USA Bone and Joint Health Supplements Market Outlook to 2030

Region:North America

Author(s):Meenakshi Bisht

Product Code:KROD7182

December 2024

81

About the Report

USA Bone and Joint Health Supplements Market Overview

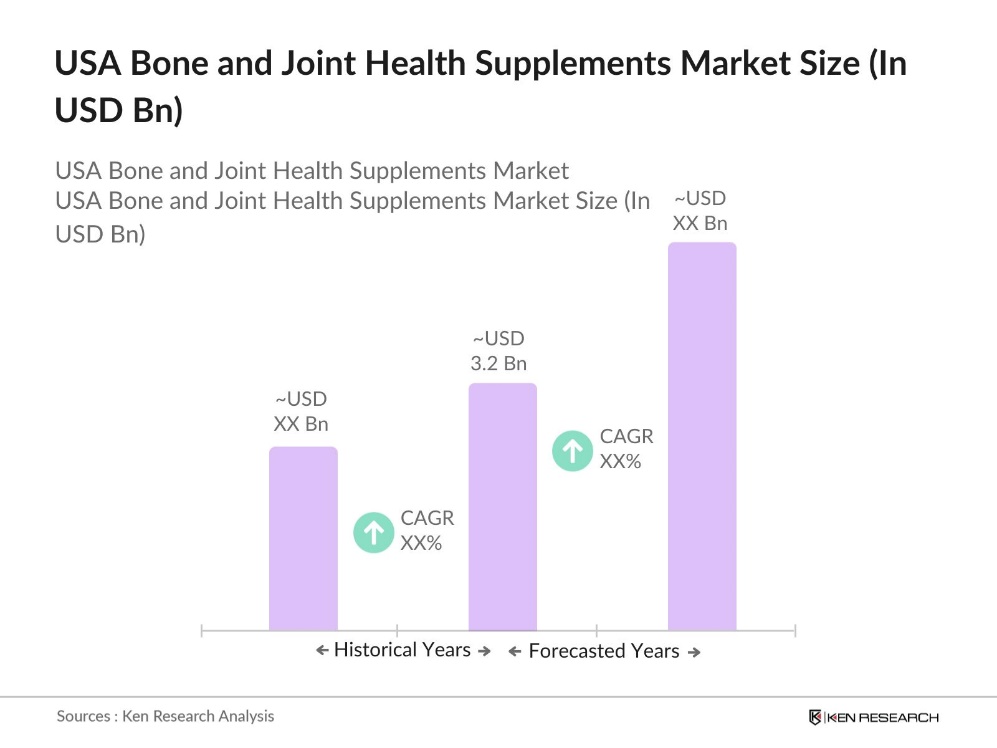

- The U.S. Bone and Joint Health Supplements market is valued at USD 3.2 billion, largely driven by the aging population and increasing prevalence of bone-related conditions. Market growth is bolstered by heightened consumer awareness of preventive healthcare and advancements in supplement formulation that enhance bioavailability. Supplements catering to bone density and joint lubrication, such as glucosamine and collagen-based products, have seen substantial demand due to the rising concern over osteoporosis and arthritis.

- Cities like New York, Los Angeles, and Chicago, along with states such as California and Florida, lead the market for bone and joint health supplements in the U.S. This dominance stems from their large populations of aging adults, high-income demographics, and a robust healthcare infrastructure that emphasizes preventive health. Additionally, these regions have a dense concentration of health-conscious consumers who prioritize dietary supplementation to maintain mobility and quality of life.

- In April 2024, the FDA issued draft guidance titled "Dietary Supplements: New Dietary Ingredient Notification Master Files." This document introduces the concept of NDI master files, which allow manufacturers to submit detailed information about a new dietary ingredient. Subsequent companies can reference these master files in their own NDI notifications, streamlining the process and promoting transparency. This is particularly relevant for bone and joint health supplements introducing novel ingredients.

