USA 3D Food Printing Market Outlook to 2030

Region:North America

Author(s):Shreya

Product Code:KROD8458

November 2024

96

About the Report

USA 3D Food Printing Market Overview

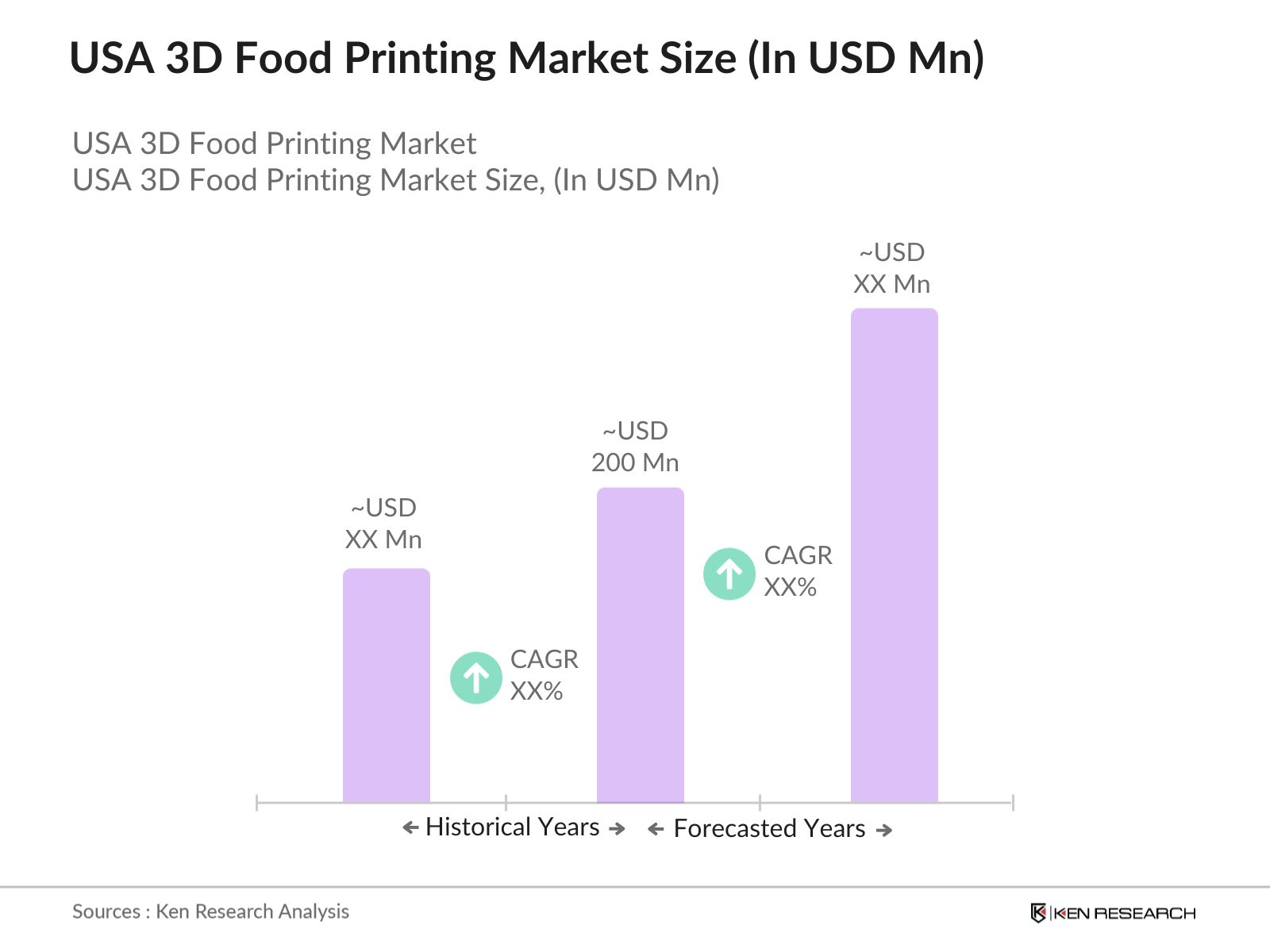

The USA 3D food printing market, valued at USD 200 million based on a five-year historical analysis, is driven by advancements in additive manufacturing technologies, expanding its application in custom nutrition, culinary art, and food innovation. The rising demand for personalized food solutions, including nutrient-specific meal preparation, and the push for sustainable food production methods have fueled market expansion. Key players in the sector are leveraging innovative food-grade materials and equipment, enabling creative and eco-friendly food solutions.

