USA Automobile Market Outlook to 2030

Region:North America

Author(s):Yogita Sahu

Product Code:KROD5171

November 2024

97

About the Report

USA Automobile Market Overview

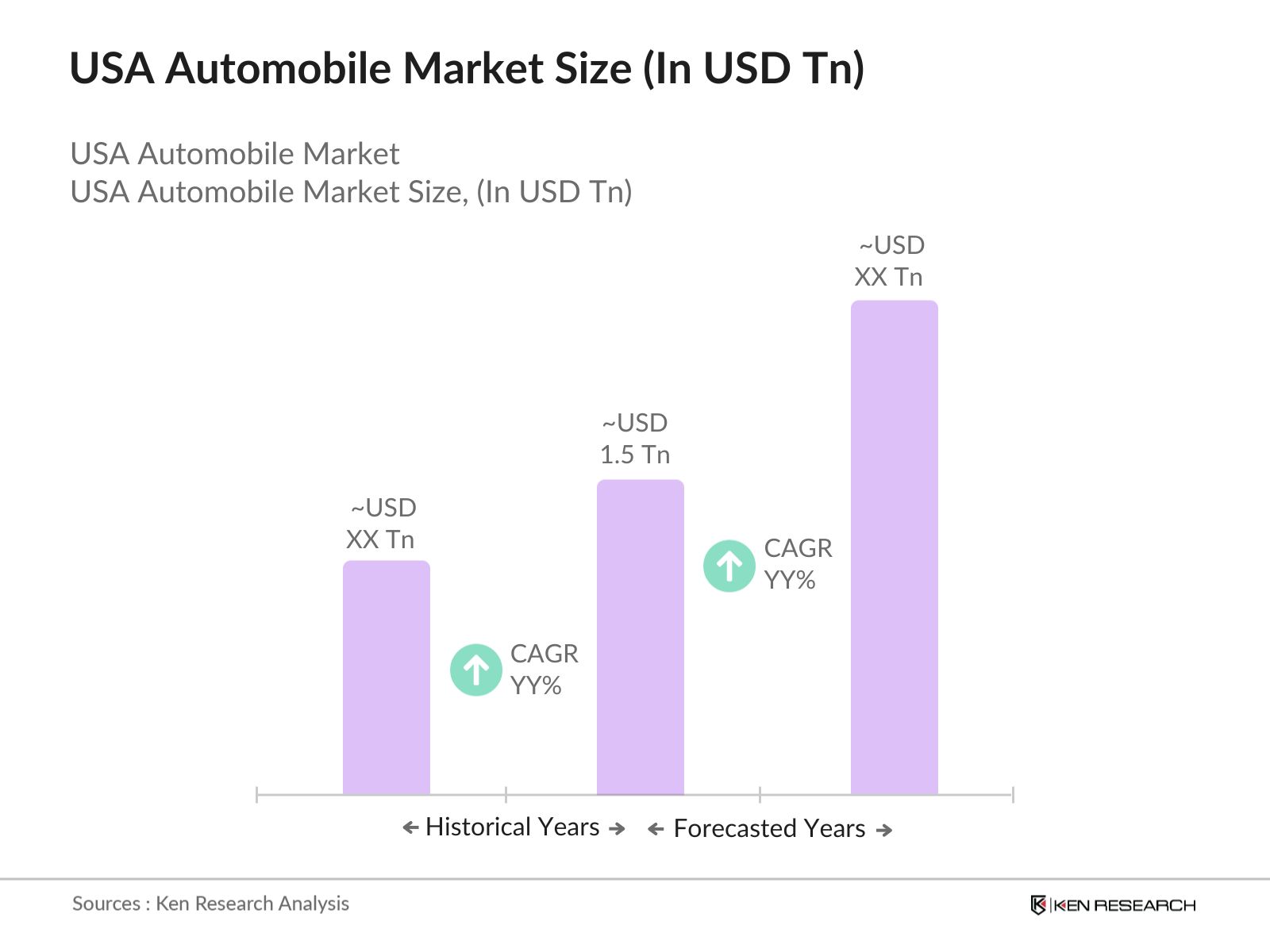

- The USA automobile market is valued at USD 1.5 trillion based on a five-year historical analysis. This substantial market size is driven by several factors, including a growing demand for electric vehicles (EVs) and autonomous driving technologies, infrastructure developments, and consumer preferences shifting toward sustainable transport solutions.

