USA Adhesives and Sealants Market Outlook to 2030

Region:North America

Author(s):Vijay Kumar

Product Code:KROD3659

October 2024

94

About the Report

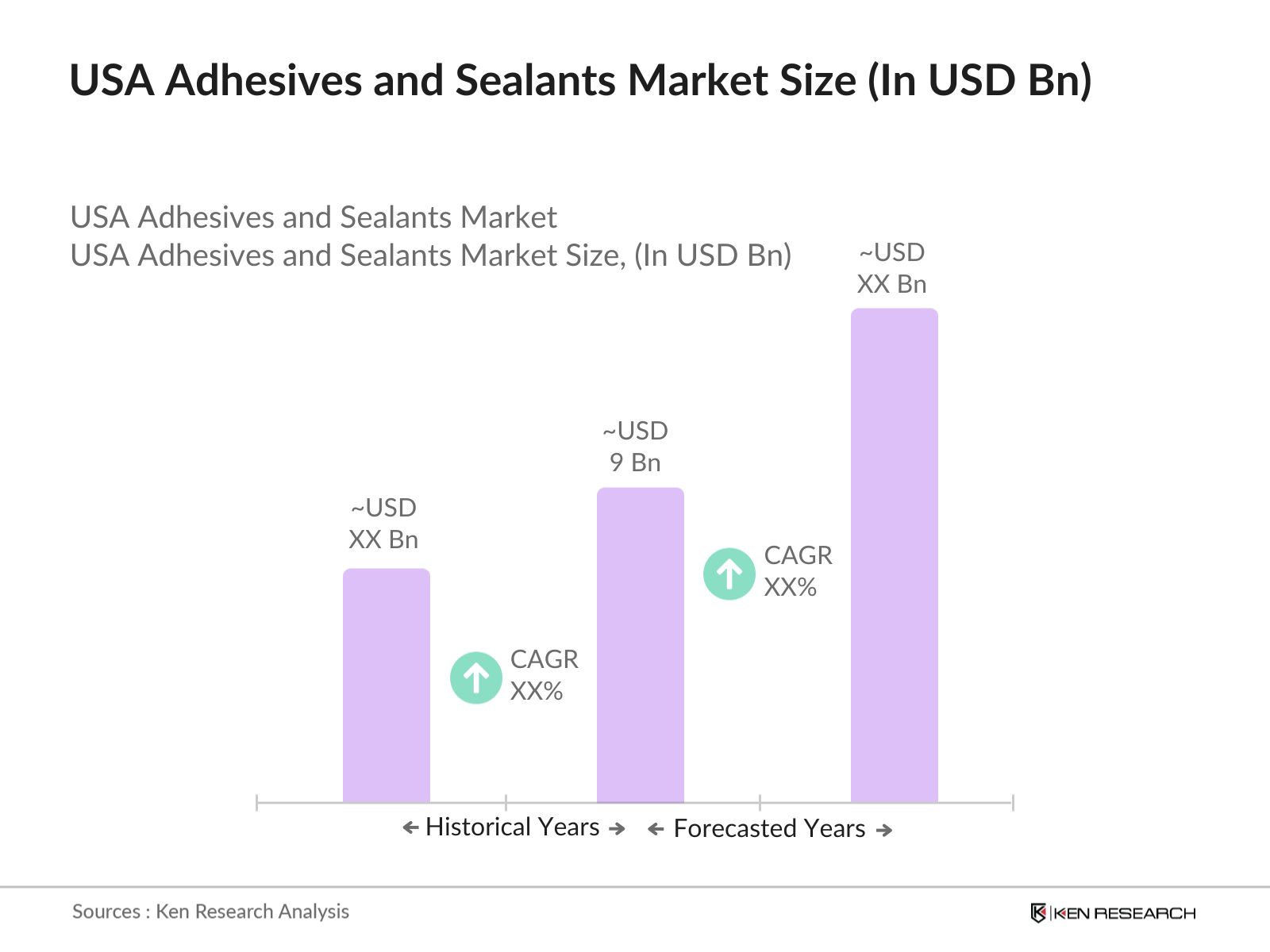

USA Adhesives and Sealants Market Overview

- The USA Adhesives and Sealants market is valued at USD 9 billion, based on a five-year historical analysis. This market is primarily driven by the rising demand from key industries such as construction, automotive, and packaging. The shift towards using adhesive bonding as an alternative to traditional mechanical fastening methods has enabled lighter-weight and stronger bonding solutions. The adoption of waterborne adhesives, which are more environmentally friendly and have lower VOC content, has also significantly boosted the market, especially in the construction and packaging sectors.

- Key cities like Los Angeles and Houston dominate the adhesives and sealants market due to their strong industrial base and infrastructure development. These cities are hubs for the construction and automotive sectors, which are significant end-users of adhesives and sealants. Their strategic geographic locations, combined with high investment in R&D activities, make them central players in the overall market growth.

- The U.S. EPA's regulations on VOC emissions have had a profound impact on the adhesive and sealant industry. Manufacturers are required to comply with the National Emission Standards for Hazardous Air Pollutants (NESHAP) and other state-level regulations, which has led to increased costs and the need for product reformulation. As a result, the market is seeing a gradual shift towards water-based and low-VOC adhesives.

USA Adhesives and Sealants Market Segmentation

By Product Type: The market is segmented by product type into water-based, solvent-based, hot-melt, and reactive adhesives. Water-based adhesives hold the largest market share due to their eco-friendly nature and extensive application across multiple industries. They are predominantly used in woodworking and packaging because they offer strong bonding capabilities without compromising on environmental safety.

By Application: The market is also segmented by application into building & construction, automotive, packaging, electronics, and others. The building and construction segment is the largest, owing to the high demand for adhesives and sealants for insulation, flooring, and panel bonding. The segment is expected to maintain its dominance due to ongoing infrastructural developments and a strong focus on green construction practices.

