USA Anti-Drone Market Outlook to 2030

Region:North America

Author(s):Shubham Kashyap

Product Code:KROD5233

December 2024

82

About the Report

USA Anti-Drone Market Overview

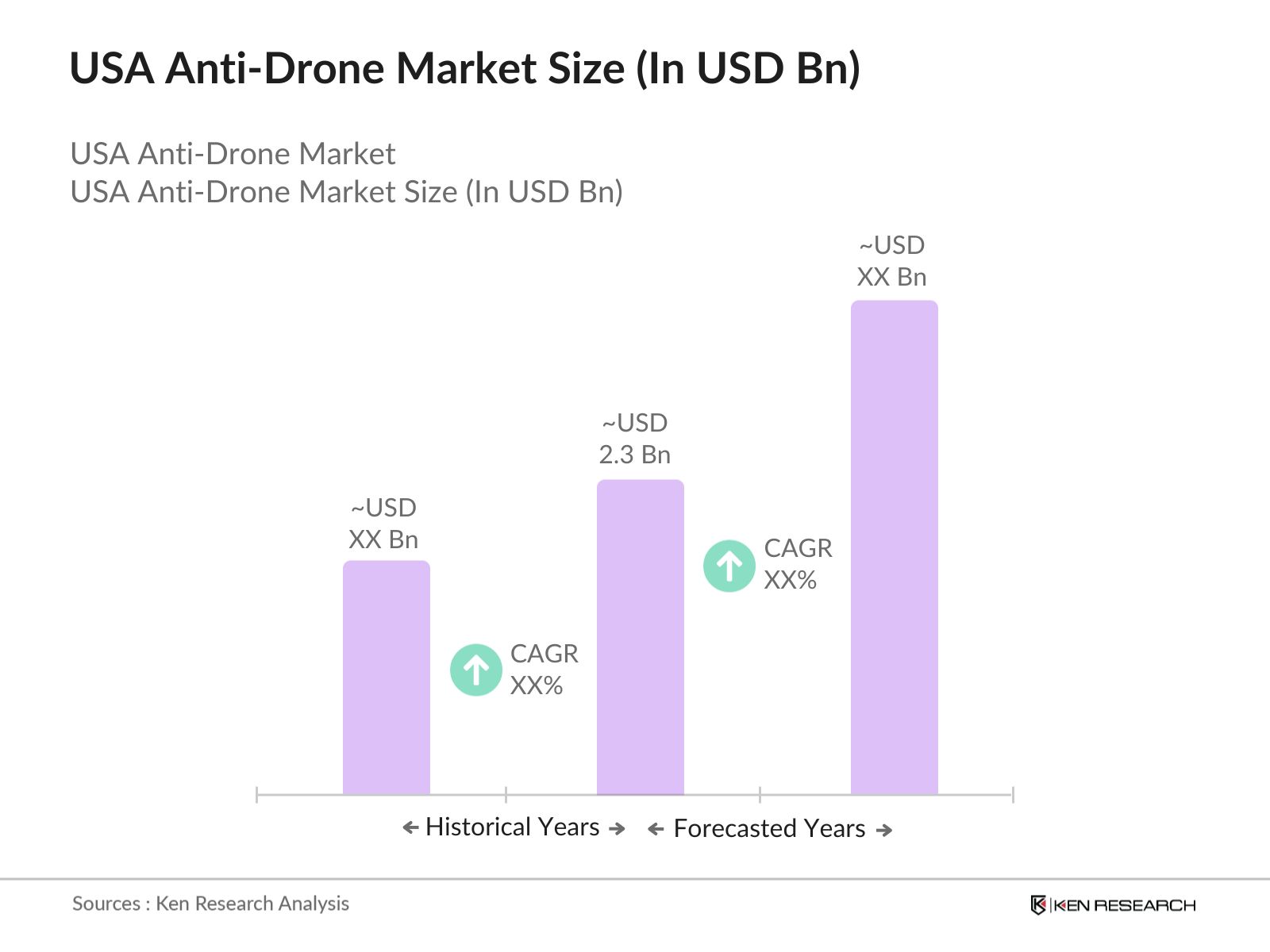

- The USA Anti-Drone Market is valued at around USD 2.3 billion, driven by the increasing demand for security solutions in critical areas like airports, defense, and public events. Factors such as the proliferation of drones and the rise in incidents involving unauthorized drone activity have accelerated market growth. The market benefits from the high demand for drone detection and interception systems across both public and private sectors, with continued government funding and the adoption of advanced technologies in security solutions.

