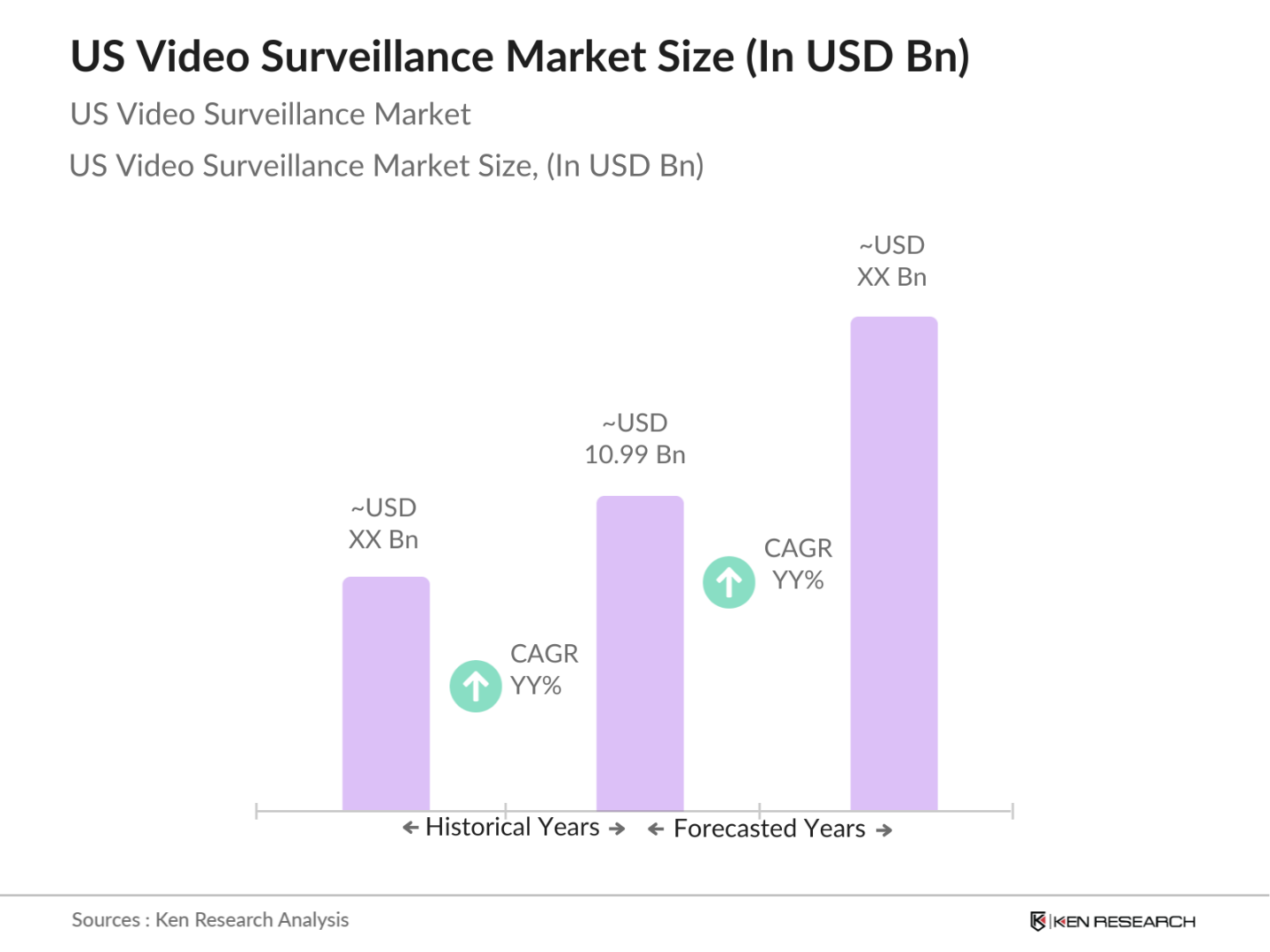

- The US Video Surveillance market is valued at USD 10.99 billion, with growth primarily driven by increasing security concerns in both public and private sectors. The integration of advanced technologies, such as AI-powered analytics, edge computing, and cloud storage, has propelled the adoption of video surveillance systems across various sectors. Additionally, government initiatives promoting safety and security further contribute to this growth, reinforcing the markets upward trajectory.