USA Adhesives and Sealants Market Competitive Landscape

The market's consolidation reflects the strategic focus of these companies on mergers, acquisitions, and product innovation to gain competitive advantages. These firms prioritize sustainability and compliance with regulatory standards, particularly with products that have low or no VOC content.

USA Adhesives and Sealants Industry Analysis

Growth Drivers

- Rise in Construction and Automotive Applications: The U.S. construction industry is a major consumer of adhesives and sealants, driven by increased investments in residential and commercial projects. As of 2023, the construction industry in the U.S. contributed over $1.8 trillion to the national GDP, with adhesives being a key component in flooring, insulation, and panel installation. Additionally, the automotive sector's robust recovery, with over 14.5 million vehicles produced in 2023, is significantly boosting demand for structural and non-structural adhesives, which are used in vehicle assembly, bonding, and sealing applications.

- Shift Towards Sustainable Products and Bio-Based Adhesives: The market is witnessing a notable shift towards bio-based adhesives due to environmental regulations and growing consumer preference for sustainable products. Bio-based adhesives made from renewable sources such as soy, starch, and lignin are gaining traction in the packaging and construction sectors. The industrys focus on reducing volatile organic compounds (VOCs) is influencing this trend. The implementation of the U.S.

- Increasing Demand in Packaging Sector: The U.S. packaging industry is one of the largest consumers of adhesives, driven by the booming e-commerce and food & beverage sectors. In 2023, the packaging industry was valued at over $200 billion, with adhesives being critical in box assembly, labeling, and flexible packaging. The demand for hot-melt adhesives, which offer quick setting and high bond strength, is particularly high in this sector.

Market Challenges

- Volatility in Raw Material Prices: Raw material costs for adhesives, especially for synthetic polymers and resins, have been highly volatile due to fluctuations in crude oil prices and supply chain disruptions. The Producer Price Index (PPI) for synthetic resin and rubber adhesives stood at 378.893 in August 2024, reflecting increased input costs for manufacturers. Such price volatility is affecting profit margins and pricing strategies for adhesive producers, making it a significant challenge for the industry.