- Key Demand Centers for Anti-Drone Systems in the USA include high-risk zones and densely populated urban areas such as New York, Washington D.C., and Los Angeles. These cities face significant risks due to high-profile events, government infrastructure, and densely populated areas where drone incursions pose a security threat. Defense-centric cities like San Diego also contribute to demand, as increased government contracts drive the adoption of anti-drone technologies to secure military airspace and sensitive installations.

- The Department of Homeland Security (DHS) issued comprehensive anti-drone guidelines in 2023, which specify operational protocols for public events and critical infrastructure. These guidelines have increased the deployment of anti-drone systems across DHS-managed sites, aligning with Homeland Securitys emphasis on proactive UAV threat mitigation. This regulatory framework has bolstered market growth, ensuring adherence to security protocols.

USA Anti-Drone Market Segmentation

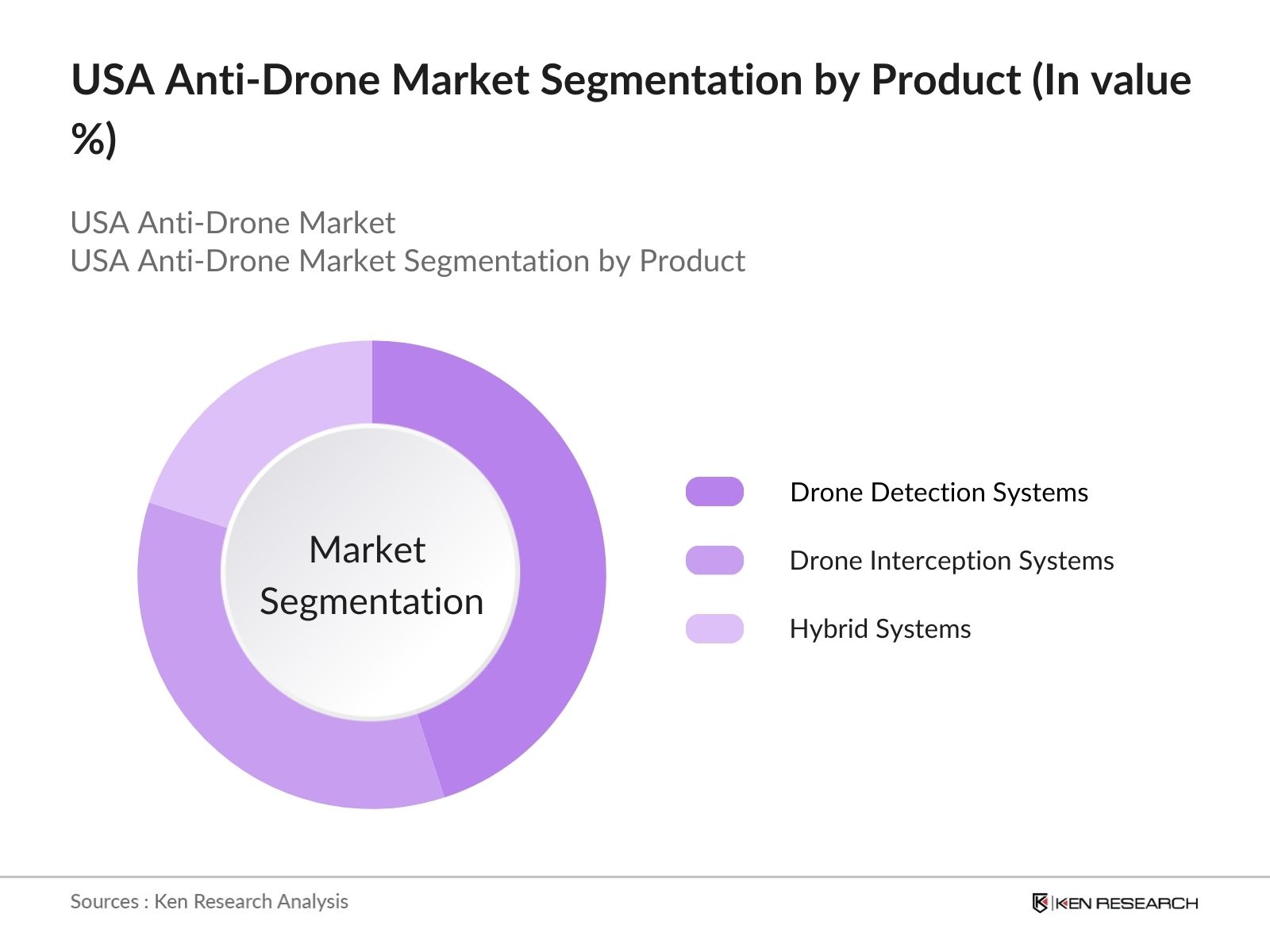

- By Product Type: The Market is segmented by product type into Drone Detection Systems, Drone Interception Systems, and Hybrid Systems. Recently, Drone Detection Systems hold the dominant market share due to their widespread adoption across commercial and government sectors, especially for monitoring airspace in urban and restricted areas. Detection systems are preferred for their ability to identify and track drones without physical interference, making them valuable for events, airports, and other sensitive locations. These systems are integral to preventive security measures, providing real-time alerts that help mitigate risks efficiently.