- The dominant regions within the market are California, Texas, and Michigan. California leads in EV adoption due to stringent environmental regulations and robust charging infrastructure, while Texas and Michigan dominate the internal combustion engine vehicle market due to their extensive manufacturing capacity and industry presence.

- In 2024, several states, including California and Texas, received approval to expand autonomous vehicle testing. The Department of Transportation approved $1.5 billion in funding for autonomous vehicle infrastructure development, which will drive innovations in the self-driving car market in the coming years.

USA Automobile Market Segmentation

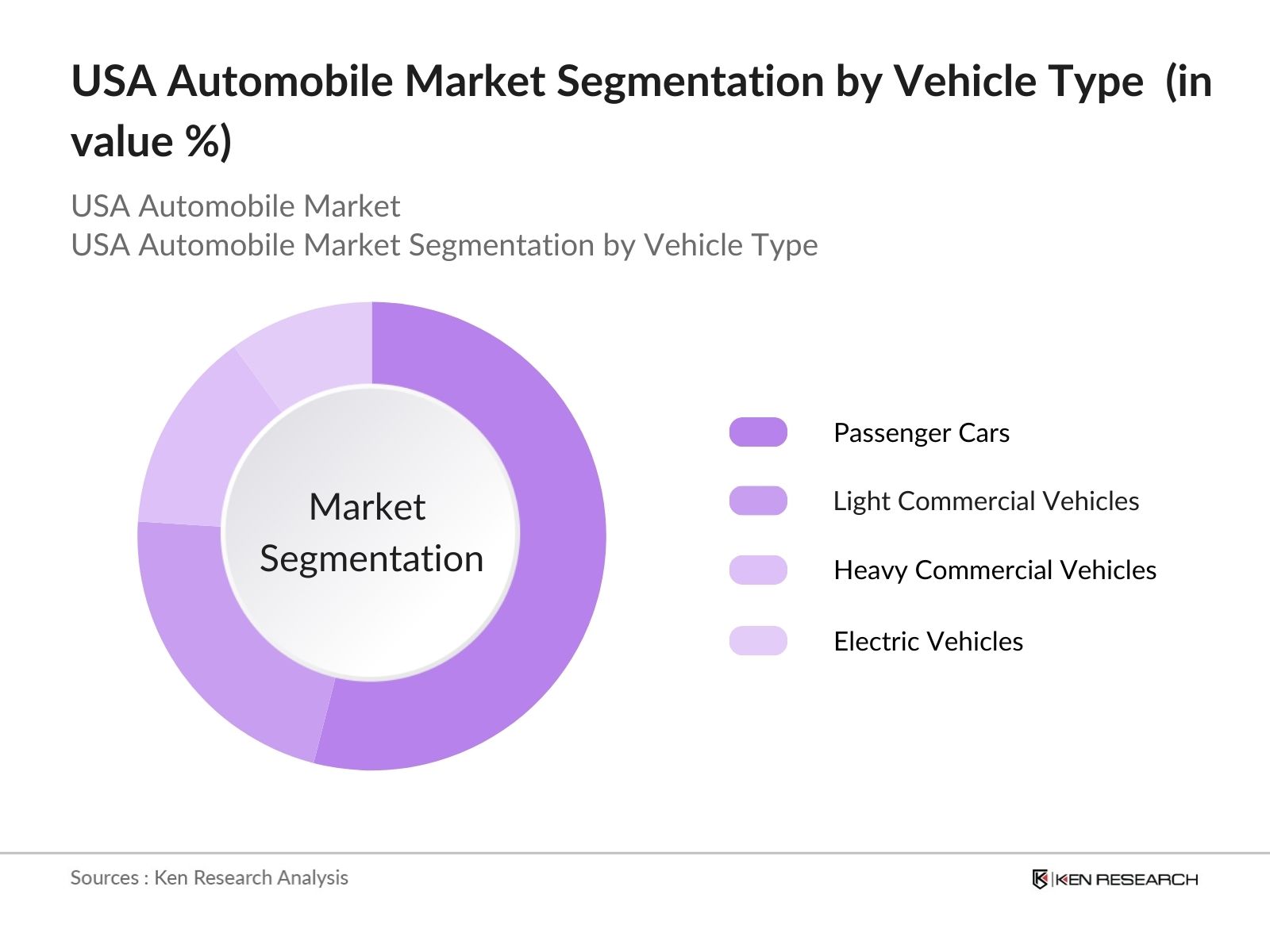

By Vehicle Type: The market is segmented by vehicle type into passenger cars, light commercial vehicles (LCVs), heavy commercial vehicles (HCVs), and electric vehicles (EVs). Recently, passenger cars have a dominant market share in the USA under the vehicle type segmentation, driven by the increasing consumer demand for personal mobility and advancements in passenger car technology. Additionally, passenger cars are increasingly integrated with advanced safety and entertainment features, further enhancing their appeal in the consumer market.