- Stringent Environmental Regulations (VOC Emissions): Adhesive manufacturers are facing regulatory pressure to reduce VOC emissions as outlined by the U.S. EPA. These regulations are forcing manufacturers to reformulate products or invest in technology to develop low-VOC adhesives. Compliance with these regulations has increased production costs and led to the phasing out of certain solvent-based products.

USA Adhesives and Sealants Market Future Outlook

Over the next five years, the U.S. adhesives and sealants market is expected to witness robust growth, driven by advancements in adhesive technologies and the increasing adoption of environmentally friendly products. The automotive and electronics sectors will remain key growth drivers as they shift towards lightweight and efficient bonding solutions. Ongoing infrastructural projects and the use of adhesives in energy-efficient construction practices are also anticipated to bolster the market further.

Market Opportunities

- Technological Advancements in Polymer-Based Adhesives: Technological innovations, especially in the development of high-performance polymer adhesives, are opening new avenues for growth. The increased use of these adhesives in critical applications, such as automotive lightweighting and electronics assembly, is driven by their superior mechanical properties and environmental resistance. This is particularly relevant in the electronics sector, which saw a 15% rise in adhesive usage in circuit board and sensor assembly in 2023.

- Growth in Electronic and Electrical Applications: The U.S. electronics and electrical sector is expected to drive substantial demand for specialty adhesives. Adhesives used in circuit assemblies, battery pack construction, and display screen bonding have seen significant innovation, especially with the rise in electric vehicle (EV) production. The U.S. produced over 670,000 EVs in 2023, and adhesives are critical for assembling lightweight materials in these vehicles.

Scope of the Report

|

Product Type |

Water-Based Solvent-Based Hot-Melt Reactive Silicone Polyurethane |

|

Application |

Building & Construction Automotive Packaging Consumer/DIY Electronics |

|

Technology |

Pressure-Sensitive Reactive Emulsion |

|

End-Use Industry |

Residential Construction Industrial Manufacturing Commercial Applications |

|

Region |

Northeast Midwest South West |

Products

Key Target Audience

Adhesives and Sealants Manufacturers

Automotive Manufacturers

Construction Companies

Electronics Manufacturers

Healthcare and Medical Device Companies

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., US Environmental Protection Agency - EPA)

R&D Institutions focusing on Chemical and Material Sciences

Companies

Players Mentioned in the Report

3M Company

H.B. Fuller Company

Henkel AG & Co. KGaA

Arkema Group

Sika AG

Illinois Tool Works Inc.

Dow Inc.

BASF SE

Avery Dennison Corporation

MAPEI S.p.A.

Table of Contents

1. USA Adhesives and Sealants Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Key Market Segments Overview

1.5. Market Dynamics Overview (Supply Chain Analysis, Key Stakeholders, Distribution Channels)

2. USA Adhesives and Sealants Market Size (in USD Billion)

2.1. Historical Market Size

2.2. Current Market Size

2.3. Year-on-Year Growth Analysis

2.4. Key Market Developments and Milestones

3. USA Adhesives and Sealants Market Analysis

3.1. Market Drivers

3.1.1. Rise in Construction and Automotive Applications

3.1.2. Shift Towards Sustainable Products and Bio-Based Adhesives

3.1.3. Increasing Demand in Packaging Sector

3.2. Market Challenges

3.2.1. Volatility in Raw Material Prices

3.2.2. Stringent Environmental Regulations (VOC Emissions)

3.3. Market Opportunities

3.3.1. Technological Advancements in Polymer-Based Adhesives

3.3.2. Growth in Electronic and Electrical Applications

3.4. Market Trends

3.4.1. Rising Adoption of Hot-Melt Adhesives

3.4.2. Use of UV-Curable and Reactive Adhesives

3.5. Environmental and Regulatory Landscape

3.5.1. Impact of VOC Regulations

3.5.2. Compliance with the Toxic Substances Control Act (TSCA)

3.6. SWOT Analysis

3.7. Value Chain Analysis

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. USA Adhesives and Sealants Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Water-Based Adhesives