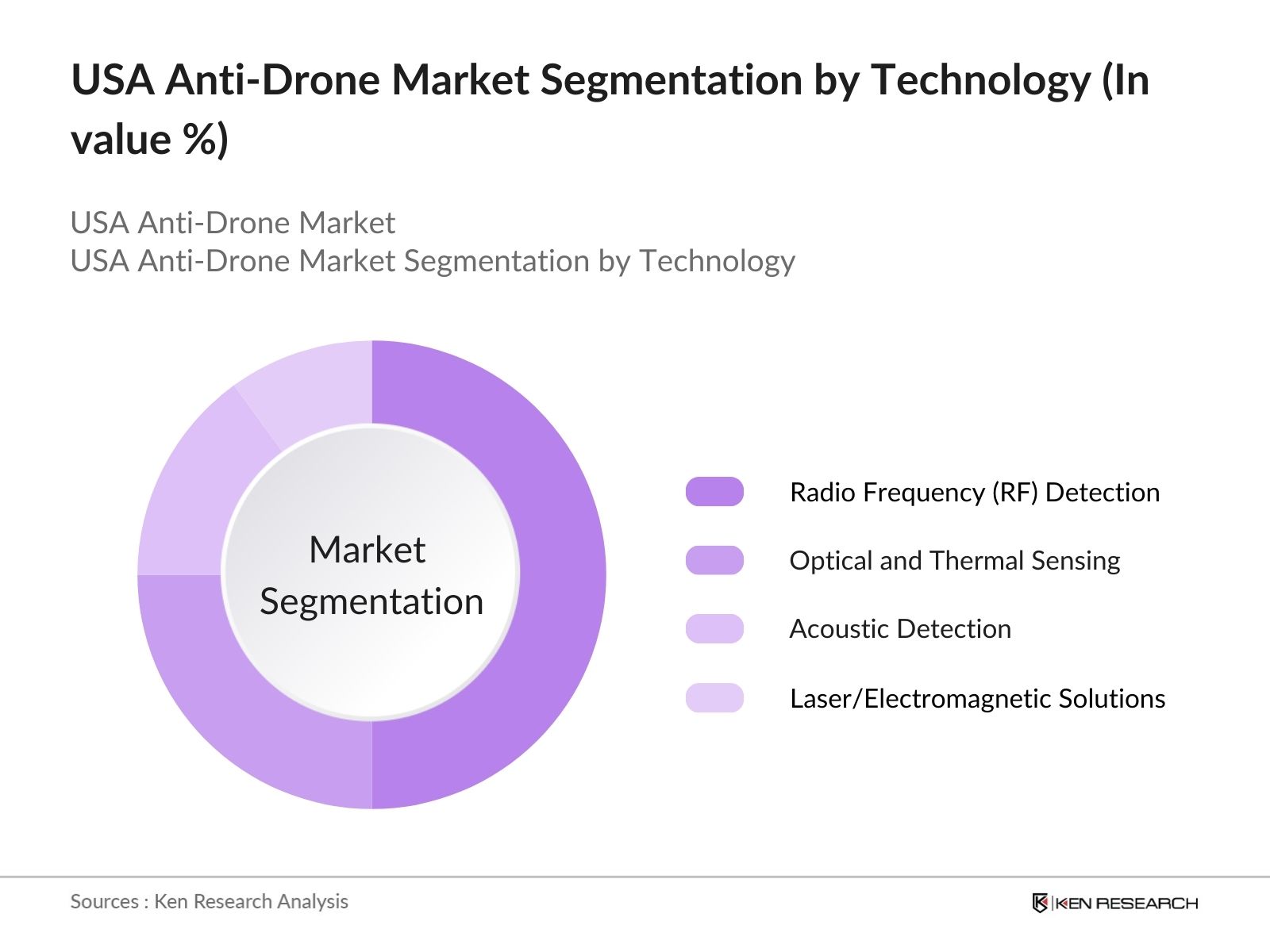

- By Technology: The market is further segmented by technology into Radio Frequency (RF) Detection, Optical and Thermal Sensing, Acoustic Detection, and Laser/Electromagnetic Solutions. Radio Frequency (RF) Detection leads this segmentation due to its ability to detect and track unauthorized drones over large areas without a line of sight. RF detection has become a primary choice, especially in urban settings and government facilities, due to its cost-effectiveness and capability to cover expansive airspace. The adoption of RF technology is also supported by its ability to provide early warnings, critical for pre-emptive measures in dense urban areas and defense applications.

USA Anti-Drone Market Competitive Landscape

The USA Anti-Drone Market is characterized by a few leading players who dominate the industry through extensive research capabilities, product innovation, and robust government partnerships. Major companies like Lockheed Martin, Raytheon Technologies, and Northrop Grumman lead due to their strong defense background and significant investments in anti-drone technology. These firms benefit from government contracts, enabling them to develop advanced, mission-critical solutions for sensitive installations.

USA Anti-Drone Market Analysis

Growth Drivers

- Increased Threat of Unmanned Aerial Vehicles (UAVs): The United States has reported a significant increase in unauthorized UAV activity, with around 2,000 incidents involving unmanned aerial vehicles breaching restricted airspaces in 2023 alone, according to the Federal Aviation Administration (FAA). The Department of Defense has noted that majority of these incidents posed potential security risks. This surge has heightened the demand for anti-drone systems capable of identifying, tracking, and neutralizing UAV threats. Such incidents illustrate the urgent need for robust counter-drone solutions to ensure airspace integrity and address emerging UAV threats to both military and civilian sectors.