- Urban centers like New York, Los Angeles, and Chicago lead in the adoption of video surveillance due to high urbanization rates, elevated crime statistics, and strong government investment in public safety infrastructure. The substantial need for monitoring and secure surveillance in these densely populated regions supports the dominance of these areas in the US Video Surveillance market.

- In 2023, the Department of Homeland Security allocated $1.5 billion for upgrading and expanding video surveillance technology across critical infrastructure facilities, including airports, seaports, and government buildings. This funding aims to enhance real-time monitoring capabilities and support threat prevention measures, underscoring the government's commitment to bolstering national security through advanced surveillance. The allocation highlights an ongoing strategy to protect vital assets against potential threats by investing in next-generation video surveillance solutions.

US Video Surveillance Market Segmentation

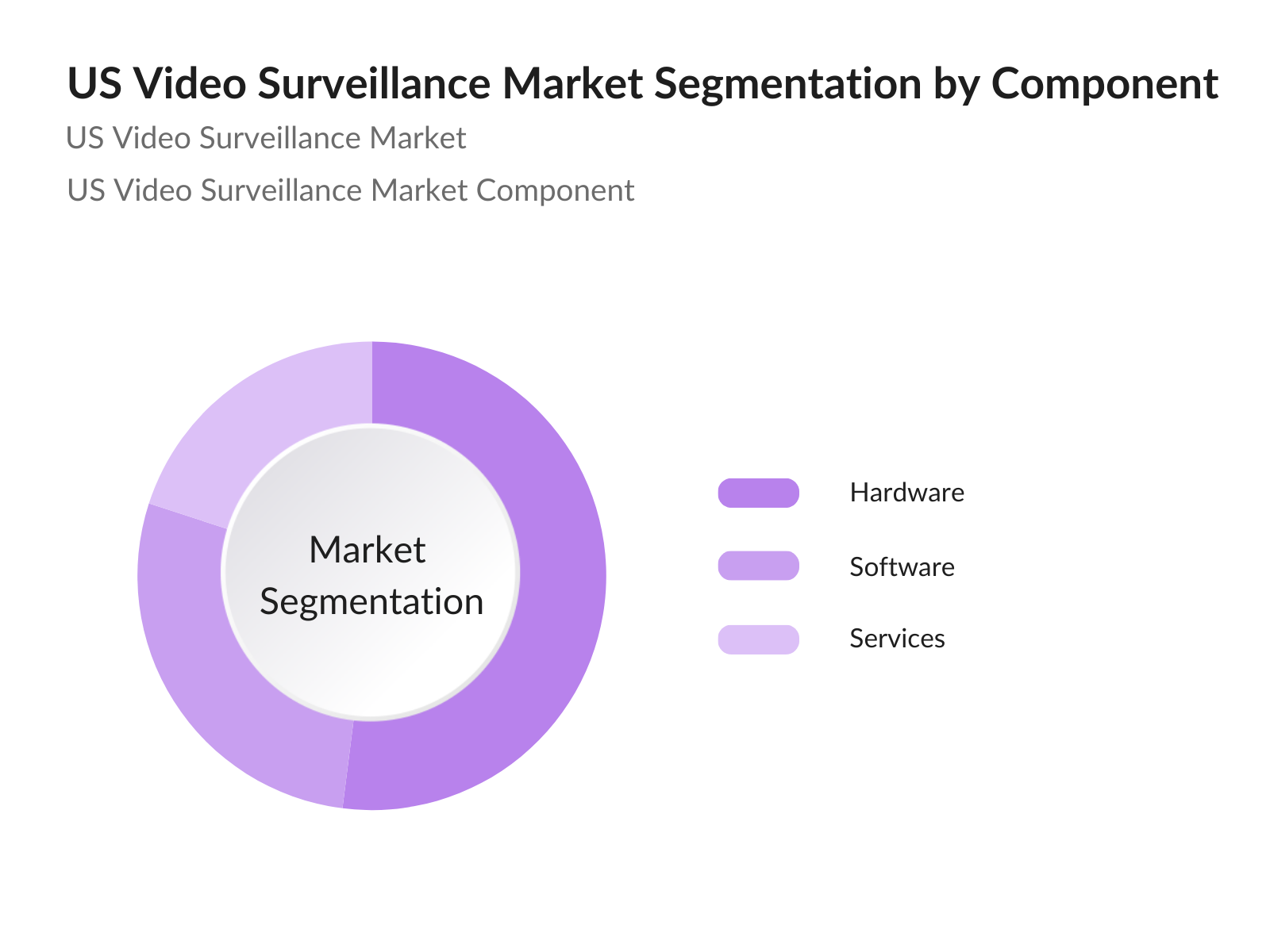

- By Component: The US Video Surveillance market is segmented by component into hardware, software, and services. Hardware, including cameras, storage devices, and monitors, currently holds the largest share due to high demand for advanced, high-resolution cameras and robust storage solutions. The extensive presence of well-established manufacturers in the hardware segment ensures sustained innovation and competitive pricing, further strengthening this segment's dominance.