USA Bone and Joint Health Supplements Market Segmentation

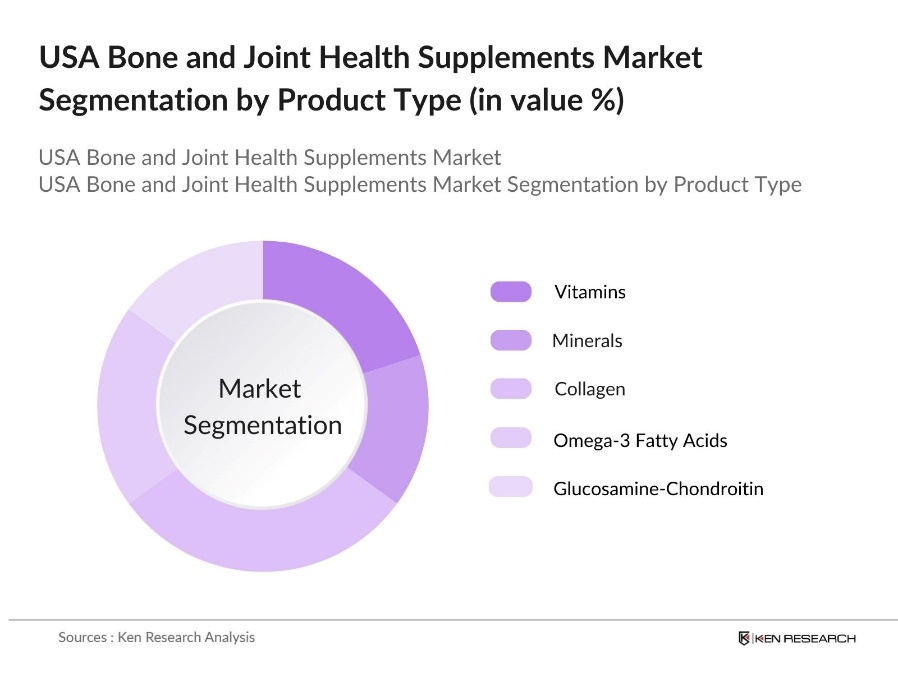

By Product Type: The market is segmented by product type into vitamins, minerals, collagen, omega-3 fatty acids, and glucosamine-chondroitin. Among these, collagen-based supplements currently hold the dominant market share, primarily due to their wide-ranging benefits for joint health, skin, and bone density. Collagens versatility and its role in supporting cartilage repair and reducing inflammation make it highly sought after, particularly among older adults and fitness enthusiasts.