- Rising Government Regulations for Airspace Protection: In 2023, the FAA introduced stricter regulations regarding UAV activity in commercial and restricted airspace, mandating additional security protocols for UAV operators near airports and sensitive locations. This regulatory pressure has pushed government bodies and commercial entities to implement anti-drone systems, especially in urban areas. The new guidelines aim to curtail unauthorized UAV activity and emphasize the need for responsive counter-drone technology to ensure compliance and safeguard airspace integrity. These regulations support the rapid deployment of anti-drone solutions across the USA.

- Technological Advancements in Anti-Drone Systems: As of 2024, the development of anti-drone technologies in the United States has advanced significantly, with government-supported projects yielding sophisticated systems featuring radar, radio frequency (RF) detection, and artificial intelligence (AI)-based tracking. The Defense Advanced Research Projects Agency (DARPA) reported funding of a substantial amount in 2023 toward enhancing counter-drone technology, particularly for radar-based systems. These technological advancements are fueling the U.S. anti-drone market, with new systems capable of targeting multiple UAVs simultaneously, thus addressing the growing demand for advanced security solutions.

Challenges

- High Development Costs of Anti-Drone Solutions: The average cost of developing an advanced anti-drone system in the U.S. ranges between USD 1.5 million-USD 3 million, according to data from the U.S. Department of Commerce in 2023. These high costs, coupled with complex technology integration requirements, limit the accessibility of these solutions for smaller organizations and local government entities. Additionally, the need for specialized components and extensive testing further increases expenses, posing a barrier to market expansion, particularly among budget-constrained entities.