4.1.2. Solvent-Based Adhesives

4.1.3. Hot-Melt Adhesives

4.1.4. Reactive Adhesives

4.1.5. Silicone Sealants

4.1.6. Polyurethane Sealants

4.2. By Application (In Value %)

4.2.1. Building & Construction

4.2.2. Automotive

4.2.3. Packaging

4.2.4. Consumer/DIY

4.2.5. Electronics

4.3. By Technology (In Value %)

4.3.1. Pressure-Sensitive Adhesives

4.3.2. Reactive Technology

4.3.3. Emulsion Technology

4.4. By End-Use Industry (In Value %)

4.4.1. Residential Construction

4.4.2. Industrial Manufacturing

4.4.3. Commercial Applications

4.5. By Region (In Value %)

4.5.1. Northeast

4.5.2. Midwest

4.5.3. South

4.5.4. West

5. USA Adhesives and Sealants Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Henkel AG & Co. KGaA

5.1.2. 3M Company

5.1.3. Sika AG

5.1.4. H.B. Fuller Company

5.1.5. Arkema Group

5.1.6. Dow Inc.

5.1.7. PPG Industries

5.1.8. BASF SE

5.1.9. Avery Dennison Corporation

5.1.10. RPM International Inc.

5.1.11. Bostik (Arkema)

5.1.12. Huntsman Corporation

5.1.13. Illinois Tool Works Inc.

5.1.14. MAPEI Corporation

5.1.15. Ashland Global Holdings Inc.

5.2. Cross Comparison Parameters (Revenue, Regional Presence, Market Share, Product Portfolio, R&D Investments, Innovation Capabilities, Sustainability Initiatives, Strategic Alliances)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. USA Adhesives and Sealants Market Regulatory Framework

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes

7. USA Adhesives and Sealants Future Market Size (in USD Billion)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. USA Adhesives and Sealants Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By End-Use Industry (In Value %)

8.5. By Region (In Value %)

9. USA Adhesives and Sealants Market Analyst Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

This stage involves a comprehensive assessment of the U.S. adhesives and sealants market, focusing on stakeholders such as manufacturers, distributors, end-users, and regulatory agencies. Extensive desk research and industry-specific databases were used to identify key market drivers and variables.

Step 2: Market Analysis and Construction

Historical data for the U.S. adhesives and sealants market was compiled to analyze market penetration and revenue generation. This step involved a thorough evaluation of key market segments and their respective growth dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were validated through telephonic and in-person interviews with industry professionals. Insights from these consultations helped refine market estimates and projections.

Step 4: Research Synthesis and Final Output

The final phase included direct engagement with leading adhesive and sealant manufacturers to validate market data. This approach ensured the reliability and accuracy of the market forecast and segmentation.

Frequently Asked Questions

01. How big is the U.S. Adhesives and Sealants Market?

The USA Adhesives and Sealants market is valued at USD 9 billion, based on a five-year historical analysis. This market is primarily driven by the rising demand from key industries such as construction, automotive, and packaging.

02. What are the challenges in the U.S. Adhesives and Sealants Market?

The USA Adhesives and Sealants market challenges include regulatory restrictions on VOC emissions, high raw material costs, and intense competition among market players.

03. Who are the major players in the U.S. Adhesives and Sealants Market?

The USA Adhesives and Sealants market major players include 3M, Henkel AG & Co. KGaA, H.B. Fuller Company, Arkema Group, and Sika AG, who dominate the market due to their extensive product portfolios and strategic investments.

04. What are the growth drivers of the U.S. Adhesives and Sealants Market?

The USA Adhesives and Sealants market key drivers include advancements in adhesive technologies, a shift towards lightweight bonding solutions, and the growing emphasis on eco-friendly and sustainable products.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.