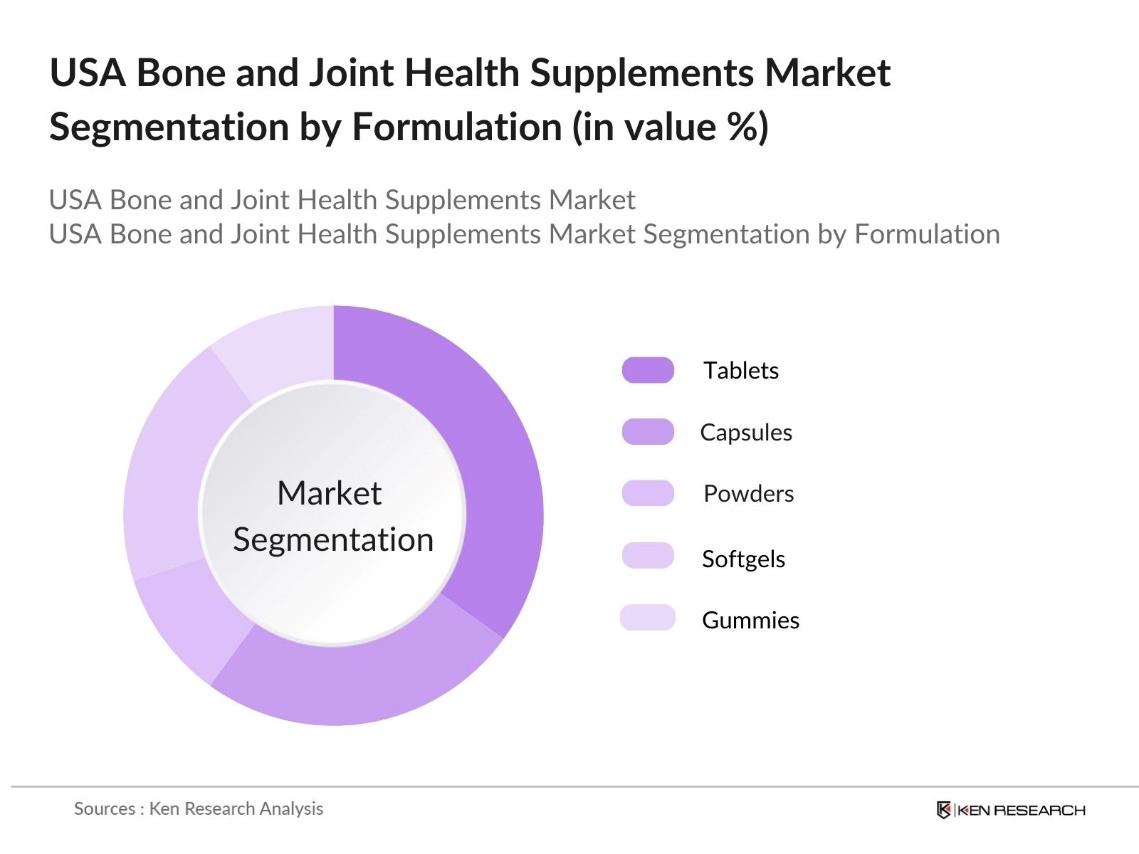

By Formulation: The market is segmented by formulation into tablets, capsules, powders, softgels, and gummies. Tablets dominate the formulation segment due to their convenience, affordability, and ease of dosage management. Tablets remain the preferred choice for consumers seeking efficacy and simplicity, especially for vitamins and minerals, as they offer controlled doses that meet daily recommended intakes.

USA Bone and Joint Health Supplements Market Competitive Landscape

The U.S. Bone and Joint Health Supplements market is highly competitive, with significant players such as Amway, Bayer AG, and Nature's Bounty dominating through expansive product lines and extensive distribution channels. This market is characterized by brands with a robust R&D focus, catering to specific consumer needs through innovative formulations and product types.

USA Bone and Joint Health Supplements Industry Analysis

Growth Drivers

- Aging Population: The United States is experiencing a significant demographic shift, with the number of individuals aged 65 and older projected to reach 56 million in 2024. This aging population is more susceptible to bone-related conditions such as osteoporosis and arthritis, leading to increased demand for bone and joint health supplements. According to the U.S. Census Bureau, the elderly population is expected to continue growing, underscoring the need for products that support bone health.

- Increasing Health Awareness: There is a growing awareness among Americans about the importance of maintaining bone health. The National Health and Nutrition Examination Survey (NHANES) indicates that a significant portion of the population is not meeting the recommended daily intake of calcium and vitamin D, essential nutrients for bone health. This awareness is driving consumers to seek supplements to bridge nutritional gaps.

- Rising Prevalence of Bone-Related Disorders: Bone-related disorders are becoming increasingly common in the U.S. The Centers for Disease Control and Prevention (CDC) reports that approximately 54 million Americans have low bone mass, placing them at increased risk for osteoporosis and fractures. This prevalence highlights the necessity for preventive measures, including the use of bone and joint health supplements.

Market Challenges

- Regulatory Hurdles: The dietary supplement industry in the U.S. faces stringent regulations enforced by the FDA. Companies must adhere to the Dietary Supplement Health and Education Act (DSHEA) and Good Manufacturing Practices (GMP), both of which require extensive resources to ensure compliance. Failure to meet these regulatory standards can result in product recalls and potential legal complications, making regulatory adherence a critical but challenging aspect of operating within the bone and joint health supplement market.