- Privacy and Ethical Concerns: With the increase in counter-drone deployments, privacy concerns have risen due to potential overreach in surveillance capabilities. In 2023, the American Civil Liberties Union (ACLU) filed multiple cases challenging the use of anti-drone systems in public spaces, highlighting privacy invasion risks. The lack of clear guidelines around the ethical use of these systems has hindered their wider adoption, especially among civilian sectors concerned about potential misuse. This ongoing debate underscores the need for balancing security measures with privacy protections.

USA Anti-Drone Market Future Outlook

The USA Anti-Drone Market is set for significant growth, supported by increasing adoption in both government and private sectors. As drone technology continues to advance, so too will the demand for innovative anti-drone solutions capable of addressing new security challenges. The shift towards AI-powered detection and automated interception systems is expected to drive future growth, as these technologies offer greater accuracy and scalability. Additionally, expanding use cases within commercial and critical infrastructure sectors will further enhance the market's growth potential.

Future Market Opportunities

- Expansion of Anti-Drone Applications in Commercial Sectors: Anti-drone applications in commercial sectors, including stadiums, shopping centers, and corporate facilities, have grown substantially, with hundreds of new installations reported in 2023. The Commercial Facilities Sector-Specific Agency reported that high-profile events attracted an increased number of unauthorized UAVs, driving demand for anti-drone systems. This expansion offers significant growth potential as more commercial enterprises adopt counter-drone measures to protect customers and staff from potential UAV threats.

- Demand for Advanced Detection and Neutralization Solutions: In response to the increased UAV incidents in critical infrastructures, the demand for advanced detection and neutralization technologies surged in 2023, with over hundreds of anti-drone deployments reported at sensitive sites. These solutions utilize RF detectors and AI-based analytics, enabling efficient UAV identification and neutralization. The growing incidents at strategic locations highlight the demand for reliable detection and neutralization systems, paving the way for innovative anti-drone technology applications.

Scope of the Report

|

By Product Type |

Drone Detection Systems Drone Interception Systems Hybrid Systems |

|

By Technology |

Radio Frequency (RF) Detection Optical and Thermal Sensing Acoustic Detection Laser and Electromagnetic Solutions |

|

By Application |

Military and Defense Government and Public Infrastructure Commercial and Industrial Sites Airports and Critical Infrastructure |

|

By End-User |

Government Organizations Private Security Firms Commercial Enterprises Individual Users |

|

By Region |

North-East Mid-West South West |

Products

Key Target Audience

Government and Regulatory Bodies (Department of Homeland Security, Federal Aviation Administration)

Defense Organizations

Commercial Enterprises (Infrastructure and Utility Companies)

Airports and Public Infrastructure

Private Security Firms

Military and Law Enforcement Agencies

Investors and Venture Capitalist Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

Lockheed Martin

Raytheon Technologies

Northrop Grumman

Dedrone Inc.

DroneShield Ltd.

Airbus Group SE

SAIC

Liteye Systems, Inc.