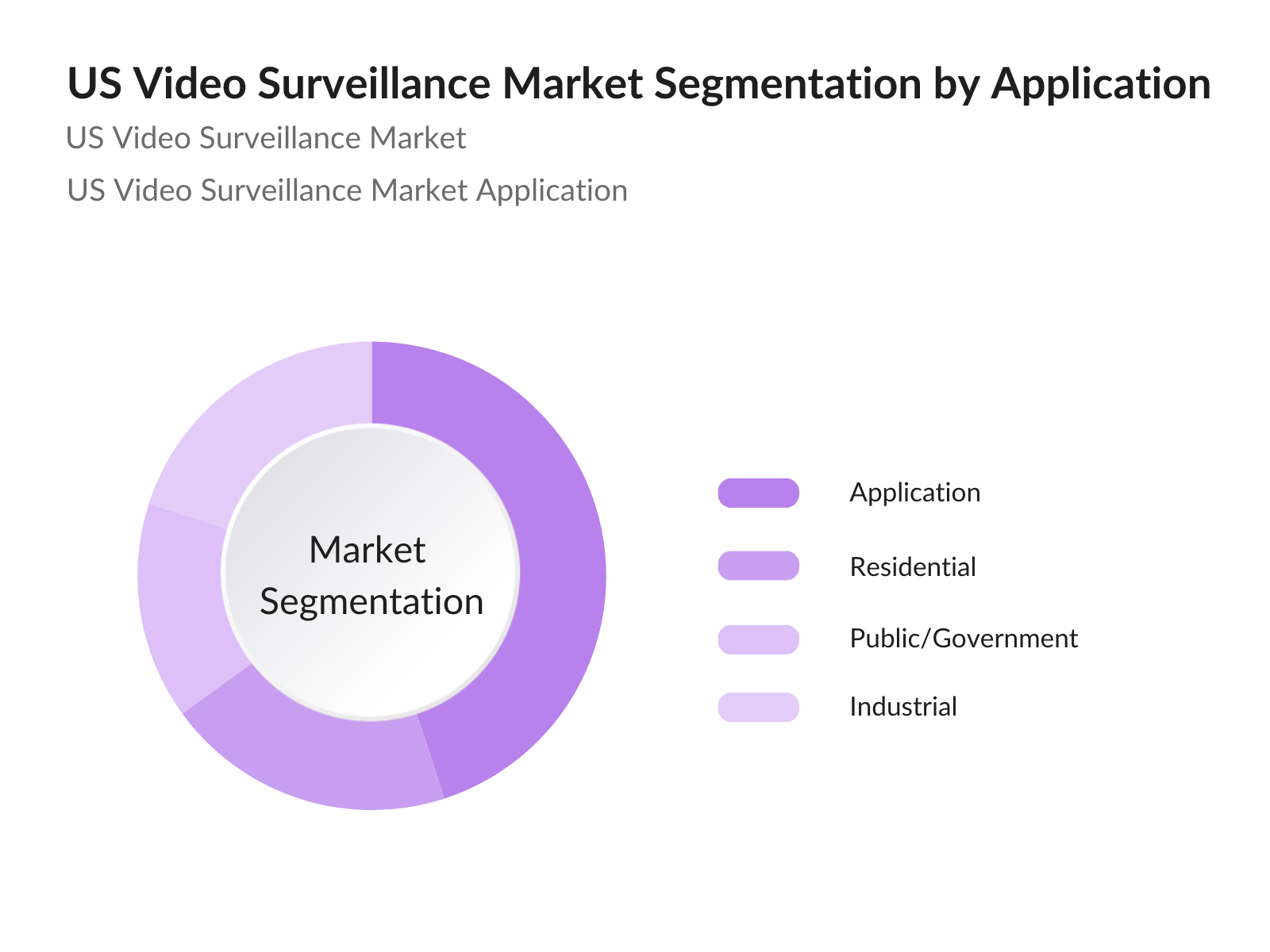

- By Application: The market is further divided by application into commercial, residential, industrial, and public/government sectors. Commercial applications hold the leading share in this market, driven by demand for video surveillance in retail, banking, and office settings to prevent theft, monitor operations, and ensure employee safety. The expansion of commercial real estate, coupled with regulatory standards requiring surveillance in public spaces, supports the prevalence of this segment.

US Video Surveillance Market Competitive Landscape

The US Video Surveillance market is dominated by a select group of companies that leverage extensive technological capabilities and market presence. Key players include:

US Video Surveillance Market Analysis

Market Growth Drivers

- Rising Demand for Public Safety: In 2023, the United States reported approximately 1.2 million violent crimes, underscoring the critical need for enhanced public safety measures. Urban areas, in particular, have experienced increased incidents, prompting municipalities to invest in advanced video surveillance systems to monitor and deter criminal activities. For instance, New York City allocated $90 million in 2023 to upgrade its surveillance infrastructure, aiming to cover high-crime neighborhoods more effectively. This trend reflects a nationwide emphasis on leveraging technology to bolster public safety and reduce crime rates.