- High Competition: The U.S. bone and joint health supplement market is highly competitive, with numerous brands vying for consumer attention. This intense competition creates significant barriers for new companies trying to enter the market and makes it challenging for established brands to retain market share. To stand out, companies must focus on investments in marketing, product innovation, and maintaining high-quality standards, which are essential to differentiate their offerings in a crowded market.

USA Bone and Joint Health Supplements Market Future Outlook

The U.S. Bone and Joint Health Supplements market is anticipated to grow significantly over the coming years, driven by consumer demand for natural and sustainable products, as well as advancements in nutraceutical formulations. Growing awareness of personalized nutrition is expected to further propel this market as consumers seek targeted solutions for bone density, joint health, and inflammation management.

Market Opportunities

- Emerging Natural and Plant-Based Supplements: Consumer interest is shifting toward natural and plant-based options in the dietary supplement market. This preference creates new opportunities for companies to develop bone and joint health products that use plant-derived ingredients, such as herbal extracts and botanical formulations. As consumers increasingly seek these alternatives, brands can cater to demand by introducing innovative plant-based supplements that support bone health and align with a natural wellness lifestyle.

- Expansion into E-commerce Channels: The rapid growth of e-commerce is reshaping the way dietary supplements reach consumers. Online platforms have opened up a convenient and accessible channel, enabling brands to connect with a larger and more diverse audience. This expansion into e-commerce offers supplement companies a direct-to-consumer approach, allowing them to build stronger brand presence, provide detailed product information, and deliver to consumers who prioritize ease and efficiency in their shopping experience.

Scope of the Report

|

Product Type |

Vitamins |

|

Formulation |

Tablets |

|

Consumer Group |

Infants |

|

Sales Channel |

E-commerce Pharmacies |

|

Region |

Northeast |

Products

Key Target Audience

Healthcare Industry

Insurance Companies

Nutraceutical Manufacturers

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (FDA, USDA)

Banks and Financial Institutions

Companies

Players Mentioned in the Report

Amway

Bayer AG

BASF SE

Procter & Gamble

GNC Holdings, LLC

Herbalife International of America, Inc.

NOW Foods

Nature's Bounty

Glanbia PLC

The Bountiful Company

Table of Contents

1. U.S. Bone and Joint Health Supplements Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. U.S. Bone and Joint Health Supplements Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. U.S. Bone and Joint Health Supplements Market Analysis