Thales Group

Aselsan AS

Boeing

Blighter Surveillance Systems

Black Sage Technologies

General Dynamics

Leonardo S.p.A

Table of Contents

01 USA Anti-Drone Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

02 USA Anti-Drone Market Size (In USD Million)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

03 USA Anti-Drone Market Analysis

3.1 Growth Drivers

3.1.1 Increased Threat of Unmanned Aerial Vehicles (UAVs)

3.1.2 Rising Government Regulations for Airspace Protection

3.1.3 Technological Advancements in Anti-Drone Systems

3.1.4 Increasing Security Concerns in Military and Civil Sectors

3.2 Market Challenges

3.2.1 High Development Costs of Anti-Drone Solutions

3.2.2 Privacy and Ethical Concerns

3.2.3 Regulatory Restrictions on Counter-Drone Technology

3.3 Opportunities

3.3.1 Expansion of Anti-Drone Applications in Commercial Sectors

3.3.2 Demand for Advanced Detection and Neutralization Solutions

3.3.3 Integration with Existing Surveillance and Security Systems

3.4 Trends

3.4.1 Adoption of Artificial Intelligence and Machine Learning

3.4.2 Increased Focus on Miniaturized and Mobile Solutions

3.4.3 Development of Multi-Layered Defense Mechanisms

3.5 Government Regulations

3.5.1 FAA Regulations on Drone Countermeasures

3.5.2 Homeland Security Guidelines

3.5.3 Anti-Drone Legislation in Urban Areas

3.6 SWOT Analysis

3.7 Stake Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competitive Landscape Analysis

04 USA Anti-Drone Market Segmentation

4.1 By Product Type (In Value %)

4.1.1 Drone Detection Systems

4.1.2 Drone Interception Systems

4.1.3 Hybrid Systems

4.2 By Technology (In Value %)

4.2.1 Radio Frequency (RF) Detection

4.2.2 Optical and Thermal Sensing

4.2.3 Acoustic Detection

4.2.4 Laser and Electromagnetic Solutions

4.3 By Application (In Value %)

4.3.1 Military and Defense

4.3.2 Government and Public Infrastructure

4.3.3 Commercial and Industrial Sites

4.3.4 Airports and Critical Infrastructure

4.4 By End-User (In Value %)

4.4.1 Government Organizations

4.4.2 Private Security Firms

4.4.3 Commercial Enterprises

4.4.4 Individual Users

4.5 By Region (In Value %)

4.5.1 North-East

4.5.2 Mid-West

4.5.3 South

4.5.4 West

05 USA Anti-Drone Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Dedrone Inc.

5.1.2 DJI Innovations

5.1.3 Airbus Group SE

5.1.4 Northrop Grumman Corporation

5.1.5 Lockheed Martin Corporation

5.1.6 Raytheon Technologies Corporation

5.1.7 Thales Group

5.1.8 SAIC (Science Applications International Corporation)

5.1.9 DroneShield Ltd.

5.1.10 SRC, Inc.

5.1.11 Liteye Systems, Inc.

5.1.12 The Boeing Company

5.1.13 Blighter Surveillance Systems Ltd.

5.1.14 Aselsan AS

5.1.15 Black Sage Technologies

5.2 Cross Comparison Parameters (No. of Employees, Revenue, Headquarters, Market Share, Product Portfolio, Technology Focus, Strategic Initiatives, R&D Investment)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

06 USA Anti-Drone Market Regulatory Framework

6.1 National Standards for Counter-Drone Technologies

6.2 Compliance Requirements for Manufacturers

6.3 Certification Processes for Anti-Drone Equipment

07 USA Anti-Drone Future Market Size (In USD Million)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

08 USA Anti-Drone Market Future Segmentation

8.1 By Product Type (In Value %)

8.2 By Technology (In Value %)

8.3 By Application (In Value %)

8.4 By End-User (In Value %)

8.5 By Region (In Value %)

09 USA Anti-Drone Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

An ecosystem map was constructed, encompassing all major stakeholders within the USA Anti-Drone Market. This included collecting data from secondary and proprietary databases to identify essential market drivers, challenges, and trends.

Step 2: Market Analysis and Construction

Historical data on the USA Anti-Drone Market was analyzed, including market penetration rates and revenue estimates. This phase incorporated evaluating service quality statistics to validate and ensure accuracy in revenue and market share estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were developed based on historical trends and validated through CATIs with industry experts from leading companies. These insights provided operational perspectives essential for refining and corroborating market data.

Step 4: Research Synthesis and Final Output

The final phase involved in-depth interactions with anti-drone solution providers to gain insights into product preferences, market demand, and customer trends. This data was validated with a bottom-up approach to ensure a comprehensive analysis of the USA Anti-Drone Market.

Frequently Asked Questions

01 How big is the USA Anti-Drone Market?

The USA Anti-Drone Market is valued at USD 2.3 billion, driven by the increased need for airspace protection across various sectors, including government and commercial.

02 What are the challenges in the USA Anti-Drone Market?

Challenges in the USA Anti-Drone Market include high development costs, regulatory limitations, and concerns over privacy and ethical use. These factors complicate widespread adoption, especially in densely populated areas.

03 Who are the major players in the USA Anti-Drone Market?

Major players in the USA Anti-Drone Market include Lockheed Martin, Raytheon Technologies, Northrop Grumman, Dedrone Inc., and DroneShield Ltd., which lead due to strong government ties and cutting-edge technology offerings.

04 What drives growth in the USA Anti-Drone Market?

USA Anti-Drone Market growth is driven by escalating security concerns, regulatory pressures, and advancements in RF and AI-based detection technologies, particularly within critical infrastructure sectors.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.