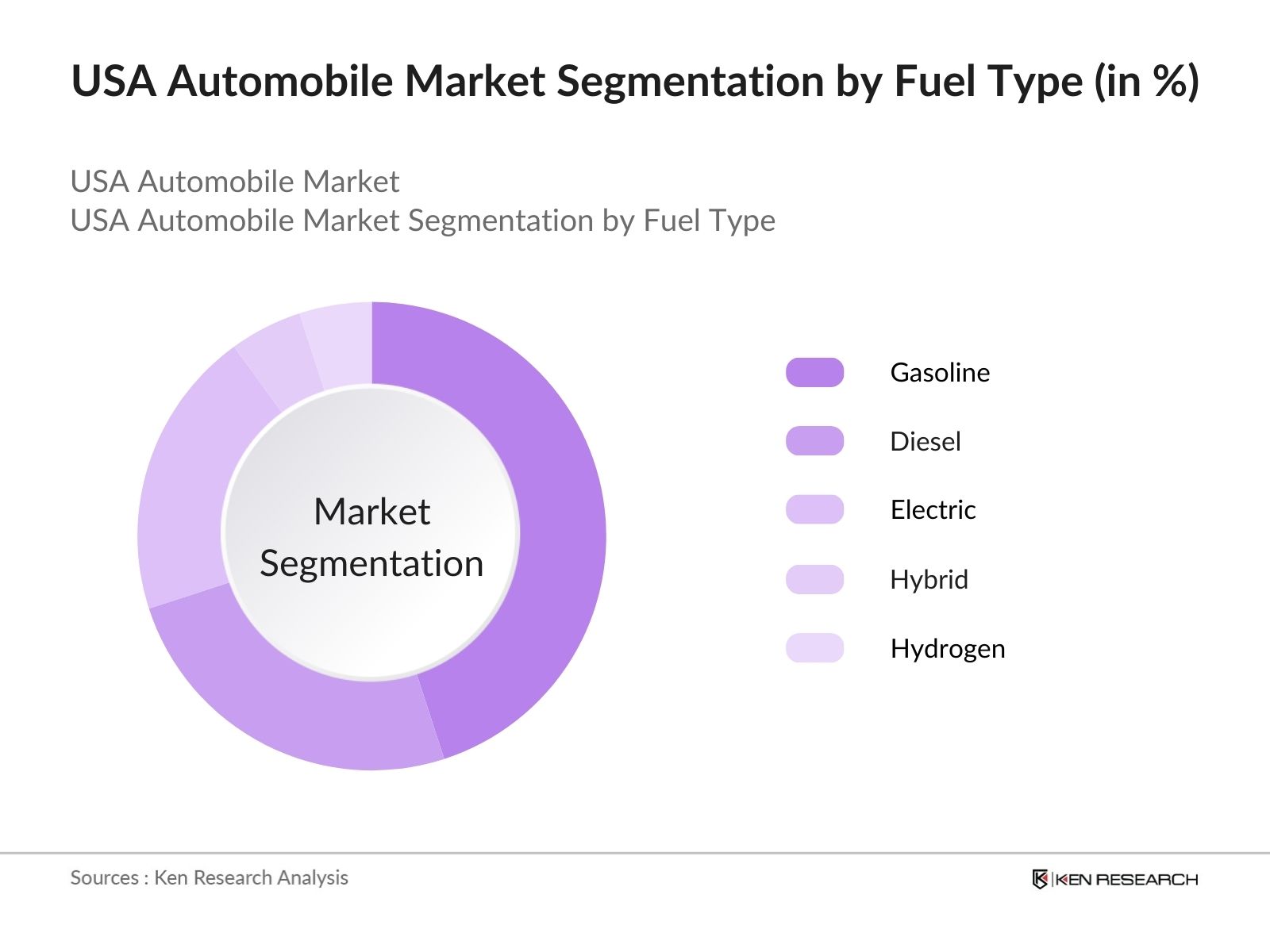

By Fuel Type: The market is also segmented by fuel type into gasoline, diesel, electric, hybrid, and hydrogen. Gasoline-powered vehicles still maintain the largest market share under the fuel type segmentation, largely due to their widespread availability and consumer familiarity. Despite growing interest in electric and hybrid vehicles, gasoline vehicles continue to dominate because of their relatively lower upfront costs and the well-established refueling infrastructure across the country.

USA Automobile Competitive Landscape

The market is dominated by a few key players, including local giants such as General Motors, Ford, and Tesla, alongside global automotive leaders like Toyota and Volkswagen. This consolidation demonstrates the strong influence of these companies, especially in terms of technological innovation, large-scale production, and brand loyalty.

|

Company |

Year of Establishment |

Headquarters |

Annual Revenue (USD Bn) |

No. of Employees |

R&D Investment (USD Bn) |

EV Model Portfolio |

Global Presence |

Autonomous Vehicle Testing |

Major Production Plants |

|

General Motors |

1908 |

Detroit, Michigan |

|||||||

|

Ford Motor Company |

1903 |

Dearborn, Michigan |

|||||||

|

Tesla Inc. |

2003 |

Palo Alto, California |

|||||||

|

Toyota Motor Corp. |

1937 |

Toyota City, Japan |

|||||||

|

Volkswagen Group |

1937 |

Wolfsburg, Germany |

USA Automobile Market Analysis

Market Growth Drivers

- Increased Vehicle Production: The USA automobile sector saw a rise in vehicle production, driven by the need for newer models with advanced safety features. In 2024, the country produced around 10 million vehicles, including electric and traditional fuel-based cars, a significant increase from the previous years due to consumer demand for safer and more fuel-efficient vehicles. The manufacturing boost aligns with the US government's push towards increasing domestic production and decreasing reliance on imports, supported manufacturing and labor market funding initiative.