3.1. Growth Drivers

3.1.1. Aging Population

3.1.2. Rising Prevalence of Bone-Related Disorders

3.1.3. Increasing Health Awareness

3.1.4. Advancements in Supplement Formulations

3.2. Market Challenges

3.2.1. Regulatory Hurdles

3.2.2. High Competition

3.2.3. Consumer Skepticism

3.3. Opportunities

3.3.1. Emerging Natural and Plant-Based Supplements

3.3.2. Expansion into E-commerce Channels

3.3.3. Personalized Nutrition Trends

3.4. Trends

3.4.1. Adoption of Gummies and Chewable Supplements

3.4.2. Integration of Probiotics for Bone Health

3.4.3. Increased Use of Collagen-Based Products

3.5. Government Regulations

3.5.1. FDA Guidelines on Dietary Supplements

3.5.2. Labeling and Health Claims Regulations

3.5.3. Good Manufacturing Practices (GMP) Compliance

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape

4. U.S. Bone and Joint Health Supplements Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Vitamins

4.1.2. Minerals

4.1.3. Collagen

4.1.4. Omega-3 Fatty Acids

4.1.5. Glucosamine-Chondroitin

4.2. By Formulation (In Value %)

4.2.1. Tablets

4.2.2. Capsules

4.2.3. Powders

4.2.4. Softgels

4.2.5. Gummies

4.3. By Consumer Group (In Value %)

4.3.1. Infants

4.3.2. Children

4.3.3. Adults

4.3.4. Pregnant Women

4.3.5. Geriatric Population

4.4. By Sales Channel (In Value %)

4.4.1. E-commerce

4.4.2. Brick-and-Mortar Stores

4.4.3. Direct Selling

4.4.4. Pharmacies

4.4.5. Health Food Shops

4.5. By Region (In Value %)

4.5.1. Northeast

4.5.2. Midwest

4.5.3. South

4.5.4. West

5. U.S. Bone and Joint Health Supplements Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Amway

5.1.2. Bayer AG

5.1.3. BASF SE

5.1.4. Procter & Gamble

5.1.5. GNC Holdings, LLC

5.1.6. Herbalife International of America, Inc.

5.1.7. NOW Foods

5.1.8. Nature's Bounty

5.1.9. Glanbia PLC

5.1.10. The Bountiful Company

5.1.11. Nestl Health Science

5.1.12. Reckitt Benckiser Group

5.1.13. Pfizer Inc.

5.1.14. Abbott Laboratories

5.1.15. Archer Daniels Midland Company

5.2. Cross Comparison Parameters (Number of Employees, Headquarters, Inception Year, Revenue, Product Portfolio, Market Share, R&D Investment, Distribution Channels)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.6.1. Venture Capital Funding

5.6.2. Government Grants

5.6.3. Private Equity Investments

6. U.S. Bone and Joint Health Supplements Market Regulatory Framework

6.1. FDA Regulations on Dietary Supplements

6.2. Compliance Requirements

6.3. Certification Processes

7. U.S. Bone and Joint Health Supplements Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. U.S. Bone and Joint Health Supplements Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Formulation (In Value %)

8.3. By Consumer Group (In Value %)

8.4. By Sales Channel (In Value %)

8.5. By Region (In Value %)

9. U.S. Bone and Joint Health Supplements Market Analysts Recommendations

9.1. Total Addressable Market (TAM), Serviceable Available Market (SAM), Serviceable Obtainable Market (SOM) Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The research begins by mapping the U.S. Bone and Joint Health Supplements Market, identifying all major stakeholders, and gathering relevant market data. This step involves extensive desk research using secondary and proprietary sources to outline key factors driving the market.

Step 2: Market Analysis and Construction

This stage entails analyzing historical data, segmentation, and market dynamics, with specific focus on consumer demand patterns, distribution channels, and competitive landscape. Data reliability is ensured through a comparison of multiple data points across various sources.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are tested through consultations with industry experts via interviews and surveys, which provide first-hand insights into emerging trends, challenges, and opportunities.

Step 4: Research Synthesis and Final Output

Final insights are synthesized, factoring in consumer behaviors, technological advancements, and regulatory impacts. This comprehensive analysis forms the foundation for actionable recommendations tailored to the U.S. Bone and Joint Health Supplements market.

Frequently Asked Questions

01 How big is the U.S. Bone and Joint Health Supplements Market?

The U.S. Bone and Joint Health Supplements Market is valued at USD 3.2 billion, driven by the increasing prevalence of bone-related conditions and consumer interest in preventive healthcare.

02 What are the main drivers of the U.S. Bone and Joint Health Supplements Market?

Key drivers in U.S. Bone and Joint Health Supplements Market include an aging population, high prevalence of osteoporosis and arthritis, and rising consumer awareness of preventive care for bone and joint health.

03 Who are the major players in the U.S. Bone and Joint Health Supplements Market?

Leading companies in U.S. Bone and Joint Health Supplements Market include Amway, Bayer AG, BASF SE, Procter & Gamble, and GNC Holdings, who have a strong market presence due to extensive distribution networks and innovative product portfolios.

04 What challenges does the U.S. Bone and Joint Health Supplements Market face?

The U.S. Bone and Joint Health Supplements Market faces challenges such as stringent regulatory requirements, high competition, and consumer skepticism regarding supplement efficacy.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.