- Technological Advancements (AI-based Analytics, Cloud Storage, and Edge Computing): The integration of artificial intelligence (AI) in video surveillance has revolutionized security operations. In 2023, numerous new surveillance systems incorporated AI-based analytics, enabling real-time threat detection and response. Cloud storage solutions have also gained significant traction, as many organizations adopted cloud-based surveillance to facilitate remote access and scalable data management. Edge computing further enhances system efficiency by processing data locally, reducing latency, and minimizing bandwidth usage. These technological advancements collectively improve the effectiveness and reliability of video surveillance systems, making them essential in modern security infrastructure.

- Government Initiatives and Regulations: The U.S. government has implemented several initiatives to strengthen national security through enhanced surveillance. In 2023, the Department of Homeland Security allocated $1.5 billion for the deployment of advanced surveillance systems across critical infrastructure. Additionally, the Federal Aviation Administration (FAA) introduced regulations in 2022 mandating the use of surveillance technologies in unmanned aerial systems to ensure airspace safety. These measures underscore the government's commitment to leveraging surveillance technology for public safety and regulatory compliance.

Market Challenges:

- High Installation Costs: The deployment of advanced surveillance systems entails significant financial investment. For example, installing a comprehensive city-wide surveillance network can cost upwards of $200 million, encompassing hardware, software, and maintenance expenses. These substantial costs pose challenges for municipalities and organizations with limited budgets, potentially hindering widespread adoption of state-of-the-art surveillance technologies.