- Surge in EV Charging Infrastructure: The expansion of EV charging stations across the USA in 2024 has propelled the electric vehicle (EV) segment. By 2024, the number of publicly available charging stations crossed 192,000 nationwide, which aligns with federal investments in clean energy infrastructure. This growth has helped increase EV adoption, which now constitutes over 15% of new vehicle registrations, further accelerating the shift from traditional gasoline-based cars to cleaner alternatives.

- Rise in Consumer Financing: The expansion of consumer financing options has fueled automobile sales in the USA, with 7 million vehicles financed through loans or leases in 2024. More favorable terms from financial institutions, coupled with a recovering economy, have increased consumer purchasing power. This driver is particularly significant in mid-segment car sales, boosting overall demand across the market.

Market Challenges

- Supply Chain Disruptions: The USA automotive industry is facing ongoing challenges related to global supply chain bottlenecks in 2024. Over 1.5 million vehicles were delayed due to shortages in critical components like semiconductors, hindering production schedules. This shortage has forced manufacturers to either pause production or scale down operations, creating significant delivery backlogs and increased operational costs.

- Labor Shortages: Labor shortages remain a challenge in the USAs automobile manufacturing sector, with around 30,000 unfilled positions in 2024.

- This shortage, particularly in skilled labor for automotive engineering and manufacturing roles, has impacted production capacities, delayed new model releases and increased labor costs for manufacturers.

USA Automobile Market Future Outlook

Over the next five years, the USA automobile industry is expected to experience growth, driven by continuous advancements in electric vehicle technology, government support through EV tax credits, and rising consumer demand for eco-friendly and fuel-efficient vehicles. The introduction of more affordable electric cars and improved charging infrastructure will further support the expansion of this market.