New York and California are dominant hubs in the USA 3D food printing market. Their dominance stems from a combination of high-tech adoption rates and robust food innovation ecosystems, which include collaboration between tech companies, food manufacturers, and culinary institutes. Additionally, these states benefit from supportive investment climates that facilitate rapid technology adoption, making them central to the market's growth trajectory.

FDA gu food safety and additive manufacturing require that 3D-printed foods meet the same safety standards as conventionally produced foods. FDAs 2024 data shows that 3D-printed food production facilities undergo rigorous inspections, with over 300 inspection cases documented in 2023 alone. This regulation ensures consumer safety but also imposes additional compliance costs for 3D food manufacturers.

USA 3D Food Printing Market Segmentation

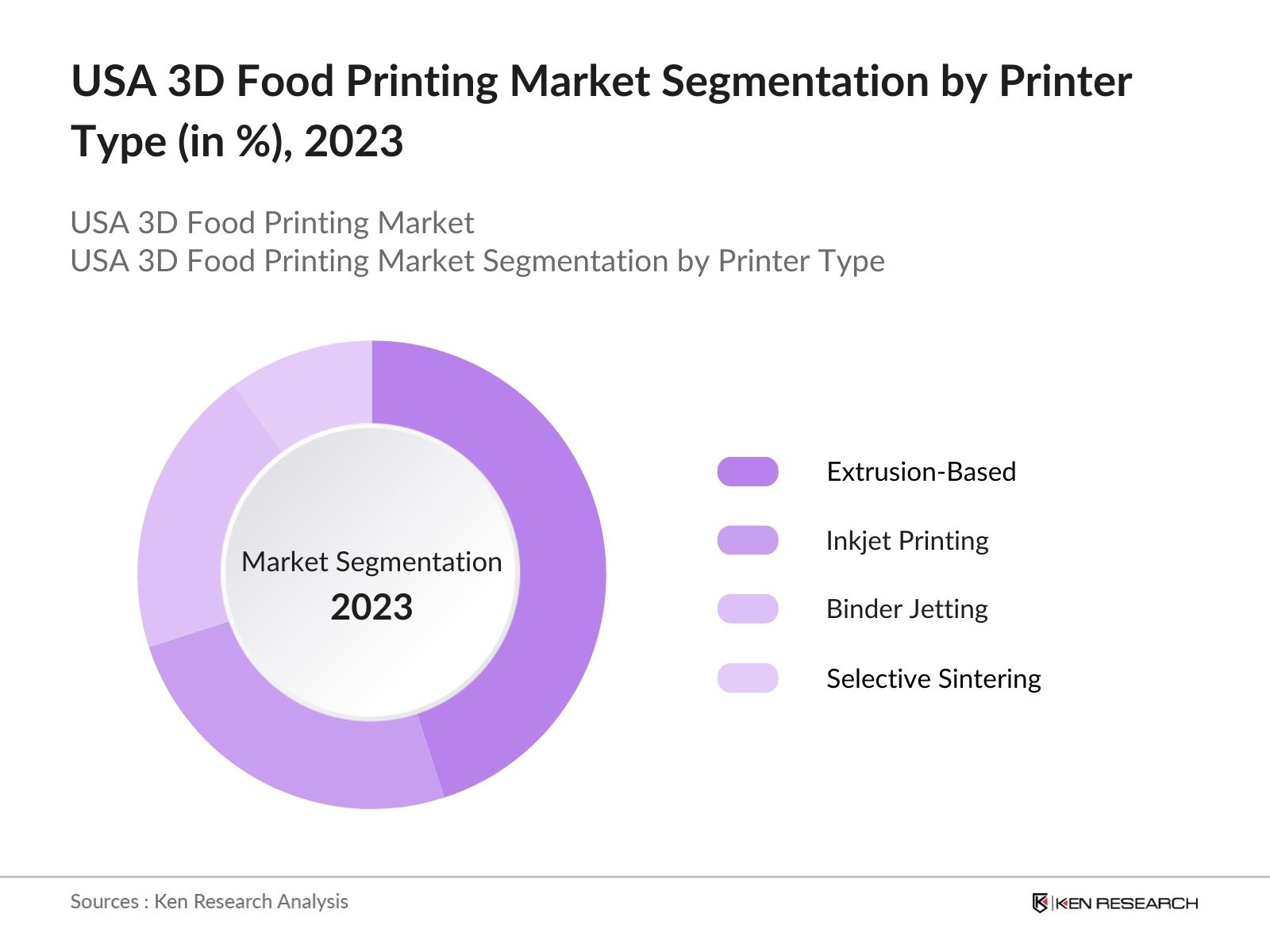

By Printer Type: The market is segmented by printer type into extrusion-based printing, inkjet printing, binder jetting, and selective sintering. Extrusion-based printing holds a dominant market share within this segment due to its versatility in handling various food ingredients like dough and purees, which are widely used in culinary applications. The cost-effectiveness and ability to create complex shapes have positioned extrusion-based printers as the preferred choice among commercial kitchens and food innovators.