- Data Privacy Concerns: The proliferation of surveillance systems has raised significant data privacy issues. In 2023, the American Civil Liberties Union (ACLU) reported over 500 cases of unauthorized data access and misuse related to surveillance footage. These incidents have led to increased public scrutiny and calls for stringent regulations to protect individual privacy rights, potentially impacting the deployment and operation of surveillance systems.

US Video Surveillance Market Future Outlook

The US Video Surveillance market is projected to experience steady growth, propelled by advancements in artificial intelligence, machine learning, and cloud-based solutions. The rising focus on safety in smart city projects, along with a growing need for enhanced monitoring systems in both private and public sectors, will likely drive demand. Innovations in facial recognition, real-time analytics, and scalable video storage solutions will further influence the growth trajectory, enhancing the value proposition of video surveillance solutions across various end-use industries.

Market Opportunities:

- Integration with Smart City Projects: The U.S. is investing heavily in smart city initiatives, with over 100 cities implementing projects that integrate surveillance systems with IoT devices to enhance urban management. For instance, Chicago's "Array of Things" project utilizes interconnected sensors and cameras to monitor environmental conditions and public safety, providing real-time data to city officials. This integration offers significant opportunities for the expansion and enhancement of surveillance technologies within urban infrastructures.

- Rising Adoption in Residential and Commercial Sectors: The residential sector has seen a significant increase in surveillance system installations, with over 20 million households in the U.S. equipped with security cameras as of 2023. Similarly, the commercial sector has embraced surveillance technologies to protect assets and ensure employee safety. Retail establishments, in particular, have invested in advanced systems to monitor customer behavior and prevent theft, reflecting a broadening market base for surveillance solutions.

Scope of the Report

|

By Component |

Hardware (Cameras, Storage Devices, Monitors) Software (Video Analytics, Video Management Software) Services (Installation, Maintenance, VSaaS) |

|

By Application |

Commercial Residential Industrial Public/Government |

|

By Technology |

Analog Surveillance IP-Based Surveillance Hybrid Surveillance |

|

By Deployment |

On-Premise Cloud-Based |

|

By Region |

North-East Midwest West Coast Southern States |

Products

Key Target Audience

Commercial Real Estate Companies

Retail Chains and Malls

Banking and Financial Institutions

Transportation and Logistics Companies

Educational Institutions

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (Department of Homeland Security, Federal Trade Commission)

Technology Integrators and Solution Providers

Companies

Players mentioned in the report

Axis Communications

Hikvision Digital Technology

Honeywell Security

Avigilon (Motorola Solutions)

FLIR Systems

Dahua Technology

Pelco

Bosch Security Systems

Hanwha Techwin America

Genetec Inc.

Cisco Systems

Johnson Controls

Panasonic System Solutions

Eagle Eye Networks

Vicon Industries

Table of Contents

1. US Video Surveillance Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. US Video Surveillance Market Size (in USD Billion)

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. US Video Surveillance Market Analysis