Future Market Opportunities

- Growth in Autonomous Vehicle Deployments: By 2028, major automakers will roll out a substantial number of autonomous vehicles across urban centers in the USA. The governments support for autonomous technology infrastructure will lead to the deployment of at least 100,000 fully autonomous vehicles within the next five years, transforming urban transport and logistics.

- Acceleration of Vehicle Electrification for Public Transport: The public transport sector will electrify a significant portion of its fleet by 2028, with over 50,000 electric buses in service across major cities. Federal and state governments will continue to prioritize grants and incentives for public transit agencies to replace diesel-powered buses with electric alternatives, reducing emissions and operational costs.

Scope of the Report

|

Vehicle Type |

Passenger Cars Light Commercial Vehicles Heavy Commercial Vehicles Electric Vehicles Hybrid Vehicles |

|

Fuel Type |

Gasoline Diesel Electric Hybrid Hydrogen |

|

Propulsion Type |

ICE BEV PHEV FCEV |

|

Application |

Private Commercial Industrial |

|

Region |

North East West South |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Automotive Manufacturers

Original Equipment Manufacturers (OEMs)

Banks and Financial Institution

Government and Regulatory Bodies (NHTSA, EPA)

Investment and Venture Capitalist Firms

Autonomous Vehicle Technology Providers

Electric Vehicle Infrastructure Companies

Companies

Players Mentioned in the Report:

General Motors

Ford Motor Company

Tesla Inc.

Toyota Motor Corporation

Volkswagen Group

Stellantis N.V.

Honda Motor Co. Ltd.

Nissan Motor Co. Ltd.

Rivian Automotive Inc.

Lucid Motors

Hyundai Motor Group

BMW Group

Mercedes-Benz AG

Subaru Corporation

Volvo Cars

Table of Contents

USA Automobile Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Unit Sales, Revenue Growth, Fleet Expansion)

1.4. Market Segmentation Overview (Electric, Hybrid, ICE, Vehicle Types)

USA Automobile Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis (Unit Sales, Market Penetration)

2.3. Key Market Developments and Milestones

USA Automobile Market Analysis

3.1. Growth Drivers (EV Adoption Rate, Infrastructure Investment, Consumer Preferences) 3.1.1. Government Incentives and Subsidies (EV Tax Credits, ZEV Mandates)