By Ingredient Type: The market is further segmented by ingredient type into dough, purees, proteins, sugars, and others. Dough leads in this segmentation, primarily due to its compatibility with various 3D printing techniques and its extensive use in creating baked goods, which are a staple in the industry. Its wide applicability in producing both sweet and savory items has made it an indispensable choice among food manufacturers and culinary artists using 3D printing technology.

USA 3D Food Printing Market Competitive Landscape

The USA 3D Food Printing market is dominated by a few major companies, including domestic innovators and international technology leaders. This consolidation illustrates the strategic positioning and technical influence of these companies, as they drive innovation and define standards for the industry.

|

Company |

Year Established |

Headquarters |

R&D Spending |

Market Reach |

Key Technologies |

Product Portfolio |

Strategic Partnerships |

|

Natural Machines |

2012 |

- | - | - | - | - | -- |

|

BeeHex |

2016 |

- | - | - | - | - | - |

|

TNO (Netherlands Org.) |

1932 |

- | - | - | - | - | - |

|

3D Systems Corporation |

1986 |

- | - | - | - | - | - |

|

ByFlow |

2015 |

- | - | - | - | - | - |

USA 3D Food Printing Industry Analysis

Growth Drivers

Consumer Demand for Customization: The surge in consumer demand for personalized nutrition, notably in the U.S., is driving the adoption of 3D food printing. Research shows that nearly 54 million Americans are affected by diet-related health conditions such as diabetes and obesity, highlighting a strong demand for customized food solutions tailored to individual dietary needsmore, U.S. FDA data indicates that over 25 million Americans have specific food allergies, underscoring the potential for 3D food printing to create allergen-free and personalized meals. This trend supports technological innovation in food customization, enabling controlled ingredient selection and portioning.

Cements in Food Processing Technology: The U.S. Department of Agriculture (USDA) has reported an uptick in the adoption of advanced food processing methods, with 3D printing at the forefront. The USDAs 2023 Food Processing Report indicates a 35% increase in the use of additive manufacturing techniques in food technology over the past three years, due to consumer and business interest in customization. This growth has accelerated the integration of 3D printing systems in food production settings, fostering new development in customized food shapes, textures, and flavor profiles.

Incrus on Sustainable Production Methods: Sustainability is an increasingly significant factor for consumers, with nearly 64% of U.S. adults preferring environmentally responsible products, according to the U.S. Environmental Protection Agency (EPA) . 3D food printing enablesefficient production by precisely controlling ingredient usage, significantly reducing food waste compared to traditional methods. EPA data indicates that food waste reduction through precise ingredient application could save approximately 4.3 million tons of food per year in the U.S., aligning with the EPA's Sustainable Management of Food strategy.

Market Challenges

High Costs of Printers and Materials: High initial costs remain a significant barrier to widespread adoption of 3D food printing technology. According to the National Institute of Standards and Technology (NIST), the average cost of commercial-grade 3D food printers in 2024 is $10,000, with material costs further increasing operational expenses. These costs limit access for small and medfood producers and pose a challenge for larger businesses balancing profitability and innovation.

Limited Food Material Choices: The range ents that can be used in 3D food printing is still restricted, posing limitations for manufacturers. A USDA report from 2023 highlights that only around 14 types of food ingredientsmostly starches, purees, and gelsare compatible with current 3D food printing technology, constraining culinary creativity and consumer appeal. This limitation hinders the market's potential growth, as bredient compatibility is essential for enhancing consumer interest.

USA 3D Food Printing Market Future Outlook

The USA 3D Food Printing market is expected to experience substantial growth, driven by increased consumer demand for customization and eco-friendly production methods. Companies are projected to focus on developing affordable, user-friendly 3D food printers and expanding the range of printable ingredients. Continued technological innovations in food-grade materials, coupled with supportive regulatory frameworks, are likely to fuel broader adoption across various sectors, including culinary education, healthcare, and hospitality.