3.1 Growth Drivers

3.1.1 Rising Demand for Public Safety

3.1.2 Technological Advancements (AI-based Analytics, Cloud Storage, and Edge Computing)

3.1.3 Government Initiatives and Regulations

3.1.4 Increasing Threats and Security Concerns

3.2 Market Challenges

3.2.1 High Installation Costs

3.2.2 Data Privacy Concerns

3.2.3 Technical Limitations

3.3 Opportunities

3.3.1 Integration with Smart City Projects

3.3.2 Expansion of Video Surveillance as a Service (VSaaS)

3.3.3 Rising Adoption in Residential and Commercial Sectors

3.4 Trends

3.4.1 Cloud-Based Solutions

3.4.2 AI and Machine Learning for Video Analytics

3.4.3 Use of Drones and Wearable Surveillance Devices

3.5 Government Regulations

3.5.1 Federal Video Surveillance Standards

3.5.2 Data Protection and Privacy Laws

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competitive Landscape

4. US Video Surveillance Market Segmentation

4.1 By Component (In Value %)

4.1.1 Hardware (Cameras, Storage Devices, Monitors)

4.1.2 Software (Video Analytics, Video Management Software)

4.1.3 Services (Installation, Maintenance, VSaaS)

4.2 By Application (In Value %)

4.2.1 Commercial

4.2.2 Residential

4.2.3 Industrial

4.2.4 Public/Government

4.3 By Technology (In Value %)

4.3.1 Analog Surveillance

4.3.2 IP-Based Surveillance

4.3.3 Hybrid Surveillance

4.4 By Deployment (In Value %)

4.4.1 On-Premise

4.4.2 Cloud-Based

4.5 By Region (In Value %)

4.5.1 Northeast

4.5.2 Midwest

4.5.3 South

4.5.4 West

5. US Video Surveillance Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Axis Communications

5.1.2 Hikvision Digital Technology

5.1.3 Dahua Technology

5.1.4 Honeywell Security

5.1.5 Avigilon (Motorola Solutions)

5.1.6 Pelco

5.1.7 Bosch Security Systems

5.1.8 Hanwha Techwin America

5.1.9 FLIR Systems

5.1.10 Genetec Inc.

5.1.11 Cisco Systems

5.1.12 Johnson Controls (Tyco Security Products)

5.1.13 Panasonic System Solutions

5.1.14 Eagle Eye Networks

5.1.15 Vicon Industries

5.2 Cross-Comparison Parameters (Market Share, Revenue, Headquarters, Product Portfolio, Innovation Capability, Clientele, Regional Presence, Partnership Strategy)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. US Video Surveillance Market Regulatory Framework

6.1 Federal Surveillance Compliance Requirements

6.2 Data Protection and Privacy Legislation (CCTV and Surveillance Data)

6.3 Industry Certifications and Standards

7. US Video Surveillance Future Market Size (in USD Billion)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. US Video Surveillance Future Market Segmentation

8.1 By Component (In Value %)

8.2 By Application (In Value %)

8.3 By Technology (In Value %)

8.4 By Deployment (In Value %)

8.5 By Region (In Value %)

9. US Video Surveillance Market Analysts' Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 White Space Opportunity Analysis

9.4 Marketing Initiatives

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

In the initial phase, we mapped the ecosystem of the US Video Surveillance market, identifying all critical stakeholders. Through secondary research and proprietary databases, we gathered detailed information to establish key market variables and gain insights into industry dynamics.

Step 2: Market Analysis and Construction

This phase included an in-depth analysis of historical data to evaluate market penetration rates, vendor availability, and revenue generation. Service quality and user experience were assessed to ensure data reliability and accuracy in revenue estimation.

Step 3: Hypothesis Validation and Expert Consultation

Our hypotheses were validated through interviews with industry experts, employing computer-assisted telephone interviews (CATIs). These consultations provided valuable insights directly from practitioners, enhancing the accuracy of our data.

Step 4: Research Synthesis and Final Output

In the final phase, we engaged directly with manufacturers and service providers in the video surveillance industry to gather detailed information on market segments, sales performance, and consumer preferences. This comprehensive interaction helped validate our data and ensure the integrity of our analysis.

Frequently Asked Questions

01. How big is the US Video Surveillance Market?

The US Video Surveillance Market is valued at USD 10.99 billion, driven by increased security concerns and the adoption of AI-based video analytics across various sectors.

02. What are the challenges in the US Video Surveillance Market?

Key challenges include high installation and maintenance costs, data privacy concerns, and technical limitations in video analytics technology.

03. Who are the major players in the US Video Surveillance Market?

Leading companies in the market include Axis Communications, Hikvision, Honeywell Security, Avigilon, and FLIR Systems, each known for their strong market presence and innovative product offerings.

04. What are the growth drivers of the US Video Surveillance Market?

The market growth is fueled by increasing security demands, advancements in AI and video analytics, and supportive government regulations aimed at public safety.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.