3.1.2. Technological Advancements (Autonomous Vehicles, AI Integration)

3.1.3. Consumer Demand Shifts (EVs, SUVs, Connected Cars)

3.1.4. Supply Chain Optimization (Reshoring of Manufacturing, Digital Twins)

3.2. Market Challenges (Semiconductor Shortages, Supply Chain Disruptions)

3.2.1. Raw Material Costs (Lithium, Aluminum)

3.2.2. Regulatory Compliance Costs (Emission Standards, Safety Regulations)

3.2.3. Infrastructure Deficit (EV Charging Stations, Hydrogen Fueling Networks)

3.3. Opportunities (Automotive Software, Mobility-as-a-Service)

3.3.1. Expansion into Autonomous Vehicle Ecosystem

3.3.2. Vehicle-to-Grid (V2G) Solutions

3.3.3. Circular Economy Initiatives (Recycling, Reuse)

3.4. Trends (EV Charging Technologies, Battery Swapping)

3.4.1. Digital Retail Platforms

3.4.2. Shared Mobility Growth (Car Subscription Models)

3.4.3. Advanced Driver Assistance Systems (ADAS) Penetration

3.5. Government Regulation (CAFE Standards, State-Level ZEV Programs)

3.5.1. Federal Fuel Efficiency Regulations

3.5.2. EV Infrastructure Bills

3.5.3. State-Specific Regulations (California ZEV Program, Texas Energy Storage)

3.6. SWOT Analysis

3.7. Stake Ecosystem (OEMs, Tier 1 Suppliers, Technology Providers)

3.8. Porters Five Forces (Competitive Rivalry, Supplier Power)

3.9. Competition Ecosystem

USA Automobile Market Segmentation

4.1. By Vehicle Type (In Value %)

4.1.1. Passenger Cars

4.1.2. Light Commercial Vehicles (LCVs)

4.1.3. Heavy Commercial Vehicles (HCVs)

4.1.4. Electric Vehicles (EVs)

4.1.5. Hybrid Vehicles

4.2. By Fuel Type (In Value %)

4.2.1. Gasoline

4.2.2. Diesel

4.2.3. Electric

4.2.4. Hybrid

4.2.5. Hydrogen

4.3. By Propulsion Type (In Value %)

4.3.1. Internal Combustion Engine (ICE)

4.3.2. Battery Electric Vehicles (BEVs)

4.3.3. Plug-in Hybrid Vehicles (PHEVs)

4.3.4. Fuel Cell Electric Vehicles (FCEVs)

4.4. By Application (In Value %)

4.4.1. Private

4.4.2. Commercial

4.4.3. Industrial

4.5. By Region (In Value %)

4.5.1. North

4.5.2. East

4.5.3. South

4.5.4. West

USA Automobile Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. General Motors

5.1.2. Ford Motor Company

5.1.3. Tesla Inc.

5.1.4. Toyota Motor Corporation

5.1.5. Stellantis N.V.

5.1.6. Honda Motor Co. Ltd.

5.1.7. Nissan Motor Co. Ltd.

5.1.8. Rivian Automotive Inc.

5.1.9. Lucid Motors

5.1.10. Volkswagen Group

5.1.11. Hyundai Motor Group

5.1.12. BMW Group

5.1.13. Mercedes-Benz AG

5.1.14. Volvo Cars

5.1.15. Subaru Corporation

5.2. Cross Comparison Parameters (No. of Manufacturing Plants, R&D Investments, EV Portfolio Size, Autonomous Vehicle Testing, Market Penetration, Unit Sales, Revenue, Headquarters Location)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

USA Automobile Market Regulatory Framework

6.1. Safety Standards (FMVSS Compliance, Crashworthiness)

6.2. Emission Standards (EPA Regulations, Tier 3 Standards)

6.3. Certification Processes (NHTSA Certification, CARB Certification)

USA Automobile Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (EV Transition, Government Incentives)

USA Automobile Future Market Segmentation

8.1. By Vehicle Type (In Value %)

8.2. By Fuel Type (In Value %)

8.3. By Propulsion Type (In Value %)

8.4. By Application (In Value %)

8.5. By Region (In Value %)

USA Automobile Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Behavior Analysis

9.3. Marketing Strategies

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase of research involves identifying key stakeholders within the USA Automobile Market. Extensive desk research is conducted using secondary databases, government publications, and proprietary sources to define crucial variables influencing market performance.

Step 2: Market Analysis and Construction

This phase focuses on gathering and analyzing historical market data, such as vehicle production, sales figures, and regulatory influences. Data is cross-referenced with industry benchmarks to validate market growth and ensure accuracy in projections.

Step 3: Hypothesis Validation and Expert Consultation

To refine our research, expert interviews are conducted with industry stakeholders, including executives from top automotive firms. This step validates key assumptions and provides deeper insights into emerging trends, competitive dynamics, and consumer behaviors.

Step 4: Research Synthesis and Final Output

In the final step, we consolidate data from multiple sources, including manufacturer insights and market performance indicators, to produce an accurate and reliable report. This ensures a well-rounded analysis and robust conclusions.

Frequently Asked Questions

01. How big is the USA Automobile Market?

The USA automobile market is valued at USD 1.5 trillion, supported by strong demand for electric vehicles and advancements in autonomous vehicle technology.

02. What are the challenges in the USA Automobile Market?

Challenges in the USA automobile market include semiconductor shortages, fluctuating raw material costs, and increasing regulatory requirements, particularly around emissions and safety standards.

03. Who are the major players in the USA Automobile Market?

Key players in the USA automobile market include General Motors, Ford, Tesla, Toyota, and Volkswagen, each dominating due to their extensive production capabilities, R&D investments, and established brand presence.

04. What are the growth drivers of the USA Automobile Market?

The USA automobile market is driven by consumer demand for electric and autonomous vehicles, government incentives, and ongoing technological advancements in vehicle connectivity and safety.

05. What role does government regulation play in the USA Automobile Market?

Government regulations, such as emissions standards and EV incentives, play a critical role in shaping the market by encouraging the adoption of cleaner, more efficient vehicles.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.