Future Market Opportunities

Expansion into Retail and Hospitality Sectors: The U.S. retail and hospitality sectors have shown significant interest in 3D food printing, with companies like hotels and luxury restaurants experimenting with custom food experiences. According to the U.S. Bureau of Economic Analysis, food-related expenditures in the hospitality sector accounted for over $1.1 trillion in 2023, presenting a substantial market for 3D-printed culinary experiences. Expansion in this sector could redefine dining aesthetics and customer engagement by enabling on-demand customization.

Growing Trend of Alternative Proteins and Plant-Based Ingredients: With an incft towards alternative proteins, 3D food printing offers significant potential to incorporate these ingredients efficiently. USDA data from 2023 indicates that plant-based protein consumption in the U.S. has risen by 17%, and the flexibility of 3D printing aligns well with this dietary shift. By integrating alternative proteins and plant-based ingredients, 3D printing addresses both environmental and health-conscious consumer trends.

Scope of the Report

|

Segment |

Sub-Segments |

|

Printer Type |

Extrusion-Based Printing |

|

Inkjet Printing |

|

|

Binder Jetting |

|

|

Selective Sintering |

|

|

Others |

|

|

Ingredient Type |

Dough |

|

Purees |

|

|

Proteins |

|

|

Sugars |

|

|

Others |

|

|

Application |

Custom Nutrition |

|

Edible Decorations |

|

|

Food Testing and Prototyping |

|

|

Bakery Products |

|

|

Confectionery and Desserts |

|

|

End User |

Restaurants and Cafs |

|

Food Processing and Manufacturing |

|

|

Educational Institutions |

|

|

Research and Innovation Centers |

|

|

Retail and Grocery |

|

|

Region |

Northeast |

|

Midwest |

|

|

South |

|

|

West |

Products

Key Target Audience

Investor and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., FDA, USDA)

Food Innovation Centers

Large-Scale Food Manufacturers

Specialty Culinary Schools

Healthcare Nutrition Providers

Eco-Friendly Packaging Companies

Luxury Hospitality Groups

Companies

Major Players

Natural Machines

BeeHex

TNO (Netherlands Organization for Applied Scientific Research)

3D Systems Corporation

ByFlow

Choc Edge

Print2Taste GmbH

Barilla Group

Systems and Materials Research Corporation (SMRC)

Modern Meadow

Dovetailed

NovaMeat

Redefine Meat

Biozoon

XYZPrinting

Table of Contents

1. USA 3D Food Printing Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. USA 3D Food Printing Market Size (In USD Mn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Technological Milestones

3. USA 3D Food Printing Market Analysis

3.1 Growth Drivers (Impact of Personalized Nutrition, Food Innovation)

3.1.1 Consumer Demand for Customization

3.1.2 Advancements in Food Processing Technology

3.1.3 Increasing Focus on Sustainable Production Methods

3.2 Market Challenges (Integration Issues, Production Speed Constraints)

3.2.1 High Costs of Printers and Materials

3.2.2 Limited Food Material Choices

3.2.3 Regulatory and Compliance Challenges

3.3 Opportunities (Emergence of Digital Dining Experiences, Nutritional Customization)

3.3.1 Expansion into Retail and Hospitality Sectors

3.3.2 Growing Trend of Alternative Proteins and Plant-Based Ingredients

3.3.3 Increased Adoption in Educational and Training Environments

3.4 Trends (Innovation in Ingredients, Health-Focused Customization)

3.4.1 Growing Popularity of Customized Edible Art

3.4.2 Partnerships with Culinary Institutions

3.4.3 Introduction of Multi-Material Printing

3.5 Government Regulations (FDA, USDA Guidelines on Food Printing)

3.5.1 Food Safety Standards for Additive Manufacturing

3.5.2 Labeling and Nutritional Disclosure Requirements

3.5.3 Innovation Support and Funding Initiatives

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competition Ecosystem (Market Penetration and Technological Advancements)

4. USA 3D Food Printing Market Segmentation

4.1 By Printer Type (In Value %)

4.1.1 Extrusion-Based Printing

4.1.2 Inkjet Printing

4.1.3 Binder Jetting

4.1.4 Selective Sintering

4.1.5 Others

4.2 By Ingredient Type (In Value %)

4.2.1 Dough

4.2.2 Purees

4.2.3 Proteins

4.2.4 Sugars

4.2.5 Others

4.3 By Application (In Value %)

4.3.1 Custom Nutrition

4.3.2 Edible Decorations

4.3.3 Food Testing and Prototyping

4.3.4 Bakery Products

4.3.5 Confectionery and Desserts

4.4 By End User (In Value %)

4.4.1 Restaurants and Cafs

4.4.2 Food Processing and Manufacturing

4.4.3 Educational Institutions

4.4.4 Research and Innovation Centers

4.4.5 Retail and Grocery

4.5 By Region (In Value %)

4.5.1 Northeast

4.5.2 Midwest

4.5.3 South

4.5.4 West

5. USA 3D Food Printing Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Natural Machines

5.1.2 BeeHex

5.1.3 TNO (Netherlands Organization for Applied Scientific Research)

5.1.4 Choc Edge

5.1.5 3D Systems Corporation

5.1.6 Print2Taste GmbH

5.1.7 Barilla Group

5.1.8 Systems and Materials Research Corporation (SMRC)

5.1.9 Modern Meadow

5.1.10 Dovetailed

5.1.11 NovaMeat

5.1.12 Redefine Meat

5.1.13 Biozoon

5.1.14 XYZPrinting

5.1.15 ByFlow

5.2 Cross Comparison Parameters (R&D Spending, Market Share, Headquarters Location, Product Range, No. of Patents, Production Capacity, Technological Capabilities, Strategic Partnerships)

5.3 Market Share Analysis

5.4 Strategic Initiatives (Product Development, Market Expansion)

5.5 Mergers and Acquisitions

5.6 Investment Analysis (Corporate Investments, Government Funding)

5.7 Venture Capital Funding Trends

5.8 Government Grants and Subsidies

5.9 Private Equity Investments

6. USA 3D Food Printing Market Regulatory Framework

6.1 Food Additive and Material Standards

6.2 Compliance and Labeling Requirements

6.3 Food Safety and Sanitation Guidelines

6.4 FDA and USDA Involvement in Additive Food Manufacturing

7. USA 3D Food Printing Future Market Size (In USD Mn)

7.1 Projected Market Size

7.2 Key Factors Driving Future Growth

8. USA 3D Food Printing Future Market Segmentation

8.1 By Printer Type (In Value %)

8.2 By Ingredient Type (In Value %)

8.3 By Application (In Value %)

8.4 By End User (In Value %)

8.5 By Region (In Value %)

9. USA 3D Food Printing Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Targeted Marketing Initiatives

9.3 Strategic Product Launches

9.4 Industry White Space Opportunities

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial stage involves creating a comprehensive map of the USA 3D Food Printing market ecosystem, identifying key stakeholders and their roles. This process is based on extensive secondary research, including government databases and proprietary industry reports, to outline essential variables influencing the market.

Step 2: Market Analysis and Construction

We conduct a detailed historical analysis, examining the adoption rates of 3D printing technologies within the food sector. This includes analyzing product usage data across industry segments and revenue generation metrics to assess growth patterns.

Step 3: Hypothesis Validation and Expert Consultation

Key market hypotheses are tested through structured interviews with experts across the food technology sector, gaining insights into operational trends and innovation drivers. This stage involves gathering qualitative data to support quantitative findings.

Step 4: Research Synthesis and Final Output

The synthesis phase consolidates data from previous stages, presenting a validated view of the market landscape. Industry insights from direct interactions with 3D food printing companies and technology providers are integrated to offer a rounded, accurate market analysis.

Frequently Asked Questions

How big is the USA 3D Food Printing Market?

The USA 3D Food Printing market is valued at USD 200 million, driven by increased interest in personalized food production, sustainability, and technological advancements in additive manufacturing.

What are the primary challenges in the USA 3D Food Printing Market?

The USA 3D Food Printing market faces challenges such as high costs of equipment, limited range of edible materials, and compliance with food safety regulations, which can hinder wider adoption among small businesses.

Who are the major players in the USA 3D Food Printing Market?

Key players in the USA 3D Food Printing market include Natural Machines, BeeHex, TNO, and 3D Systems Corporation. These companies lead due to their innovative product portfolios, strong R&D capabilities, and strategic partnerships.

What drives the growth of the USA 3D Food Printing Market?

Growth in the USA 3D Food Printing market is primarily driven by consumer demand for customization, innovations in food-grade materials, and the push for eco-friendly production methods that reduce food waste.

What are the applications of 3D food printing in the USA?

Applications span across custom nutrition, food decoration, prototyping, and specialized dietary needs, with sectors like restaurants, healthcare, and education adopting this technology rapidly in the USA 3D Food Printing market.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.